As someone who views corporate finance through a pragmatic lens, I’ve been closely watching the current surge in capital expenditures (capex) tied to artificial intelligence (AI). The question I’m addressing here is this: when a company spends massive amounts of free cash flow and takes on increasing debt, in this case for AI CapEx, does that lead to a positive outcome for investors? The short answer is that the answer is sometimes yes, but only under particular conditions. If those conditions are not present, the result can be negative. In this post, we will explore the historical context, provide examples, discuss the associated risks, and offer guidance on navigating the current environment.

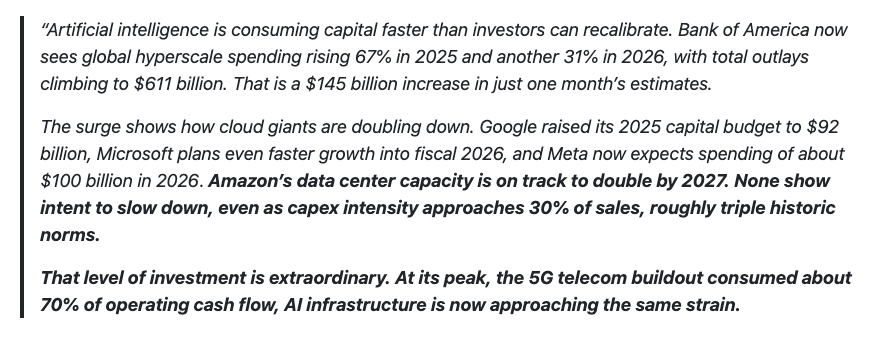

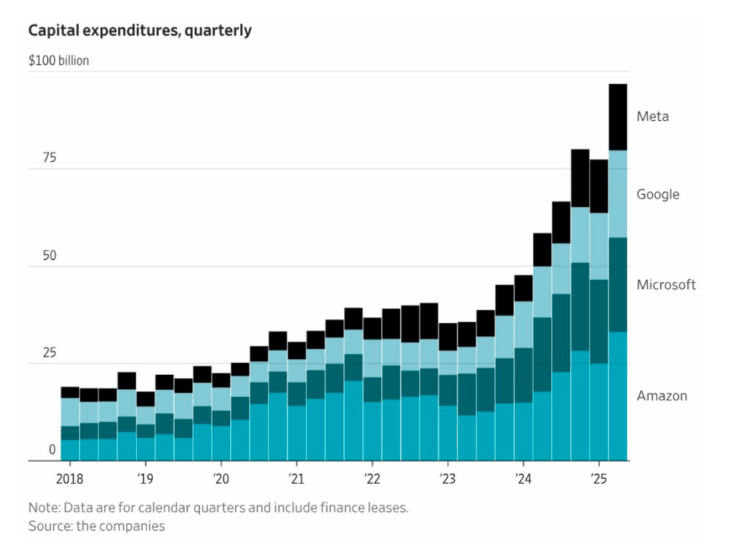

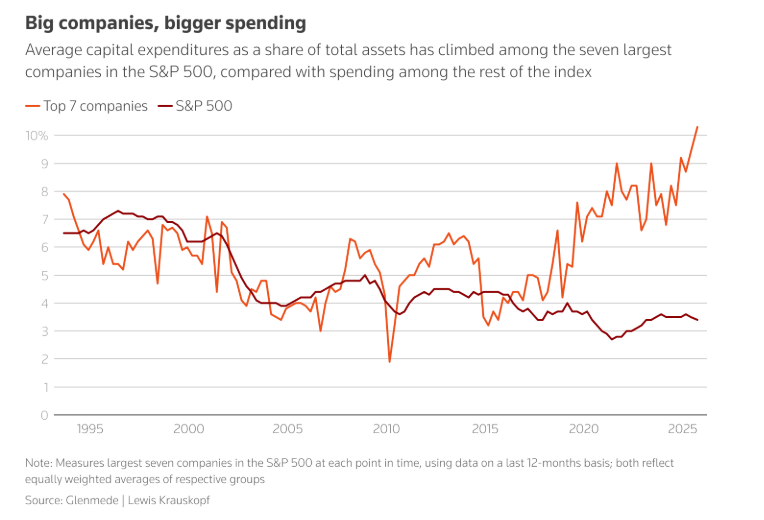

In a recent post, we discussed how the surge in capital expenditures (CapEx) by the largest U.S. companies has been nothing short of extraordinary.

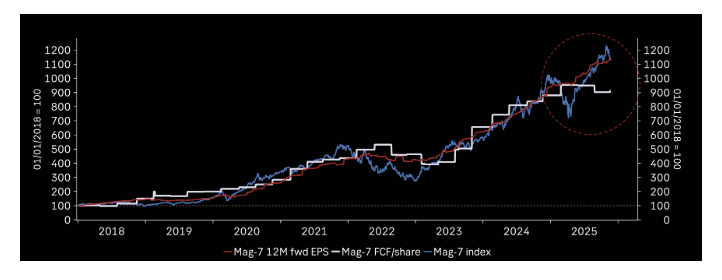

The question, of course, is whether these massive CapEx investments provide adequate financial returns. So far, earnings for the “Magnificent 7” have continued to rise, despite a stagnation in free cash flow due to these massive capital expenditures.

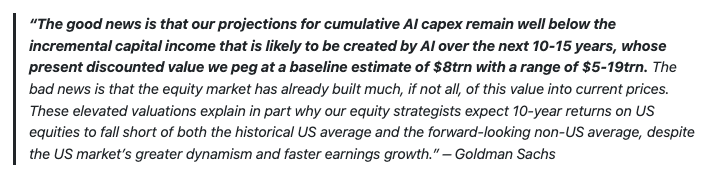

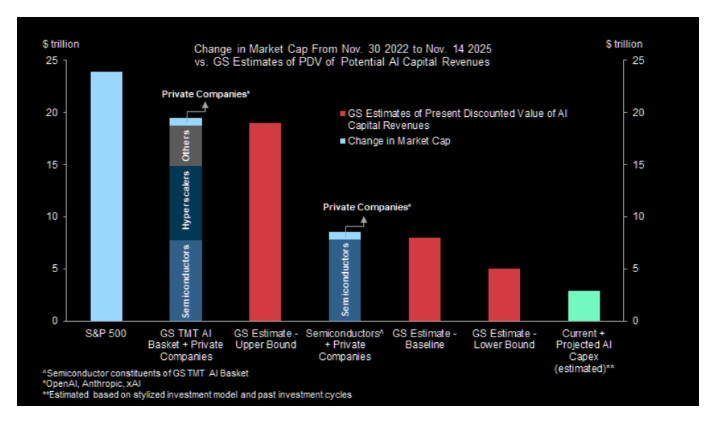

As noted recently by Sparkline Capital, Bain Capital estimates that, to justify their cost, these data centers will need to generate $2 trillion in annual revenue by 2030. Yet, three years after ChatGPT’s launch, AI revenues remain modest, estimated at $20 billion. In other words, revenues need to grow 100-fold to justify the expected buildout. Furthermore, enterprises have struggled to implement AI, and even ChatGPT, the most popular AI consumer application, has yet to fully monetize its users.

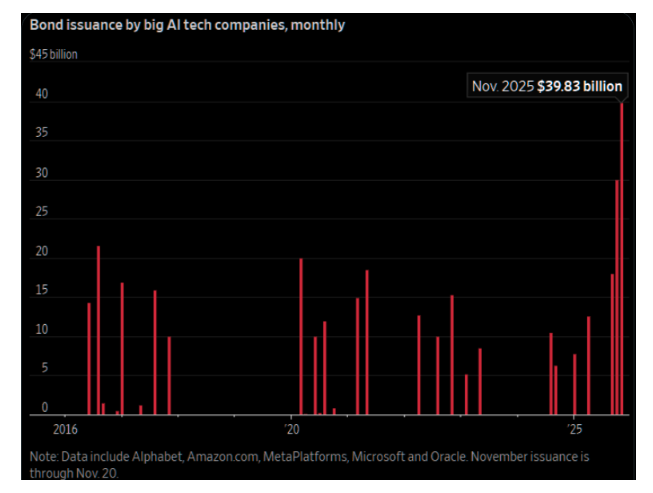

Simultaneously, as free cash flow stagnates, companies are turning to the debt market for the funding they need to meet their AI CapEx requirements.

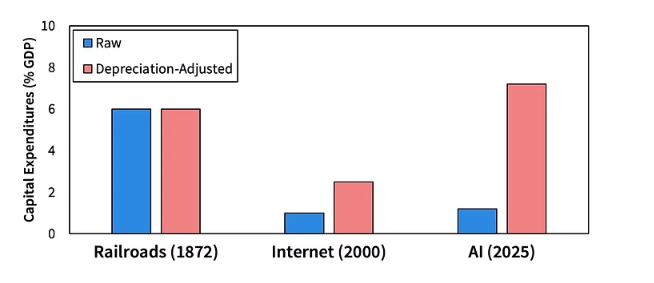

However, while the current CapEx expenditures seem high, the fundamentals of the companies engaged in artificial intelligence are vastly different than those during the “Dot.com” mania. But even in this case, it does not mean there is no risk in the financial markets.

History can also provide us with some clues as to what is most likely to happen next.

The Historical Capex and Free-Cash-Flow Relationship

Historically, companies have funded investment spending primarily from internally generated funds. In the three decades preceding the 2001 recession, U.S. firms allocated approximately 6 percent of their assets to capital expenditures (capex) and around 89 percent of their cash flow to capex, on average. That close link began to break down after 2000, and by 2015, CapEx had fallen to approximately 4.5 percent of assets, and has now fallen to 3.5%. It is worth noting that historically, the capital expenditure (CapEx) spending by the top-7 companies has mostly correlated with the rest of the economy. However, this correlation changed with the onset of the COVID pandemic, when companies shifted to increase profitability and productivity through technology to offset the economic shutdown’s impact.

From academic research, the relationship between free cash flow and capital investment is not uniformly positive. One study found that capital spending is directly associated with the size of free cash flow. Another found that leverage, or debt, has a negative association with future CapEx. Specifically, a 1-point increase in the debt-to-assets ratio reduced capital expenditures relative to assets by approximately 0.07 points. What this tells us is that a company with healthy free cash flow is better positioned to invest. But increasing debt may act as a drag on investment if not paired with a strong opportunity. Capex only adds value when it leads to incremental returns above the cost of capital.

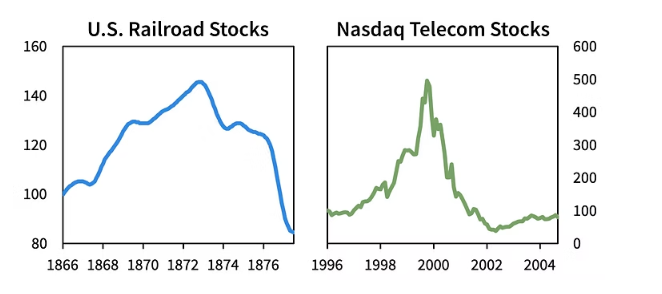

That is currently the hope of the market; however, prior cycles of heavy investment may tell a different story. As Sparkline noted:

Then, during the late 1990s, the telecom and IT sector expanded rapidly. Firms built infrastructure, laid fiber, and rolled out broadband. But many of those investments didn’t generate the expected returns. Some companies incurred heavy debt, and when demand growth failed to meet expectations, they faced write-downs and restructuring.

These two examples illustrate the risk that spending without commensurate returns destroys shareholder value. If demand is ultimately unable to keep up with the influx of new supply coming online, it will cause prices to crater and saddle firms with years of excess capacity. Corporate values collapse, with those that took on debt to finance the buildout facing the risk of bankruptcy.

The current AI CapEx wave is arguably larger than both of those previous examples. If the revenues materialize as expected and demand exceeds supply, those who invested in the space early will be the primary beneficiaries. However, that is the basis of all investing: measuring risk versus opportunity.

Risk Or Opportunity?

What are the risks and opportunities of spending large amounts of free cash flow and increasing debt levels?

- There is the risk of capital allocation without return. AI CapEx is only worthwhile if it produces a return above the cost of capital. Academic work affirms that capital expenditures have a positive effect on firm value only if they are profitable. If the investment yields sub-par returns, value is destroyed.

- Increasing leverage reduces future investment flexibility. Research reveals a strong negative correlation between leverage and future capital expenditures. Firms with greater debt invest less. In the AI context, if a company borrows heavily to finance capex, it may have less capacity to adjust or redeploy capital when conditions change.

- There’s the risk of free cash flow saturation. When firms commit large proportions of FCF to capex, they reduce or eliminate funds available for dividends, buybacks or other shareholder returns. One market comment warned investors to be wary of companies whose capital spending is growing faster than revenue, especially if they’re issuing debt to finance expansion.

- Timing the investment cycle poorly can have consequences. If capex coincides with the top of a cycle, firms risk entering periods of lower demand and lower asset utilization. The correlation between capital expenditures (capex) and cash flows dropped significantly after 2000, indicating that many firms are spending without a clear anchor to actual earnings or liquidity.

- Execution and monetization risk. Spending on AI infrastructure doesn’t guarantee revenue or profit. One study introduced the Capability Realization Rate model, which highlights valuation misalignment when expectations exceed realized performance. There is a risk that investments may not be monetized or that competitive advantages may disappear.

Despite those risks, there are conditions under which opportunity thrives. The questions that investors must answer correctly are:

-

Does the firm have a clear investment opportunity? If AI infrastructure enables a hyperscaler to expand its addressable market or materially improve margins, then the return on capital can exceed the cost.

- Is free cash flow coverage sufficient? If the firm uses free cash flow rather than only debt to fund the capex, financial strain is lower.

- Are debt levels moderate and manageable? If growth is strong and debt is controlled, using leverage to accelerate growth is rational.

- Does the company have execution capability and a clear monetization path? Without this, the spending becomes a liability.

- Does CapEx align with shareholder return expectations? If the company balances future growth with returning capital to shareholders, then value is more likely to accrue.

For most of the Magnificent-7 companies, most of those answers are “yes.” However, the question of a “clear monetization path” remains unclear.

I believe that we are still in the early stages of the current cycle, but many risks could negatively impact returns in the future. As such, we should consider a set of actionable guidelines as we participate in the current market.

- Focus on firms with disciplined capex and clear ROI. Prioritize companies that articulate a credible path from capital expenditures to incremental cash flow and have historically generated high returns on invested capital. Avoid firms that are simply raising debt, spending aggressively, but lacking clear revenue targets or margin expansion.

- Check the debt liberalization. Assess the debt levels, interest coverage, and maturity profiles. If a firm is issuing large amounts of debt while FCF is stagnant or declining, that is a warning sign. For example, commentary noted that major tech firms “are using debt” to fund both capex and buybacks concurrently.

- Monitor free cash flow coverage of capex. Determine what proportion of FCF is being used for capex (and debt servicing). If FCF is fully absorbed into capital expenditures, leaving nothing for dividends, buybacks, or debt reduction, risk is elevated.

- Screen for early‑stage misalignment. Use the CRR framework: are valuations based on near‑term returns, or purely on slender hopes? Academic research shows markets reward the “potential” but punish when returns don’t materialise.

- Consider the macro backdrop. In a tightening interest rate environment, debt financing becomes more expensive; asset utilization may also be challenged if demand growth slows. Some research suggests that the correlation between capital expenditures (capex) and cash flow declines during weak economic cycles.

- Balance growth and value orientation in your portfolio. If you are investing in high-capex companies, ensure that a portion of your portfolio also includes more conservative firms that return cash to shareholders, thereby reducing overall portfolio risk.

The current AI CapEx wave represents one of the most significant investment cycles in recent decades. However, significance does not guarantee success, and heavy spending of free cash flow and elevated debt levels must lead to value creation. Those massive investments must yield returns, debt must remain manageable, and cash flows must support those expenditures. Without such results, it can erode value and expose you to downside risk.

You, as the investor, must assume the role of financial disciplinarian. The direction is promising, but the execution will be critical. There are clearly risks present, and, as such, it is crucial to remain disciplined, measure carefully, and allocate risk accordingly.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice