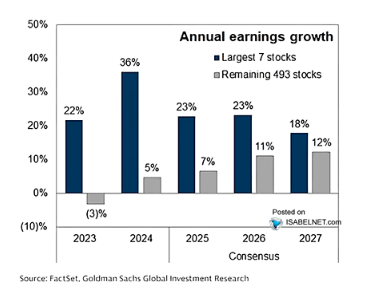

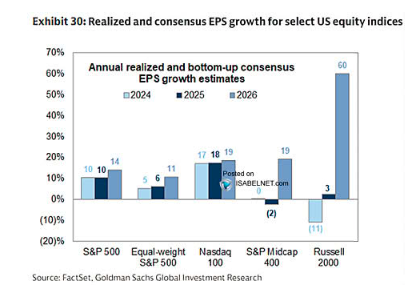

There is a rising market risk in 2026 that is largely overlooked as we wrap up this year. As discussed in the “Fed’s Soft Landing Narrative,” optimism about 2026 is running high. Currently, investors are pricing in strong economic growth, robust earnings, and a smooth path of disinflation. Notably, Wall Street estimates suggest a significant acceleration in corporate profits, particularly among cyclical stocks and small- to mid-cap sectors. To wit:

There is nothing wrong with having an optimistic outlook when it comes to investing; however, “outlooks can change rapidly,” which is a significant market risk, particularly when expectations and valuations are elevated.

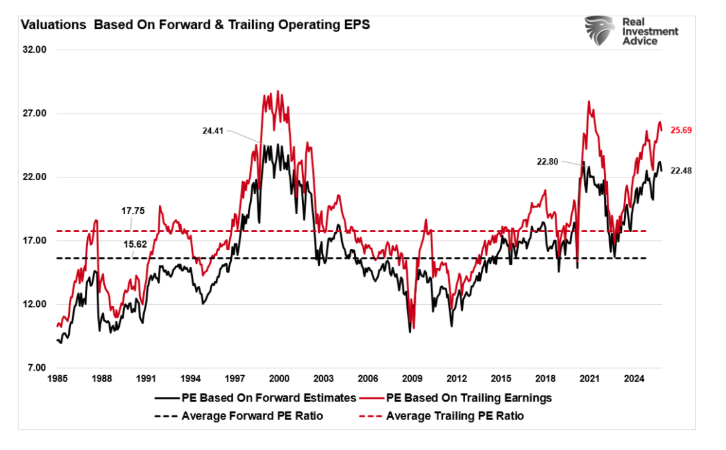

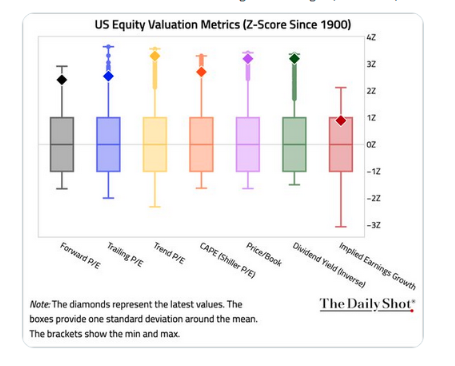

Notably, these forecasts rest on an assumption that the economy will not only avoid recession but reaccelerate in the face of waning inflation. As noted, equity markets have responded by pushing valuations higher across major indexes, with price-to-earnings ratios well above historical medians. Simultaneously, investors have rewarded narratives built on the idea of a soft landing and a return to pre-pandemic trends.

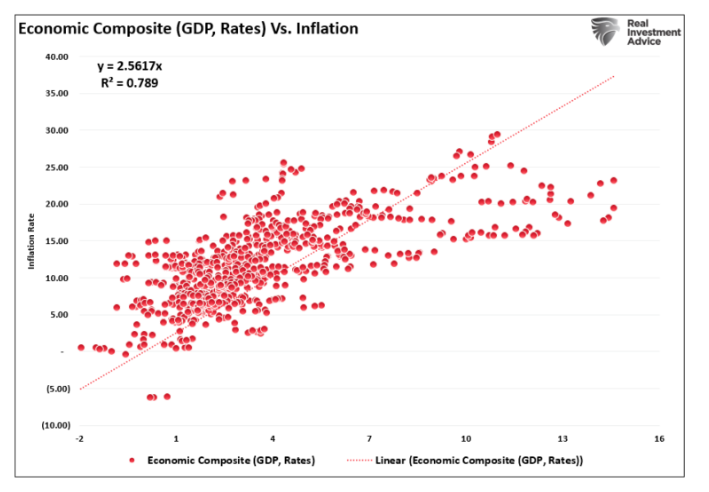

However, this narrative appears to overlook the trends in recent economic data. Inflation expectations have moderated, not because of increased demand, but due to weaker consumption and cooling labor dynamics. As recent economic data indicate, disinflation has accompanied slower GDP growth and a decline in personal consumption momentum. If the economy were indeed set to reaccelerate, these trends should be increasing rather than returning to historical averages.

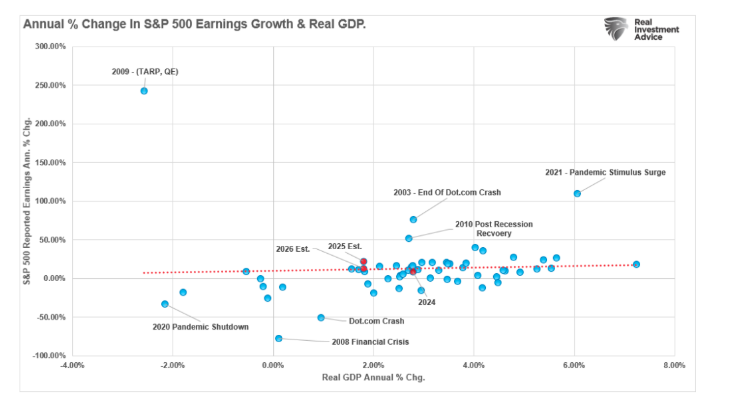

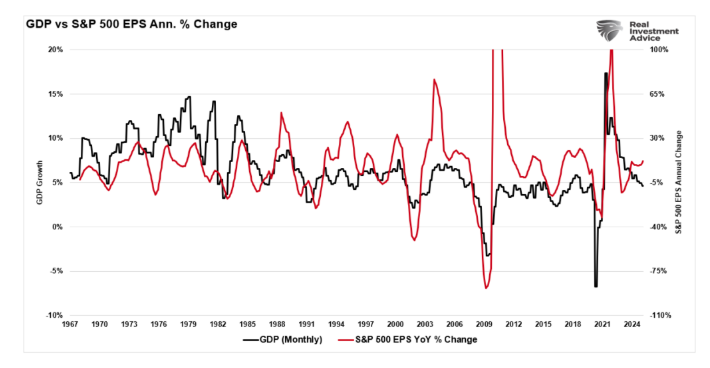

The soft landing thesis posits a benign cycle in which inflation declines, growth remains stable, and earnings increase. Yet, that outcome would be historically rare. When inflation falls this quickly, it typically reflects a slowdown in demand rather than policy success. Additionally, the strong relationship between economic growth and earnings should not be dismissed. That disconnect exposes investors to market risk if growth does not materialize as expected and valuations are reconsidered.

With analysts expecting strong revenue growth and margin expansion despite rising input costs, global uncertainty, and declining employment, a market priced for perfection leaves little room for earnings misses or growth shocks. If those optimistic assumptions fail, market risk could rise abruptly.

Let’s dig in.

Structural Headwinds

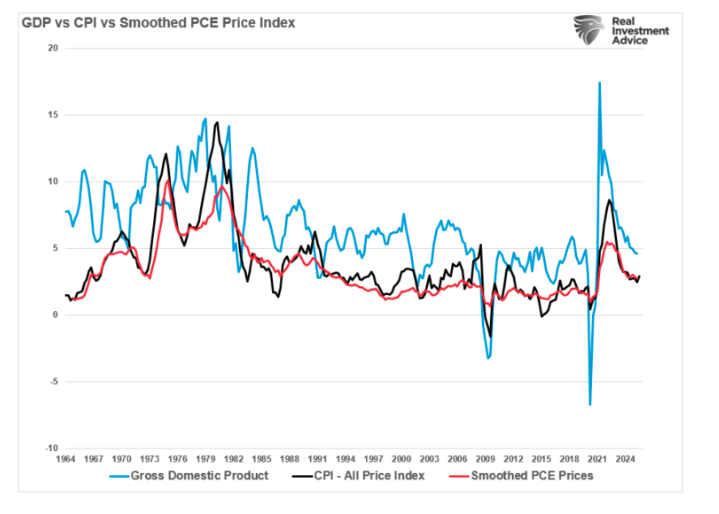

As noted above, earnings growth is fundamentally tied to economic growth. When demand exceeds supply, companies expand output, raise prices, and increase profits. As discussed recently, this is why, without inflation, there can not be economic growth, increasing wages, and an improving standard of living. In other words, for there to be stronger economic growth and rising prosperity, prices must increase over time. Such is why the Fed targets a 2% inflation rate, thereby supporting 2% economic growth and stable employment levels.

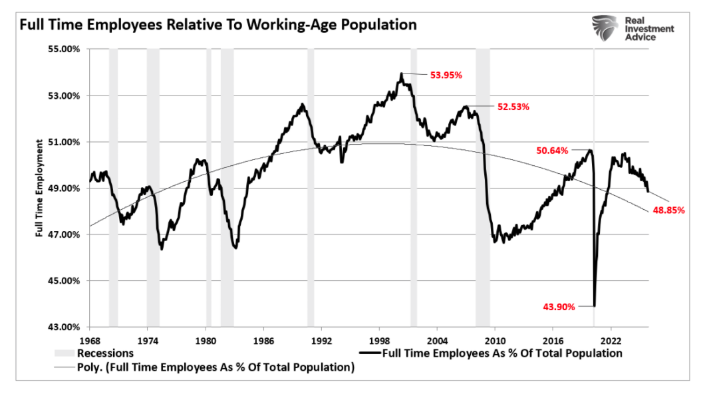

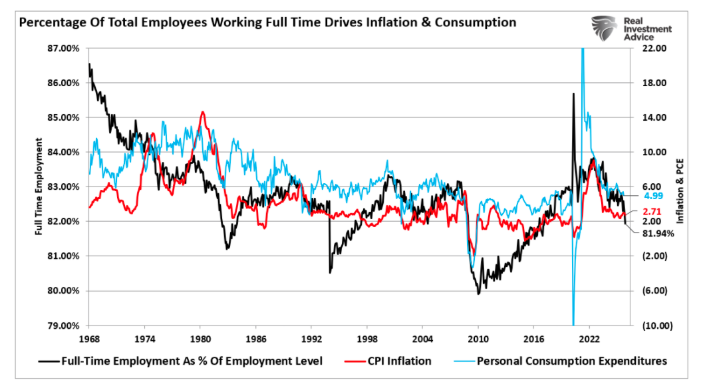

However, the employment data over the last year doesn’t tell a story of substantial employment, rising wages, or a trend suggesting a more robust economic outlook. Instead, the latest data confirmed a deceleration in economic activity, as full-time employment (as a percentage of the population) declined.

The importance of full-time employment should not be readily dismissed. Full-time employment pays higher wages, provides family benefits, and allows for an expansion of consumption. The decline in full-time employment currently is normally associated with recessions rather than expansions. Economic growth, inflation, and personal consumption are trending lower, given that employment, particularly full-time employment, supports economic supply and demand.

Furthermore, economic growth relies heavily on consumer spending, which accounts for nearly 70% of U.S. GDP. For that consumption to persist or grow, consumers must have rising incomes, which come from employment and wage growth. Without job creation or real wage increases, consumption growth stagnates, and the earnings narrative breaks down. As shown, when economic growth declines, so do earnings growth rates.

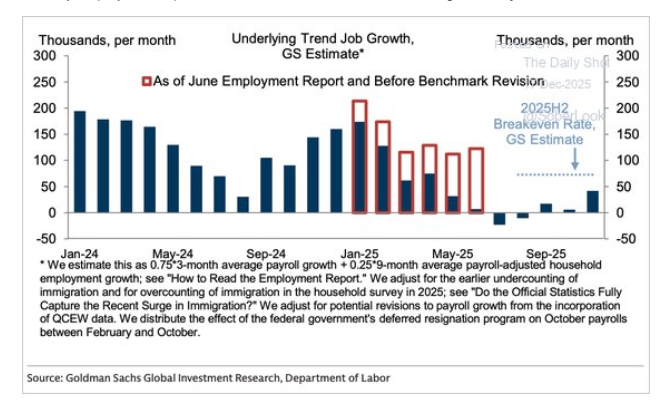

Recent employment data show cracks in this cycle. While headline job numbers suggest continued hiring, the quality and composition of those jobs are weakening. Today, we see part-time workers filling full-time positions, often with lower pay and fewer benefits. Labor force participation remains below pre-pandemic levels, and many prime-age workers are not returning. Most notably, the negative revision of every monthly employment report in 2025 further undermines the “strong economy” narrative.

Even where wages are rising nominally, inflation-adjusted wages tell a different story. Real wage growth has been flat or negative in several key sectors. As housing, energy, and service prices remain high, the squeeze of disposable income increases. As such, consumers compensate by drawing down savings or using credit, both of which are unsustainable long-term strategies.

The market risk in 2026 is that for corporate earnings to accelerate and meet Wall Street’s expectations, the consumer must be healthy. That means rising real wages and broad-based job creation. Without those pillars, top-line revenue growth slows, and margin pressures increase. Analysts projecting double-digit earnings growth into 2026 are assuming a demand-driven economy without the income growth needed to support it. That assumption is increasingly fragile. Without real economic growth, earnings become a product of financial engineering or cost-cutting, not organic expansion. Markets are pricing in a demand surge that the employment data do not confirm.

If this disconnect persists, Wall Street will revise earnings expectations lower.