In the current installment of The Roundup,1 Oaktree experts explore the need for renewed vigilance in the direct lending market, discuss the future of private credit in Europe, identify the evolution of the high yield bond market, and reflect on the backdrop for emerging markets equities. Plus, we’ve included an excerpt from one of Howard Marks’s recent memos.

1. Market Outlook: Systemic or Systematic?

The well-publicized credit episodes of the last few months aren’t an indictment of the whole sub-investment grade debt market, or the whole private credit market. Rather, they’re just a reminder that the yield spreads people care about so much are there for a reason: because sub-investment grade debt entails credit risk. And thus a reminder that credit skills are always a necessity for debt investors . . . even if the need for those skills isn’t apparent in good times.

When times have been good for a while, the possibility of loss recedes from consciousness. Investors’ risk tolerance grows, and they tend to focus less on due diligence and more on bidding aggressively for deals. The result is a lowering of standards.

Nowadays, I’m often asked whether the recent episodes in sub-investment grade credit are “systemic.” In other words, are they “pertaining to the system” or “affecting the system,” as opposed to idiosyncratic occurrences that don’t say anything about the system. For an example of something systemic, consider the counterparty risk that arose during the Global Financial Crisis. Because financial institutions had entered into hedging transactions with each other, one bank’s weakness weakened the others, impacting the system overall.

I don’t think today’s issues are systemic in the sense that there’s something wrong with the lending system, or that they will trigger other defaults and lead to a breakdown of the system. In simpler words, there’s nothing wrong with the plumbing. But imprudent loans and business frauds often occur in clusters for the simple reason that people who make investments and loans are highly prone to error in good times. Investors and lenders are supposed to be risk-averse and thus exercise discipline and vigilance, but sometimes they fail in this regard. This isn’t part of the plumbing of the financial system but rather a regularly recurring behavioral phenomenon. So, it isn’t “systemic,” but it is “systematic.”

We’ve lived through generally good times in the last 16 years. The coming period is likely to be more “interesting,” as errors that were made in those good times come to light. On the other hand, the recent credit events have probably chastened lenders and investors, putting them on alert. Thus, they’re likely to incorporate a re-elevated level of prudence in their decisions in the coming months and perhaps years. This would be a positive development.

2. Direct Lending: Stay Disciplined

In the direct lending market, we’re beginning to see a divergence in deal flow between large-cap and middle-market sponsor-backed deals. This year has seen an increasing number of large-cap sponsors opting to finance deals in the cheaper broadly syndicated loan (BSL) market: 63% of LBOs larger than $1 billion have been financed in the BSL market so far in 2025, compared to 51% in 2024 and 39% in 2023.2 Alternatively, middle-market deal flow appears to have picked up meaningfully after the lull starting in 1Q2025. The volume of deals under consideration in the market today is above levels seen in the first half of the year, when policy uncertainty kept smaller sponsors sidelined.3

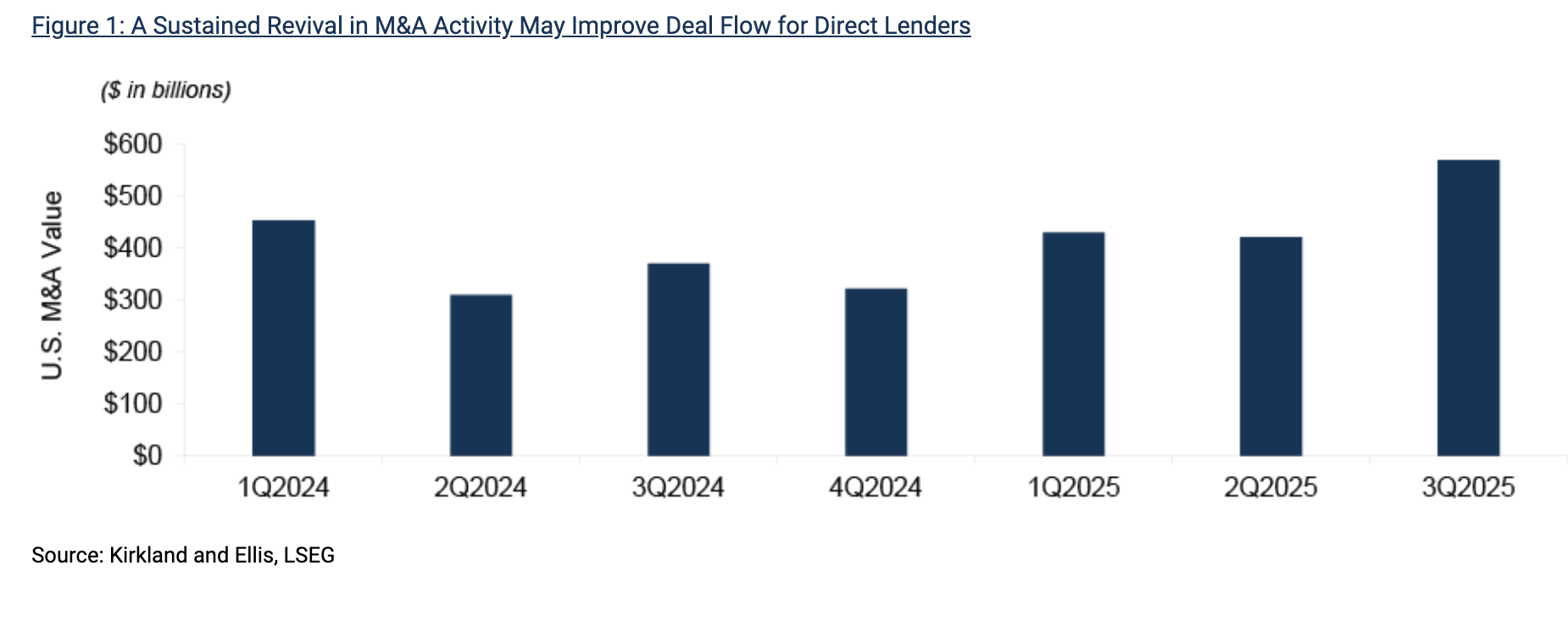

This increase hasn’t yet been enough to reverse the tightening of pricing we’ve seen in recent months. The large volume of dry powder available to business development companies and other lenders exemplifies a supply/demand imbalance that has pushed average spreads in middle-market deals down to around 450-475 bps over SOFR, only marginally above large-cap deals.4 That said, M&A activity has recently shown signs of positive momentum – if this trend continues into 2026, pricing could stabilize or even marginally widen. (See Figure 1.)

Prices remain tight and base rates have declined over the past year. Thus, the prospective risk-adjusted returns available in sponsor-backed direct lending today are lower than they were a year ago. We believe direct lending managers should stay disciplined, passing on opportunities where risk-adjusted returns fall short. To be clear, the direct lending market continues to offer higher prospective yields and stronger creditor protections relative to liquid credit markets, earning direct lending a pivotal role in a well-diversified portfolio.

3. European Direct Lending: Early Innings

We believe Europe is still early in its private credit journey, with significant growth ahead. Direct lending has risen to become a key financing pillar in Europe, but the region remains overly dependent on banks and likely to face significant private capital needs over the coming years. For investors, this may present the opportunity to tap into an inherently diversified and fundamentally solid credit market.

Specifically, growth drivers may include:

-

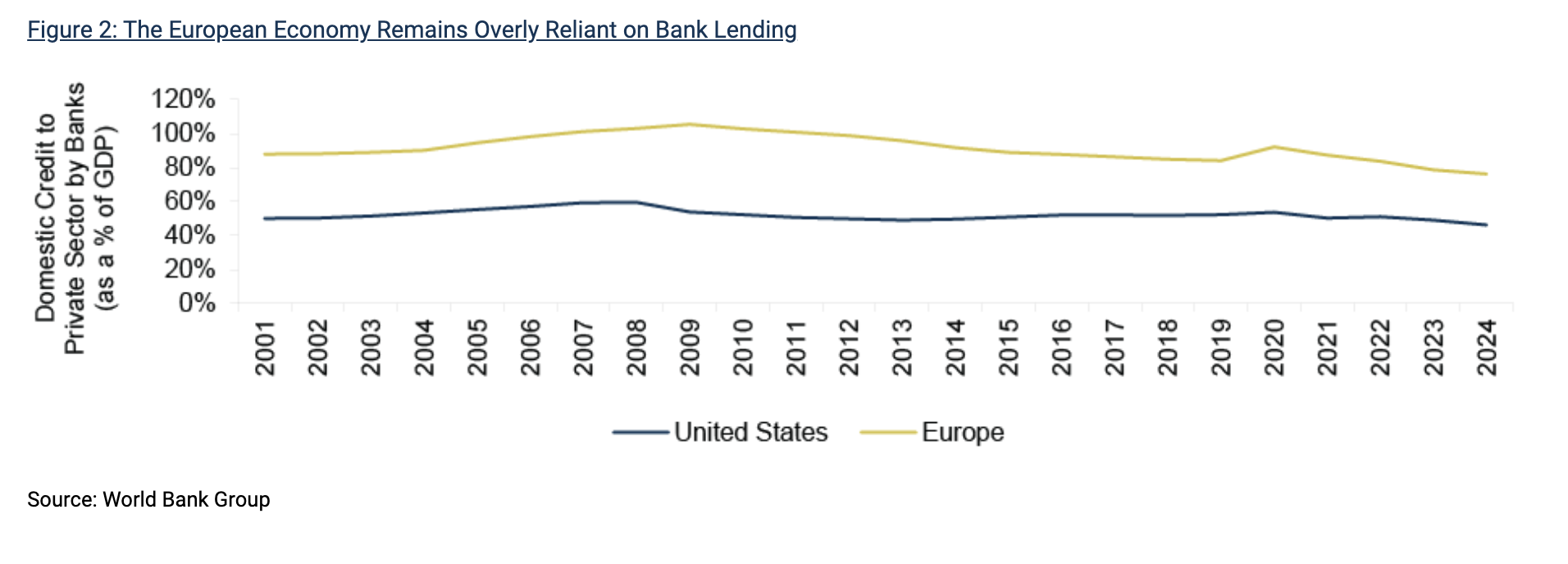

Fading reliance on banks: Traditional banking institutions still dominate European corporate lending. Banks’ provision of credit to the private sector constitutes over 75% of GDP in Europe, compared to less than 50% in the U.S. (See Figure 2.) At the same time, European banks are dealing with tough regulatory capital requirements, constraining their lending ability and pushing borrowers toward alternative lenders.

-

Impending private equity (PE) activity: There’s an exceptional volume of PE dry powder in Europe, far beyond current private credit dry powder.5 This indicates a meaningful leveraged buyout financing gap. The broadly syndicated loan market will likely fill some of the gap but won’t provide the flexible solution many borrowers require.

-

A supportive economic backdrop: Europe is set to benefit from a prolonged increase in government expenditure. This includes a core focus on bolstering its military and industrial bases following years of underinvestment, with Germany making the seismic decision to release its “debt brake.” This will bring a stimulative wave of capital expenditure, providing a handy tailwind to the European economy.

As the market continues to mature, we believe the primary focus is pivoting away from origination volume to sophisticated risk management. This is amplified by signs of cracks in private credit portfolios, with a dramatic rise in borrowers using payment-in-kind interest and some well publicized credit issues. We believe the keys to success in the next phase of European direct lending will be (a) rigorous risk control, (b) experience across multiple market cycles, and © localized but broad sourcing networks.

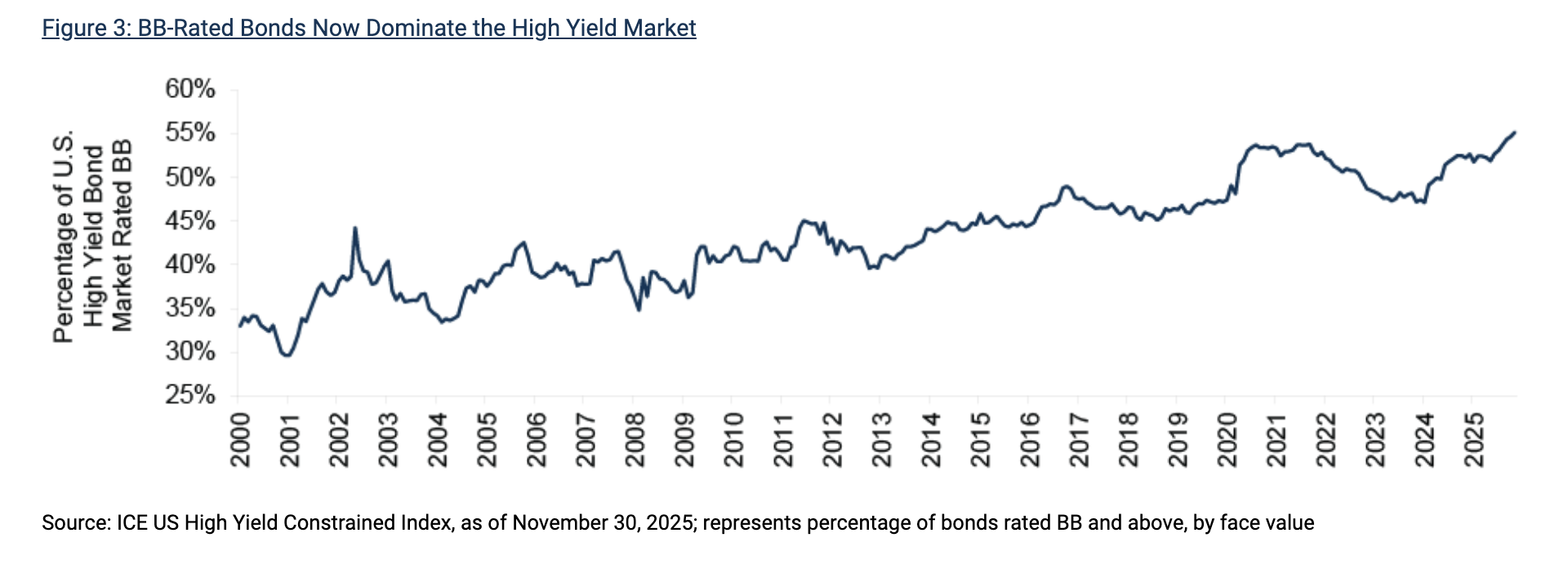

4. High Yield Bonds: Not Your Parents’ Market

The discourse on “tight high yield bond spreads” is both technically factual and potentially misleading. Spreads, at around 300 bps, aren’t much to shout about, but they must be considered against a high yield market that has dramatically risen in quality.6

Over 55% of the U.S. high yield bond market is now rated BB, the highest sub-investment grade credit rating. (See Figure 3.) That’s a record level, and around 10 percentage points more than it was a decade ago. Meanwhile, bonds rated CCC and below constitute 12.1% of the market, compared to the long-term average of 17.2%.7 In short, the high yield market is about as good quality as it has ever been.

Fallen angels (i.e., bonds downgraded from investment grade to high yield) also present a potentially favorable tailwind for the high yield market’s overall quality. Barclays anticipates $70-90bn of fallen angels in 2026, with a number of large BBB-rated bonds at risk of being downgraded and ultimately swelling the BB-rated portion of the high yield market.8

With quality up, defaults are down. The high yield bond default rate currently stands at 1.8%, compared to the post-GFC average of 2.5%.9 Simply put, that’s allowed high yield investors to enjoy more of their contractual returns. Moreover, more high yield bonds are now being issued in senior secured format, which may support greater recoveries for those bonds that default.

However, a higher-rated market doesn’t mean managers should relax their underwriting standards. Ratings aren’t a perfect guide to quality and avoiding defaults remains the name of the game. Get that right and the high yield market can present attractive contractual income with manageable credit risk.

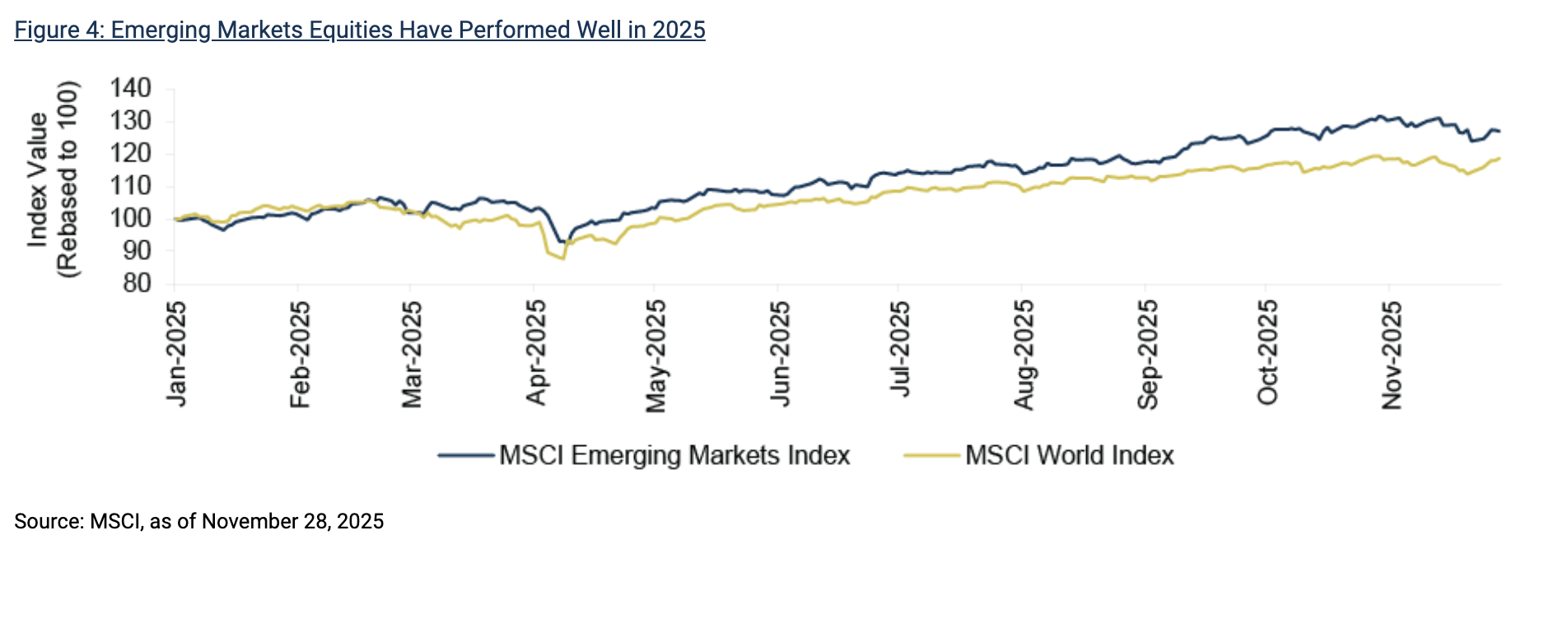

5. Emerging Markets Equities: EM Shines in 2025

Emerging markets (EM) equities rose during the third quarter and outperformed those in developed markets by a wide margin. This marked the third consecutive quarter of EM outperformance, a trend not seen since 2017.10 (See Figure 4.)

Key positive themes for the emerging markets include:

-

Commodities strength: EM commodity producers continue to benefit from high demand for precious and industrial metals. Gold prices reached a record level earlier this year, amid macroeconomic uncertainty. Meanwhile, supply discipline among copper and aluminum producers has supported a constructive pricing environment.

-

A weaker U.S. dollar: The dollar weakened by nearly 10% over the first three quarters of 2025, driving renewed investor interest in EM equities and benefitting EM issuers with outstanding USD-denominated corporate bonds.11

-

Financial resilience: We’ve noted the improving balance sheets and disciplined capital allocation of EM companies. Management teams have remained prudent regarding capital expenditure while simultaneously enhancing shareholder returns through dividends and buybacks.

China was the best-performing large market in the third quarter, buoyed by renewed optimism around U.S.-China trade relations, supportive policy measures, and continued AI enthusiasm. China has remained committed to transitioning its economy away from property dependence and toward more sustainable growth drivers such as innovation, consumption, and capital-market reform. This includes a focus on share buybacks, improved dividend policies, and better corporate governance. However, Chinese equities remain discounted, trading at roughly 12.7x forward earnings and 1.7x book value.12

At the end of September, the EM equities index was trading at 1.9x book value and 14.0x consensus forward estimated earnings, both of which are lower than those in the U.S. and all developed market equities.13 Fundamental bottom-up selection will remain critical, and they’ll likely be volatility along the way, but we believe we’re still in the early stages of a long-term emerging markets rally.

Endnotes

1 The content is derived from or inspired by ideas in recent letters, or other materials featuring or produced by Oaktree thought leaders; the text has been edited for space, updated, and expanded upon where appropriate.

2 Kirkland and Ellis, PitchBook LCD, September 30, 2025.

3 Kirkland and Ellis, Ontra: sell-side M&A NDAs from middle-market investment banks have meaningfully increased in number between 1Q2025 and 3Q2025, based on mandates processed by Ontra, an NDA automation platform.

4 Oaktree portfolio manager observations of recent deal flow.

5 Preqin.

6 ICE US High Yield Constrained Index, as of December 12, 2025.

7 ICE US High Yield Constrained Index, bonds rated CCC and below as a percentage of total market face value. Long-term average measured between January 2001 and November 2025.

8 Barclays, Rising star and fallen angel 2026 outlook, as of October 24, 2025.

9 JP Morgan Default Monitor, 12-month trailing default rate, as of December 1, 2025.

10 JP Morgan.

11 DXY Index.

12 MSCI China Index, as of November 30, 2025.

13 Bloomberg.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2025 Oaktree Capital Management, L.P.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Oaktree Capital Management

Read more commentaries by Oaktree Capital Management