Compounding Opportunity

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEconomic outlook takeaways

-

Growth remains surprisingly resilient

After global growth withstood tariff pressures in 2025, the near-term outlook appears stronger, aided by AI-related capital spending and efficiency gains. Lower Chinese export prices have helped ease the shift in trade flows away from the U.S. -

Winners and losers drive “K-shaped” economic trends

In the U.S., capital-intensive companies deploying AI are better positioned, as are wealthier households that benefit from tech-driven stock market gains. Others are increasingly at risk of being left behind. Globally, trade frictions, AI adoption, and associated policy responses are driving divergence among countries. -

Global monetary and fiscal policies are moving in different directions

The U.K. and several emerging market (EM) economies with high real rates and limited fiscal space are likely to ease monetary policy more than the European Central Bank or Bank of Canada, where policy is already neutral. Fiscal policy is set to become more influential in China amid trade pressures, and in the U.S. where tax cuts will likely boost households and businesses.

Investment outlook takeaways

-

Bonds present compelling and durable opportunities

Active fixed income strategies delivered their best results in years in 2025, and the outlook for 2026 is just as compelling. The post-pandemic bond market repricing set up an extended period of attractive starting yields. Divergent economic conditions offer abundant avenues for active managers to generate alpha, or outperformance versus the broader market. Investors have a rare opportunity to increase quality and liquidity without giving up equity-like return potential – at a time when equity valuations have reached extremes. -

Use global diversification to help mitigate risks

Diverse economic and policy conditions across countries present investment opportunities in both developed markets (DM) and EM. Notably, several large EM economies offer significant real yield premiums over DM bonds – compensation for risks that are increasingly idiosyncratic and diversifiable rather than systemic. EM local currency bonds delivered strong returns in 2025 while providing crucial portfolio diversification at a time when DM correlations remain elevated. -

Choose investments carefully in a late-cycle credit environment

We favor high quality areas such as securitized credit and asset-based finance, which benefit from robust lending standards and strength among higher-income consumers. We are prioritizing security selection and reducing more generic credit and private corporate credit exposure.

Economic outlook: Dimensions of divergence

The Trump administration’s sweeping tax, trade, and immigration policy overhauls – including quadrupling the effective U.S. tariff rate – were widely expected to stifle global growth, trade and investment. In response, various DM and EM governments announced preemptive yet targeted fiscal measures to buffer the economic transitions, while central banks focused on downside risks.

It turns out that economic growth has been surprisingly resilient as these policy trends intersected with a new general-purpose technology: AI. The result has been a lasting expansion with notable divergence under the surface. “K-shaped” economic trends are apparent across households, companies, and regions. Indeed, those who are better positioned to benefit from the AI race and associated wealth effects are fueling growth.

Several key macro trends have unfolded:

- In the U.S., elevated competition has limited corporate pricing power and muted tariff-related price increases. Large companies are focusing on gaining market share by competing on price and absorbing tariff costs, fueling a productivity push to protect margins. Small and midsize labor-intensive companies exposed to trade sectors or immigration policy changes have been relative losers.

- To defend margins, companies accelerated AI adoption to manage labor costs. In the U.S., AI-related software and R&D investment accelerated, while data center investment, including structures, servers, chips, and other components doubled.

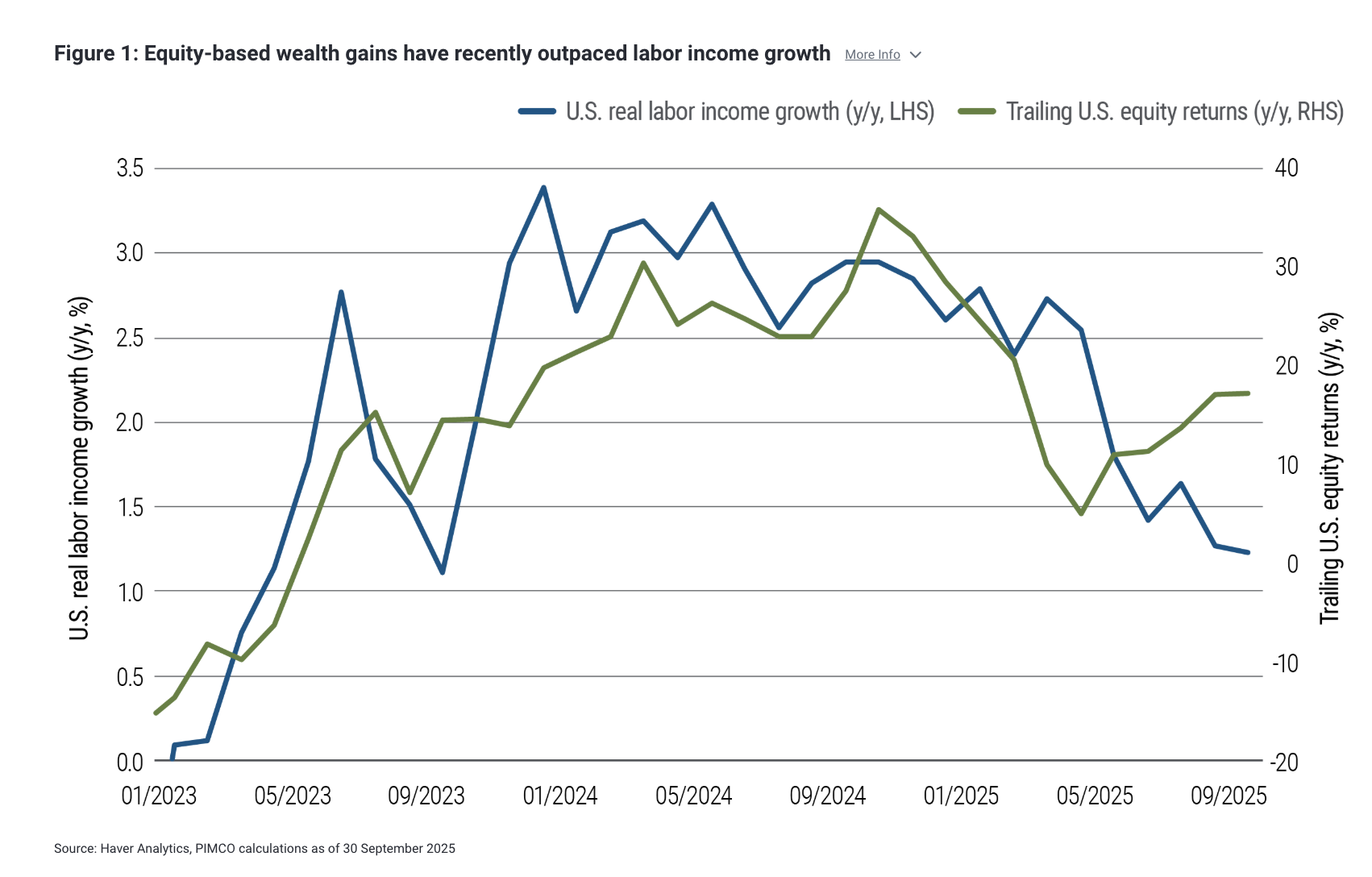

- Policy and technology changes also contributed to a U.S. household divide. The wealth effect of AI-led stock market gains has helped sustain consumption, but the benefits haven’t reached lower- and middle-income households (see Figure 1). As elevated uncertainty has stifled hiring and trade- and AI-exposed sectors shed jobs, real labor income growth has stalled. The AI related build-out also appears to be crowding out other investment, including residential housing, further reducing housing affordability.

- AI trends have supported global industrial output and trade despite tariff drags, although gains remain uneven. Growth is concentrated in computers and components tied to AI infrastructure. Asian economies, including Taiwan, Japan, South Korea, and China, have shared the U.S.’s resilience as they dominate production of chips, servers, and related hardware. Production elsewhere has slowed as earlier inventory stocking ahead of tariffs unwinds.

- China is being pushed to find other markets for its goods, while also accelerating its AI infrastructure build-out and further improving manufacturing productivity. U.S. tariffs have reduced trade between the two nations. Lower export prices have facilitated a smoother-than-expected trade rotation to EM. Still, sluggish consumption and falling investment have left China overly reliant on exports and inventory building to maintain growth.

Technology and fiscal policy bolster demand

We expect overall economic resilience to continue in 2026. There are also good reasons to expect some broadening in growth, but the trend toward winners and losers is likely to persist.

First, fiscal policy is set to diverge across countries. Fiscal policy easing in several regions should further offset trade drags. China, Japan, Germany, Canada, and the U.S. are all poised to loosen fiscal policy – China through central government support, and the U.S. via large, front-loaded business and household tax cuts. But many countries lack fiscal space, leaving policy tight in the U.K., France, and parts of EM.

Second, the AI investment cycle should keep supporting global growth as AI adoption spreads, but winners and losers will abound. In the U.S., broader corporate spending on AI implementation, software, and R&D could offset cooling data‑center capital spending from high 2025 levels. An additional tailwind could come from other countries stepping up infrastructure investment amid national security concerns. In the race for AI dominance, regional and industry laggards are at risk.

Third, trade uncertainty and tariff-related drags should also diminish in 2026, but not without further policy shifts as the legality of U.S. tariffs is tested. The U.S. Supreme Court could potentially strike down some or all tariffs implemented under the International Emergency Economic Powers Act. As the Trump administration shifts tariff policy to a more stable and legally secure framework, various regions and sectors will need to adjust, while reduced uncertainty reaccelerates investment and hiring, both in the U.S. and globally.

Monetary policy set to diverge

Most central banks embarked on rate-cutting cycles over the past few years, albeit at differing speeds based on inflation progress. With global inflation now broadly benign, we expect most central banks to reach neutral policy levels by the end of 2026. However, the outlook for additional cuts is now more nuanced.

Central banks with still-high real rates and tight fiscal policy are poised to cut more aggressively, particularly in countries more exposed to downside inflation risks from Chinese exports. This includes various EM central banks, as well as the Bank of England.

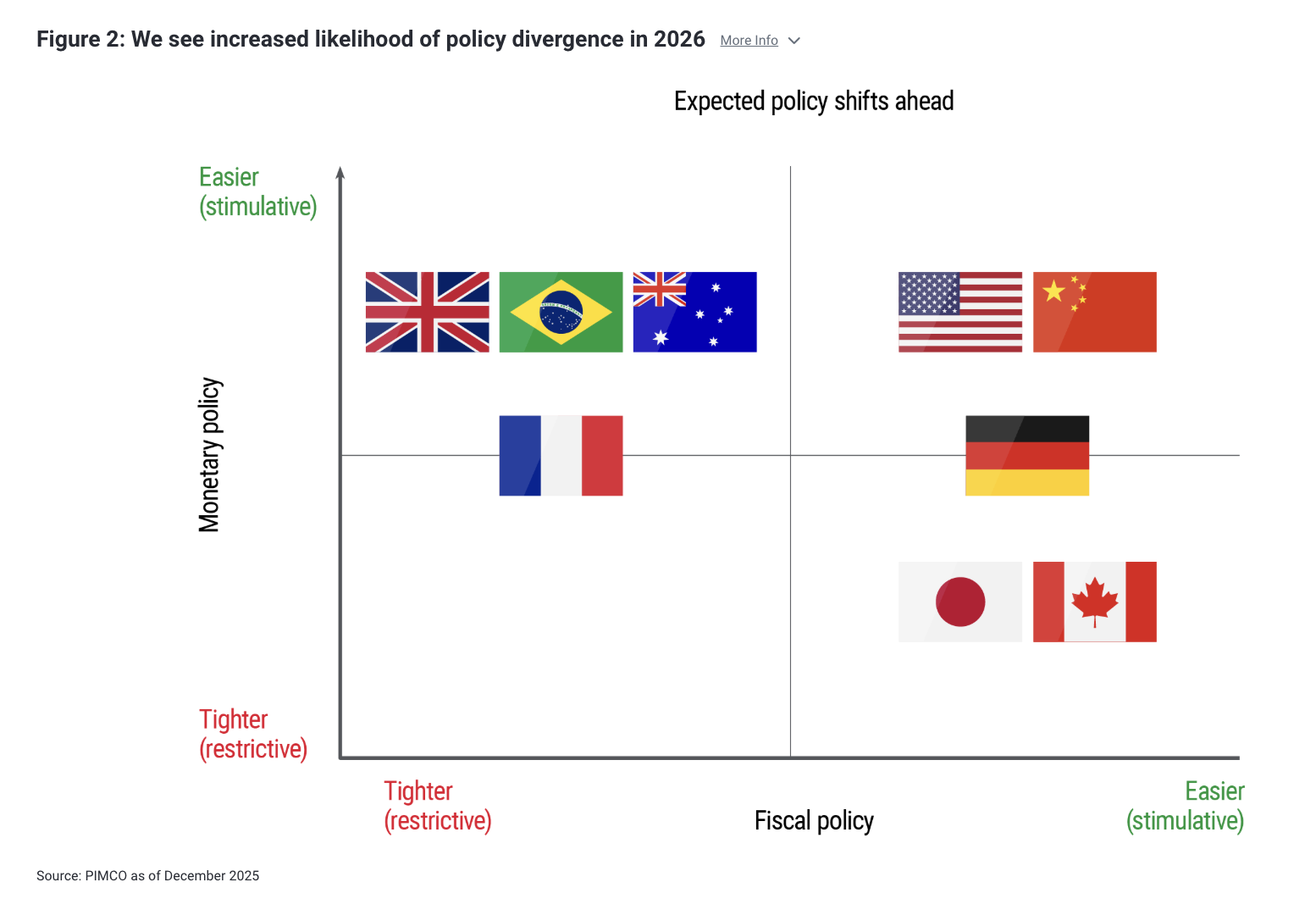

Elsewhere, where monetary policy is already near neutral and fiscal policy is poised to expand – notably Canada and, to a lesser extent, Europe – there is limited need for additional cuts. The Bank of Japan, meanwhile, with still-easy monetary policy and where fiscal policy is set to expand, is expected to hike rates further (see Figure 2), while in China both monetary and fiscal policy are expected to ease substantially, as policymakers manage debt deflation and overcapacity.

Finally, markets are pricing expectations for the U.S. Federal Reserve to lower its policy rate further, to 3%. We also expect Fed cuts in 2026, likely in the latter half of the year.

Uncertainty remains about the terminal rate amid a transition to a new Fed chair and as the White House pushes for lower rates. While there is a range of possible outcomes, the market has consistently priced a continuation with orthodoxy, reflecting the fairly conventional candidates and checks and balances inherent in the Fed policy-setting process.

The risks around U.S. inflation also look more two-sided. AI-fueled productivity and stagnant housing market trends could help keep overall prices in check. Tariffs, demand-augmenting fiscal policy, and technological infrastructure buildout could push prices higher.

Durability alongside vulnerability

While we expect economic resilience to continue, clashing forces and widespread haves-versus-have-nots dynamics create risks:

- U.S. risk-asset valuations: Traditional valuation metrics suggest U.S. stocks are expensive, both relative to history and to other markets. How much AI adoption accelerates and how much value can be created by AI (and when) – along with which companies will capture that value – remain key questions. Meanwhile, credit spreads continue to look tight.

- Sustainability of the K-shaped economy: Wealth-fueled consumption depends on additional equity and housing market appreciation, but high valuations and affordability pressures make this challenging. Areas of private credit look particularly vulnerable to policy- and AI-related transformations.

- Government deficit and debt dynamics: We haven’t changed our secular outlook for challenging debt and deficit dynamics across many DM economies, including the U.S., U.K., France, and Japan (for more, see our June 2025 Secular Outlook, “The Fragmentation Era”). While debt appears sustainable now – the average interest rate paid on government debt is still below trend growth levels – AI and trade policies could drive investment trends that prompt higher interest rates, adding pressure to sovereign debt.

- China challenges: A multiyear housing sector bust and already high global manufacturing share add to questions about how long China can sustain its production- and export-led growth model. Without materially more direct central government support for domestic demand, China will find it harder to reach growth targets, with disinflationary implications for the rest of the world.

Investment implications: Take advantage of the fixed income opportunity

After years of strong risk-asset returns, equity valuations remain elevated and credit spreads are tight. While our base case calls for growth to remain solid and potentially even reaccelerate in some regions, such optimism is already priced into most risk-asset markets. History suggests that these starting valuations will influence forward returns, which may be lower than investors have come to expect.

By contrast, bonds are cheap versus stocks at current valuations. After a sharp post-pandemic repricing, starting yields on high quality bonds remain attractive, highlighting the sustainable return potential in fixed income. Investors today have a rare opportunity to increase quality, liquidity, and portfolio diversification without giving up equity-like return potential.

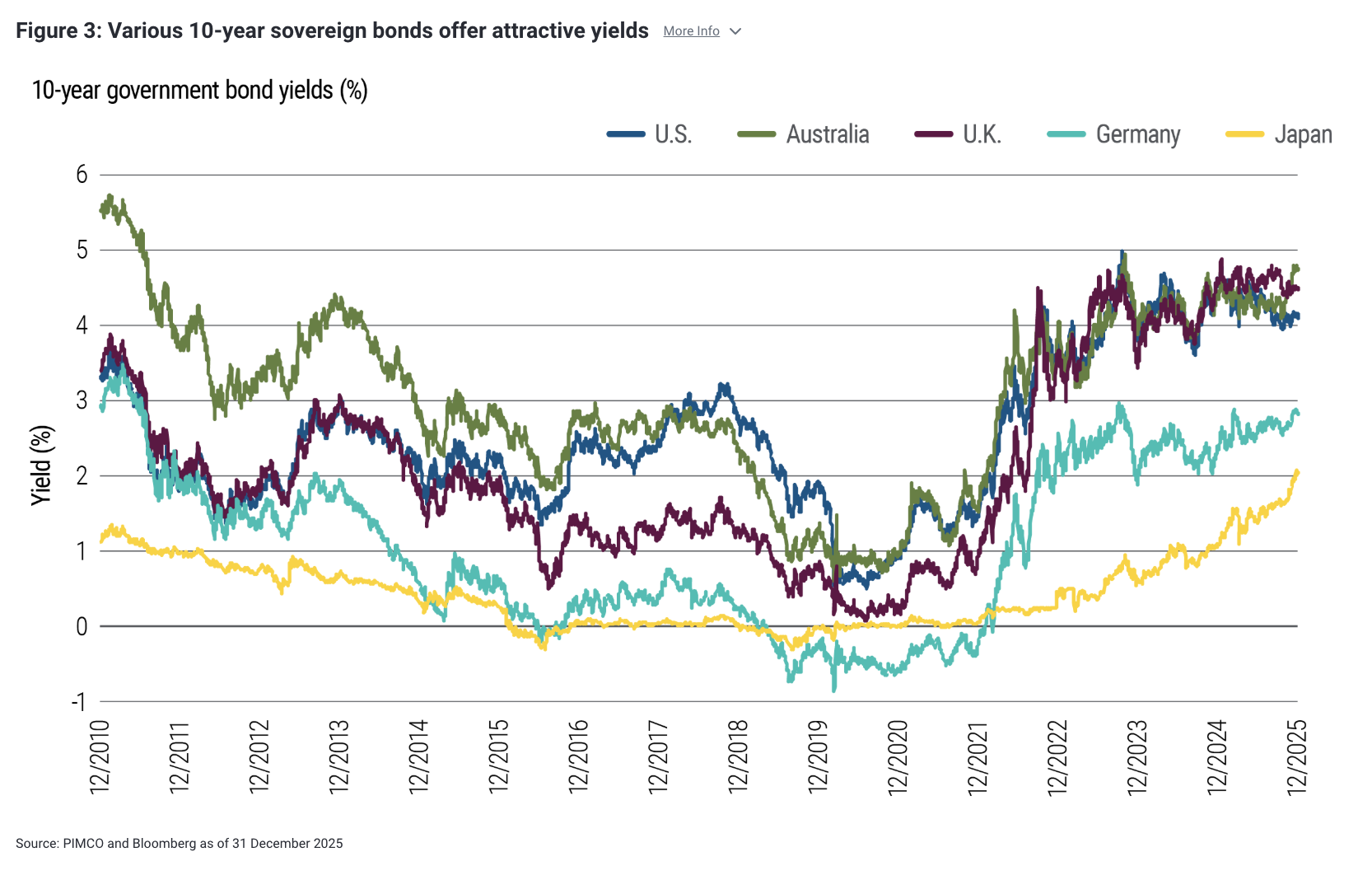

Even after broadly strong bond market returns in 2025, the yield on the benchmark 10-year U.S. Treasury note – about 4.19% as of 12 January 2026 – remains in the middle of the 3.5%–5% range that it has occupied for more than three years. Other DM sovereign 10-year yields tell a similar story (see Figure 3). This illustrates that robust bond returns don’t depend on a broad rally in rates.

Rather, attractive starting yields provide a baseline from which active managers can seek to construct portfolios potentially yielding about 5%–7% by capitalizing on alpha opportunities. (Learn more in our recent article, “Calculating the Active Advantage in Fixed Income.”) Active fixed income strategies delivered their best results in years in 2025 – and the outlook ahead is just as compelling amid one of the most exciting environments for alpha generation in recent memory.

Our 2026 playbook remains similar to 2025 in many respects. Amid a generally benign global growth outlook, and with attractive yields available in many countries, we favor a diversified portfolio of exposures across regions with different economic and policy paths, including DM and select EM local markets. Overall, our approach remains flexible. We expect to add and trim exposures based on valuations and market dislocations.

Rates, duration, and global opportunities

As yield curves have steepened, we believe investors who continue holding excess cash are missing a potential opportunity. By turning to fixed income, which has outperformed cash, investors can lock in more attractive yields over a longer period while also benefiting from potential price appreciation for a modest increase in risk.

We maintain a modest overweight to duration – a gauge of interest rate exposure – with a focus on global diversification. (Explore other opportunities to bolster portfolio diversification and resilience in our recent article, “Charting the Year Ahead: Investment Ideas for 2026.”) While we continue to favor 2- to 5-year bond maturities, our curve positioning has grown more balanced as longer-term yields have become more attractive.

U.S. duration still looks attractive and can help hedge portfolios against a potential slowdown in the U.S. labor market or AI-related equity volatility. European duration looks comparatively less attractive.

While Australian duration has underperformed, it remains a useful diversifier within a broader basket, especially now that markets are pricing in potential rate hikes in 2026 – a policy move we believe is unlikely.

Despite inflation above central bank targets and near-term risk of reacceleration, longer-term breakevens remain low. We continue to like Treasury Inflation-Protected Securities (TIPS), commodities, and real asset exposures.

We see select opportunities in countries with higher real policy rates, tighter fiscal settings, and more balanced inflation risks. This includes the U.K. and select EM countries.

Emerging markets: Asymmetric opportunities in a fragmented world

The EM investment landscape has structurally transformed, with lower aggregate government debt-to-GDP than DM, improved monetary policy frameworks and current accounts, and deepening local capital markets. In a twist, several advanced economies now exhibit fiscal dynamics once considered “EM-style risks.”

For active managers, dispersion creates opportunity. Unlike the 2010s when EM moved as a bloc, today’s environment rewards granular country selection across rates, currencies, and credit – generating alpha through structural analysis rather than beta timing. Across EM, we find attractive starting yields and a variety of idiosyncratic, diversifiable risks.

EM central banks are expected to continue to cut rates amid low inflation and resilient foreign exchange. We prefer duration overweights in South Africa and Peru, where yield curves are steeper than domestic fundamentals warrant, and Brazil, where we see room for a large and extended rate-cutting cycle.

We continue to see the potential for U.S. dollar weakness, reflecting the ongoing Fed easing cycle, secular fiscal concerns, and starting valuations that favor an overweight to EM currencies versus DM counterparts. EM currencies provide a liquid way to access the asset class outside of our dedicated EM strategies, and we can potentially generate attractive income with a carefully managed and well-diversified basket of EM country exposures.

Credit: Constructive but selective

Our stance toward credit remains constructive but has grown more selective. At PIMCO, we have witnessed many credit cycles across the five-plus decades since the firm’s founding. We are seeing signs of later-cycle behavior as strong recent returns have fueled complacency.

We expect continued deterioration in credit fundamentals, especially in floating-rate sectors of corporate markets, given weaker underwriting standards in recent years. Industry and single name exposure will matter, as we see fundamental pressure in areas such as healthcare, retail, and technology.

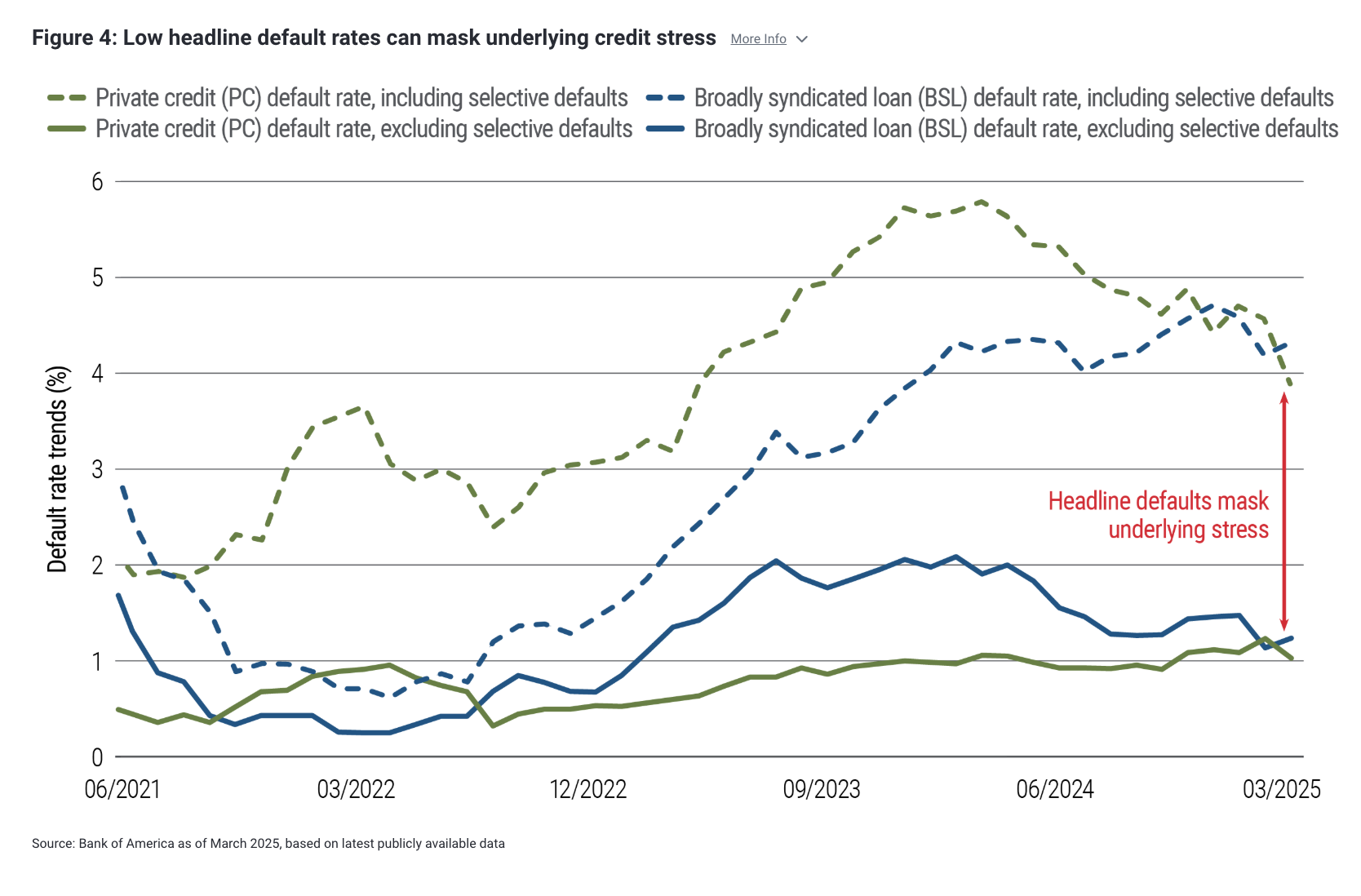

We have seen an increase in amendment activity, such as payment in kind (PIK) provisions that allow borrowers to repay debt with more debt. Such trends can mask underlying stress by keeping headline default rates low (see Figure 4).

We have also observed overreliance on rating agency ratings as a barometer for risk, and vehicles promising more liquidity than their underlying investment strategies may be able to deliver. These conditions are occurring in the wake of rapid growth in private credit markets in recent years.

During such periods, we look to reduce generic credit exposure – or beta – and focus on independent, bottom-up analysis and security selection.

We continue to favor U.S. agency mortgage-backed securities (MBS). Agencies remain a preferred partial substitute for corporate credit beta, supported by strong structural features, robust liquidity, and attractive spreads.

Rather than regarding credit markets as separate public and private segments, we continue to evaluate investments along continuums of economic sensitivity and liquidity risk, and we focus on ensuring adequate compensation for these risks. We consider the reasons companies turn to private versus public credit, such as greater flexibility or less restrictive regulation, and what that means for investors.

Investment grade issuers with stable cash flow and strong balance sheets remain the core of our credit positioning. We value the robust liquidity in public investment grade markets and believe investors should be selective when venturing into private investment grade, especially when incremental spread over more liquid opportunities is limited.

We continue to seek unique, well-structured credit opportunities that leverage PIMCO’s scale. We look to avoid lower-quality deals with less attractive spreads, weak collateral, and fewer lender protections. We expect secured lending in areas such as asset-based finance, real estate credit, and well-structured infrastructure debt to outperform. Lower-quality segments of corporate markets are more likely to disappoint given tight spreads, weak underwriting, and broader signs of overall complacency.

We continue to see value in areas offering robust collateral and clear structural protections. We see these opportunities in both liquid securitized markets and less liquid asset-based finance areas, especially those linked to higher-income consumers. Real estate debt, while out of favor, benefits from asset values that are well below peak levels.

Within high yield markets, we are cautious where covenant erosion or sponsor behavior creates greater downside risk. Direct lending, bank loans, and weaker high yield segments require particular caution, given questions about the quality of lender safeguards and potential liquidity challenges. Excess capital formation in these markets has resulted in programmatic lending activity that resembles more passive investment strategies.

Conclusion

In recent decades, abundant capital, low interest rates, and a stable global order reduced the need for diversification. In contrast, today’s environment is defined by dispersion, two-way risk, and economies across regions moving at different speeds. This creates a wide range of opportunities across global rates, EM, high quality credit, and securitized markets, reinforcing the value of an active approach.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. References to Agency and non-agency mortgage-backed securities refer to mortgages issued in the United States. Structured products such as Collateralized Debt Obligations (CDOs), Constant Proportion Portfolio Insurance (CPPI), and Constant Proportion Debt Obligations (CPDOs) are complex instruments, typically involving a high degree of risk and intended for qualified investors only. Use of these instruments may involve derivative instruments that could lose more than the principal amount invested. The market value may also be affected by changes in economic, financial, and political environment (including, but not limited to spot and forward interest and exchange rates), maturity, market, and the credit quality of any issuer. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. Diversification does not ensure against loss.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-1231-5092029

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Back to top

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All