Systematic fixed-income investing is an active approach that aims to beat bond-market returns by identifying and harnessing the factors that drive bond-market performance.

Well-known factors such as value and momentum are widely recognized to have predictive power. Advanced systematic approaches, however, seek to identify additional drivers of performance—including proprietary factors—to integrate into their multifactor models.

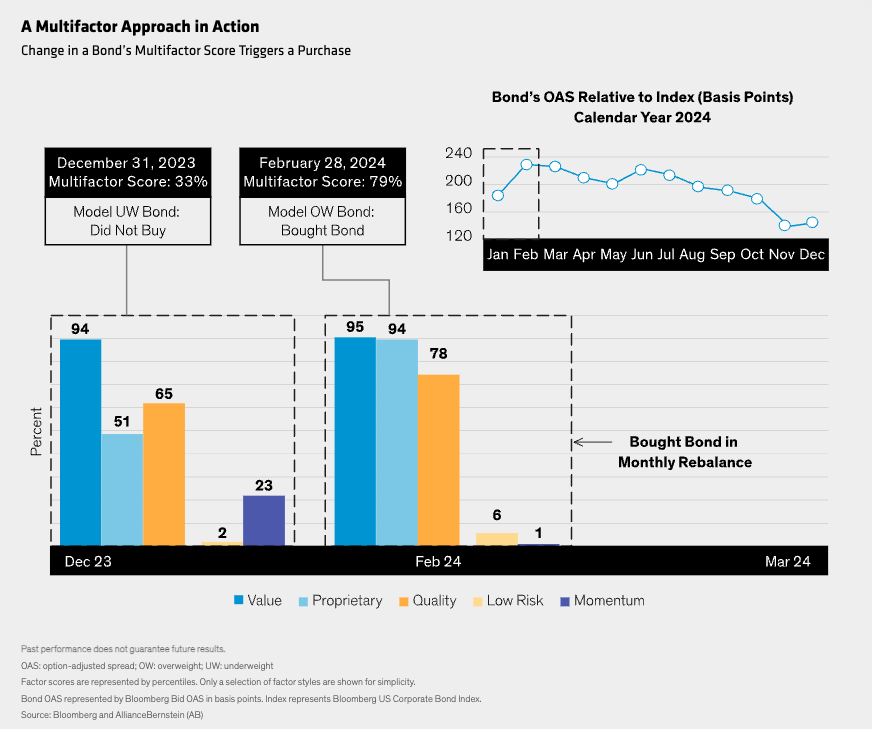

Using a specific bond as a case study, the display above shows how a multifactor model determined a total score for the bond based on its underlying factor scores.

At the start of the year, the bond scored highly on well-known factors such as value and quality. However, it scored low on some of the other factors. This reduced the total multifactor score, avoiding a premature purchase.

By the end of February, several of the factors’ scores had improved significantly, leading to a higher total multifactor score and to the bond being added to the portfolio.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.