Major tax legislation passed in 2025 represents the most sweeping changes to the tax code since the Tax Cuts and Jobs Act (TCJA) in 2017. In addition to extending current tax brackets and rates and introducing new tax deductions, the law creates new savings accounts for minors known as Trump Accounts. These accounts allow families to make after-tax contributions of up to $5,000 annually until the calendar year the child turns age 18. This is referred to as the growth period. Upon reaching the calendar year the minor turns 18, these accounts are treated as Traditional IRAs going forward. This is referred to as the post-growth period.

As part of a pilot program, the federal government will contribute $1,000 into these accounts for US citizens born in 2025 through the end of 2028.

A closer look at how Trump Accounts work

Contributions

Contributions may be made by the child, the child’s parents or other individuals (relatives, legal guardians, etc.), an employer, other organizations (nonprofit, governmental) or the federal government as part of the initial pilot program.

- Accounts are subject to an annual contribution limit of $5,000 and available to everyone regardless of household income. Contributions are indexed for inflation beginning in 2028.

- Contributions are allowed until the calendar year the minor reaches age 18 (i.e., once the growth period ends).

- An annual employer contribution is available of up to $2,500 per employee (not child); the employer contribution counts toward annual $5,000 contribution limit per child.

- Under a pilot program, the federal government will make a one-time $1,000 contribution to eligible children born in 2025 through the end of 2028. This contribution does not count toward the $5,000 annual contribution limit.

- State and local governments, tribal entities or nonprofit organizations can make additional contributions (known as General Funding Contributions) on behalf of a “qualified class” of beneficiaries, such as all children who reside in a certain geographic area or other factors; these contributions must be at least $25 per recipient and do not count toward the annual contribution limit of $5,000.

Tax treatment

- Family contributions are made with after-tax dollars and are considered basis (i.e., not taxed when withdrawn).

- Employer contributions are tax deductible to the employer and not considered taxable income to the employee (subject to taxation when withdrawn, however).

- Contributions by a governmental entity or other qualified organization are not considered taxable income to the minor child but would be subject to taxation when withdrawn.

- Account earnings are subject to taxation when distributed.

- Family contributions are subject to the annual gift tax limit.

Distributions

- During the growth period, no distributions are allowed except for rollovers to another Trump account, transfers to an ABLE account at age 17 or a distribution to correct an excess contribution.

- Once the calendar year the minor turns 18 is reached (the post-growth period), the account is treated as a Traditional IRA subject to those distribution rules (subject to a 10% early withdrawal penalty unless an exception applies, for example).

- For tax purposes, IRA distribution rules apply, which means a distribution consists of a pro-rata portion of basis (not taxed) and earnings plus any non-taxable contributions made into the account from an employer or other entity, which would be subject to taxation.

Investments

- Accounts are limited to a low-cost index fund that tracks returns of primarily US companies.

- The annual expense must not exceed 0.1% (10 basis points).

Sources: H.R.1 – 119th Congress (2025–2026): One Big Beautiful Bill Act. July 4, 2025. IRS Notice 2025-68. Interpretation of Trump Account provisions may be subject to change as the IRS issues additional guidance. ABLE accounts (Achieving a Better Life Experience) are accounts for individuals with disabilities established by the ABLE Act of 2014.

Other points on Trump accounts

- Once the growth period ends, a Trump Account could be converted to a Roth IRA or transferred to another Traditional IRA or employer retirement plan.

- Note that a conversion of a Trump Account to a Roth IRA may trigger the kiddie tax potentially resulting in taxable income for a parent.

- The kiddie tax applies to dependents as old as 23 years if they are full-time students receiving more than half of their support from parents (For more information on the kiddie tax see https://www.irs.gov/taxtopics/tc553).

- Trump Account contributions do not impact or count toward the IRA contribution limit, meaning if a minor has earned income from employment, a contribution into an IRA can be made in addition to a Trump Account contribution.

- There can only be one Trump Account for an individual at any time.

- Unlike IRAs, there is no ability to make a prior-year contribution into a Trump account.

- The $1,000 pilot program contribution for newborns is not automatic, meaning that families need to establish a Trump account to receive the contribution.

- It’s unclear on how funds within a Trump account would be treated for federal financial aid purposes.

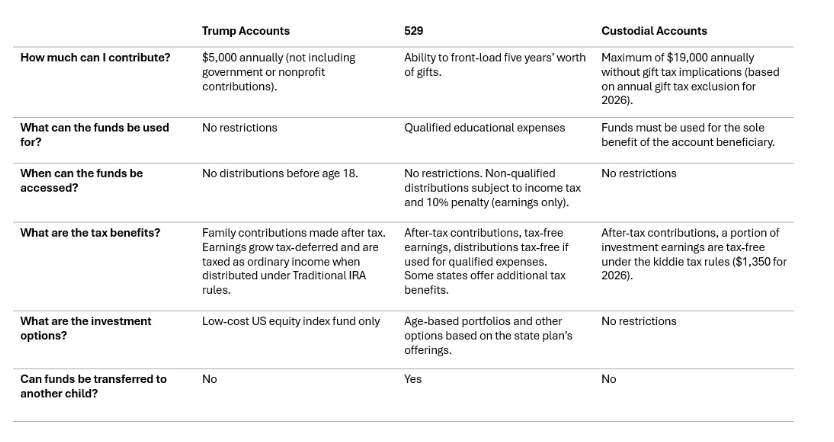

How do Trump Accounts compare with other savings options?

While Trump Accounts offer flexibility for families to help children jumpstart their savings, there may be better options for families depending on specific needs or circumstances. For example, if the funds are likely earmarked for higher education needs, a 529 account may be a better alternative. If used for qualified expenses, distributions from a 529 account are free from taxes. A 529 account allows for significant contributions as well, with the option to front-load five years’ worth of annual gifts ($19,000 for 2026 for a total of $95,000).1

Additionally, a recent tax law change allows up to $35,000 (lifetime) to be transferred tax free from a 529 plan to a Roth IRA in the name of the beneficiary if certain requirements are met. Since Trump Accounts are treated as IRAs once the child reaches age 18, a portion of a distribution (earnings, any non-taxable contributions) will be subject to taxes when withdrawn.

Saving for minors with a custodial account has historically been a viable option to build long-term savings and may be a better alternative for some than a Trump Account. For example, funds held within a Trump Account cannot be withdrawn before the calendar year the child turns 18. A custodial minor account (UTMA, UGMA) may provide more flexibility to access funds to address the financial needs of the minor since there are no restrictions on when funds can be withdrawn. Also, there is the added potential for higher annual contributions (vs. the $5,000 Trump account annual limit), more investment choice and preferential tax treatment since investment earnings may be tax free (up to $1,350 in 2026 under the kiddie tax rules) or taxed at the child’s lower tax rate. Custodial minor accounts may benefit from lower qualified dividend or long-term capital gains tax rates, while the taxable portion of a Trump distribution is considered ordinary income subject to higher tax rates.

Quick Comparison of Savings Accounts for Minors

Next steps: How to establish a Trump account

Per the legislation, contributions into Trump accounts are not available until after July 4, 2026. Those wishing to establish an account, either to make direct contributions, receive the federal government pilot program “seed” contribution for eligible newborns, or both, can file IRS Form 4547 or access the program online at trumpaccounts.gov.

If funded regularly, Trump accounts provide an opportunity to create significant savings over many years. At the very least, families of eligible newborns should establish an account to receive the seed funding contribution from the federal government. Additionally, there may be opportunities for certain organizations, such as non-profits, to make an impact by funding Trump accounts for certain groups of beneficiaries. For example, those living in lower-income areas. Since the individual decision on whether to fund a Trump account is based on individual circumstances and needs, it may be prudent to seek professional advice.

Register Here for the upcoming Financial Professional Webinar on February 3: The tax-aware advisor's 2026 playbook

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnotes

1A special federal tax election allows a taxpayer to contribute five years of annual gifts ($19,000 per person in 2026) into a 529 savings account. The taxpayer must file IRS Form 709 to make this election and cannot make any more gifts to that recipient for the five-year period.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton

Read more commentaries by Franklin Templeton