We believe that tax-free municipal bonds continue to be well positioned in the current market environment. Their characteristics warrant a place in most retail investors’ investment portfolios, and not just due to their appeal of relatively high taxable equivalent yields (TEYs). This subsector of fixed income is generally of very high-credit quality with significantly lower default levels relative to other sectors. Historically, it has acted as an important diversifier particularly for equity allocations, and after two straight years of record issuance levels, the technical picture looks solid.

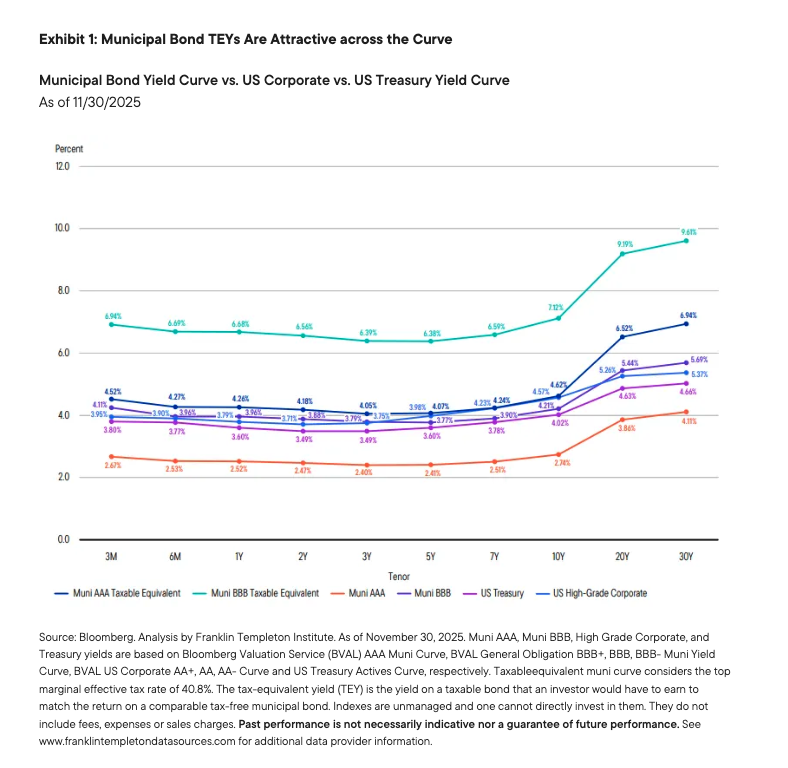

Taxable-equivalent yields (TEYs) remain robust

In most instances, the income from municipal bonds is not subject to federal income tax and can also be exempt from state income tax for investors holding bonds in the state in which they reside. It is essential for comparison purposes to consider this feature when comparing municipal bonds to other subsectors of fixed income which are fully taxable, to get a true apples-to-apples comparison. This can be accomplished through the lens of taxable equivalent yield (TEY), which puts tax-free and taxable securities on an equal playing field.1 As Exhibit 1 shows, TEYs for the municipal bond sector are attractive across the yield curve relative to both US Treasuries and US investment-grade corporate bonds. As of the end of November 2025, the yield advantage continued to be most pronounced for the intermediate to long end of the curve, as it has steepened.

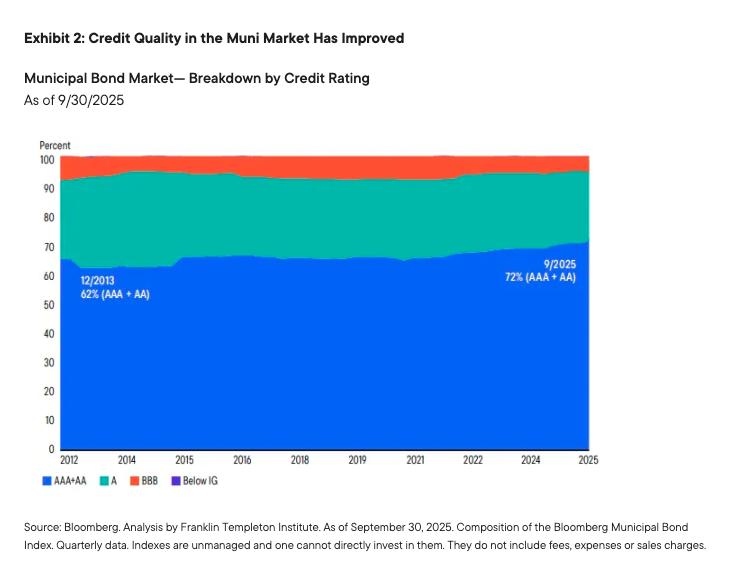

Credit quality remains high and is improving

The credit profile of the overall municipal bond market is extremely solid, in our view. As of third quarter of 2025, nearly three-quarters of the market was rated AAA or AA, up from less than two-thirds just a decade ago. Most of the remaining credit qualities in the municipal bond space are single A, with less than 10% of the market being BBB rated. Exhibit 2 illustrates this breakdown of credit quality over the last dozen calendar years.

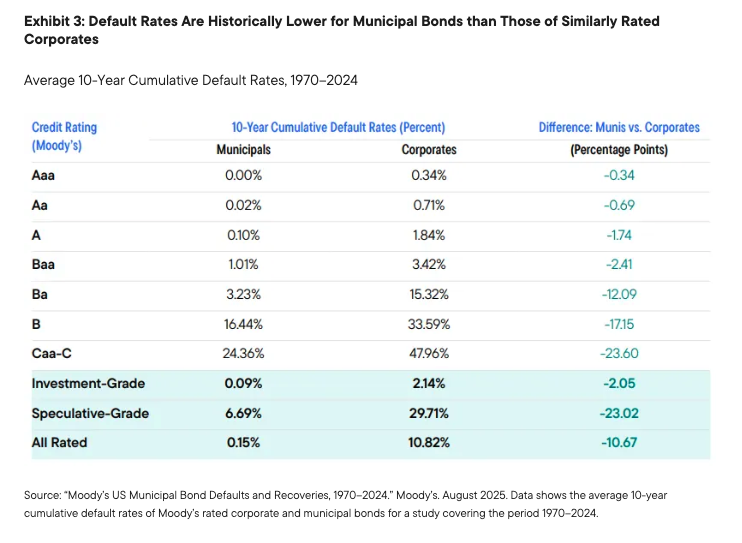

Default level of municipal bonds is very low versus taxable bonds

As you might expect, the high credit quality in the municipal space has led to extremely low default rates for the asset class over the past decade. For every credit tier, from AAA down to CCC, the 10-year cumulative default rate for municipal bonds has been much lower than for corporate bonds of comparable credit quality. Our analysis suggests that in the investment-grade space, defaults have been almost 25 times higher for corporate bonds when compared to their tax-free counterparts over the past decade. Exhibit 3 illustrates the default levels by credit quality rating for tax-free munis versus corporates and splits out investment-grade, non-investment-grade and all ratings.

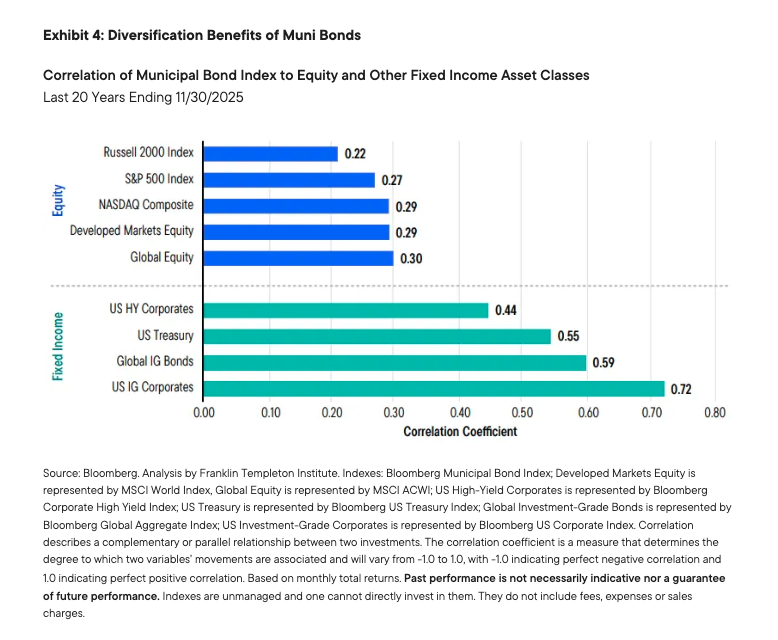

Municipal bonds can be a powerful diversifier

Over the past couple of decades, municipal bonds have been a very powerful diversifier, particularly to stock market indexes. Tax-free bonds have also had relatively low correlations with their taxable counterparts, especially high-yield bonds and US Treasuries. These important diversifiers can help dampen portfolio volatility in most cases, leading to investors staying invested throughout different market cycles. Exhibit 4 illustrates just how low the correlations have been with both equity and fixed income indexes over the past 20 years.

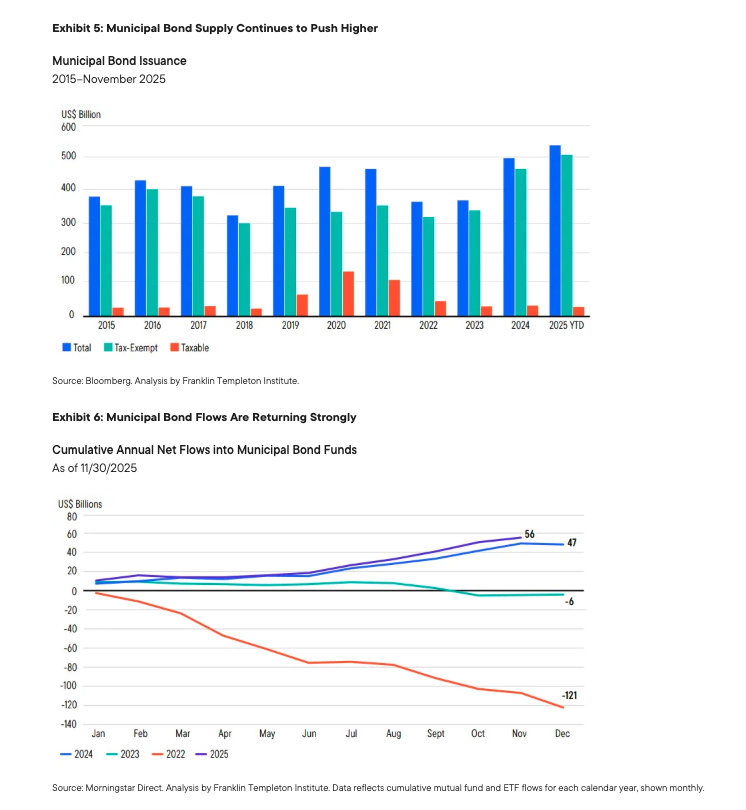

Technicals appear supportive of munis

Following two consecutive record years of tax-exempt municipal bond supply in 2024 and 2025, the supply/demand dynamics appear poised to return back to more normalized levels. We believe issuance levels will continue to remain high; however, they should be met with strong investor demand. After an incredibly challenging landscape in 2022 led to approximately US$120 billion in net outflows, 2023 was a year of only modest outflows in the municipal market. In 2024 around US$47 billion flowed into the asset class, and 2025 is on track to be another modestly positive year of inflows. Exhibits 5 and 6 illustrate supply and demand in the asset class.

Conclusion

We believe there are many types of investment portfolios that can benefit from having allocations to tax-free municipal bonds. They offer attractive TEYs relative to their taxable bond counterparts, while acting as a powerful diversifier of equities and even other fixed income subsectors. Municipal bonds continue to have high credit quality with extremely low default rates, and elevated levels of supply are being well absorbed by the strong demand across the retail channel since flows turned positive in 2024. We also believe that the municipal bond market should benefit from future clarity around both monetary and fiscal policy.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnote

1TEY, or taxable-equivalent yield, is the yield on a taxable bond that an investor would have to earn to match the yield of a comparable tax-free municipal bond.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

The allocation of assets among different strategies, asset classes and investments may not prove beneficial or produce the desired results.

An investor may be subject to the federal Alternative Minimum Tax, and state and local taxes may apply.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

To the extent the portfolio invests in a concentration of certain securities, regions or industries, it is subject to increased volatility.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton

Read more commentaries by Franklin Templeton