When it comes to mergers and acquisitions (M&A), 2025 has seen the most activity and some of the strongest returns since the post-pandemic period when dealmaking soared. In our view, a mix of forces behind this year’s resurgence should lead to more opportunities in 2026.

There was reason for optimism when the year began, as we noted at the time. And a more predictable regulatory backdrop has certainly helped set the stage, leading to a stronger flow of deals, faster deal completions and fewer “deal breaks,” commonly caused by failure to get regulatory approval.

The HFRI Event Driven Merger Arbitrage Index was up 8.2% through the end of September this year, delivering the strongest first three quarters since 2021 and second best since 2009. As the year winds down, we’re also seeing stronger deal flow and solid returns for merger strategies globally, which we think bodes well for the year ahead.

Where 2025’s Strong Returns Came From

The recovery in merger activity came in a few waves. First, a more hands-off approach to regulation in the US and more openness to mergers in Europe and the UK set the tone.

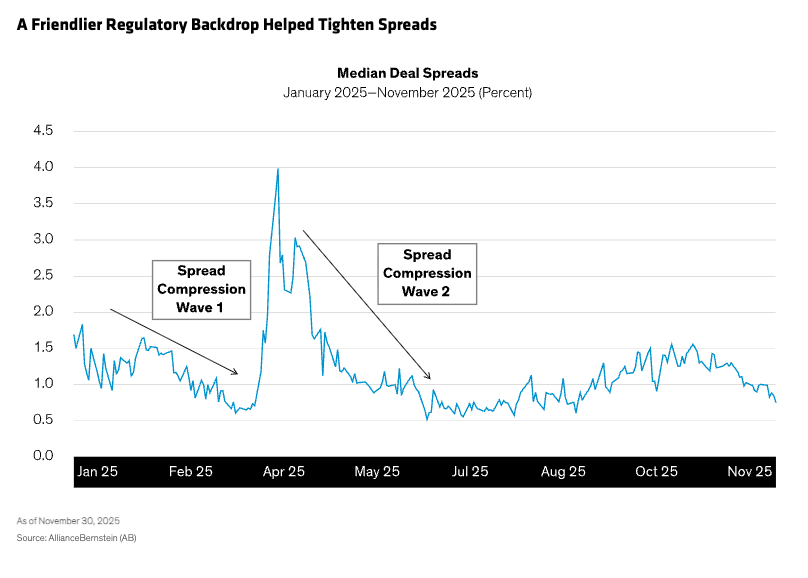

Early in the year, we saw spreads compress in deals carried over from 2024, when the regulatory environment was more challenging. The closing of this spread—the gap between the target company’s trading price and the deal payout value—created the first wave of returns for arbitrageurs.

The sudden announcement of a new US tariff regime triggered an April market downturn and briefly slowed deal-making activity. But the tumble in equity prices created a buying opportunity for merger-arbitrage investors, who were able to ride a second wave of spread-tightening and increased dealmaking into July (Display).

Meanwhile, deal flow—a key driver of merger-arbitrage performance—started to surge. With more deals coming to market and completing, arbitrageurs were able to realize higher returns in the period.

By the third quarter, the number of US deals worth more than $5 billion had risen some 166% compared to the same period in 2024. That included the ongoing merger between freight railroads Union Pacific and Norfolk Southern—the largest M&A deal in the last five years—as well as the deal for video game developer Electronic Arts, the largest take-private deal on record.

A lack of deal breaks—the primary risk merger arbitrageurs face—has been a critical driver, too. Compared to the long-run average, remarkably few deals collapsed, reducing what is often a sizable drag on merger-arbitrage performance.

Supportive Policy, Private Equity Firepower Bode Well for 2026

Will the story end when 2025 does? We don’t think so. Deal flow is a key driver of merger-arbitrage performance, and we expect it to remain strong heading into 2026. Here’s why:

The regulatory environment should remain supportive. The current US administration, which has embraced a lighter touch on regulation, has three more years to run. That’s enough runway for large strategic deals to get negotiated and announced. We expect to see more mergers in Europe and the UK, too.

Monetary policy may get a bit looser. This is most important in the US, where the majority of deal activity occurs. It’s likely to create more room for companies and private equity buyers who are financing deals with debt, allowing management teams to bid on previously unreachable targets.

Private equity firms are under pressure to deploy capital. These investors have substantial stockpiles that can be put to work. We think this suggests that leveraged buyouts will play a key role in deal-making in 2026.

Concern about high equity valuations could create some resistance—but not much, in our view. Many would-be buyers have significant cash reserves, and high valuations provide further opportunities for these firms to use their stock to make acquisitions.

Companies that have underperformed this year may be more tentative about stock-driven acquisitions. But some of these firms may also be attractive targets for others with the capital to pursue them. We think a reasonable correction in equity prices next year may create new buying opportunities and spur competition among buyers, given the favorable regulatory environment.

Parsing the Potential Risks to Merger Arbitrage

Headwinds in 2026 may come from spread compression as more arbitrage capital is deployed to take advantage of a favorable M&A environment. It’s also worth watching equity market valuations—if they stay high, some corporate boards worried about overpaying for companies may offer lower premiums or make fewer counterbids, which might reduce the strategy’s return potential. Geopolitical and regulatory risks should always be on investors’ radar, and we think deal flow may slow if inflation expectations rise and monetary policy starts to lean toward tightening.

Overall, though, we don’t expect to see significant dampening of the merger mood. We expect 2026 to be another strong year.

Eugene Smit is a Portfolio Analyst and Manager on the AB Hedge Fund Solutions (HFS) team within Multi-Asset.

Scott Schefrin is the Portfolio Manager of the AB Hedge Fund Solutions’ Systematic Merger Arbitrage strategy.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

References to specific securities discussed are for illustrative purposes only and should not to be considered recommendations by AllianceBernstein L.P. It should not be assumed that investments in the securities mentioned have necessarily been or will necessarily be profitable.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein