Is Greenland Really Worth the Gamble?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSeven hundred billion dollars. That’s the figure being floated as the potential price tag for acquiring Greenland, according to recent reporting.

Call me skeptical, but I don’t think anyone’s cutting a $700 billion check anytime soon. For comparison’s sake, that’s more than half of the Defense Department’s entire 2024 budget.

Public opinion isn’t exactly lining up behind the idea, either, despite President Donald Trump’s insistence that “anything less than [the complete U.S. control of Greenland] is unacceptable.”

Americans are telling pollsters they don’t support the idea, whether peacefully or otherwise. A recent YouGov survey showed that only 13% of Americans are in favor of paying Greenland’s residents to join the U.S., while an even smaller share—just 8%—support taking the island by force.

Greenlanders are likewise not warm to the idea, as the overwhelming majority don’t want to leave the Danish realm. Europe, especially Denmark, is firmly opposed.

But dismissing Greenland entirely would, I think, be a mistake.

Why Greenland Matters, Even If No One Buys It

Sitting between North America, Europe and Russia, Greenland is home to the Pituffik Space Base, where the U.S. Space Force tracks anything that might come flying over the North Pole.

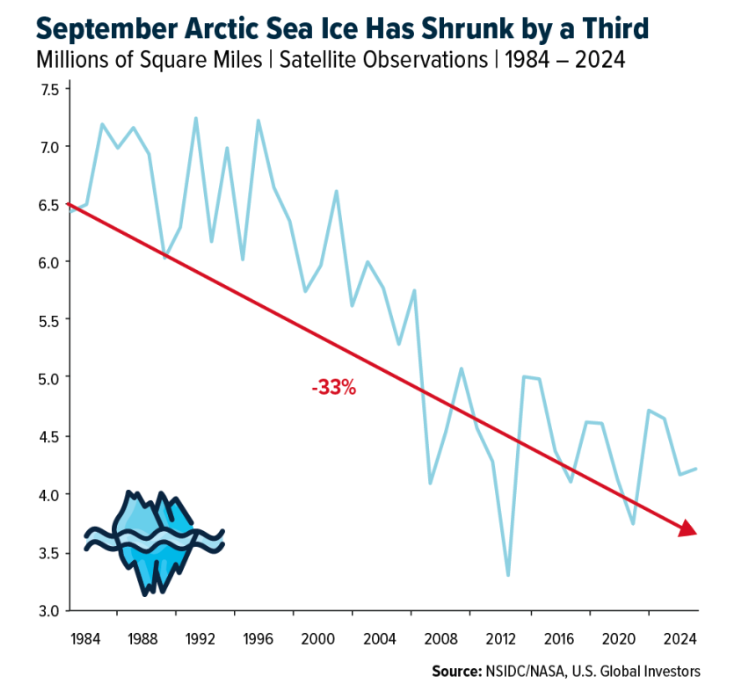

That role has become more important as Arctic ice continues to retreat. Satellite imagery shows summer Arctic sea ice shrinking over 12% per decade, or 33% since 1984, opening new shipping lanes and creating new military and commercial realities.

As I shared with you last year, the Arctic is becoming more navigable and investable.

Denmark understands this. The Kingdom just committed more than $4 billion to Arctic and North Atlantic defense through 2033, in coordination with fellow NATO members. Danish and allied aircraft, naval vessels and ground units are expanding their presence on and around the island. Exercises include guarding critical infrastructure and operating fighter aircraft in Arctic conditions. Meanwhile, Denmark’s Chief of the Army Command, Peter Boysen, is talking about boots on the ground.

The Harsh Realties of Developing Greenland

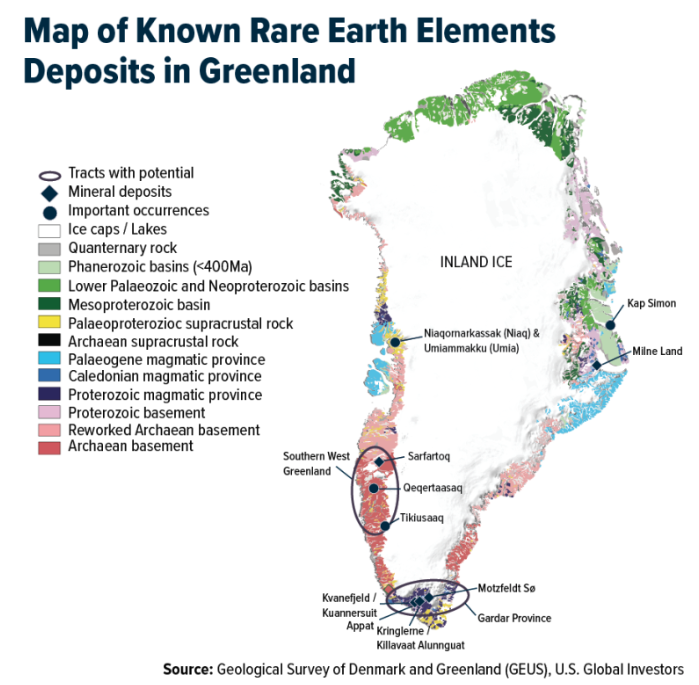

And then there’s the minerals. Greenland is rich in iron ore, copper, zinc, graphite, tungsten and more.

But what really captures headlines are rare earth elements (REEs), the materials that power everything from fighter jets to smartphones to missile guidance systems. According to the Center for Strategic and International Studies (CSIS), Greenland ranks eighth globally in proven rare earths, with the potential to move even higher as exploration advances.

That looks incredibly attractive from a mining company’s point of view. But in practice, development would be slow and capital-intensive.

Greenland is three times the size of Texas and yet, unbelievably, has fewer than 100 miles of road, none of which connects two towns together. Energy infrastructure is limited. Transport costs are high. Many deposits are co-located with uranium, which Greenland banned from mining in 2021 after local opposition.

In this respect, it’s helpful to compare Greenland to Venezuela. Both are being treated as instant windfalls waiting to be unlocked—rare earths in the former and oil in the latter—but the truth is that they’ll require billions in capital and long timelines to develop. According to Wood Mackenzie, just 25 hydrocarbon exploration wells have even been drilled in Greenland—all of them unsuccessful.

Neither region, then, should be seen as a get-rich-quick story.

China Has Tried to Operate in Greenland… but Failed

China understand Greenland’s strategic and resource value as well as anyone. Over the past decade, Beijing has tried to gain a foothold through airport construction, infrastructure projects, scientific research and other means.

Nearly all of these efforts have been blocked—either by Denmark or the U.S.—on national security grounds.

In 2016, for instance, a Chinese mining company’s attempt to buy an abandoned, U.S. naval base in Greenland was thwarted. Two years later, the state-run Chinese Communication Construction Company (CCCC) sought to be awarded the bid to expand a set of airports, a job that would cost $550 million, but the then-Secretary of Defense James Mattis managed to convince Denmark to pull the contract.

So Why Does Trump Want It?

Having said all that, why does President Trump want Greenland so badly?

He insists it’s for national security, but, as I mentioned earlier, the U.S. military already has broad access to the island, as spelled out in the 1951 agreement signed by the U.S. and Denmark.

Further, Greenland is under the protection of NATO, of which the U.S. is a member. If Russia or China tried to attack it, Article 5 of the treaty would be triggered, activating NATO forces.

Recent reporting suggests that some of Trump’s wealthiest backers see Greenland not as a military outpost or mining play, but as a blank slate. According to Reuters, influential tech investors—including Peter Thiel and Marc Andreessen—have pitched the idea of turning parts of Greenland into a so-called “freedom city,” offering a low-regulation, quasi-autonomous hub for next-gen technologies.

Another explanation? Trump’s reaffirmation of the Monroe Doctrine, which the White House has dubbed the “Trump Corollary” or “Donroe” Doctrine. As stated in the president’s December 2 proclamation, the “American people—not foreign nations nor globalist institutions—will always control their own destiny” in the Western Hemisphere.

Denmark, notably, sits in the Eastern Hemisphere.

Japan’s Gold Reserves at a New Record

On a final note, central banks across the globe continue to stack gold to support their currency and diversify away from the U.S. dollar.

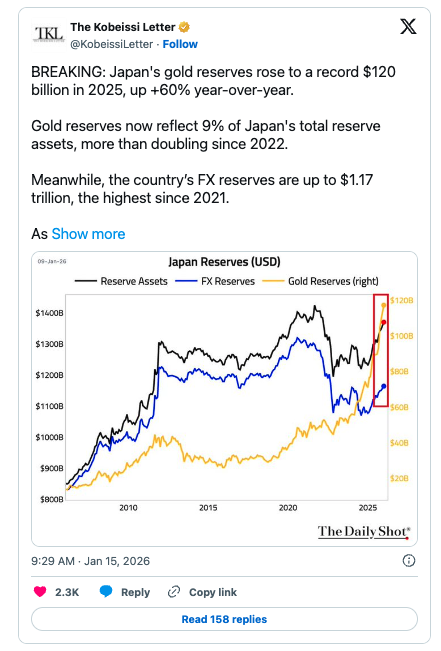

Emerging markets have led purchases over the past decade, but some high-income countries have also participated. The Kobeissi Letter reports that Japan’s gold reserves rose to a new all-time high in 2025. Reserves stood at $120 billion, an impressive 60% increase from a year earlier.

Japan currently has the world’s ninth-largest gold reserves, excluding the International Monetary Fund (IMF), according to World Gold Council (WGC) data.

As I’ve pointed out before, these massive institutions clearly understand the importance of having exposure to hard assets such as gold. That’s why I still recommend a 10% weighting in gold, split equally between physical bullion and high-quality gold mining names. Don’t forget to rebalance on an annual basis.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Sun Country, up 12.3%. The Nikkei Shimbun reported that Japan Airlines (JAL) has embarked on a reorganization of its domestic routes and plans to restore its operating margin to the 10% level in Q3 2029 by dropping some routes and using smaller aircraft on others.

- According to Morgan Stanley, shippers’ economic outlook improved modestly, marking the strongest sequential gain since late 2024 despite remaining below the long-term average. Inventory trends continue to move in a positive direction, with destocking easing and conditions approaching restocking territory for the first time since 2024.

- Alaska Air (ALK)’s customer satisfaction scores were the highest in UBS’s coverage universe, with an overall rating of 1.90, followed closely by Southwest (LUV) at 1.87 and Delta (DAL) at 1.86. United (UAL) scored 1.72. Alaska Air stands out, ranking first in categories that include cleanliness, legroom, and value for money.

Weaknesses

- The worst-performing airline stock for the week was Trip.com, down 18.4%. According to UBS, Spring Air estimated that the Japan-related capacity readjustment could reduce its full-year 2026 profit by Rmb50–60 million, though the impact is expected to be manageable and fade over time. That said, for its Japan-related routes alone, there may be no meaningful improvement in 2026.

- COSCO Shipping Management noted that there is no clear timetable for a full return of Red Sea routes, which could take 3–5 months to progress from a reopening attempt to full reopening. Multiple conditions need to be met for a Red Sea reopening, including approval from industry associations after evaluation, reduced insurance premiums on related routes, client agreement that the routes are safe, and consensus among shipping alliances, according to UBS.

- The number of return trips by Canadian residents from the U.S. declined by 18.7% year-over-year (YoY) to 470.7K in December, a slight improvement from the 19.3% year-over-year (YoY) decline seen in November, indicating that demand is stabilizing, according to RBC. This aligns with broader expectations and commentary regarding gradual stabilization.

Opportunities

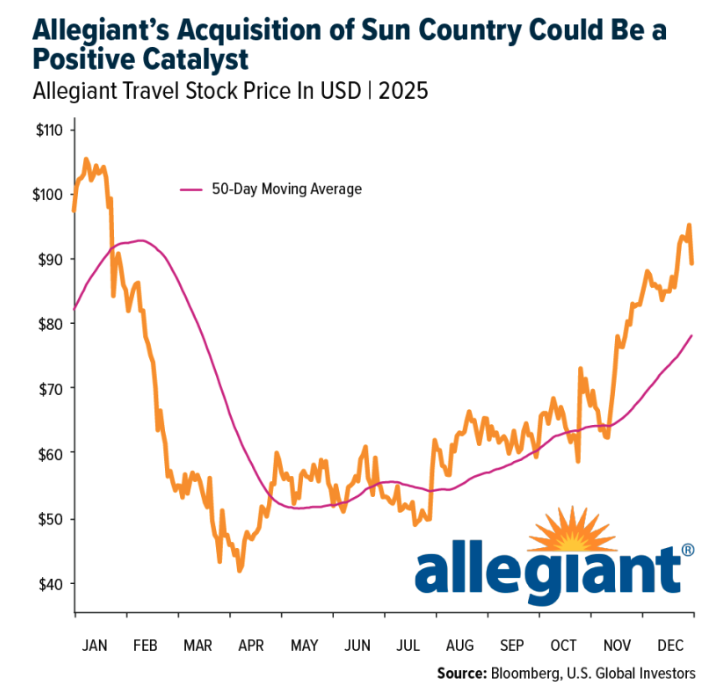

- Allegiant will acquire Sun Country for $1.5 billion, including $0.4 billion of debt. Sun Country shareholders will receive $18.89 per share, including 0.1557 Allegiant shares and $4.10 in cash. Management expects $140 million in synergies within three years, and the deal is projected to be earnings accretive one year after closing, with Net Debt/EBITDAR below 3.0x. Allegiant and Sun Country shareholders will own 67% and 33% of the combined company, with Gregory C. Anderson as CEO and Robert Neal as President and CFO.

- SITC management highlighted a significant arbitrage: current chartered vessels cost $20–30K per day, whereas newly owned vessels operate at less than $10K per day. With two new vessels delivering in 2026, seven in 2027, and more than ten in 2028, management expects to maintain the current unit cost of $430 per TEU, providing a buffer against industry-wide cost inflation (compared with peers’ $550–600 per TEU in 2025, according to UBS).

- Embraer and Adani signed a manufacturing agreement to produce commercial jets in India. While details of the partnership remain limited, Embraer Senior VP Raul Villaron for Asia noted that India could demand 500 regional aircraft over the next 20 years, representing a potential market of $21 billion based on $42 million per aircraft, according to JP Morgan.

Threats

- Azul approved a R$7.4 billion equity offering, issuing over 1.4 trillion new common and preferred shares to convert debt into equity as part of its judicial recovery plan, according to JP Morgan.

- Shippers’ economic outlook remained below the long-term average. Inventory trends continue to improve, with destocking easing and conditions approaching restocking territory for the first time since 2024, according to Morgan Stanley.

- Trip.com fell 17% following news that China has opened a formal anti-monopoly case. This coincides with Alibaba’s recent release of Qwen, raising AI competition concerns for online travel agencies.

Luxury Goods and International Markets

Strengths

- Brunello Cucinelli reported solid revenue growth last quarter, supported by broad demand across regions. The company also reaffirmed its outlook for roughly 10% revenue growth in 2026, signaling continued confidence in its brand and order pipeline.

- Industrial production in the European Union showed improvement both month-over-month and year-over-year, signaling that manufacturing activity and broader industrial momentum are stabilizing after a weaker 2025. This uptick supports expectations for a firmer economic backdrop heading into 2026. At the same time, China reported an increase in money supply, which typically reflects stronger credit conditions and potential support for consumption and investment.

- Shiseido Corporation is a major Japanese beauty and cosmetics company specializing in skincare, makeup, fragrance, and premium personal care brands. Investors reacted positively to improving China beauty demand in the stock, signaling expectations for margin recovery.

Weaknesses

- Donald Trump has proposed capping credit card interest rates, posing a potential threat to banks and payment companies that rely on high interest income. Lower credit card yields could pressure margins, weaken rewards economics, and reduce earnings from credit card portfolios. This could also affect wealth management businesses tied to premium card clients and slow customer acquisition. Financial stocks declined this week on concerns about reduced sector profitability.

- Cruise lines were among the weakest performers this week, with shares of Royal Caribbean, Carnival, Norwegian Cruise Line, and Viking all trading lower. Royal Caribbean declined the most. Citi raised its price target and maintained a Buy rating but issued a “downside 30-day short-term view,” expecting a more conservative outlook from cruise operators during the fourth-quarter earnings season. Royal Caribbean will be the first to report later this month.

- Rivian Automotive, a U.S. electric vehicle manufacturer focused on premium electric pickup trucks, SUVs, and commercial delivery vans, faced increased investor caution over cash burn and production outlook.

Opportunities

- As the fourth-quarter 2025 reporting season begins, the luxury sector presents an opportunity for investors, with companies expected to show modest growth supported by resilient high-income consumers and a strong holiday quarter. With sequentially improving spending trends and several brands already signaling stronger sales momentum, earnings results could highlight continued strength in key luxury categories.

- Recent Bloomberg coverage of luxury brands highlights that 2026 could be one of the biggest years ever for Tesla shares, as the company advances physical artificial intelligence initiatives such as robotaxis, humanoid robots, and broader AI integration. These developments could serve as a catalyst for Tesla’s stock if investors begin pricing in growth from these next-generation opportunities beyond traditional EV sales.

- Morgan Stanley names Kering as a top pick in the personal luxury space, assigning it an Overweight rating. The broker expects sequential improvements in the last three months of the year compared with the previous quarter. Morgan Stanley also notes that Kering operates in a structurally attractive industry, owns strong brands, and anticipates that newly appointed CEO Luca de Meo will unlock significant value in the coming years.

Threats

- Chinese tourists are traveling more across Asia after the pandemic thanks to expanded visa-free policies and a stronger yuan, but they are spending less. Bloomberg reports that in South Korea, which relied on Chinese travelers for roughly 70% of its duty-free sales before COVID-19, duty-free sales have fallen to levels last seen in 2015. Other Asian destinations, including Thailand and Singapore, are seeing similarly weak retail performance despite a rebound in Chinese tourist arrivals.

- Saks Global, the parent company of Saks Fifth Avenue, Neiman Marcus, and Bergdorf Goodman, has filed for Chapter 11 bankruptcy in the U.S. Bankruptcy Court for the Southern District of Texas after struggling with heavy debt and declining sales. The filing follows a costly $2.7 billion acquisition of Neiman Marcus in 2024. Saks has secured approximately $1.75 billion in financing to support operations during restructuring and plans to keep stores open while negotiating with creditors and strengthening its business.

- Local fashion and jewelry brands are gaining market share in China and the U.S., putting pressure on European luxury houses. According to the Financial Times, analysts note that younger consumers are shifting toward culturally relevant, domestically produced brands, which are outperforming traditional luxury labels in key categories. In China, for example, Laopu Gold continues to grow in popularity with younger shoppers, reflecting a trend toward domestic jewelry brands.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was lithium carbonate, which rose 17.48%. Chinese lithium carbonate futures jumped over 20% in early 2026 to a more than two-year high as battery makers rushed to export ahead of Beijing’s phased cuts to export tax rebates, compounded by temporary supply tightness from refinery maintenance. While policy-driven demand has fueled short-term volatility, analysts expect supply and demand to broadly balance later in 2026, limiting sustained price gains amid risks of new production and alternative battery technologies.

- Talen Energy Corp. has agreed to acquire three natural gas power plants—Waterford Energy Center and Darby Generating Station in Ohio, and Lawrenceburg Power Plant in Indiana—from Energy Capital Partners for $3.5 billion ($2.6 billion cash plus $900 million in Talen stock), adding 2.6 GW of capacity to meet surging U.S. electricity demand from data centers. The transaction, expected to close in the early second half of 2026 pending regulatory approvals, expands Talen’s presence in the western PJM market and drove its shares up as much as 13% in premarket trading.

- Amazon is set to buy America’s first new copper output in more than a decade, securing supply from a Rio Tinto operation in Arizona that uses bacteria and acid to extract the metal. The copper will be directed toward data-center construction, underscoring how AI-driven power and infrastructure buildouts are increasingly shaping strategic demand for critical industrial metals.

Weaknesses

- Iron ore was the weakest performing commodity of the week, declining approximately 5.56%. The metal has stayed stubbornly within the $100–$110 a ton range, but growing signs of loosening market conditions are raising the risk of a downside break. Record Australian shipments, swelling Chinese port stockpiles, and expectations of weaker Chinese steel output and robust miner supply all point to mounting pressure on prices.

- A growing share of the “dark fleet” shipping sanctioned oil is reflagging to Russia after the U.S. began seizing tankers tied to Venezuelan crude, betting Moscow will provide political cover as enforcement intensifies. The shift raises geopolitical stakes by turning sanctions evasion from a compliance issue into a state-backed risk, increasing the odds of direct confrontation as Washington expands interdictions, Reuters reports.

- BHP Group finds itself on the sidelines of a copper-driven M&A wave it helped ignite, as rival tie-ups like a potential Rio Tinto–Glencore deal threatens to erode its relative scale. With its prior Anglo bid abandoned and leadership transition approaching, BHP is monitoring developments but faces growing investor pressure to respond as copper consolidation reshapes the industry.

Opportunities

- LibertyStream Infrastructure Partners Inc. has called a March 31, 2026, special meeting to seek shareholder approval to re-domicile to Texas and establish its head office in Dallas, aligning its corporate base with its Permian Basin operations and advancing plans for a future U.S. exchange listing. The move positions the company closer to customers and U.S. policymakers, improving access to deep U.S. capital markets and eligibility for Department of Energy and Department of Defense funding as it targets commercial lithium production in late 2026.

- U.S. lawmakers introduced bipartisan legislation to establish a $2.5B Strategic Resilience Reserve aimed at countering China’s dominance in critical minerals like lithium, rare earths, graphite and cobalt, stabilizing prices and insulating supply chains vital to EVs, defense and high-tech manufacturing. If passed and signed by Donald Trump, the reserve would allow the United States to stockpile, recycle and deploy minerals strategically—reducing vulnerability to Chinese export controls while helping establish Western price benchmarks.

- Surging electricity demand in India, where coal still supplies ~75% of generation, underscores coal’s critical role as the marginal fuel during demand shocks as electrification and appliance penetration rise. In parallel, the United States is moving to keep its existing coal fleet running to support data centers and industrial growth, reinforcing coal’s value as a near-term reliability backstop. Together, these dynamics create a multi-year window of support for coal demand and pricing, even as longer-term capacity additions tilt toward gas, nuclear and renewables Bloomberg writes.

Threats

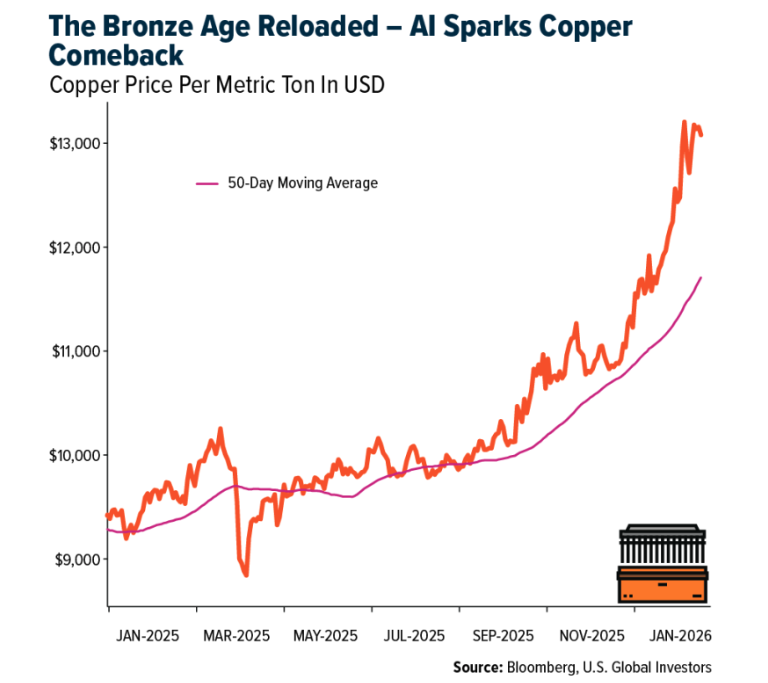

- Copper demand growth could slow in 2026 as record prices near $13,000/ton drive substitution—particularly toward aluminum—while fading Chinese stimulus and softer U.S. manufacturing capex normalize growth toward ~1.5–2.5% from 2025’s elevated levels. Bloomberg Intelligence notes that the widening copper–aluminum price gap raises longer-term substitution risk, especially in EVs, even as electrification and India continue to provide underlying support.

- Japan’s heavy reliance on China for rare earths leaves its manufacturers exposed to geopolitical escalation, as Beijing’s tightening export controls could disrupt supply chains with effects likely emerging next month as license reviews slow. Even if civilian trade is officially exempt, the episode underscores China’s leverage over critical minerals—raising risks for Japan’s EV, electronics and defense-linked industries amid worsening bilateral tensions, Bloomberg writes.

- Metals sold off after Chinese regulators ordered exchanges including the Shanghai Futures Exchange to remove high-frequency trading servers, cooling speculative momentum that had driven copper and tin to records. While the move may dampen liquidity and near-term prices across venues like the London Metal Exchange, it’s unlikely to alter longer-term fundamentals, reinforcing the risk of sharper pullbacks amid already elevated valuations.

Bitcoin and Digital Assets

Strengths

- Stablecoins are increasingly integrated into traditional payment systems. Visa reported $4.5 billion in annualized stablecoin settlement volume, growing month over month, and launched USDC-based settlement pilots with U.S. banks, signaling early institutional adoption. With over $270 billion in stablecoins outstanding, companies like Visa are positioning themselves as key bridges between on-chain funds and global merchant networks.

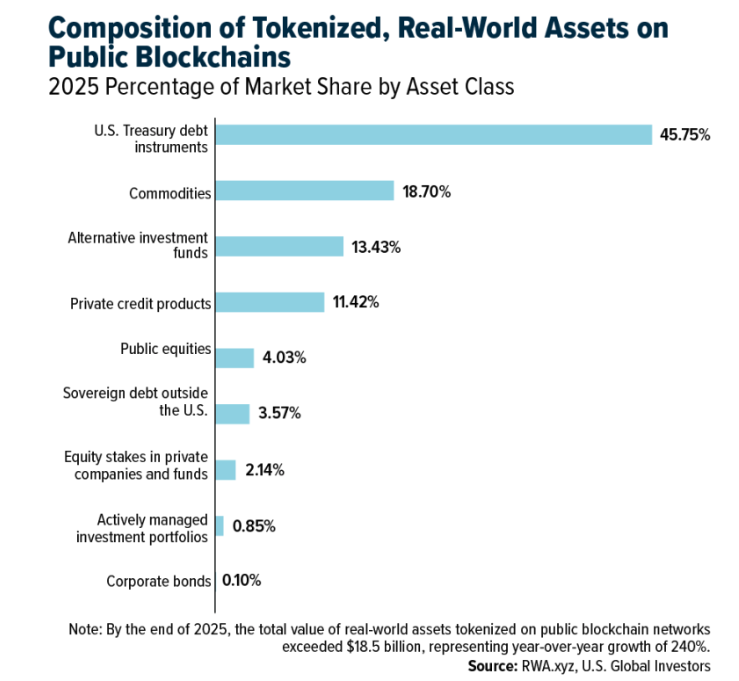

- U.S. lawmakers advanced the Digital Asset Market Clarity (CLARITY) Act, which aims to define SEC vs. CFTC oversight and create legal pathways for tokenized assets. While still debated, the framework reflects growing acceptance of blockchain-based capital markets and could accelerate tokenization of equities, funds, and real-world assets under U.S. regulation—an important step for institutional adoption.

- Stablecoins are becoming integrated into core institutional market infrastructure. Interactive Brokers now allows 24/7 account funding via USDC, enabling near-instant trading outside banking hours, something traditional wire transfers cannot offer. The integration, powered by Zerohash, supports Ethereum, Solana and Base, and reflects growing institutional demand for faster, lower-cost funding rails within regulated brokerage platforms

Weaknesses

- As reported by CoinDesk and CoinTelegraph, Bitcoin has repeatedly tested the $95,000–$97,000 range this week without a successful breakout, revealing weakness in “organic” buying power. After a massive rally to start the year, the market shows signs of exhaustion, indicating that without a significant new wave of capital, Bitcoin may struggle to reach $100,000.

- Bitcoin’s market is over-extended, with Open Interest near a three-week high (~700,000 BTC) and persistently positive funding rates (+0.09%). Traders are now trapped in expensive long positions, creating a high risk of liquidations if the price drops to $89,200, which could trigger a domino effect regardless of positive news.

- The KAITO selloff highlights the fragility of crypto projects tied to centralized platforms. After X revised its API policies banning paid engagement apps, KAITO’s token fell over 14% in a single day, cutting its market cap to roughly $140 million from a ~$2 billion fully diluted valuation peak, showing how sudden platform changes can disrupt token utility and investor confidence.

Opportunities

- Regulated, U.S. Treasury–backed stablecoins are expanding into Bitcoin-native ecosystems, unlocking institutional-grade on-chain liquidity. Citrea’s launch of ctUSD, backed 1:1 by cash and short-term U.S. Treasurys and available in 49 U.S. states and 160+ countries, addresses stablecoin fragmentation by issuing natively rather than via bridges, positioning Bitcoin as a scalable and compliant settlement layer for tokenized finance.

- AI-driven power demand is transforming crypto infrastructure into a strategic asset class. Galaxy Digital’s approval to expand its Texas data center by +830 MW and HIVE Digital Technologies’ expansion of Tier III data centers in Paraguay, powered by low-cost renewable energy, illustrate how former crypto miners are becoming critical providers of AI and high-performance computing infrastructure.

- The creator economy is emerging as a powerful new distribution channel for crypto and DeFi adoption. BitMine’s $200M equity investment into MrBeast’s Beast Industries, a platform reaching 450M+ subscribers and generating $400M in annual revenue, positions crypto capital at the intersection of media, Gen-Z finance, and future fintech platforms. Planned exploration of DeFi within Beast’s upcoming financial services could accelerate mainstream adoption at unprecedented scale.

Threats

- Stablecoins threaten bank funding and credit transmission. Large banks warn that up to $6 trillion in deposits could migrate into stablecoins offering yield-like incentives, reducing banks’ deposit bases that fund loans. A sustained shift would force banks to rely on more expensive wholesale funding, tightening credit and raising borrowing costs, especially for small and mid-sized businesses, while regulatory gaps around stablecoin rewards remain unresolved.

- The expansion of mandatory digital ID and age-verification regimes signals a structural shift toward tighter state control over online access. As governments in the UK, Australia, and the EU push ID-verified platforms, compliance burdens could rise across fintech and crypto, limiting user anonymity, increasing onboarding friction, and setting precedents that may extend to wallets, DeFi interfaces, and other on-chain services.

- India’s crypto market faces pressure from a punitive tax regime: a 30% flat tax on gains, 1% transaction-level TDS, and a ban on loss offsetting. Compliance requirements, including KYC, geolocation, and transaction monitoring, are pushing liquidity offshore and limiting domestic innovation, risking India’s position in the global crypto ecosystem unless policies are recalibrated in the February 2026 Union Budget.

Defense and Cybersecurity

Strengths

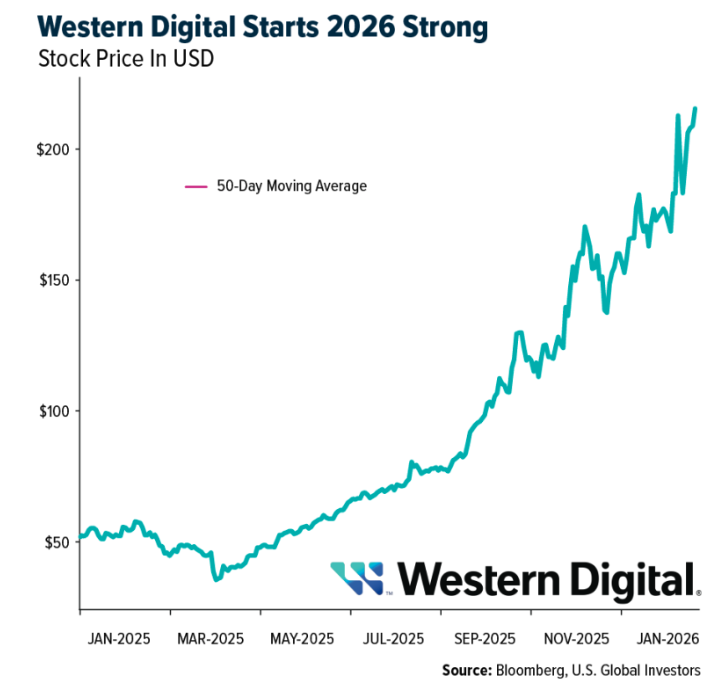

- Western Digital headed into fiscal 2Q riding a powerful wave of AI‑driven storage demand, its higher‑capacity 28–36TB drives pushing sales, margins, and confidence sharply higher. Capacity constraints through 2026–2027 and the shift toward 11‑platter platforms set the stage for continued double‑digit growth and stronger earnings ahead.

- Global semiconductor revenue reached $793 billion in 2025, with Nvidia accounting for over 35% of industry growth and surpassing $100B in annual sales. Moody’s projection of $3T in global data-center investment over the next five years confirms sustained demand for compute, memory, power, and cooling infrastructure.

- The best-performing stock this week in the XAR ETF was RED CAT Holdings, which rose 16.84% after reporting preliminary Q4 2025 revenue of $24–26.5 million, up approximately 1,842% year over year, and full-year revenue growth of roughly 153%, driven by surging defense demand, expanded program wins, and rapid production scaling.

Weaknesses

- Severe shortages in memory and storage have driven 4TB–8TB NVMe SSD prices above the value of gold per gram, pressuring data-center build economics. Nvidia’s prioritization of mid-range GPUs reflects supply constraints that may cap high-end output and margin expansion.

- Recent campaigns by North Korea–linked actors and malware distribution via trusted platforms highlight how infrastructure growth is outpacing security maturity. This elevates operational risk for enterprises, cloud providers, and defense contractors.

- The weakest stock this week in the XAR ETF was Byrna Technologies, which declined 3.16% after Wrap Technologies announced its new DFR X drone interdiction system, introducing fresh competitive pressure in the non-lethal public safety market.

Opportunities

- Expanded Space Force launch awards, Europe’s adoption of MQ-9B SeaGuardian, and HII’s scaling of autonomous underwater and surface vessels point to accelerating demand for ISR, satellite networks, and command-and-control systems. China’s plan for a massive satellite constellation further intensifies the global space race.

- The Amazon’s European Sovereign Cloud and OpenAI’s $10 billion, multi-year compute deal with Cerebras, signal a strategic shift toward sovereign infrastructure and non-GPU-centric architecture. This opens opportunities for custom silicon, energy-efficient computing, and regional cloud ecosystems.

- The U.S.–Taiwan trade framework, encouraging up to 40% of Taiwan’s semiconductor supply chain to relocate to the U.S., supports sustained CAPEX in fabs, equipment, and secure manufacturing, benefiting defense-aligned and infrastructure-critical suppliers.

Threats

- China’s ban on U.S. and Israeli cybersecurity vendors underlines accelerating technological bifurcation. This reduces addressable markets and increases regulatory and geopolitical risk for globally exposed tech firms.

- The UK’s accelerated development of long-range ballistic missiles for Ukraine highlights a shift toward deeper-strike and EW-contested battlefields. While supportive for defense spending, it raises tail risks of broader escalation.

- Advanced scams such as the “Truman Show Scam” demonstrate how AI is being weaponized to undermine confidence in digital investing platforms. Rising fraud risk may trigger stricter regulation and dampen retail participation.

Gold Market

This week gold futures closed the week at $4,588, up $87.10 per ounce, or 1.94%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.38%. The S&P/TSX Venture Index came in up 3.67%. The U.S. Trade-Weighted Dollar rose 0.23%.

Strengths

- The best-performing precious metal for the week was silver, up 11.00%. Gold and silver climbed to record levels in a broad-based metals rally after the U.S. Justice Department threatened the Federal Reserve with a criminal indictment, reviving concerns over the central bank’s independence. Gold spiked toward $4,600 an ounce, while silver rose above $84 after Fed Chair Jerome Powell said the potential indictment comes amid threats and ongoing pressure by the administration to influence interest rate decisions, according to Bloomberg.

- Central banks continue to increase their holdings. Polish Central Bank Governor Adam Glapinski plans to seek approval from the management board to raise gold holdings from 550 tons, or 28% of total reserves, to 700 tons.

- Metals continued their strong start to the year, with gold, silver, copper, and tin all reaching record highs, supported by expectations for lower U.S. interest rates and improving sentiment in Chinese financial markets. Commodities have posted substantial gains since late 2025, with precious metals benefiting from renewed pressure on the Federal Reserve by the Trump administration and a more tense geopolitical environment, according to Bloomberg.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 2.84% as the market cooled from historic moves. The LBMA has appointed ICE Benchmark Administration to run the platinum and palladium benchmark price auctions beginning in the third quarter of 2026, replacing the London Metal Exchange. This move consolidates all four precious metals benchmarks under ICE, which already administers LBMA gold and silver prices.

- According to RBC, Alamos Gold fourth-quarter production totaled 142K ounces, 12% below consensus. Production was lower at Island and Young-Davidson due to winter weather in December. As a result, full-year 2025 production totaled 545K ounces, below revised guidance of 560K to 580K ounces. Alamos Gold was the worst-performing stock in the GDX this week, falling more than 6%.

- Fund outflows from silver raise questions about the durability of the metal’s rally. More than 60 silver-denominated funds have seen aggregate net outflows of nearly $860 million so far this year. This contrasts with gold, which has seen net inflows of more than $2.55 billion, according to Bloomberg.

Opportunities

- Bloomberg reports that silver, currently at $89 per ounce, remains well below its inflation-adjusted peak of more than $160 per ounce. Gold surpassed its inflation-adjusted high three months ago and continues to climb. Despite skepticism about an imminent correction, silver may simply be catching up to gold by retesting prior highs.

- Silver demand is expected to remain strong as State Grid Corp. of China plans to invest 4 trillion yuan, or $574 billion, over the next five years to expand its power network. According to Shanghai Securities News, fixed asset investment will increase by roughly 40% through 2030 compared with the 2021 to 2025 period. China, the world’s largest clean energy investor, saw combined wind and solar installations surpass coal for the first time in 2024.

- Ivanhoe reported a positive update at Platreef, with the Phase 1 concentrator ramp progressing as planned and first concentrate sales completed. Shaft No. 3 remains on schedule for April 2026, increasing hoisting capacity roughly fivefold to about 5 million tons per annum. Phase 2 is on track to scale output to approximately 450,000 ounces of PGMs and gold within about 24 months, supported by a roughly $700 million senior project finance facility.

Threats

- CME Group will change the way it sets margins for gold, silver, platinum, and palladium futures after a surge in prices and volatile trading. The new approach will set margins based on a percentage of notional value, the CME said in a notice. Previously, margins were based on a fixed dollar amount. The shift takes effect from Tuesday’s close and follows a normal review of market volatility to ensure adequate collateral coverage, the CME said.

- Veteran investor Mark Mobius noted that China, India, Korea, and Taiwan currently offer the most attractive markets for global investors. Regarding gold, Mobius said he would not chase the gold price at these levels, but might consider buying if the price corrected by 20%.

- BMO’s analysis suggests that the balance between silver supply and consumption is a strong predictor of the gold/silver ratio, with periods of high physical surplus causing steady gains in the ratio. The gold/silver ratio is currently at its lowest level since 2013, below 50 at the time of writing. BMO forecasts a growing physical surplus, which is expected to push the ratio higher in the coming years, continuing a trend that has been sustained since the 1970s.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2025):

Trip.com

Japan Airlines

Alaska Air

Southwest Airlines

Delta Air Lines

United Airlines

COSCO Shipping Management

Allegiant

Embraer

Sun Country

SITC Management

Brunello Cucinelli

Royal Caribbean

Carnival

Viking

Tesla

Kering

Laopu Gold

BHP Group Ltd.

Glencore PLC

Ivanhoe

Alamos Gold

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All