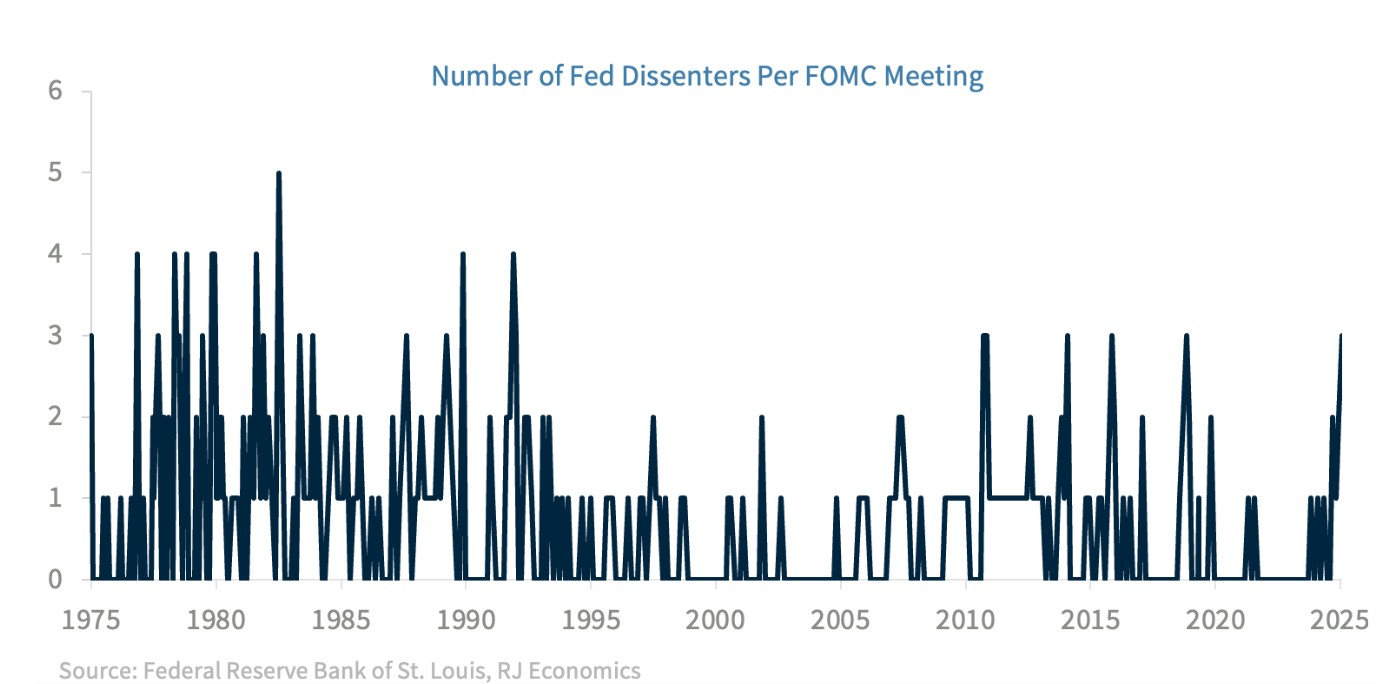

Since this is our first Weekly Economics of this new year, we felt it was important to mention what transpired during the last Federal Open Market Committee (FOMC) meeting of 2025, according to the FOMC minutes. This week’s release of the FOMC meeting minutes showed relatively strong diverging views on current monetary policy as well as on the path for policy this year. Although we already know those who were in favor, those who were against, and those who wanted even a larger cut, it seems that many of those FOMC members who supported the December rate cut were indifferent between a cut or no cut in rates, which could become an issue for those expecting another cut early this year.

The minutes indicated that “Against this backdrop1, most participants supported lowering the target range for the federal funds rate at this meeting, while some preferred to keep the target range unchanged. A few of those who supported lowering the policy rate at this meeting indicated that the decision was finely balanced or that they could have supported keeping the target range unchanged.” This is in line with our own assessment in our December 12, 2025, Weekly Economics when we argued that “We favored a rate cut at this time. However, we realize that a very good case could have been made, from a monetary policy as well as an economic point of view, for no cuts or even higher rates, although the latter alternative had a very, very, high bar, as the Chairman of the Fed seems to have alluded to during the press conference after the FOMC decision. In fact, we believe that Fed officials finally decided to go ahead with a rate cut as a way to buy time to get a better reading on economic activity after the delay in data releases due to the government shutdown. However, it is clear that there was an important lack of conviction that a rate cut was really needed at this time, which is why two dissenters opted for no cut in rates during the meeting.”

We added that “For the majority of FOMC members, they were probably indifferent between cutting by 25 basis points or keeping rates steady, as long as markets kept upward pressure on longer term rates, as it has been the case since September of 2024, when the cycle started. Meanwhile, those preferring to keep rates unchanged were probably more concerned with inflation expectations being affected by the political pressure coming from the Trump administration to lower rates more forcefully.”

Although there was no mention of the administration’s efforts to influence the Fed to push interest rates much lower and much faster, “… several participants pointed to the risk of higher inflation becoming entrenched and suggested that lowering the policy rate further in the context of elevated inflation readings could be misinterpreted as implying diminished policymaker commitment to the 2 percent inflation objective.” That is, many FOMC members were clearly concerned about not bringing down inflation to the 2% target faster and that this could be construed as not being committed to the inflation target, which could help de-anchor inflation expectations.

Looking ahead, the minutes suggested a more cautious stance than what markets currently imply, noting that “With respect to the extent and timing of additional adjustments to the target range for the federal funds rate, some participants suggested that, under their economic outlooks, it would likely be appropriate to keep the target range unchanged for some time after a lowering of the range at this meeting.”

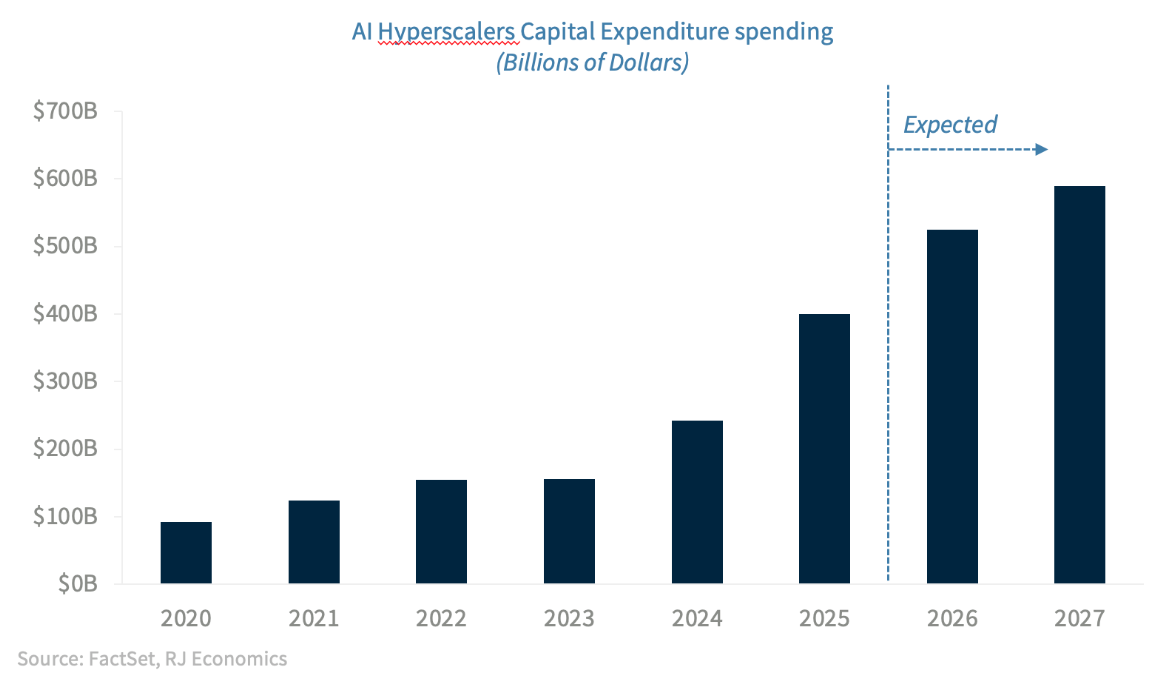

This is also in line with our view. Given stronger economic growth driven by AI investments and expansive fiscal policy, while maintaining still relatively high inflation readings, it is highly unlikely that Fed members are going to be more aggressive with rate cuts. The only thing that could radically change their view on rates would be heightened risks of labor market deterioration and/or higher risks of recession, which is not the Fed members’ base case, nor is it ours.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

J.D. Power 2025 U.S. Investor Satisfaction Study, which measures overall investor satisfaction with investment firms, was released 3/20/25, based on investors surveyed 1/24-12/24, who may be working with a financial advisor. Based on 7,876 responses from Advised Investors, 1 company out of 24 was chosen as the winner. The award is not representative of any one client’s experience, is not an endorsement, and is not indicative of an advisor’s future performance. The study is independently conducted, and the participating firms do not pay to participate. Use of study results in promotional materials is subject to a license fee. J.D. Power is not affiliated with Raymond James. For J.D. Power 2025 award information, visit jdpower.com/awards.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

© 2025 Raymond James Financial, Inc. All rights reserved.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - September 2025 (PDF)

© Raymond James

Read more commentaries by Raymond James