Key Takeaways

- Emerging markets (EM) equities enter 2026 supported by a weaker U.S. dollar, improving fundamentals, and broad country and sector leadership.

- The EM opportunity set has broadened beyond technology, with durable growth drivers emerging across AI infrastructure, power, defense, healthcare, and advanced manufacturing.

- Improving macro conditions, narrowing valuation gaps, and still-light investor positioning suggest continued scope for capital reallocation toward high-quality EM companies across regions.

EMs are entering 2026 from a position of renewed strength. A weakening U.S. dollar, improving fundamentals, and broadening country and sector leadership have created a favorable backdrop for investors—and we believe EM equities continue to offer an efficient gateway to global secular themes such as AI, power infrastructure investment, healthcare innovation, changing consumer patterns, and manufacturing upgrades.

Performance Highlights From 2025

After more than a decade of underperformance, EM equities outpaced developed market (DM) equities in 2025. The MSCI Emerging Markets Index rose 30% year to date as of November 30, compared with 17% for the MSCI USA Investable Market Index (IMI), marking EM’s strongest relative year since 2009.

Gains were widespread across regions: North Asia led, with Korea and Taiwan benefiting from AI-related semiconductor demand, and China’s robust exports and renewed focus on innovation driving its performance. Elsewhere, Latin America and South Africa rebounded amid policy easing, a weaker dollar, and stronger commodity prices.

Sector performance also broadened beyond information technology to include materials, industrials, and healthcare, underscoring that the opportunity set in EMs now extends beyond technology.

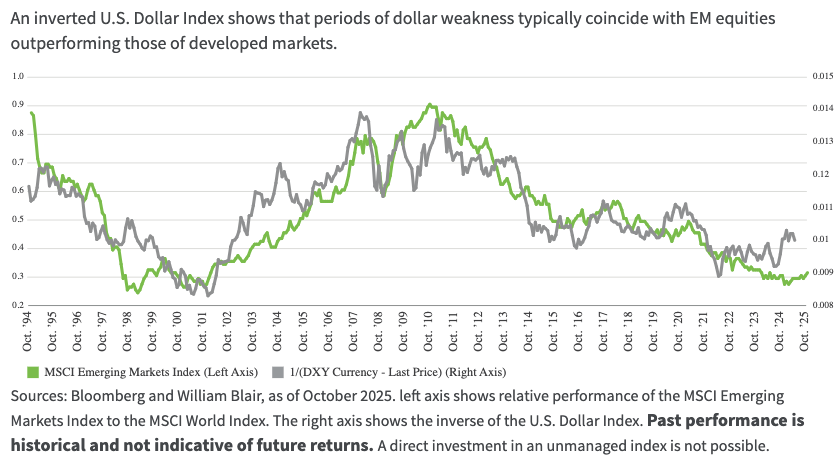

EM Relative Performance Strengthened When the U.S. Dollar Weakened

A key driver of renewed EM performance has been a sustained shift in global macro conditions. EM markets historically exhibit a strong inverse relationship with the U.S. dollar, and 2025’s weakening U.S. dollar trend provided a significant tailwind. The strong negative correlation between EM relative returns and dollar strength highlights the importance of currency cycles to EM valuations.

The rerating of EM equities stands on a firm foundation. After U.S. President Trump’s April “Liberation Day” announcement of sweeping tariffs triggered a brief bout of volatility, investor flows into EM equities turned positive and have remained steady since. Institutional positioning, however, is still relatively light despite the performance recovery, suggesting continued room for capital reallocation. At the same time, heightened concentration risk in U.S. markets has likely strengthened investors’ motivation to diversify globally. The United States now represents roughly two-thirds of the MSCI All Country World Index by market capitalization, or nearly three times its share of global gross domestic product (GDP).

Broadening Drivers: AI, Power, and Defense

The AI investment cycle is redefining the global landscape, and EMs are deeply embedded in the AI growth story. Markets such as Taiwan and Korea remain integral to the global semiconductor and server-component supply chains, providing much of the hardware required for AI applications. More than 20% of total EM revenue is expected to be AI-related in 2029, according to Goldman Sachs, and we believe the ongoing AI capex cycle should remain a durable source of growth across North Asia.

While U.S. firms have captured a disproportionate share of the AI-related market-cap expansion, EMs play a central role in the infrastructure buildout. This is most pronounced in semiconductors, memory, and data-center power systems. China’s domestic AI initiatives, including the emergence of locally developed models, have also accelerated technology investment, placing the country roughly two years behind the United States in the AI investment cycle, in our view.

Rising AI-driven energy demand has created parallel opportunities in EM power infrastructure. Korean firms such as Hyundai Electric and Hyosung Heavy are key suppliers of transformers and grid components, while Indian manufacturers are expanding renewable-energy and transmission capacity to meet industrial demand.

Defense spending has also emerged as a durable global theme. Korea’s Hanwha Aerospace and Hyundai Rotem, along with Turkey’s Aselsan Elektronik, have become major exporters of defense systems to Western Europe and the Middle East, while Indian defense companies such as Bharat Electronics and Hindustan Aeronautics are benefiting from increased domestic defense budgets and import substitution. The Korean shipbuilding sector, through HD Hyundai Heavy Industries and related firms, is participating in both liquefied natural gas (LNG) infrastructure and potentially the U.S. naval upgrade program, reinforcing its industrial relevance.

Healthcare is another source of structural growth. After several years of weakness, Chinese and Indian contract research and contract development and manufacturing (CRO/CDMO) firms are seeing renewed demand linked to biotechnology investment and GLP-1 production. As domestic research-and-development (R&D) ecosystems mature, healthcare innovation is becoming a more enduring contributor to EM earnings quality.

Outlook for 2026: Quality Growth in a Broader EM Cycle

After several years of relative underperformance, the valuation gap between quality and value within EM has begun to narrow as investors refocus on sustainable earnings and resilient business models. Historically, periods in which quality-oriented EM equities have lagged the index have been short-lived.

As inflation moderates and monetary policy across several EM economies shifts toward easing, market leadership is likely to broaden beyond early-cycle beneficiaries. A U.S. Federal Reserve pivot to rate cuts and a softer dollar would create room for many EM central banks to lower rates without undermining currency stability, reinforcing domestic growth prospects and supporting asset valuations. Investor sentiment has improved meaningfully, with renewed inflows into EM equities and bonds reflecting rising confidence in the durability of this cycle.

The macro backdrop remains constructive. EM economic growth is expected to continue outpacing that of developed markets, supported by improving fiscal balances, moderating inflation, and an increasingly stable global policy environment. As fundamentals regain influence, we believe corporate earnings momentum should strengthen, particularly in markets in which high real yields previously constrained growth.

From a portfolio perspective, we believe investors could benefit from maintaining core exposure to high-quality manufacturing companies in North Asia and India, two markets positioned to capture the next wave of AI and industrial spending. In Latin America, opportunities are emerging in quality growth names with attractive valuations in Brazil and Mexico as monetary and fiscal conditions improve. Meanwhile, exposure to defensive quality companies, particularly in healthcare and select areas of the consumption-related sector, can serve as portfolio ballasts and provide resilience against market volatility.

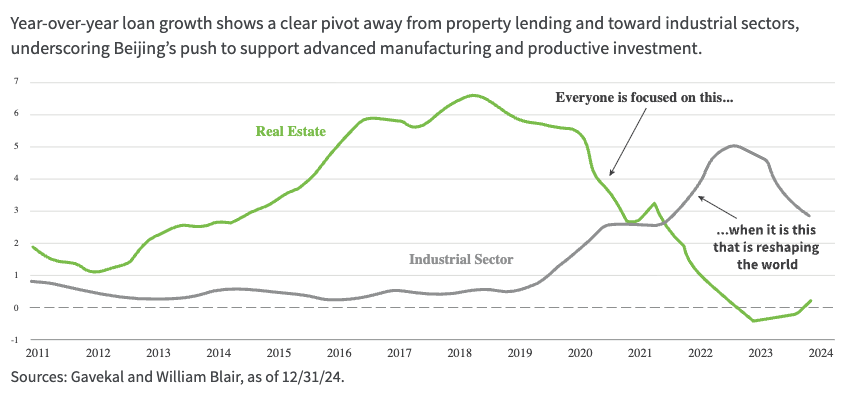

China: From Property Drag to Industrial Upgrade

China’s economy continues its transition from property-driven growth to advanced manufacturing. The government’s massive fiscal support program has prioritized industrial upgrading and technological self-reliance. Bank lending has shifted accordingly, with financing to the property sector declining sharply, while credit to manufacturing, semiconductors, robotics, and biotech has surged.

China’s Credit Allocation Shifts From Real Estate to Industry

Although domestic consumption remains subdued, rising exports to EMs are helping offset trade frictions with the West. China’s dominance in electric vehicles (EVs), batteries, and solar power continues to anchor its manufacturing edge, while infrastructure investment and targeted fiscal programs provide a steady policy backstop. Despite lingering structural headwinds and geopolitical risks, we believe current valuations are attractive, and point to potential reengagement from Western investors, which could have an outsized impact on performance.

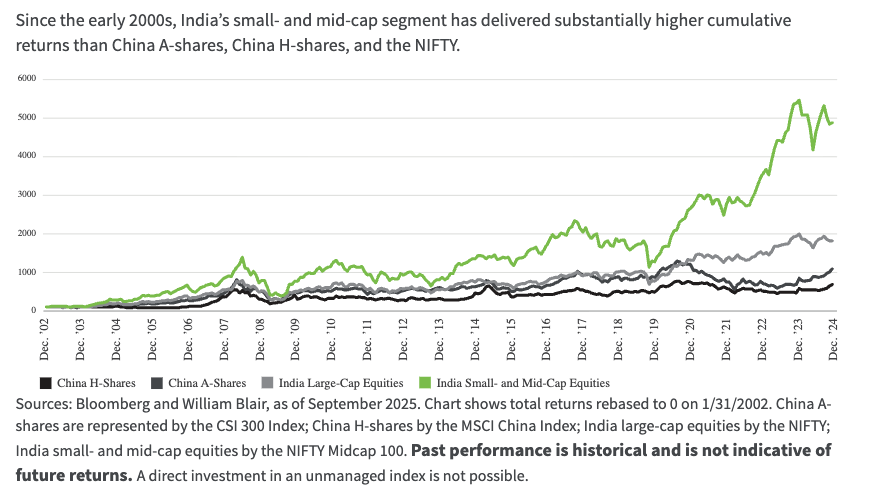

India: A Strong Engine Amid Consolidation

India’s market lagged in 2025 as high valuations, modest earnings growth, trade tensions with the United States, and limited AI exposure weighed on performance. Yet India’s structural story remains compelling. The country’s ongoing infrastructure buildout continues to drive growth, supported by sustained public investment and pro-manufacturing initiatives, such as the Make in India and Production Linked Incentive programs.

India’s Small- and Mid-Cap Stocks Have Outperformed Major Asian Equity Markets

Consumption and the deepening of the financial system continue to serve as key growth engines. Low household leverage and a young, expanding workforce underpin steady demand for credit and durable goods, while rising incomes support the shift from staples to discretionary spending. India’s economy is forecast by Morgan Stanley and World Bank to grow at roughly twice the pace of global GDP over the medium term.

Despite near-term consolidation, we believe India’s encouraging long-term equity story remains intact. Over the past decade, Indian small- and midcap equities have far outperformed both the NIFTY and Chinese benchmarks, illustrating the country’s depth of entrepreneurial opportunity. Corporate earnings are expected to strengthen in 2026, supported by policy continuity, fiscal stimulus, and an improving macro backdrop.

Although valuations are still somewhat elevated, we believe the combination of reform momentum, expanding manufacturing capacity, and resilient consumer demand continues to reinforce India’s position as one of the most durable growth stories in EMs.

Latin America: Turning a Corner on Rates and Reform

Brazil and Mexico headline a Latin American recovery story centered on improving monetary conditions and fiscal pragmatism. Brazil’s benchmark interest rate was 15% as of November 2025, its highest level in nearly two decades. However, its disinflation trend has strengthened, and analysts expect a gradual easing cycle to commence in early 2026. Despite the drag from high borrowing costs, Brazil’s macroeconomic backdrop remains stable, and lower rates should help revive credit growth and corporate investment.

Mexico continues to benefit from nearshoring: roughly 85% of its exports enter the U.S. tariff-free under existing trade agreements. Foreign direct investment reached a record high in the first half of 2025 as manufacturers continued to relocate supply chains closer to the U.S. market. Elsewhere, Argentina’s market remains small and illiquid, though scope for renewed policy reforms under President Javier Milei’s administration have drawn cautious optimism.

UAE and South Africa: Standouts in EMEA

In Europe, the Middle East, and Africa (EMEA), we believe United Arab Emirates (UAE) equities offer a compelling case supported by strong macro fundamentals, geopolitical stability, and positive investor sentiment. The economy is projected to grow at 4% to 5% annually, driven by diversification into non-oil sectors, such as technology, renewable energy, and tourism. Real estate continues to benefit from robust demand and rising prices, while financial institutions enjoy healthy credit growth and digital transformation. Infrastructure spending on transport, logistics, and energy projects underpins long-term growth, reinforcing the UAE’s position as a resilient and diversified market in the region.

Meanwhile, South Africa’s market rebounded in 2025, supported by improved political sentiment, a steadier macro backdrop, and stronger commodity prices. With valuations still below historical averages and sectors like mining, financials, and consumer staples positioned to benefit from cyclical recovery, we believe South Africa offers selective opportunities for long-term investors seeking exposure to EMs with commodity leverage.

Conclusion: The Case for Sustained EM Leadership

EMs now account for 60% of global population and 40% of global GDP (driving 70% of real growth), but represent only 11% of the MSCI ACWI weight. They also remain underweighted in global portfolios, underscoring the long-term potential for reallocation.

With the U.S. dollar in retreat, fundamentals improving, and new growth engines emerging across regions, we believe the case for sustained EM leadership is gaining traction. EMs are home to many of the world’s most competitive companies, many of which are global leaders in semiconductors, energy infrastructure, and healthcare innovation.

As capital redistributes, we expect investors reward proven profitability and quality, and we believe EM equities are poised to continue their shift from potential to performance.

Todd McClone, CFA, partner, is a portfolio manager on William Blair’s global equity team.

Ian Smith, partner, is a portfolio manager on William Blair’s global equity team.

The CSI 300 Index is a market-capitalization-weighted index that consists of 300 A-share stocks traded on the Shanghai and Shenzhen exchanges. The MSCI All Country World Index (ACWI) captures large- and mid-cap representation across developed and emerging markets. The MSCI Emerging Markets (EM) Index captures large- and mid-cap representation across 27 EMs. The MSCI China Index captures large- and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (such as ADRs). The MSCI USA Investable Market Index (IMI) captures large-, mid-, and small-cap companies across the U.S. equity market. The NIFTY (formally NIFTY 50) is India’s main stock market benchmark. It tracks the 50 largest and most liquid companies listed on the National Stock Exchange of India (NSE). The NIFTY Midcap 100 Index tracks the performance of the 100 mid-sized companies listed on the National Stock Exchange of India.

References to specific companies are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. The securities discussed do not represent all securities purchased, sold, or recommended for clients. It should not be assumed that any investment in the securities referenced was or will be profitable. As of the date of publication, William Blair Investment Management held positions in the following companies referenced in one or more of its investment strategies: Aselsan Elektronik, Bharat Electronics, Hanwha Aerospace, HD Hyundai Heavy Industries, Hindustan Aeronautics, Hyundai Electric, Hyosung Heavy, Hyundai Rotem. Companies discussed but not listed were not held by William Blair Investment Management. Holdings are subject to change without notice.

Any investment or strategy mentioned herein may not be appropriate for every investor. There can be no assurance that investment objectives will be met. Products and services listed are available only to residents of this jurisdiction and may only be available to certain categories of investors. The information on this website does not constitute an offer for products or services, or a solicitation of an offer to any persons outside of this jurisdiction who are prohibited from receiving such information under applicable laws and regulations. Nothing on this webpage should be construed as advice and is therefore not a recommendation to buy or sell shares.

Please carefully consider the William Blair Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus and summary prospectus, which you may obtain by calling 1-800-742-7272. Read the prospectus and summary prospectus carefully before investing. Investing includes the risk of loss.

The William Blair Funds are distributed by William Blair & Company, L.L.C., member FINRA/SIPC.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Different investment styles may shift in and out of favor depending on market conditions. Diversification does not ensure against loss.

Past performance is not indicative of future returns. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security.

William Blair Investment Management, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by William Blair