Summary

- Water can be a byproduct of oil and gas production that requires disposal, while fresh water is also needed to support hydraulic fracturing.

- Midstream companies collect fees for handling produced water and supplying water for fracking.

- Some companies with oil and gas gathering businesses also provide water services, while WaterBridge (WBI) is solely focused on water.

While often overlooked, water management plays an important role in oil and gas production. Oil wells typically produce more water than oil, while hydraulic fracturing (or fracking) requires water to be pumped into wells. Water infrastructure related to oil and gas production is considered midstream and is classified within gathering and processing.

Water infrastructure has been in greater focus lately given recent M&A activity and a significant initial public offering in the space. There is also growing chatter around the potential for recycled water to be used for cooling data centers supporting artificial intelligence.

What are water services and why are they needed?

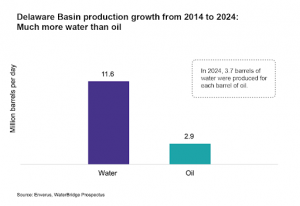

Beyond handling oil and natural gas, midstream companies can also transport, store, and process or recycle water. Water is a significant byproduct of oil and natural gas production and occurs naturally in reservoirs alongside oil and gas. Produced water describes the salty water that comes out of a wellbore. As shown in the chart below, produced water significantly outpaced oil production growth in the Delaware basin of the Permian from 2014 to 2024. The amount of water produced by wells can vary and can increase as a well ages.

Water is admittedly a headache for producers that need it to be removed from the well site to support continued production. Midstream companies take produced water from sites (usually using pipelines) and process the water to remove any oil, solids, or minerals. From there, the water can be disposed underground through injection wells, or it can be further processed for recycling. Recycled produced water can be used to support fracking operations. Skimmed oil may be resold.

Water also needs to be brought to well sites for fracking. Fracking entails pumping special fluid and proppant (sand) into a reservoir to support production from a well. The water required to frack a well can range from 1.5 million gallons up to 16 million gallons. In the Delaware basin, the water required for fracking is far more modest than the amount of water that can be produced.

In short, producers need “freshwater” for fracking wells, and they need produced water taken away and disposed. Producers pay midstream service providers to handle both these activities. Providing freshwater for fracking is more sensitive to upstream activity levels.

Who are the players?

Water services have garnered more headlines lately. WaterBridge Infrastructure (WBI) raised $677 million in its initial public offering in September. In October, MLP Western Midstream (WES) completed the acquisition of C-Corp Aris Water Solutions (former ticker ARIS), which was originally announced in August. The Aris acquisition expanded WES’s existing water business.

The water infrastructure for WES and WBI is predominantly focused on the Delaware basin, though WBI also has water assets in the Eagle Ford and Arkoma. Both are in the process of building new pipeline capacity to support disposal of produced water from the Delaware basin.

While WBI is solely focused on water, WES has traditional gathering and processing assets handling oil, natural gas, and natural gas liquids. NGL Energy Partners (NGL) predominantly makes money from water infrastructure in the Delaware basin but also has hydrocarbon assets. In Appalachia, C-Corp Antero Midstream (AM) has a significant water handling business, alongside traditional gathering and processing. Private companies are also involved in providing water services in producing regions. Deep Blue, owned by Diamondback Energy (FANG) and Five Point Infrastructure, provides water services in the Midland basin of the Permian.

How do they make money?

Contracts for water services can resemble traditional gathering and processing contracts with acreage dedications or minimum volume commitments (MVCs) covering a period of years. With an acreage dedication, a producer agrees to have a certain midstream provider handle all the output from an area (in this case produced water). With MVCs, customers agree to provide a minimum amount of volume over a period or pay to keep the provider whole if volumes are below the minimum.

For WBI, contracts typically have an initial term of 15 years and include annual fee escalators tied to inflation. WBI receives a fixed fee per barrel for handling produced water, and produced water handling accounts for 90% of the company’s revenue.

Going forward, there could be an opportunity for companies to take produced water, treat it, and sell it to data centers for cooling purposes. This would be attractive as produced water could be recycled for a value-added use, instead of simply disposed underground. In March, the Environmental Protection Agency (EPA) announced a review of regulations to support the reuse of produced water for other purposes, including data center cooling. While it is early days, this could be a compelling growth opportunity in time.

Bottom Line:

Water is key feature of energy production, both as an inconvenient byproduct and an essential input for fracking. Select midstream companies provide water services similar to a traditional gathering and processing framework.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

Originally published on ETF Trends

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi