Key takeaways

- Despite bubble fears, there are several key differences between the late 1990s and today that we believe bode well for US equities in the year to come.

- A pickup in productivity from artificial intelligence (AI), combined with moderating wage gains, a softening labor market, weaker shelter prices and lower commodity costs could all push inflation lower as we move deeper into 2026.

- While valuations are elevated, we believe equities will “grow into the multiple” in 2026 with strong earnings fueled by ongoing AI capex strength as well as fiscal and monetary stimulus.

“Party like it’s 1999” is a phrase made famous by the musician Prince’s 1982 song, which experienced a renaissance amid Y2K fears and has since entered the lexicon meaning to celebrate intensely because the future is uncertain. The phrase seems apt to describe the current investment landscape, given the similarities between the late 1990s dot-com bubble and today. These include lofty valuations, strong market momentum and a focus on growth stocks. However, we believe there are several key differences between the present environment and 1999 that will keep the markets moving higher in the year to come, which may be a surprise to many.

1999 vs. 2025: Economic differences

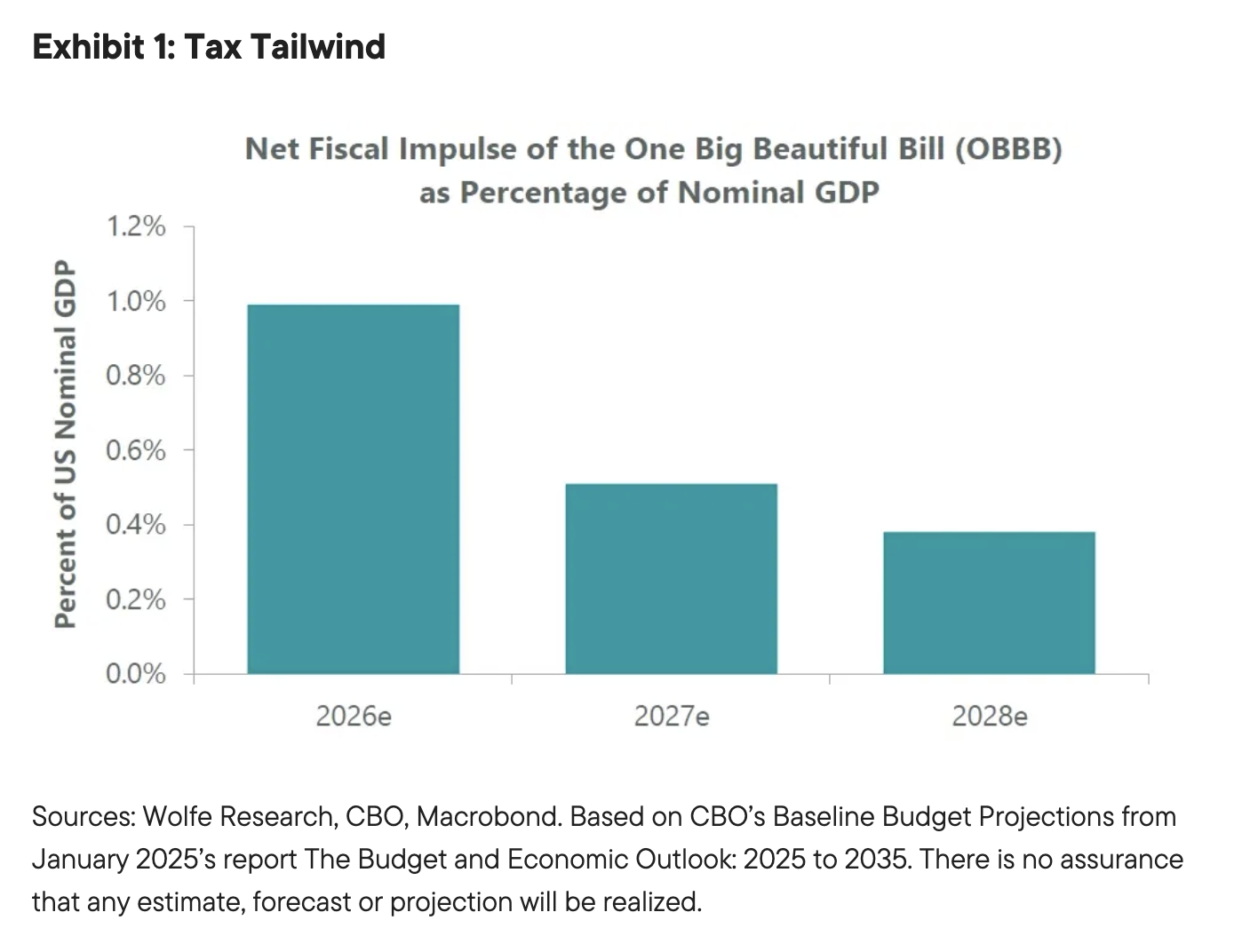

The first key difference is that the US economy is poised to benefit from both fiscal and monetary stimulus in 2026, a potent combination typically only seen coming out of recessions. The net impulse from the One Big Beautiful Bill (OBBB) is expected to deliver ~1% of GDP this year with supercharged tax refunds providing support to low- and middle-income households.

Tax refunds are typically spent rather than saved, suggesting that much of this cash will make its way back into the economy relatively quickly. The COVID stimulus payments provide a good example of this dynamic, with research from the Peter G. Peterson Foundation showing that households earning below US$75,000 spent around 80% of the initial stimulus payments they received. That figure dropped but stayed above 50% for households with over US$150,000 in earnings. While the 2026 tax refund bonanza will likely fade in the second half of 2026, the OBBB’s fiscal impact should continue in 2027 and 2028 but at lower levels of support around 0.5% of gross domestic product (GDP) according to Congressional Budget Office and Wolfe Research estimates.

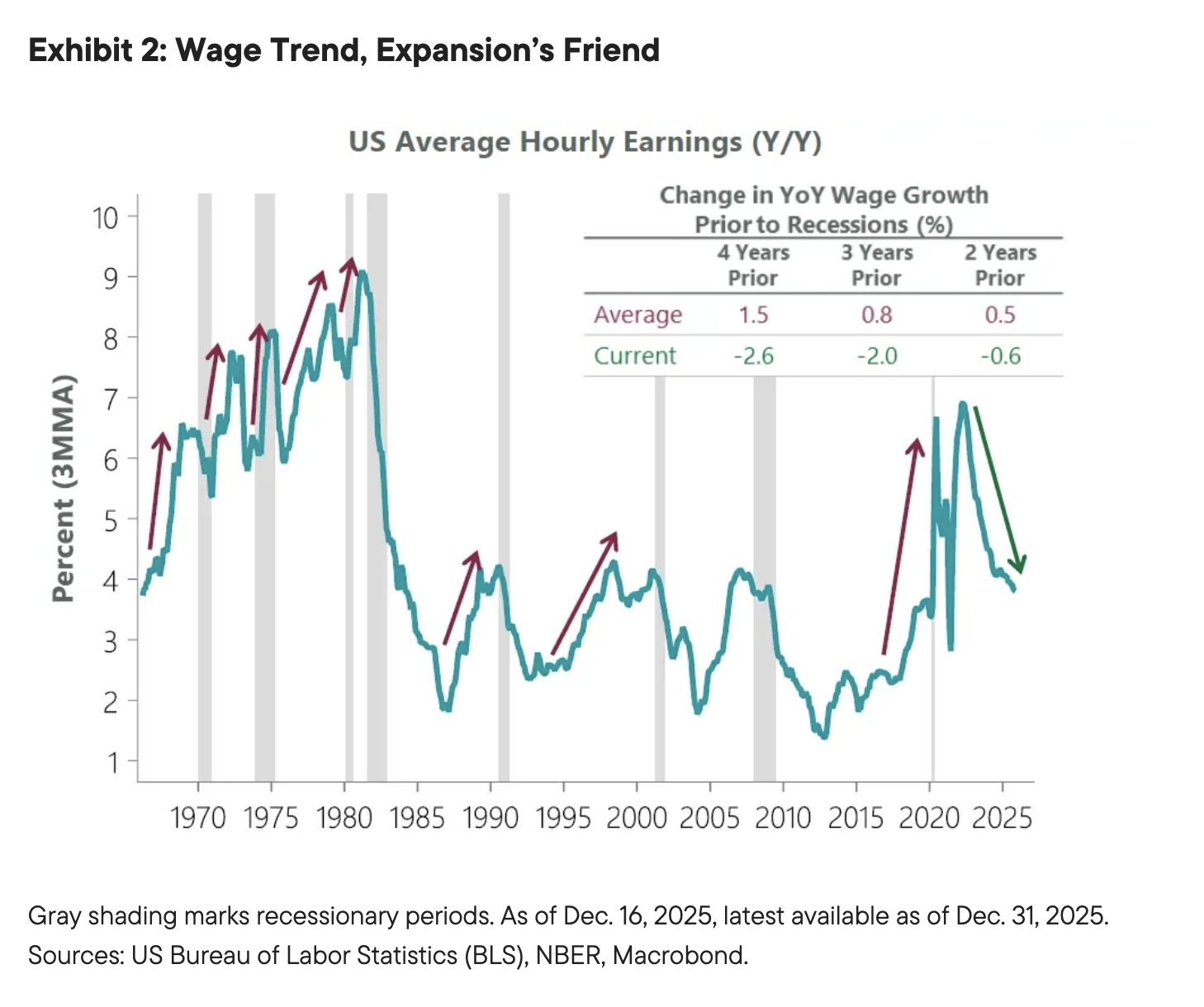

The benefit from this stimulus should be significant because wage growth—the largest source of spending power for most Americans—has continued to moderate following the post-pandemic spike. Although this moderation has strained lower income cohorts and led to the “K-shaped” economy, it is somewhat encouraging from a macro perspective. Typically, maturing economic expansions see accelerating wages that often spook the Fed into tightening to prevent a wage-price inflationary spiral. This, in turn, can choke off economic growth and help set the stage for a recession. However, this dynamic is not in place today, which marks a second key difference between the present and 1999.

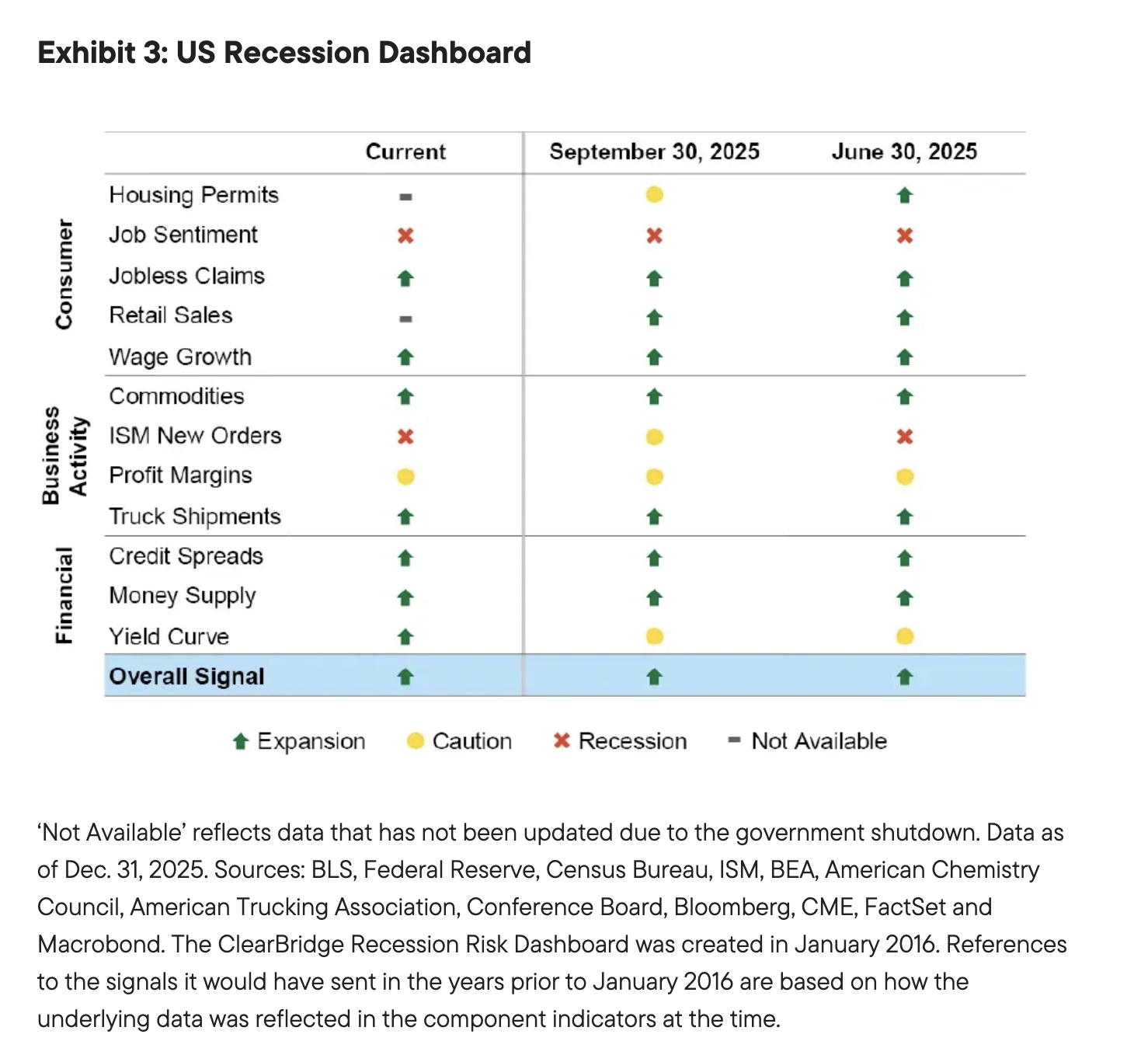

Cooling wages have resulted in the Wage Growth indicator on the ClearBridge Recession Risk Dashboard remaining in solid green territory, which is also where the overall signal continues to reside. The dashboard did see two changes in December: ISM New Orders dropped back to red after the second consecutive monthly reading below 48, while the Yield Curve improved to green as it steepened above 50 basis points. Housing Permits and Retail Sales remain on hold due to lingering delays related to the US government shutdown in October and November, but these issues should hopefully be resolved in the coming weeks.

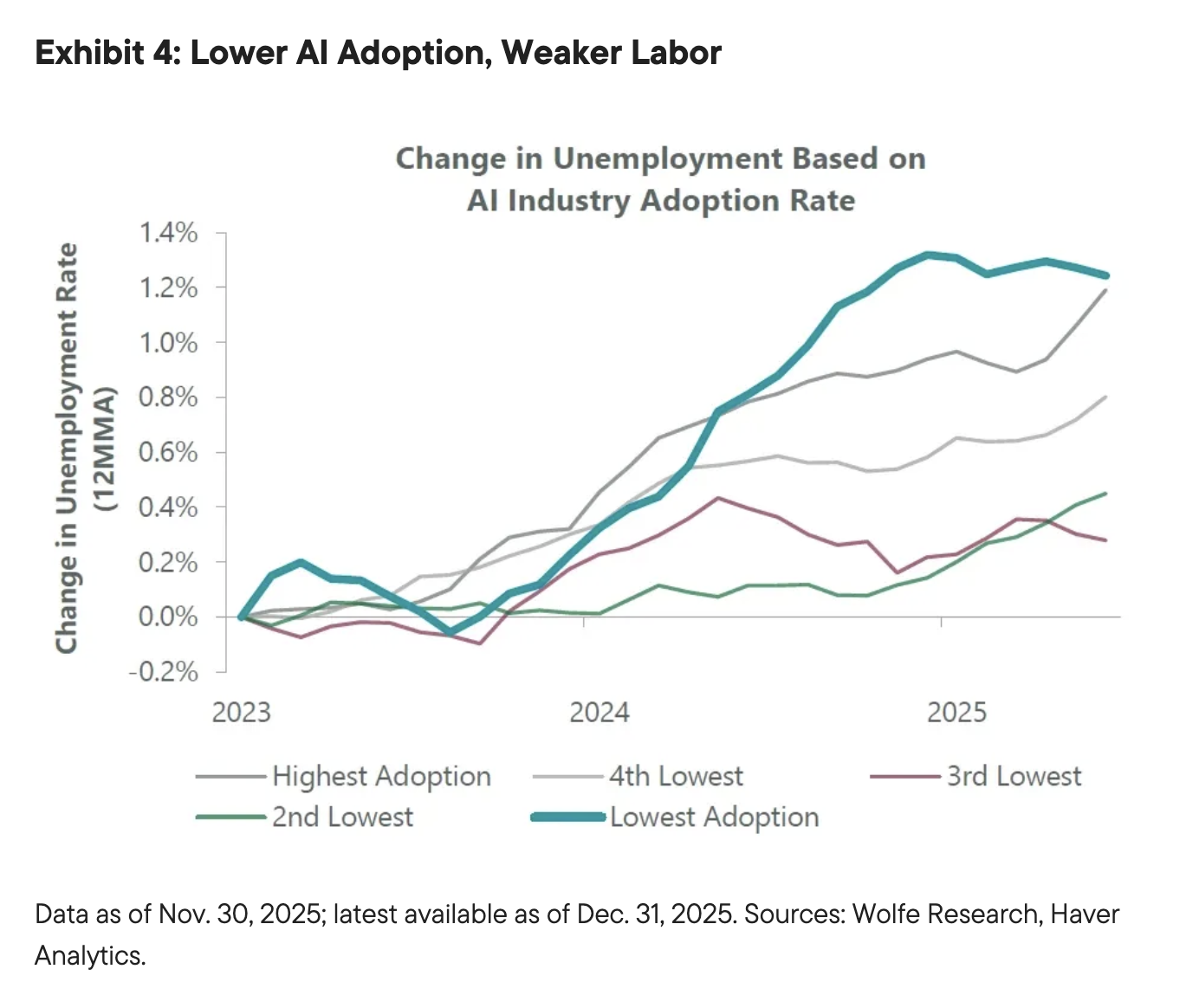

The trend of moderating wage gains over the past few years has stood in stark contrast to an economy that has continued to deliver solid growth. Gross domestic product (GDP) has grown by an average of 2.8% on a real basis since the end of the first quarter of 2023. This momentum has shown little sign of slowing recently, with the third quarter of 2025 coming in at 4.3%. At the same time, the unemployment rate has risen over a full percentage point to 4.6% from the 3.4% lows in April 2023. As a result, some observers are blaming the rise of artificial intelligence (AI) for recent labor market weakness.

AI does appear to be contributing toward softer hiring in the technology industry and for entry-level roles in particular. However, a broader review shows that occupations where AI adoption is the lowest have seen the greatest rise in unemployment, suggesting that other factors have been driving labor weakness. Job growth for industries more rapidly adopting AI is actually positive, driven by AI augmentation as opposed to substitution—a dynamic we explored in last month’s blog.

AI adoption has been advancing at an extremely fast pace compared to past innovations. Positive technological breakthroughs typically lead to a pickup in productivity and a drop in inflation (or even deflation). This dynamic usually takes time to bear out as was the case during the 1990s. Given the rapid adoption of AI over the past few years, however, we believe there’s a strong possibility this lag could be compressed. If this proves true, the risk to inflation could end up being to the downside, not the upside, in 2026.

The “January effect” is likely to be larger than normal once again this year. However, a pickup in productivity combined with moderating wage gains, a softening labor market, weaker shelter prices and lower commodity costs could all push inflation lower as we move deeper into 2026. Further disinflation—the aforementioned scenario largely represents a continuation of 2025 trends—would likely be bullish for financial markets as it would allow for further Fed easing should employment growth remain lackluster (50k-75k jobs per month).

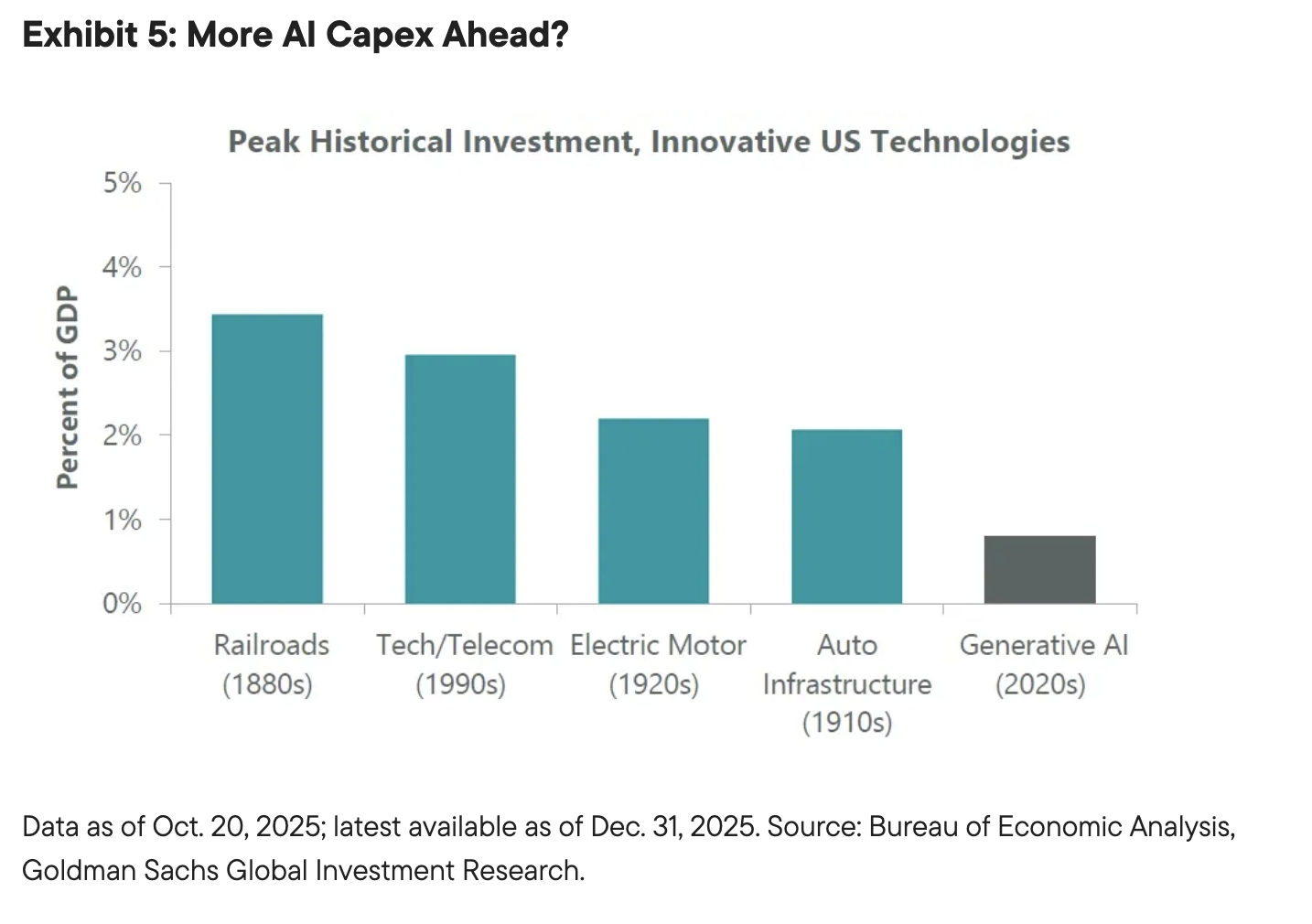

Another 2025 trend likely to continue in the new year is the rapid growth of AI capital expenditures (capex) as the AI infrastructure buildout continues. Despite fears that AI capex has reached bubble territory, current levels of spending are well below the peak seen during prior innovative technological cycles in the United States, as a percentage of GDP. For example, AI investment accounts for about 1% of the US economy today compared to 3% during the late 1990s tech/telecom bubble. Should history repeat, AI capex could surprise to the upside in the years to come, providing continued support for both the economy and markets.

1999 vs. 2025: Market differences

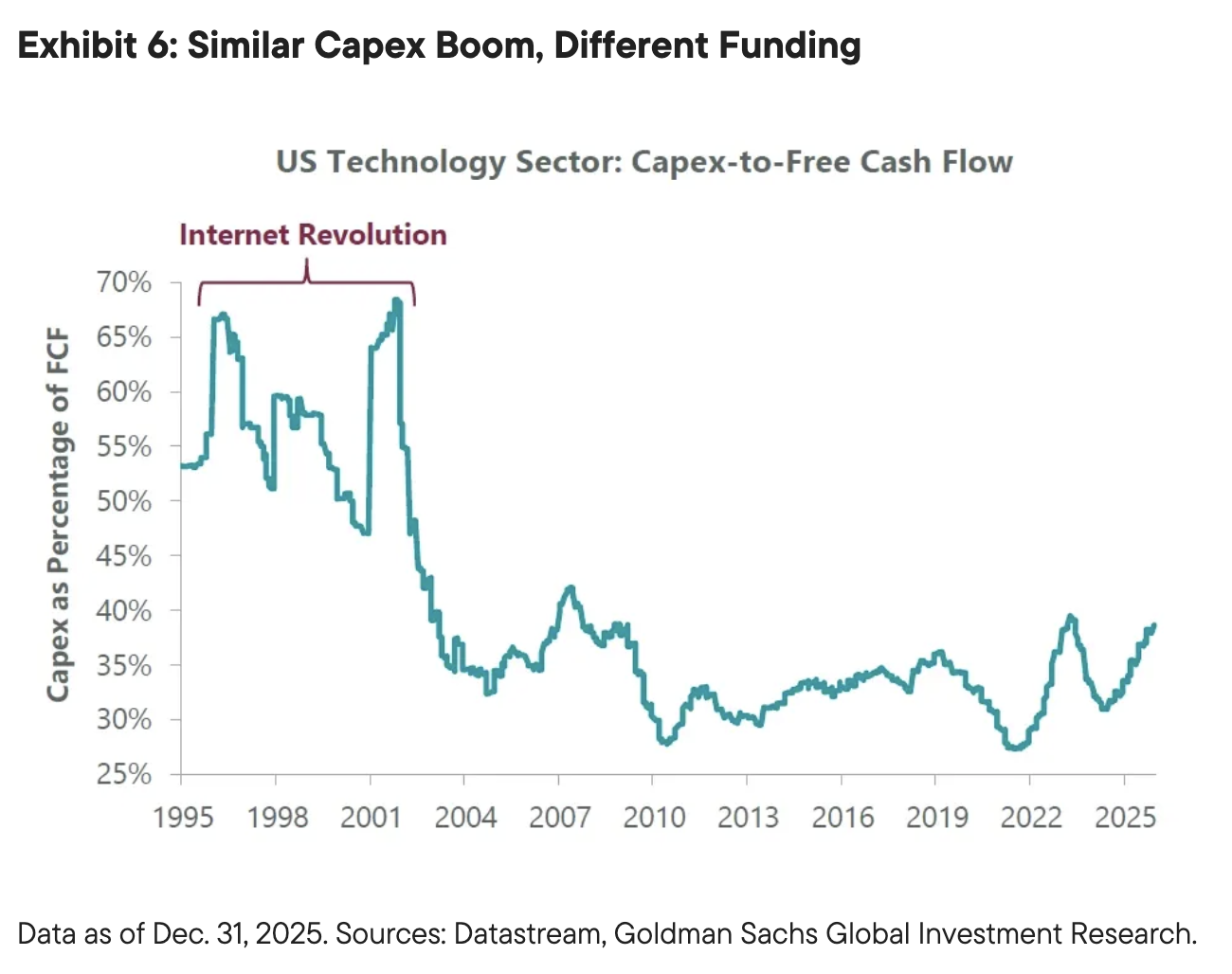

The funding source of this capex brings us to the third key difference between the late 1990s and today. Today’s spending is largely financed from corporate free cash flow (FCF), whereas the tech/telecom capex buildout was primarily underwritten in the capital markets through debt and/or equity issuance. Recently, smaller players have begun to increasingly tap debt markets and even the hyperscalers have begun to dip a toe. However, the tech sector’s aggregate capex spending equates to under 40% of FCF, well below the mid-1990s peak of 67%. With today’s leaders flush with cash, so far there has been less of a need to raise capital to fund the AI buildout. Put differently, debt financing will likely become more prevalent in 2026 (and beyond), but we are not currently near concerning levels.

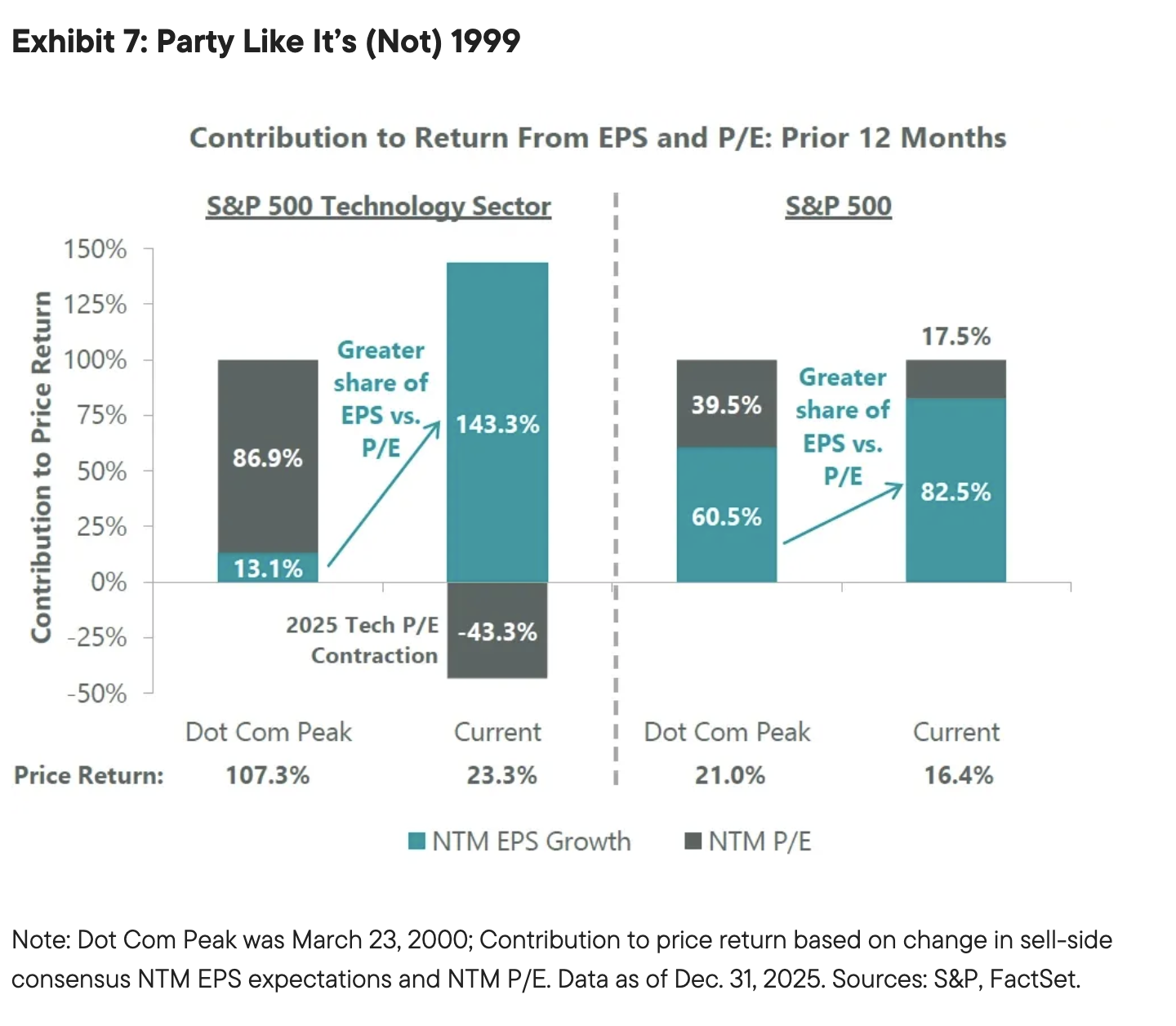

A fourth key distinction between the late 1990s and 2025 is what has been powering the equity market higher. During the final surge of the dot-com bubble, price to earnings (P/E) expansion was the primary driver of upside, a stark difference from 2025’s improving earnings per share (EPS) expectations-powered rally. Within the technology sector specifically, this year’s 23.3% price move was more than fully driven by improving EPS expectations, while multiples contracted and actually detracted from returns. Similarly, over 80% of the S&P 500 Index’s price return in 2025 was driven by improving fundamentals (aka earnings). This illustrates that market participants today are engaging in less speculative behavior as compared with the heyday of the dot-com bubble.

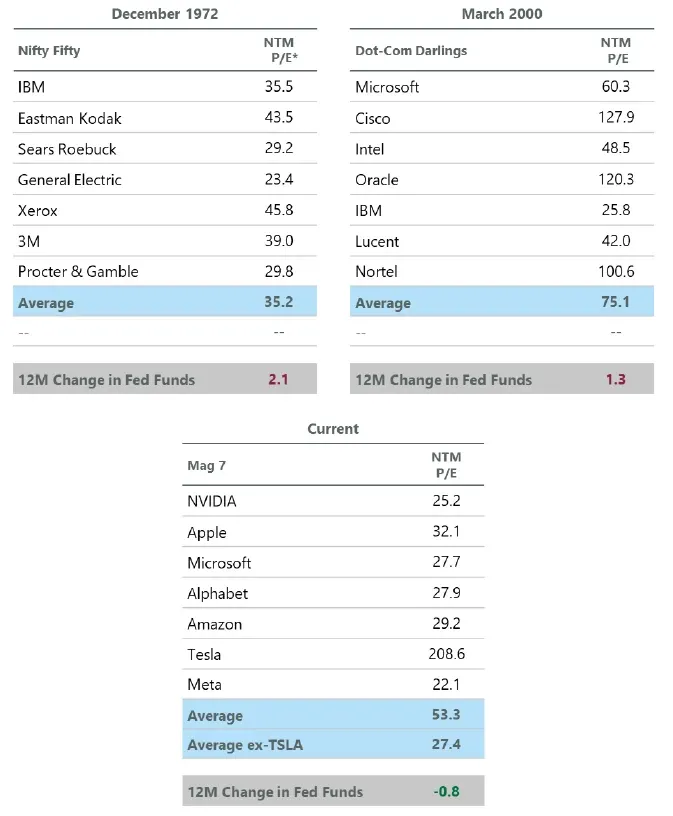

An additional sign that investors are behaving less exuberantly than in past bubbles comes from the lower valuation multiples assigned to today’s market darlings. The Magnificent Seven currently trade at 53.3x as a group, in the ballpark of what was seen during the peak of the Nifty Fifty and dot-com bubbles. However, a large portion of the current valuation is driven by Tesla; a “Magnificent Six” or Magnificent Seven ex-Tesla trades at a less lofty 27.4x, which bears far less resemblance to former speculative manias.

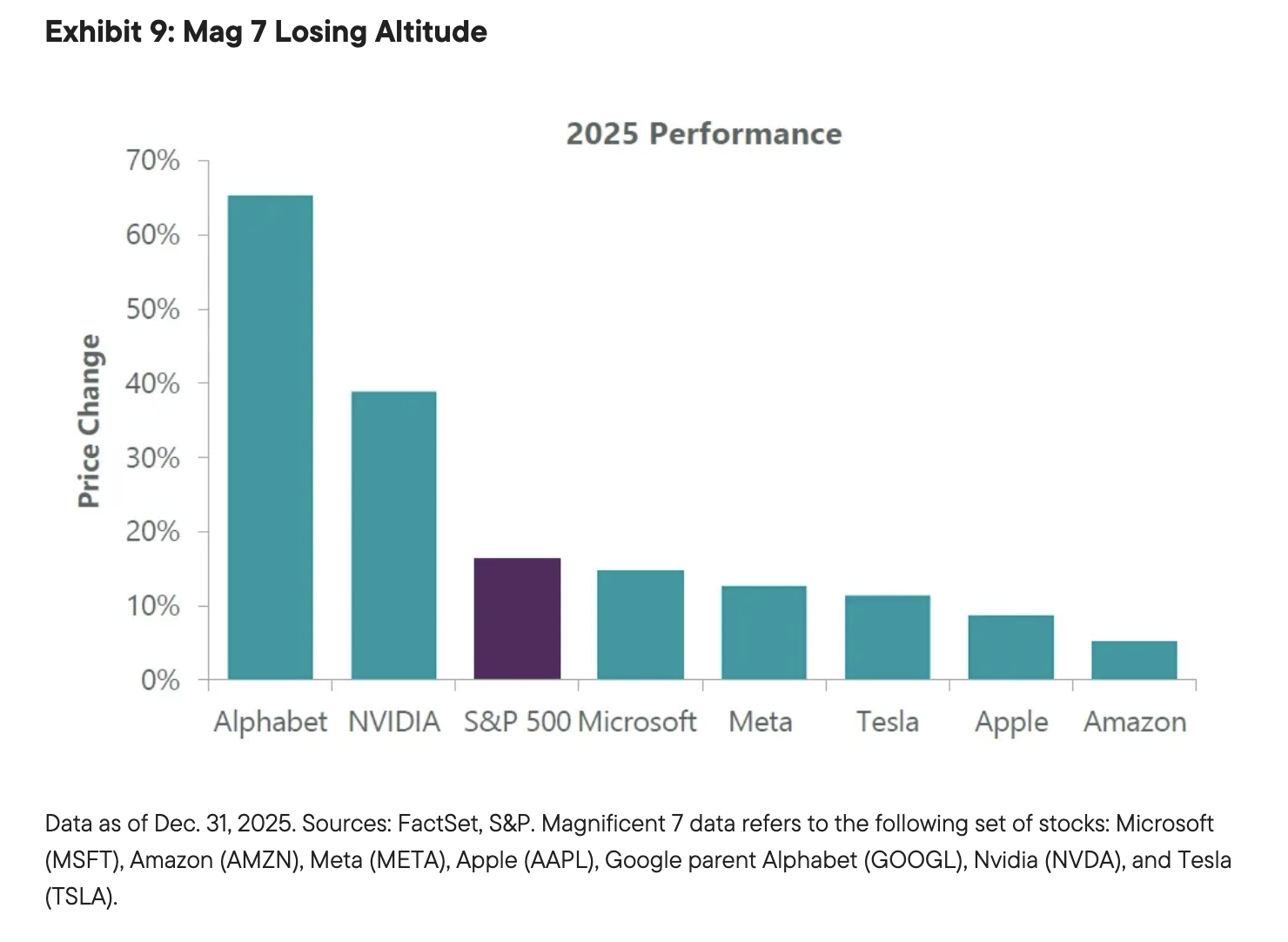

Part of this excitement may be due to the Magnificent Seven’s superb earnings over the past three years. However, we continue to anticipate a rotation in leadership as earnings delivery broadens in 2026. Third-quarter earnings season was encouraging on this front, with US companies largely reporting robust earnings and equities beginning to price this dynamic during the fourth quarter of this year. Given the hype around AI, it may surprise some to learn that, among the Magnificent Seven, only Google and Nvidia outperformed the S&P 500 in 2025. We also believe there is further room to run for this trade, which should be a tailwind for active stock pickers who can navigate the concentration risks associated with these recent winners.

The market’s great paradox

A comprehensive comparison of today’s backdrop and the final hurrah of the dot-com era shows more differences than similarities at this point. While valuations are elevated, we believe equities will “grow into the multiple” in 2026 with strong earnings fueled by ongoing AI capex strength, as well as fiscal and monetary stimulus. Additional upside could come from deregulation, AI-related productivity gains and further labor cost moderation, the latter of which could also open the door to additional Fed easing. Although AI will disrupt labor markets to some degree, we believe the impact will be more like the jobless recovery that followed the dot-com bubble with weaker job gains (50k-75k per month) as opposed to a recession. Additionally, AI should contribute to a disinflationary backdrop that should be bullish for financial assets.

Although it may feel at times like the markets are partying like it’s 1999, we believe the eventual hangover that will follow (such as in 2000-2003) remains further on the horizon. With this in mind, we are reminded of a quote from famous investor William O’Neil: “It is one of the great paradoxes of the stock market that what seems too high usually goes higher and what seems too low usually goes lower.” While the dot-com bubble does have some parallels to the present, it is important to also consider the risks from sitting on the sidelines during periods of large technological change. As such, we remain buyers of dips should any arise in the coming months.

Definitions

The ClearBridge Recession Risk Dashboard is a group of 12 indicators that examine the health of the US economy and the likelihood of a downturn.

The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the United States.

The One Big Beautiful Bill Act of 2025 is a US federal statute passed by the 119th United States Congress containing tax and spending policies that form the core of President Donald Trump's second-term agenda. The bill was signed into law by President Trump on July 4, 2025.

Capital expenditure (capex) refers to investment spending in long-term assets (fixed assets). These expenditures include new buildings, machinery, and other equipment needed for an organization's day-to-day operations. Most companies use capex financing to fund their long-term investments.

Free cash flow (FCF) is the cash a company generates from operations after accounting for the cash outflows required to support and maintain its capital assets.

Earnings per share (EPS) is the portion of a company's profit allocated to each outstanding share of common stock. An index EPS is an aggregation of the EPS of its component companies.

The price-to-earnings (P/E) ratio is a stock's (or index’s) price divided by its earnings per share (or index earnings). The forward P/E ratio is a stock’s (or index’s) current price divided by its estimated earnings per share (or estimated index earnings), usually one-year ahead.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Large-capitalization companies may fall out of favor with investors based on market and economic conditions. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

US Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the US government. The US government guarantees the principal and interest payments on US Treasuries when the securities are held to maturity. Unlike US Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the US government. Even when the US government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© ClearBridge Investments

Read more commentaries by ClearBridge Investments