If you’ve been around anyone under the age of 25 lately, you have likely been exposed to the “Six-Seven” phenomenon, whereby kids react excitedly upon hearing or seeing the numbers 6 and 7 in sequence. It can come from anywhere at any time - a teacher reading numbers, a football score, a seemingly harmless estimate by an unwitting individual (“about 6 or 7”) – but once the fire is lit it sends kids into a frenzy, with them enthusiastically repeating “6-7, 6-7!” while quickly moving their hands up and down. It’s remarkable how frequently this occurs and how quickly it can become tiresome. We know people that have banned the phrase in their house. The craze apparently originated from a line in a rap song and a subsequent video post by an NBA player and grew out of control from there. Perhaps in a few weeks it will be considered passe by those that determine such things. We can hope.

Stocks, as measured by the S&P 500, eked out a modest gain in the quarter, making 2025 another year of 15%+ returns – the sixth such year in the past - you guessed it - seven. This has been an incredible run for stocks, propelled by rising corporate profit margins and a healthy economy. There hasn’t been an extended bear market in over 15 years, which we believe has fostered a buy-the-dip mentality and engendered complacency among some market participants, as evidenced by overly bullish positioning, high interest in expensive stocks, and a willingness to look the other way on issues that would ordinarily raise concern.

Despite the consumer finally showing signs of fatigue, GDP continues to grow at a strong rate, a slowly rising unemployment rate notwithstanding. It’s possible that the historically massive investment in artificial intelligence has been propping up the economy. The AI trade showed some cracks in the quarter though. The corporate bonds of some heavy investors in AI infrastructure sold off, signaling that it may be time for them to exercise some spending discipline. Some AI equity plays fell out of favor as well, after huge upswings. CoreWeave fell by about half, while Oracle and Soundhound gave back about 1/3 of their value in the quarter. But many AI stocks have continued their ascent, as the momentum trade exhibited some volatility but stayed intact. According to Empirical Research Partners, other than what occurred in 1999, the current nine-month relative return of momentum stocks is unprecedented in the last 70 years. In other words, the winners have kept winning to an almost unprecedented degree.

The characteristics of the winning stocks have been noteworthy. In some parts of the market, companies with negative earnings, fast sales growth, less stability, or low interest coverage have not just outperformed but done so to an unusually large degree, based on data from Empirical. What’s interesting about this is that historically, each of these factors tend to augur underperformance. It’s counterintuitive, but yes, rapid sales growth at a company, on average, leads to subpar prospective returns. So, this has been a very unusual time in terms of the makeup of some winning stocks. The flip side is that the factors that usually work, such as valuation, have not worked as well – at least in some segments, such as technology.

The rapid rise in the share prices of unprofitable tech companies has stalled but has yet to fall off a cliff. The current price action reminds us of the “disruptive innovation” funds in 2021. Like the unprofitable tech companies of 2025, these funds enjoyed a swift climb that was followed by a significant but not back-breaking correction and some sideways volatility. Then in late 2021 and early 2022, these funds collapsed. We think the unprofitable tech companies of today may suffer a similar fate in 2026.

We wrote on multiple occasions this year about the phenomenon of floundering companies shifting their strategy to that of cryptocurrency treasury, thereby seemingly creating billions of dollars of value purely through this change in strategy. Not surprisingly, that game appears to be in the process of ending, as many of these stocks fell by 50% or more in the fourth quarter, while Bitcoin lost about 24%.

The Federal Reserve enacted two more rate cuts in the quarter in spite of inflation that remains above target. The consensus is that there will be more cuts in 2026, as Chair Powell gives way to his yet-to-be-named successor, who is almost surely to be highly dovish (i.e. favorable to cutting rates), as he or she will be nominated by President Trump, a vocal proponent of easier monetary policy.

It feels like a significant portion of the stock market, and the private market for that matter, is dependent on the fate of AI. In addition to the various technology companies that are exposed, such as semiconductors, there are many industrial and utility enterprises that have been beneficiaries of the build-out. And as we alluded to earlier, the economic activity brought on by AI investment has been important. There is no doubt that AI is here to stay and will become an increasingly important part of our lives. The question though is how much investment will end up being misbegotten. The owner of ChatGPT, Open AI, which is private, has committed to investing over $1 trillion in infrastructure and is talking about going public with a valuation close to $1 trillion. Its sales in 2025 are running at about $13 billion. That equates to a P/S of 77x, an extremely high level, especially considering, for the time being at least, it has lost its performance lead to Google, a company with tremendous built-in advantages. Furthermore, if folks like Open AI decide to stop investing, or dial back their spending plans significantly, either because they aren’t pleased with the expected return of such projects or because the capital markets have dried up, it would have serious downstream effects as well. Caution appears warranted.

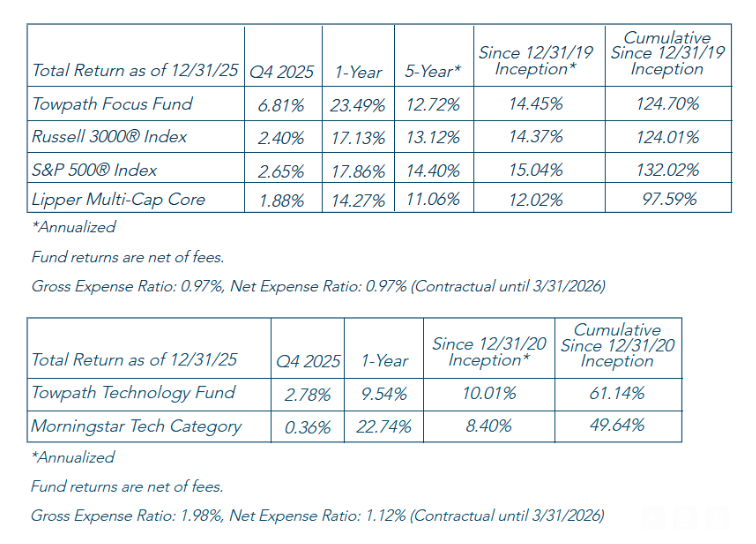

As we complete our sixth year and move into our seventh (there it is again), it’s interesting to look back. For the majority of that six-year period, we have had a conservative or defensive portfolio positioning, all while the market generally has roared. If you had told us six years ago that the market would do as well as it has, with growth, momentum, and mega-caps leading the way, we would have expected significant underperformance from our portfolios. So, the fact that we are, since inception, in line with the Russell 3000 Index and marginally behind the S&P 500 Index, during a period in which it has been extraordinarily difficult for active managers to beat those benchmarks, is, in a sense, a win, though perhaps we deserve criticism for being too conservative. Our record against other managers is strong, as we have outperformed the vast majority of our peers, whether taken from the Lipper Multi-Cap Core Average, the Morningstar Large Value Category, or the Morningstar Large Blend Category, all while exhibiting lower downside risk. Looking forward, with many measures of market valuations at or near all-time highs, we are positioned relatively defensively, which we believe should allow us to better weather a storm than our competitors might.

Mark Oelschlager, CFA

Oelschlager Investments

The performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please call Shareholder Services at 1-877-593-8637 to obtain performance data current to the most recent month-end.

To determine if this Fund is an appropriate investment for you, carefully consider the Fund's investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Fund's Prospectus which may be obtained by calling 1-877-593-8637 or visiting our website at www.oelschlagerinvestments.com. Please read it carefully before investing.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT INFORMATION: Mutual fund investing involves risk, including possible loss of principal.

The statements and opinions expressed are those of the author and do not represent the opinions of Towpath Funds or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell.

This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

The Russell 3000 Index is a market-capitalization weighted index measuring the performance of the 3,000 largest U.S. companies based on total market capitalization. The S&P 500 Index is a commonly recognized market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. The Morningstar US Technology index measures the performance of companies engaged in design, development, and support of computer operating systems and applications, manufacturing of computer equipment, data storage products, networking products, semiconductors, and components. Unlike mutual funds, an index does not incur expenses. If expenses were deducted, the actual returns of an index would be lower. You cannot invest directly in an index.

Click here to view Towpath Focus Fund Top 10 Holdings as of the most recent quarter-end. Click here to view Towpath Technology Fund Top 10 Holdings as of the most recent quarter-end. Current and future portfolio holdings subject to change.

CFA is a registered trademark of the CFA Institute.

Towpath Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Towpath Funds are separate and unaffiliated.

© Oelschlager Investments

Read more commentaries by Oelschlager Investments