I am not going to insult the intelligence of the reader by making a list of claims for the future, which is common theatre this time of year. “For folly that he wisely shows is fit; but wise men, folly-fallen, quite taint their wit” and Shakespeare and stuff. But we have 3600 or so words that digress as EM Forster noted, “How do I know what I think until I see what I say?”

It is very arguably much more helpful to review some of the “things that happened this year” and try to place that in context to improve future decision-making. The flaw in this logic, however, is that it is precisely and falsely easy to understand what happened within the context of what we know now. But what the hell did we know then? After all, everything that has already happened must have been inevitable.

For example, the world is now full of resident geniuses as to what will happen or not as far as Warner Brothers and whether it goes to Paramount or Netflix, and then what might happen in the world of entertainment content and its distribution. I can tell you after buying it back earlier this year in the single digits after the third year of taking tax losses at the end of 2024, that there were relatively few geniuses saying anything other than WBD was a dying collection of assets run by a grossly overpaid megalomaniac. An impressively aggressive young man and his gazillion dollar dad? A giant strategic U-turn from Netflix? The vagaries of FCC leans and the White House? Asset separations? A few hit movies? All scenarios with uncertain weights that in retrospect were difficult to weight, including certain buyers like the author who stubbornly saw cheap. (The mentionable postscript is that I have confirmed my status as an awful risk arbitrageur and sold in the low 20’s.)

What is to be learned other than to be humble in what you think you know about the past? There is a cognitive illusion makes the past seem orderly and predictable, which can be referred to as the “knew-it-all-along” effect.” I didn’t. But I like markers of “cheap and universally hated, a reason to be alive with 100 years of IP, an improving balance sheet, and lots of reasons to suspect something other than a nonzero probability of continued descent into equity hell.”

Other versions of this that come to mind? Emerging markets booming in 2025 and trouncing most US indices? There were plenty of scenarios — relative valuation and dollar depreciation being two — but you could have lost tens of billions and a few careers along the way waiting for it. The caveat to brilliant paper thought and process are the constraints of the real world is that something is less likely to happen unless someone is being paid to make it happen “nowish.” And that is why the change we often see in financial markets is non-linear and seems sudden, dramatic and explosive. Idea takeoff can be tortuously denied, and then, damn it, I wasn’t wrong those four years, I was just early.

Writing and philosophizing aside, the learning I am repeating to myself is constant employment of “scenarioizing,” avoiding the temporal sense of helplessness when things aren’t going according to “the plan,” an appreciation of conflicting time horizons, and appreciating the power of unexpected ideas and scenarios. Reemphasize baselines that consider what tends to happen more frequently and other things less frequently? Create idea diversity without the false precision of attaching mathematical probabilities? Understand what market pricing is sometimes telling you. And appreciate that the more you know, the deeper and darker your pool of foolery.

And with more to come later in the Letter, a use for AI tools? If one doesn’t expect absolute precision or the need for decision making, maybe hallucination outside of your own 4 corners is not a terrible exercise.

Hey, did I mention smallcap investing? We have had very solid relative and absolute performance this year vs almost anything but your favorite 3x leveraged crypto or Mag 5 ETF in our separately managed smallcap, and much less so in our concentrated LP, which was the reverse of 2024. Nothing more explanatory other than a wider boat can catch more tides, and not managing against an index with 7 investments can be fat and lumpy. For compliance’s sake, please reach out and we would be DELIGHTED to share.

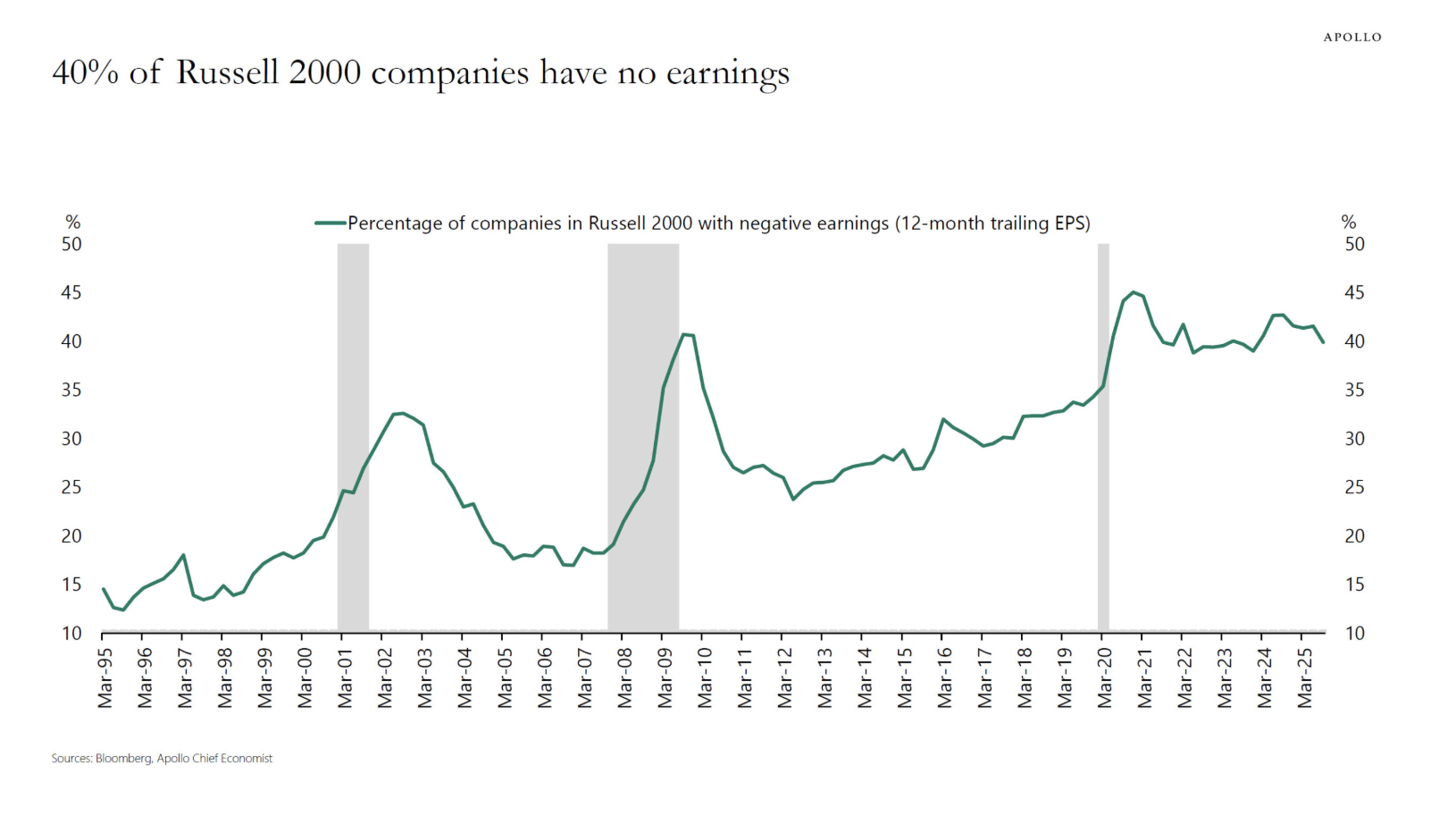

And finishing the commercial, this is the nothing new chart.

Thoughts:

- The Russell 2000 remains a terrible way to effect a “I think Cove Street is right – years of less capital in US public smallcap has created a fertile environment for the less discovered.”

- The S+P 600 is arguably a better index, but we have always used the Rusell and hate the snide eye properly cast when a manager changes indices for whatever reason.

- The crap will get worse if the SEC just opens the floodgates to “anyone” with new ideas on making it easier to go public. (https://www.sec.gov/newsroom/speeches-statements/daly-remarks-aba-fed-reg-ia-ic-subcommittees-120225)

- We are all kidding ourselves. Private equity remains in the driver’s seat to uncover and take private anything good that is small and public, and/or we just never see something good go public anymore?

- If 600 is better than 2000, then how about considering being more selective — say between 7 and 30? If your goal is “risk by some measure adjusted return” with some semblance of diversification of said risk factors, and you don’t need to invest $1 billion in a thought to make it worth getting out of bed, I am seriously telling you there is money to be made in smaller cap equities with a focused approach.(From the enlightened height of our all self-interest hereby noted.)

Active management is difficult to scale vs indexation which is why the latter grows at the expense of the former. There is a real limit to finding good and under-recognized ideas and it is time consuming. So, time at CSC is spent doing that and less so in marketing the concept to the world at large. So don’t feel neglected if we aren’t in your face all day long.

A few other moments in 2025 come to mind — remember DOGE? Do you recall the incredible amount of market movement in the largest, most liquid market in the world — US Treasuries — in regard to the possibility of massive government spending reductions and how that might produce a recession on its own? The “Takeover of Social Security?” Defense cuts and national security? Some consultant named Musk running around the hallowed halls of DC? Said another way, we live in a world where the creation of fear or massive ebullience is a 24/7 business across every open sensory orifice you carry. Try to limit intake unless there is banging on the door or your phone is ringing after midnight. The world as you know it rarely comes to end, and even so, it will be difficult to collect if you are right.

Strategy Inc. was/is a masterclass for all-time in so many things that one can say are wrong with the world. To start, a wildly promotional social media CEO with 9.9%-ish economic ownership but effective 45% voting control of the company. A truly INANE and self-coined “business” model entitled a Bitcoin Treasury Company, which consists of nothing but issuing fixed debt and equity to buy the floating asset of Bitcoin in a plan referencing the Hitchhiker’s Guide to the Galaxy. A willing group of moronic investors were willing to pay as high as 3.4x times the value of the underlying Bitcoin, which enables a perfectly rational egotist to sell equity at a premium to NAV and buy more of the underlying. It does not account for what was always obvious — there is NO underlying business of cashflow, so if you cannot sell equity at a premium to your value, you start bleeding cash and then you either have to sell the underlying or sell more equity at lower and lower prices, neither of which is a good thing if you are a mere equity investor. Like many things in life, it only works when the getting is good. And it was damn good if you count 20 or 30 baggers good in the sublime smugness of a well-timed speculative bet. And even better, if you sold near the top.

I can accept the premise that in the year 2025, the world can have something resembling a digital asset/currency that is not subject to any government control, dilution and does not have to be dug out of the ground. Referencing Bitcoin only for the moment — and that statement is a question mark because I am sure if the world of tertiary crypto nonsense unwound badly there is no telling what bodies will be found where and used what for leverage — we could also state the world of custody and regulation has gamely created something resembling an “institutional” look for acceptability.(Yet to be tested.) And then there is the problem that you shouldn’t have enough of it in your asset allocation to really make a difference if the world truly goes to hell.

But my point here is the idiocy of paying 3x for a dollar, a willingness embraced by many more seemingly credible than our man Dan at the Tiki Bar in Hermosa Beach. And the shameless promotion involved selling securities that somehow did not blink an eye at the SEC — yet. If “this” can happen in front of our eyes, the bet remains there is a lot of pent-up stupid to be revealed going forward.

Strategy stock is down some 70% from its November 2024 highs, and trades roughly at the fair value of its Bitcoin, which as noted above, has zero “intrinsic value.” Trying to answer “what’s it worth” without a hedge in place is failing the test no matter what your answer. This press release is a giant WTF of nonsense where the company announced it had raised $1.4bn of equity, not to buy bitcoin but to build a reserve to cover dividends on its five classes of preferred stock for the next two years, redefining the concept that equity is at the bottom of the money stack. And note to someone’s self, “convertible debt” becomes real debt if your strike price is WAY out of money.

If the largest, leveraged buyer of Bitcoin pushing the price to new highs for most of 2025 is now conceptually a seller, what might that mean? CEO Phong Lee helps with the answer on a recent podcast: “We can sell bitcoin and we would sell bitcoin if we needed to fund our dividend payments below 1x NAV, although that wouldn’t be good for the ecosystem and it wouldn’t be good for the narrative.” And that is the world in which we live.

We spent a fair amount of time in our last letter talking about some of the cracks in the facade of Private Credit and we will refer you to that piece for further reading. We will simply add that one of the fun things about being private is that assets are mostly self-marked and as such, are naturally priced by those who would tend to have the most optimistic view of that value. Public markets entertain the idea of a consensus value whereby some might express a more pessimistic view. It is NOT fundamentally less volatile or less risky anywhere than in what passes for process at a consultant led pension committee meeting. But as recently as last week, we still get headlines like “Endowments and foundations have been increasingly turning to private markets to bolster returns and weather market volatility,” Senior Data Reporter at FundFire Michael Taffe reports.

We again note from our last Letter that massive amounts of capital and activity in a narrow frame tend to produce sloppy analysis and losing money in increasingly more tertiary “opportunities.” Sniping from the younger Mr. Grant, Jim Cooney, Bank of America’s head of Americas equity capital markets, described to Bloomberg yesterday: “The velocity of IPO pitch activity is overwhelming, in a good way, across every industry. All of our teams are flat out.”

Which neatly leads into snarking from a recent Institutional Investor piece:

In 2003, Saturday Night Live aired a sketch featuring an evil and duplicitous head of a fictional brokerage called Global Century, played with perfectly snarky faux-earnestness by Chris Parnell, who is addressing investors. It’s clear that these customers (Amy Poehler! Jimmy Fallon! Seth Meyers!) have lost a lot of money by following the advice of Global Century’s advisors — and they have questions. Specifically, an exchange about what Global Century had disclosed in its prospectus:

”At Global Century, we like to be completely up front with our clients. That’s why in our prospectus, we clearly state that our investment advice is often self-interested, or deceitful, and may work to a client’s disadvantage. We think you deserve to know that.”

Client:“It doesn’t say that in the prospectus.”

Global Century guy: “Sure it does.”

Client: “No it doesn’t.”

Global Century guy: “Yes, it’s in there, you have to read it.”

Client: “I’ve read it; it’s not in there.”

Global Century guy: “You’re right, it’s not in there. I just assumed you hadn’t read it.”

What’s in your wallet will be a question more investment committees should be discussing in 2026.

Say something about the FED? Well let’s go to Jay Powell for probably the last time:

“Our two goals are a bit in tension. Right? So, interestingly, everyone around the table at the FOMC agrees that inflation is too high and that we want it to come down and agrees that the labor market has softened and that there’s further risk. Everyone agrees on that. Where the difference is, is how do you weigh those risks, and what [does] your forecast look like, and ultimately where do you think the bigger risk is?”

Ten-year Treasury yields are higher since the Fed started cutting short-term rates and you can all look at the price of Gold.

The AI world commands attention as does any proposal to spend a few trillion dollars from wallets that at present time only involve people who don’t actually own printing presses that create currency. I am not sure we have anything new to add to the trillions of words harassing your well-being on what it all means or how to depreciate a GPU except to note that this all has rhyming feature to it: rarely does a monstrous and fevered allocation of capital to “one thing” result into economics for those investors, excepting the speculative sublimity argument again.

For mankind at large and younger investors? One Jonathan Bliss wrote in the NY Times recently (Don’t say it, I got a terrific “intro” deal with a date to cancel) on AI and music. I think it applies to the investment world and any number of other things. A shovel improves the ability to dig holes, and I am delighted to own one, but I sort of like the idea of knowing how the hell that hole appeared in my backyard.

“For young musicians, it is tempting to sidestep the complicated work of discovering and internalizing these works, blood and guts and all. It’s simpler to declare a specific performance sacrosanct and aim to reproduce it. Playing an instrument well is phenomenally difficult. It takes a lifetime of arduous work and can become all-consuming, making it easy to forget that technical mastery is a means to an expressive end, not the goal. Mastery is a prerequisite if one is to communicate the essence of a piece of music. In and of itself, it is uninteresting.”

I have spent a lot of interesting time in 2025 exploring how AI tools can make me smarter, wider, quicker when it is needed and more time efficient. I will expertly conclude that it dumbs down a lot of the world. Do I want to spend 2 weeks in a foreign world on an itinerary that the whole world just “found?” Do I want any variety of random inane thoughts and somewhat made-up words I put in “quotes” to be removed because the stochastic parrot rules that is a low probability sentence in the eyes of everyone else? Outside of a “how to solder” manual, do I want to spend the rest of my life reading more clever sanitization? Does everything really have to be about AI spend and depreciation schedules? We will discover new and interesting ways to apply it and add to our apparent cleverness. So will the companies in which we are investing. So will the rest of you.

I am going to “out” this man https://www.convexitymaven.com/ whom I have mentioned in the past in these Letters. Besides learning new graph colors that can only be found in a Crayola 100 Party set, there is thinking that makes one think. (Being right remains a different conversation.)

He led a recent email with “As many of you know, I am the Managing Partner at a firm I cannot mention, where I create and manage financial “strategies” whose tickers I cannot name. “

But having dumped our mutual fund, I feel more comfortable recognizing that listening to us yack without something actionable is cheating, here are our top 5 as we speak. Insert the usual disclaimers, do your own work and size for yourself, the process of which is another interesting quirk in our world. Our research suggests that one year from now we will be quoting the ever-entertaining Alex Karp from Palantir: “We were right, you were wrong and we are going to go very, very deep on our rightness.”

American Vanguard – AVD

Butler National – BUKS

Outdoor/Clear Channel – OUT/CCO

Research Solutions – RSSS

Six Flags Entertainment – FUN

And we blissfully close. We would suggest that investing is not about rolling out of bed and rolling from 1 cascading speculative scheme to the next. Yes, just as there do exist 6’2 Jewish guys with Ivy League degrees, play tennis at a 4.5 level, can guitar solo to make Slash blush, and have loving first wives and children who only eye-roll twice a day, there are magnificent moments of speculative “I bought Bitcoin at $1200 genius and you get and deserve the cash and the magic handclap.

But most understand that life is not consistently that easy. And as an industry, we have “rules” set up to prevent us from buying a 5% position in XYZ and riding it to 81% of your portfolio tax-free. (That must be why I haven’t done it.)

I hope I have made it painfully easy to understand where we are coming from: this is an unusually risky world from the standpoint of valuation to whatever the heck is going on out there in a highly speculative world. We apply a fundamental process that evaluates business models –ROIC and cash flow per share growth; management as friend or foe — capital allocation, personal incentives and culture; and valuation — current and the present value of our guesstimates. This is a day in and day out process that has compounded knowledge and tiny bits of wisdom over 4 plus decades. When you see a pitch that you “know” and it is in your “good” strike zone of the previously mentioned variables, you swing at it as hard as your stomach and client understanding can tolerate. From time to time, we have the ability to apply said experience at the governance level, either through addition from our network or now “me” personally. We are not smarter or better per se, but we know a lot about not repeating the same mistakes over and over. Same as it ever was.

We really close with a paragraph from one of the very rare and arguably best “and now my son is going to run things” example I have seen in my career — WR Berkley’s Robert Berkley, Jr. I entitle it, “It’s hard to sit on your ass and do nothing, but sometimes that is the smart move.”

“We start from a place where we are managers of capital. We manage the capital in part through selecting and pricing risk and then all of the activities that come behind that. But we are not in the business of issuing insurance policies. We’re in the business of making good risk-adjusted returns, full stop period. We also recognize it’s a cyclical industry. So there are moments in time you can grow and there are moments of time you can’t. So long story short, Rob, you tell me what the market conditions are going to be, and I can tell you much more thoughtfully what expectations should be of the top line. What I can tell you is regardless of market conditions, we will be focused on profitability. And if the window of opportunity is there, we will have no problem leaning into it and growing dramatically. But if we do not see that opportunity, again, we have no problem folding our arms and waiting for market conditions that are more attractive to present themselves.”

A wonderful 2026 to y’all. We would welcome the opportunity to work together.

Jeffrey Bronchick, CFA

Principal, Portfolio Manager

Cove Street Capital, LLC

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

*The opinions expressed herein are those of Cove Street Capital, LLC (CSC) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. Consider the investment objectives, risks and expenses before investing.

You should not consider the information in this letter as a recommendation to buy or sell any particular security and should not be considered as investment advice of any kind. You should not assume that any of the securities discussed in this report are or will be profitable, or that recommendations we make in the future will be profitable or equal the performance of the securities listed in this newsletter. Recommendations made for the past year are available upon request. These securities may not be in an account’s portfolio by the time this report is received, or may have been repurchased for an account’s portfolio. These securities do not represent an entire account’s portfolio and may represent only a small percentage of the account’s portfolio. Partners, employees or their family members may have a position in securities mentioned herein.

CSC was established in 2011 and is registered under the Investment Advisors Act of 1940. Additional information about CSC can be found in our Form ADV Part 2a,

© Cove Street Capital

Read more commentaries by Cove Street Capital