Mohit Mittal Explores Why Core Bonds Are Compelling Investments Today

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary:

- Elevated yields, steeper yield curves, and ongoing volatility make core bonds a compelling choice for total return, income, diversification, and downside risk mitigation in today’s markets.

- Active management is key: Historically, it has helped core bond portfolios outperform passive strategies – according to Morningstar data1 – through a rigorous, diversified approach.

- In a target-rich environment marked by global dispersion and macro volatility, active managers can seek to unlock repeatable sources of return – turning fixed income from a static allocation into a dynamic edge.

Fixed income investing used to consist solely of buying bonds, holding them to maturity, and earning coupon payments. More than 50 years ago, PIMCO was born out of a radical idea: Why not actively trade bonds – taking advantage of price movements and valuation discrepancies over time – to maximize total returns by combining income with capital appreciation? The idea took off and the modern, more liquid bond market came into existence. In the ensuing decades, the PIMCO Total Return Fund, under the stewardship of bond investing pioneer Bill Gross, became an exemplar of seeking outperformance through active management.

Today, it can feel like markets have come full circle. Many investors have been drawn into passive fixed income allocations, such as index-tracking funds and private investment grade (IG) credit, that look more like the buy-and-hold bond investing of half a century ago. This full-circle turn has been accompanied by a false narrative that there is no alpha potential – or excess returns beyond the broader market’s performance – in liquid, public fixed income markets. The reality: Data continue to show consistent alpha in fixed income2, and active management of core bonds is a potent way to harness this potential.

Here, Mohit Mittal, who manages the PIMCO Total Return Fund with Dan Ivascyn, Qi Wang, and Mike Cudzil, discusses how the investment team is positioning the fund in the current environment.

Q: Why own core bonds today?

Mittal: For years, ultra-low core bond yields pushed investors toward equities and higher-risk credit. But the tide has turned. With the Bloomberg U.S. Aggregate Index yielding more than 4%, core bonds offer compelling value – especially as equity and credit valuations look stretched.

Steeper yield curves create opportunities for higher total return through roll-down. Diverging growth and inflation trends across global economies present intriguing relative value opportunities. We’re also seeing signs of late cycle dynamics, such as isolated credit-related issues among some lower-quality borrowers.

As the economy slows and volatility rises, core bonds provide high quality yield exposure, potential for attractive income, and diversification from the risks of equities and lower-quality credit assets. Core bonds’ higher starting yields currently also offer an enticing value proposition relative to cash for those investors willing to accept the investment risk. This means investors can target returns from a high-quality core allocation that also helps mitigate the downside of more risk-asset heavy portfolios.

Investors have been asking whether they’ve missed the window. But even as core bonds have delivered more than 4.5% annualized over the past three years (represented by the Bloomberg U.S. Aggregate Index as of 30 November 2025), the opportunity isn’t gone, in our view. Yields today on core bonds are nearly the same as they were three years ago. With additional Federal Reserve interest-rate cuts likely ahead and the 10-year U.S. Treasury hovering around 4%, investors can lock in attractive yields and benefit from potential price appreciation. Also, as inflation cools and growth slows, core bonds are well-positioned to outperform in risk-off environments – offering both the potential for income and diversification.

Q: Why should investors choose PIMCO for their core bond allocation?

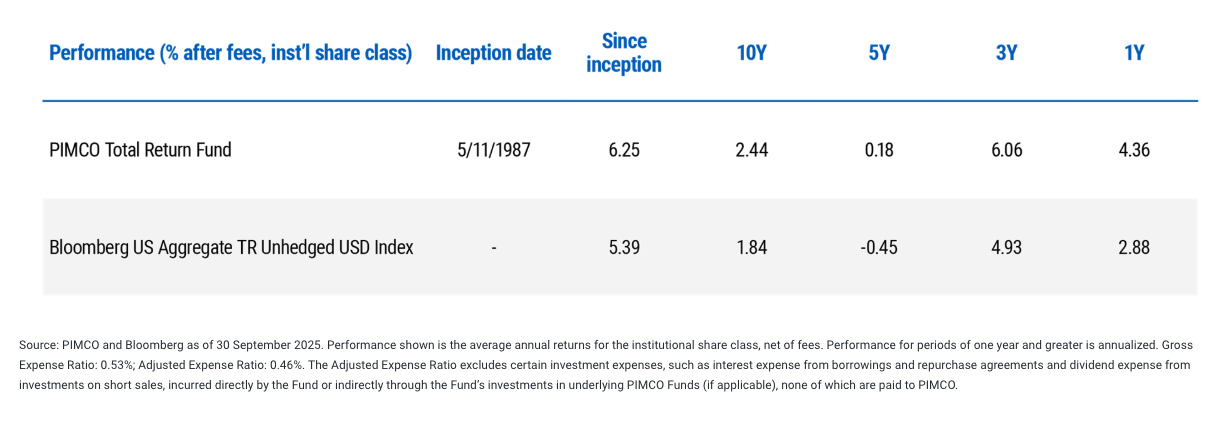

Mittal: Passive funds may be cheaper than active funds, but they may miss the mark in a market full of inefficiencies. The PIMCO Total Return Fund (institutional share class, after fees) delivered 5.96% in annualized returns, and importantly 466 basis points of cumulative alpha, over the three years ending on 30 November 2025. That is money that passive investors may have left on the table.

Our edge? A time-tested, fully integrated process that taps into insights from macro strategists, specialty desks, and credit research teams. We combine top-down macro views, rigorous risk management, and bottom-up relative value selection across global rates, securitized assets, corporates, and emerging markets.

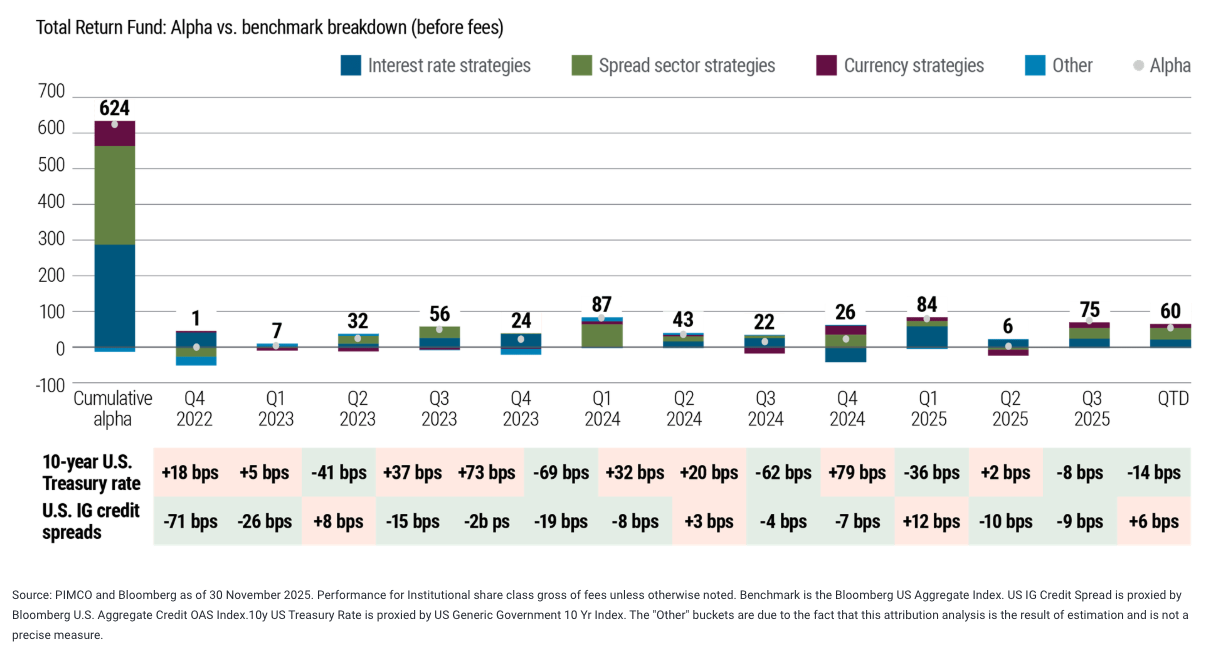

Our differentiator is a scenario-based investment framework that emphasizes diversification and systematic exploitation of market inefficiencies. This allows our portfolio managers to seek to generate alpha from multiple diversified and repeatable sources while limiting correlation with market movements (see Figures 1 and 2). In our view, if clients are paying active fees, they should seek true alpha – not simply more beta – to provide equity diversification to their portfolios.

Figure 1: PIMCO Total Return Fund alpha breakdown vs. benchmark highlights active management approach

Figure 2: PIMCO Total Return Fund performance, net of fees (insitutional share class)

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit www.pimco.com or call 888.87.PIMCO.

Through 30 November 2025, the PIMCO Total Return Fund returned 18.96% over the past three years (cumulative, after fees, institutional shares), outperforming its benchmark by 4.66 percentage points. Over that period marked by elevated volatility and uneven peer performance, the Fund outpaced the Morningstar Core-Plus Bond category average by 262 bps (cumulative, after fees, institutional shares), according to Morningstar. As of 30 November 2025, the Fund (institutional class shares) was ranked by Morningstar in the 3rd percentile over the 1-year period, the top quartile over the 3-year period, and the second quartile over the 5-year and 10-year horizons.3

Past performance looks compelling, but we believe the future opportunity remains very exciting as well: We anticipate continued strength in active core bond strategies. Starting yields remain elevated relative to the past decade. Diverging monetary and fiscal policies create relative value opportunities in both developed and emerging economies. Macro and market volatility drives dispersion across fixed income markets. All of these factors contribute to a target-rich environment for active bond managers to source alpha.

Q: How are you structuring portfolios to take advantage of opportunities today?

Mittal: We aim to deliver strong risk-adjusted total returns through diversified sources of alpha:

- Yield curve and duration: We regularly shift allocations across maturities to accommodate evolving views and market conditions. While we continue to favor short and intermediate maturities, we have used the recent steepening in the yield curve to reduce our yield curve steepener trade. Similarly, we regularly adjust duration, a gauge of price sensitivity to interest rates moves that’s typically higher in longer-dated bonds.

- Global investments: We actively adjust bond exposures in specific countries and regions as they become more or less attractive over time – a particularly useful tool in a year of trade turbulence and a decline in the value of the U.S. dollar (for more, see our latest Secular Outlook, “The Fragmentation Era”). We currently favor 30-year Japanese bonds, 10-year Australian bonds, and 5- and 10-year U.K. bonds.

- Credit: Corporate credit spreads are tight both by absolute historical standards and relative to other fixed income asset classes. We favor a significant underweight to benchmark levels in corporate credit risk, preferring exposure to other higher-quality spread areas such as agency mortgages and structured products. At the same time, intensifying capital needs related to AI data centers and energy demand offer unique opportunities to structure high quality transactions at a healthy premium relative to tight generic corporate credit spreads.

- Mortgages: Mortgages remain among our higher-conviction views. While targeting a high aggregate overweight to mortgages, we have remained tactical in scaling our exposure – notably using the market weakness in April 2025 to increase exposures further, before reducing more recently.

- Structured products: Detailed data analysis and modeling can help identify attractive opportunities based upon resilient consumer credit and real estate collateral across various structured products. Leveraging PIMCO’s vast data and credit analytics, we continue to see significant value in certain segments of securitized credit such as non-agency mortgage-backed securities and collateralized loan obligations, where we emphasize senior positions in the credit structure.

- Currencies: During this “Fragmentation Era,” we are likely to see growing divergence in economic trajectories and central bank paths as well as trade, capital, and portfolio flows. This increases volatility across currencies, thereby further providing opportunities to add value relative to passive strategies.

Q: Why is active management particularly suited to bond markets?

Mittal: Many fixed income investors – such as central banks and insurance companies – are driven by non-economic factors rather than risk-adjusted total return. They operate within rigid regulatory parameters and often prioritize broad market exposure over relative value – enabling active managers to target more of those opportunities. Similarly, passive managers often invest and rebalance systematically, and active managers may be able to capitalize on distortions created by these passive investment patterns.

The complexity of bond markets makes index replication challenging. Unlike equities, bonds mature, creating constant turnover. Bond indexes also assign the highest weights to issuers with the most debt outstanding, not necessarily those with the best economic value.

Additionally, many fixed income securities incorporate an added layer of complexity, liquidity, and volatility premiums, which require a depth and breadth of resources to appropriately model and analyze – creating further structural opportunities for active management. Structural alpha, achieved by identifying repeatable market inefficiencies, remains a key tool for outperformance in active management.

Active management in core bonds also calls for robust macro, sector level, and security level research to identify medium-term themes as well as tactical opportunistic dislocations. Recent examples include active duration and yield curve management amid a shifting rate outlook, relative value across credit sectors in light of tariff uncertainty and AI investment, opportunities in mortgage markets following the bank failures of 2023, and currency-related opportunities amid global macro and policy divergence.

By combining structural, thematic, and opportunistic sources of alpha, active management seeks to deliver consistent outperformance versus passive strategies across market environments.

Q: How does private investment grade (IG) credit compare with core bonds?

Mittal: Private IG credit has gained popularity by offering higher potential returns than public IG credit. However, many investors may not be adequately compensated for the illiquidity and complexity of these strategies. In fact, the elevated starting yield and diversification properties in high quality core bonds can create notable value relative to private IG, given the compression in liquidity and risk premiums.

Public fixed income markets tend to offer robust, real-time liquidity that gives investors the flexibility to pivot to more attractive opportunities as they arise – to pursue active alpha instead of a buy-and-hold approach. Less liquid private investments should offer a premium to compensate investors for potential lost alpha and other opportunity costs (for more, see our July 2024 Economic and Market Commentary, “Navigating Public and Private Credit Markets: Liquidity, Risk, and Return Potential”).

We believe investors considering private IG allocations should use a relative value approach to find opportunities where the compensation justifies the additional illiquidity and complexity – which often isn’t the case as private markets get more crowded. Investors should also consider differences in credit quality between public and private markets (for more, see our September 2025 Investment Strategies article, “An Active Manager’s Lens Into Private Investment Grade Credit”).

Q: Any final thoughts?

Mittal: Investors today may want to consider selling shares of private corporate direct lending strategies (around NAV if possible) and replacing with high quality active public fixed income. Investors willing to accept additional risks could also consider stepping out of cash given the high likelihood of cash rates coming down. And it’s also worth recognizing the rich valuations in equities, as evident in high CAPE (cyclically adjusted price-to-earnings) ratios.

On the other hand, high starting yields in high quality, liquid, public fixed income create a compelling opportunity for investors to lock in today’s yields and diversify exposures away from riskier assets, particularly amid early signs of late cycle dynamics.

However, not all core bond strategies are created equal. Active management is imperative in our view to navigate complexity, capitalize on liquidity opportunities, and unlock differentiated sources of return – turning fixed income from a static allocation into a dynamic advantage that can result in the potential for attractive investment returns. Elevated yields, persistent macro volatility, and global dispersion create a target-rich environment for strategies such as the Total Return Fund to seek structural, repeatable alpha through diversified sources.

Investors should consider the investment objectives, risks, charges and expenses of the funds carefully before investing. This and other information are contained in the fund’s prospectus and summary prospectus, if available, which may be obtained by contacting your investment professional or PIMCO representative or by visiting www.pimco.com. Please read them carefully before you invest or send money.

Footnotes

1 Based on Percentage of active funds within the Intermediate Core Bond, Intermediate Core Plus, Global Bond (USD hedged) and High Yield Bond categories that outperform the average passive fund on a 10-year return basis, according to Morningstar Direct data as of 30 September 2025. For each category we use the U.S. ETFs and U.S. Open-End Funds (institutional shares only). To avoid potential survivorship bias, we included funds and ETFs that were live at the beginning of each sample period but were liquidated or merged before the end of the period. ↩

2 87% of Intermediate Core and Core-Plus funds have outperformed their benchmark over a 10-year period, according to Morningstar Direct data as of 30 September 2025. Based on Morningstar U.S. Fund categories (Institutional shares only and net of fees). Combines the Morningstar U.S. Fund Intermediate Core and Core-Plus categories. ↩

3 Monthly Morningstar Ranking for PIMCO Income Fund Institutional Class 1 Yr 11 out of 523 funds, 3 Yrs 73 out of 490 funds, 5 Yrs 147 out of 450 funds and 10 Yrs 126 out of 325 funds as of 11/30/2025 based on total returns. Category: Core-Plus Bond.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results. The performance figures presented reflect the total return performance, unless otherwise noted, for the Institutional Class shares (after fees) and reflect changes in share price and reinvestment of dividend and capital gain distributions. All periods longer than one year are annualized. Periods less than one year are cumulative. The minimum initial investment for Institutional, I-2, I-3 and Administrative class shares is $1 million; however, it may be modified for certain financial intermediaries who submit trades on behalf of eligible investors.

Investments made by a Fund and the results achieved by a Fund are not expected to be the same as those made by any other PIMCO-advised Fund, including those with a similar name, investment objective or policies. A new or smaller Fund’s performance may not represent how the Fund is expected to or may perform in the long-term. New Funds have limited operating histories for investors to evaluate and new and smaller Funds may not attract sufficient assets to achieve investment and trading efficiencies. A Fund may be forced to sell a comparatively large portion of its portfolio to meet significant shareholder redemptions for cash, or hold a comparatively large portion of its portfolio in cash due to significant share purchases for cash, in each case when the Fund otherwise would not seek to do so, which may adversely affect performance.

Differences in the Fund’s performance versus the index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Fund and the index.

There is no assurance that any fund, including any fund that has experienced high or unusual performance for one or more periods, will experience similar levels of performance in the future. High performance is defined as a significant increase in either 1) a fund’s total return in excess of that of the fund’s benchmark between reporting periods or 2) a fund’s total return in excess of the fund’s historical returns between reporting periods. Unusual performance is defined as a significant change in a fund’s performance as compared to one or more previous reporting periods.

Monthly Morningstar rankings for the Institutional Class Shares; other classes may have different performance characteristics. The Morningstar Rankings are calculated by Morningstar and are based on the total return performance, with distributions reinvested and operating expenses deducted. Morningstar does not take into account sales charges. Waived fees or reimbursed expenses, if applicable, may affect rankings. Past rankings are no guarantee of future rankings.

© 2025 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

A word about risk: Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee there is no assurance that private guarantors will meet their obligations. Structured products such as collateralized debt obligations are also highly complex instruments, typically involving a high degree of risk; use of these instruments may involve derivative instruments that could lose more than the principal amount invested. High-yield, lower-rated, securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. Diversification does not ensure against loss.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

References to liquidity refer to normal market conditions.

Alpha is a measure of performance on a risk-adjusted basis calculated by comparing the volatility (price risk) of a portfolio vs. its risk-adjusted performance to a benchmark index; the excess return relative to the benchmark is alpha. Beta is a measure of price sensitivity to market movements. Market beta is 1. Correlation is a statistical measure of how two securities move in relation to each other. The correlation of various indexes or securities against one another or against inflation is based upon data over a certain time period. These correlations may vary substantially in the future or over different time periods that can result in greater volatility. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

Morningstar Category: Intermediate-term core-plus bond portfolios invest primarily in investment-grade U.S. fixed-income issues including government, corporate, and securitized debt, but generally have greater flexibility than core offerings to hold non-core sectors such as corporate high yield, bank loan, emerging-markets debt, and non-U.S. currency exposures. Their durations (a measure of interest-rate sensitivity) typically range between 75% and 125% of the three-year average of the effective duration of the Morningstar Core Bond Index.

Bloomberg U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis.

It is not possible to invest directly in an unmanaged Morningstar category or index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

PIMCO Investments LLC, distributor, 1633 Broadway, New York, NY, 10019 is a company of PIMCO.

Investment Products

Not FDIC Insured | May Lose Value | Not Bank Guaranteed

CMR2025-1204-5041252

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All