The U.S. economy appears poised for a measured and confident expansion into 2026 driven by a stabilizing monetary policy, corporate strength, and resilient household income growth. Our outlook suggests a supportive environment for risk assets, particularly domestic equities, while favoring specialized strategies in fixed income.

A key foundational element of our outlook is the expectation of U.S. Federal Reserve (Fed) progress toward a more neutral interest rate stance after recently ending their Quantitative Tightening program. Current market pricing reflected in the CME Group’s FedWatch Tool favors additional rate cuts with the most likely scenario suggesting two more 0.25% reductions.

These reductions will bring the Federal Funds Rate range down to 3.00% to 3.25% by the end of 2026. The preemptive cuts in the absence of a severe crisis aim to lower the Federal Funds Rate to a level that neither stimulates nor constricts the economy. This normalization of monetary policy reduces the cost of capital and provides a favorable backdrop for investment and corporate earnings growth without igniting inflation.

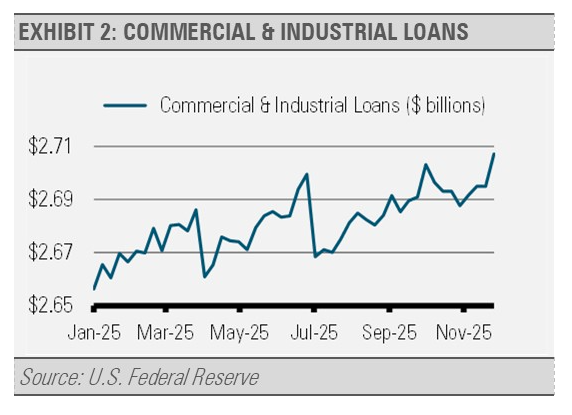

Additionally, the business sector is exhibiting confidence despite lingering concerns about slowing economic momentum. The increase in commercial and industrial (C&I) lending to new highs for the year signifies that businesses are willing to take on credit for expansion, capital expenditure, and working capital needs.

With non-financial sector debt-to-GDP falling to its lowest level since 2014, the business sector overall has plenty of room to increase borrowing to fuel investment growth.

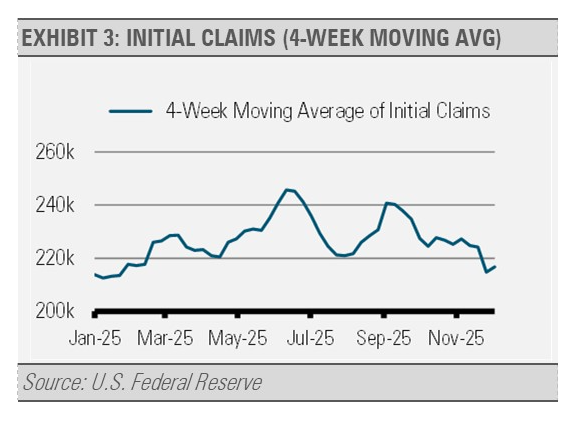

This increased risk appetite is further supported by a remarkably resilient labor market. While jobs growth has slowed, businesses have voiced frustration with finding qualified workers according to the latest NFIB Small Business Optimism Index. In the same survey, small businesses expressed increased confidence overall. We can see this conviction in layoff figures, such as the Weekly Jobless Claims, which are still near the low for the year despite reports of rising announced job cuts related to restructuring and the adoption of Artificial Intelligence (AI).

While we do not expect the labor market to return to its previous strong pace, we do anticipate jobs growth to continue. Importantly, this growth combined with wage gains that continue to outpace inflation supports higher inflation-adjusted disposable income for households. This combination of a confident business sector and a resilient, albeit slowing, consumer base forms a solid foundation for further economic expansion into 2026.

INVESTMENT IMPLICATIONS

The continuation of strong earnings growth forms our primary bullish thesis for the U.S. equity market. As corporate profitability expands, driven by productivity gains and a stabilized cost of capital, we expect stock market levels to move higher. We continue to favor U.S. equities, which offer superior growth prospects and are beneficiaries of major secular trends. Sector-specific opportunities are concentrated on three key areas in our opinion:

- Information technology remains the primary engine of growth, fueled by massive capital expenditure in AI infrastructure, data centers, and advanced computing.

- Industrials should benefit from the onshoring of manufacturing, large-scale infrastructure projects, and the industrial demand generated by the AI build-out.

- Financials will benefit from falling short-term interest rates and a steeper yield curve that supports net interest margins, while the general economic expansion boosts demand for lending and capital markets activity.

In the fixed income space, we currently favor a selective approach designed to balance attractive yields with limited duration risk. Specifically, we favor asset-backed securities (ABS), which are collateralized by assets like auto loans or credit card receivables. We are focused on the belly of the yield curve in the maturity range of 3- to 7-years.

We believe ABS offers higher relative values and are less correlated with traditional corporate credit risk, which provides diversification. The moderate duration of the belly of the curve can allow investors to capture attractive intermediate-term yields while avoiding the potential volatility at the longer end of the curve, which is often sensitive to evolving inflation and fiscal policy expectations.

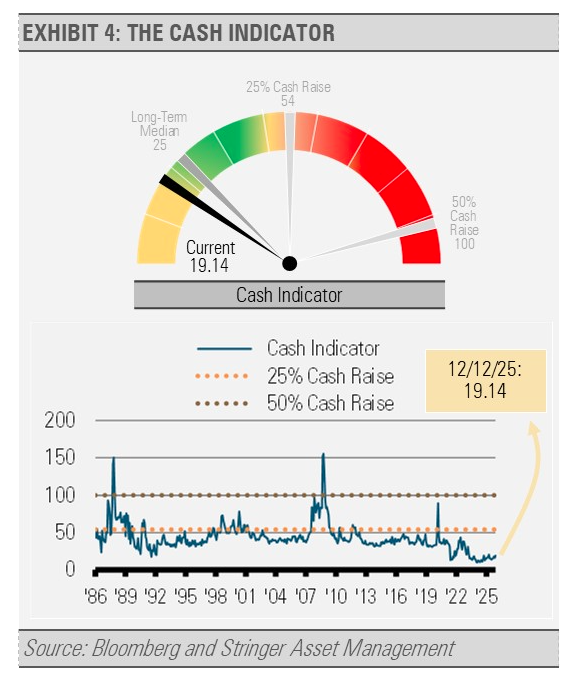

THE CASH INDICATOR

Though the Cash Indicator has been hovering at levels persistently below normal, it has been more elevated in recent months. We think that these levels reflect healthier financial markets where investors show some caution and less complacency. This healthy skepticism can make markets more resilient to shocks.

For more news, information, and strategy, visit the ETF Strategist Content Hub.

Originally published on ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Read more commentaries by Stringer Asset Management