The Wall Street consensus forecast for 2026 earnings growth is strong by historical standards. Analysts are giddy and projecting another year of double-digit growth in S&P 500 earnings per share (EPS). FactSet’s most recent data showed an expected 2026 earnings growth rate for the S&P 500 of about 15 percent. That is well above the long‑term average of roughly 8–9 percent. If FactSet is correct, such would mark a third consecutive year of double‑digit earnings gains.

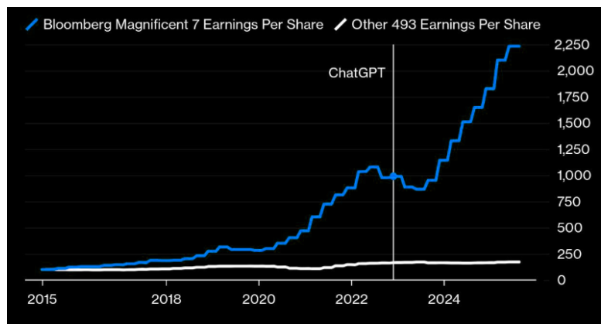

Notably, the 2026 earnings assumptions are driven by the continued strength in the large technology and communications sectors. With those sectors dominated by the “Magnificent Seven,” it is hoped that they continue to contribute disproportionately to earnings growth. Those seven companies alone are forecast to grow earnings strongly once again. As shown, since 2018, there has been very little earnings growth from the bottom 493 companies.

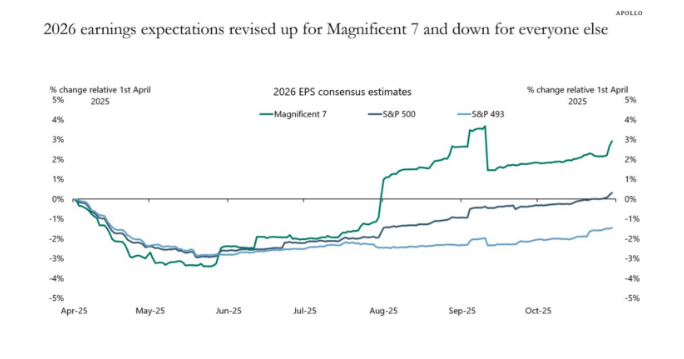

Furthermore, despite the exuberance from Wall Street analysts regarding the overall index, expectations for 2026 earnings improved only for the top seven companies, while estimates for the bottom 493 have seen virtually no change since April.

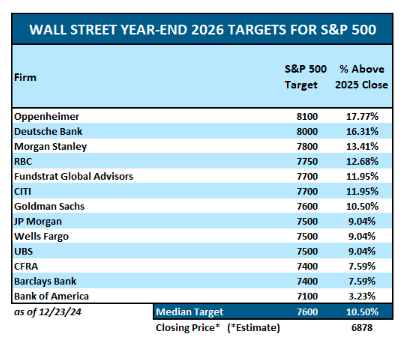

Notably, these 2026 earnings forecasts are influenced by broader market return expectations. For example, many sell‑side strategists are assigning S&P 500 price targets that embed this earnings growth outlook. For example, as shown, current analysts’ forecasts imply that the index could rise between 8% and 17% in 2026. However, to justify that price increase (P), they assume an earnings (E) rate that keeps valuations (P/E) stable.

In other words, Wall Street hopes that earnings expansion rather than valuation multiples will drive market gains. However, over the last 5 years, multiple expansions led the charge as earnings growth failed to keep pace.

This optimism currently comes against a backdrop of a resilient U.S. economy. GDP growth forecasts center on continued expansion, albeit modest, with some estimates indicating annual growth of around 2 percent. That stability reinforces the case for continued corporate profitability. One support is fiscal policy from the recently passed OBBB, which provides tax relief and deregulation. Still, this type of projected growth is not guaranteed. As such, investors should recognize that earnings forecasts reflect analysts’ estimates at a given moment, which is always “bullish” to ensure that Wall Street can sell you products.

As we previously reported, the accuracy of analysts’ estimates is far down their list of concerns.

However, instead of focusing on Wall Street estimates, which will likely be revised lower in the future, investors should pay closer attention to what will drive 2026 earnings growth.

The Link Between Economic Growth, Profit Margins, and Earnings

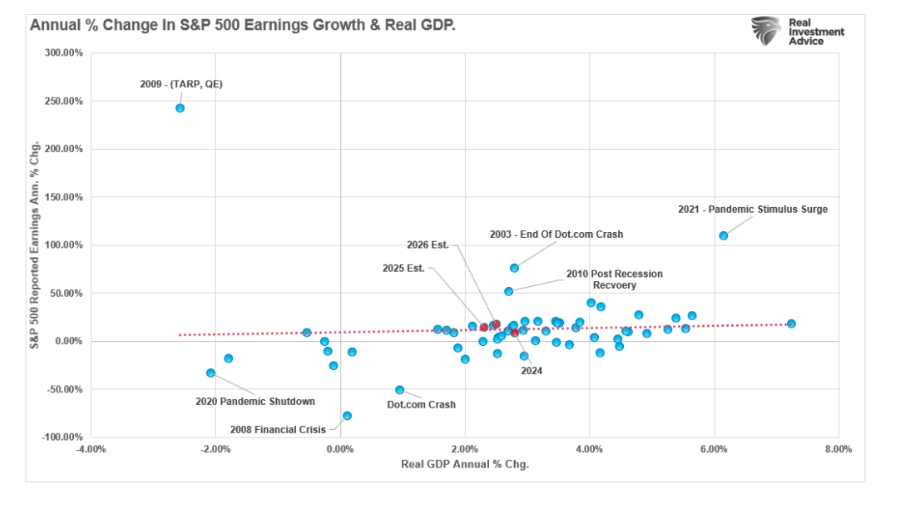

Earnings growth does not occur in a vacuum. Corporate profits are inherently a function of economic growth, pricing power, input costs, and labor dynamics. If the economy grows at a moderate pace, as most anticipate, corporate revenues are expected to expand in line with broader demand. Many forecasts for GDP growth in 2026 hover around the 1.8% to 3% range. Those estimates are driven partly by fiscal support and ongoing investment in sectors such as technology and infrastructure. This modest expansion provides a supportive backdrop for 2026 earnings, as historical correlations suggest. (Outliers are historically a function of recovery or impact from a crisis or recession)

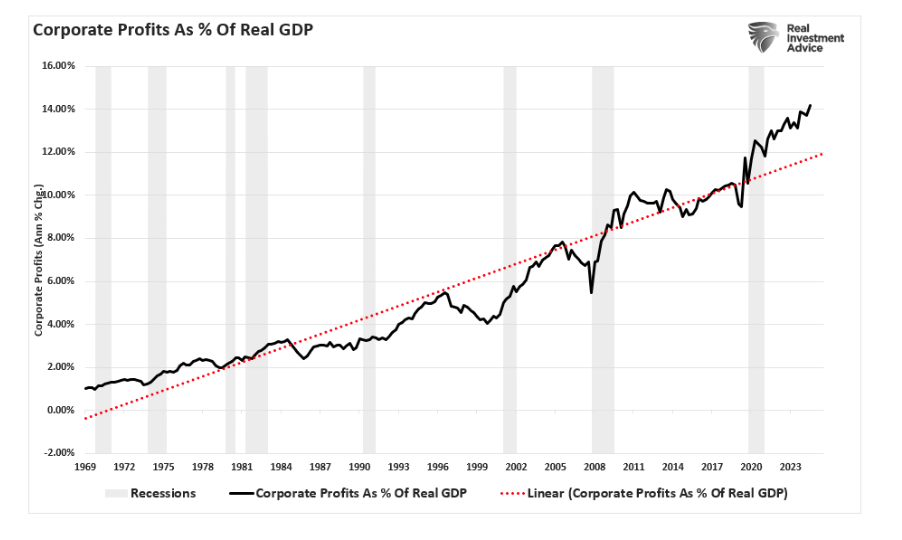

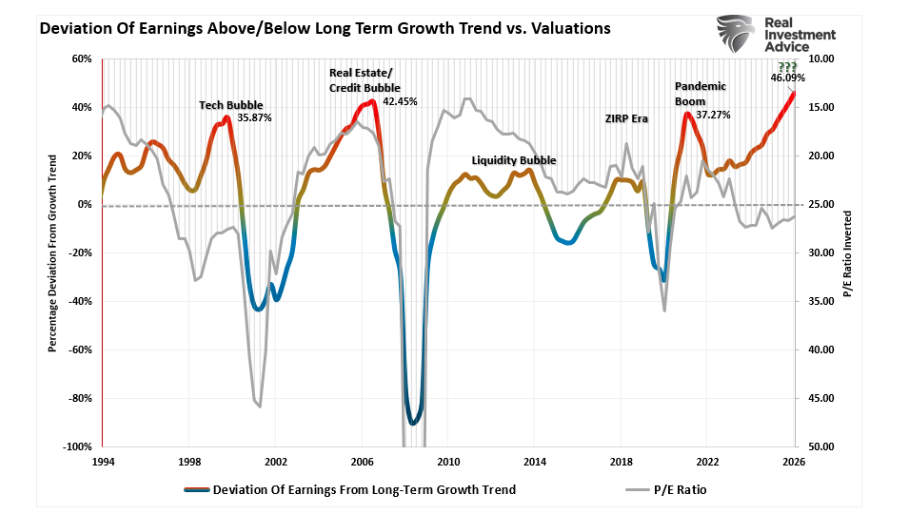

At the same time, corporate profit margins in the S&P 500 are currently very high relative to historical norms. According to FactSet, the estimated net profit margin for the index is near its highest level since tracking began in 2008, at around 13.9%, compared to a ten-year average of 11%. We also see this in corporate profits as a percentage of real economic growth, which is at its highest deviation from the long-term profit growth trend in history.

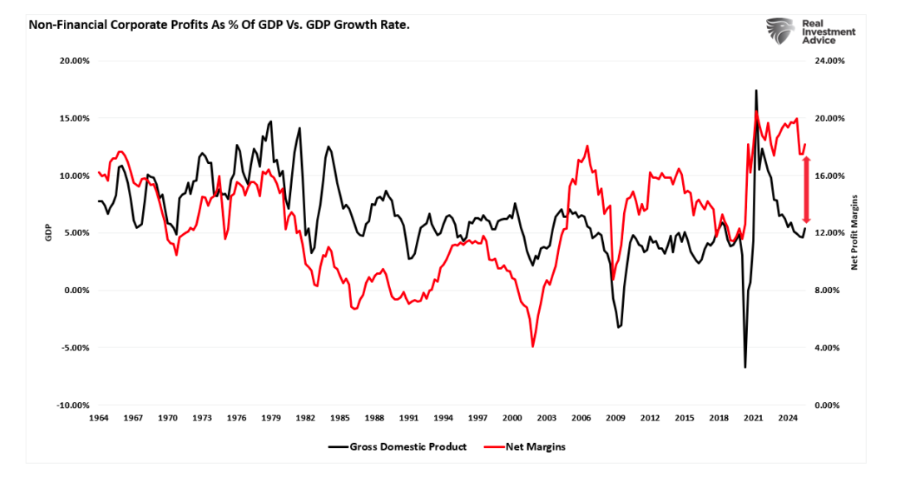

Elevated margins suggest companies have maintained pricing power and cost control, even amid inflationary pressures. But these high margins raise questions about sustainability. Given the supply-demand imbalances (more demand than supply), which allow for elevated margins, it is worth noting that as the economy returns to more normalized growth rates, profit margins tend to follow. Such is particularly the case as inflation pressures subside, employment weakens, and competitive forces erode pricing power. Margin compression has historically dampened earnings growth. Even if revenues are rising, if rising costs cannot be passed on to consumers, they eat into profits.

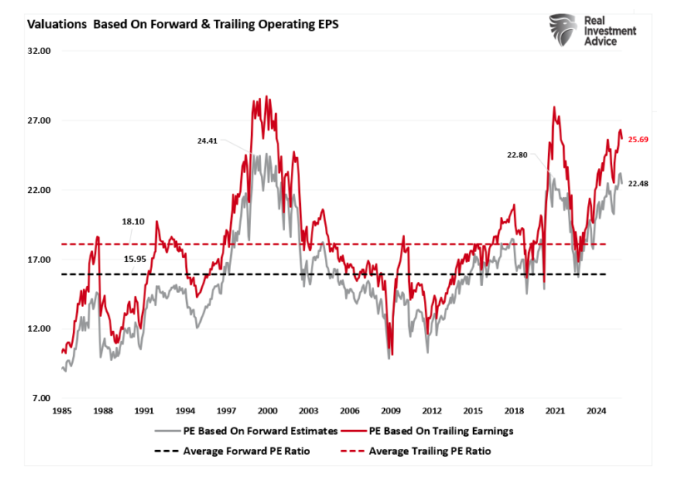

Valuations also matter. As noted above, the current price-to-earnings ratio for the S&P 500 remains above historical averages, at approximately 22x forward earnings. Those valuation levels are also well above the five- and ten-year averages. In other words, the market is pricing in continued earnings momentum. Therefore, if growth slows toward historical norms or margins compress, elevated valuations will mean even modest earnings disappointments could result in share price declines rather than gains.

The most considerable risk to investors is that the 2026 earnings estimates, which are the most deviated above its 125-year growth trend, disappoint, and the markets reprice lower. As shown, historically, when earnings become deviated from actual economic activity, the mean reversion process is not kind to investors.

In this context, understanding the mechanics behind earnings expectations becomes critical. Analysts’ expectations for robust earnings growth assume that these economic and profit margin conditions remain supportive; however, any divergence from this script increases the risk of downward earnings revisions, valuation compression, and market volatility.

Analyst Optimism, Valuation Risk, and Structural Challenges

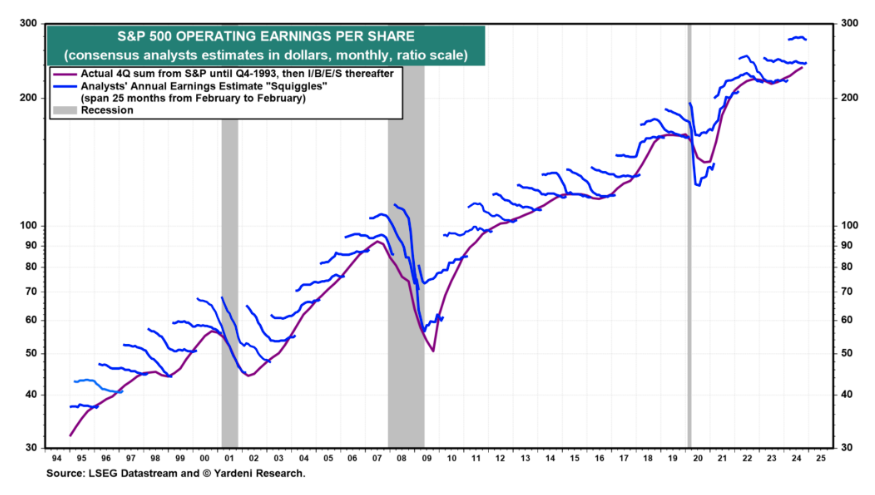

One of the enduring themes in earnings forecasting is the bias toward optimism early in the forecast cycle. Analysts typically issue forward earnings estimates at the start of a year and revise them lower later as actual economic and corporate results become available.

As noted above, such optimism is partly behavioral and partly structural; analysts often have incentives tied to institutional clients who favor growth narratives. When growth assumptions falter due to weaker demand, rising costs, or unforeseen macroeconomic shocks, analysts will typically revise their estimates downward. This creates the familiar pattern of “estimates drifting lower” over the course of the reporting year.

The current earnings growth consensus for 2026 is no exception. While forecasts indicate roughly 12.5–15% EPS growth, several structural vulnerabilities underpin these expectations. As discussed, profit margins are at elevated levels, which makes sustaining margin levels challenging in an environment where employment is declining.Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice