“I’d rather risk ‘misspending a couple of hundred billion’ than be late to superintelligence.” – Mark Zuckerberg

Year end is often a time for reflection both personally and professionally. In business, you see things like organizational planning, budgets, and goal setting. In our personal lives, we have New Year’s resolutions. As I sit back and reflect, I seem to be rattling off year end letters too frequently lately. This is my 17th at iCM and 22nd overall I’ve been charged with writing. Time certainly flies.

In the investment business, it’s common to address not only what occurred during the past twelve months but also to provide an assessment of future prospects. So, I will address each of the major asset classes from a performance and valuation perspective. What’s unique in this 22nd edition is that this will be the first time that I refer to the same thing as both an opportunity and threat. This is not to say I haven’t experienced this before as an investment professional. I have, during the infancy of the internet, but those were a few years prior to my letter writing days. In this quarter’s Market Insights, My AI is Smarter than Your AI, I intend to address both the enormous potential and looming threat that Artificial Intelligence (AI) poses to our economy and capital markets.

Background

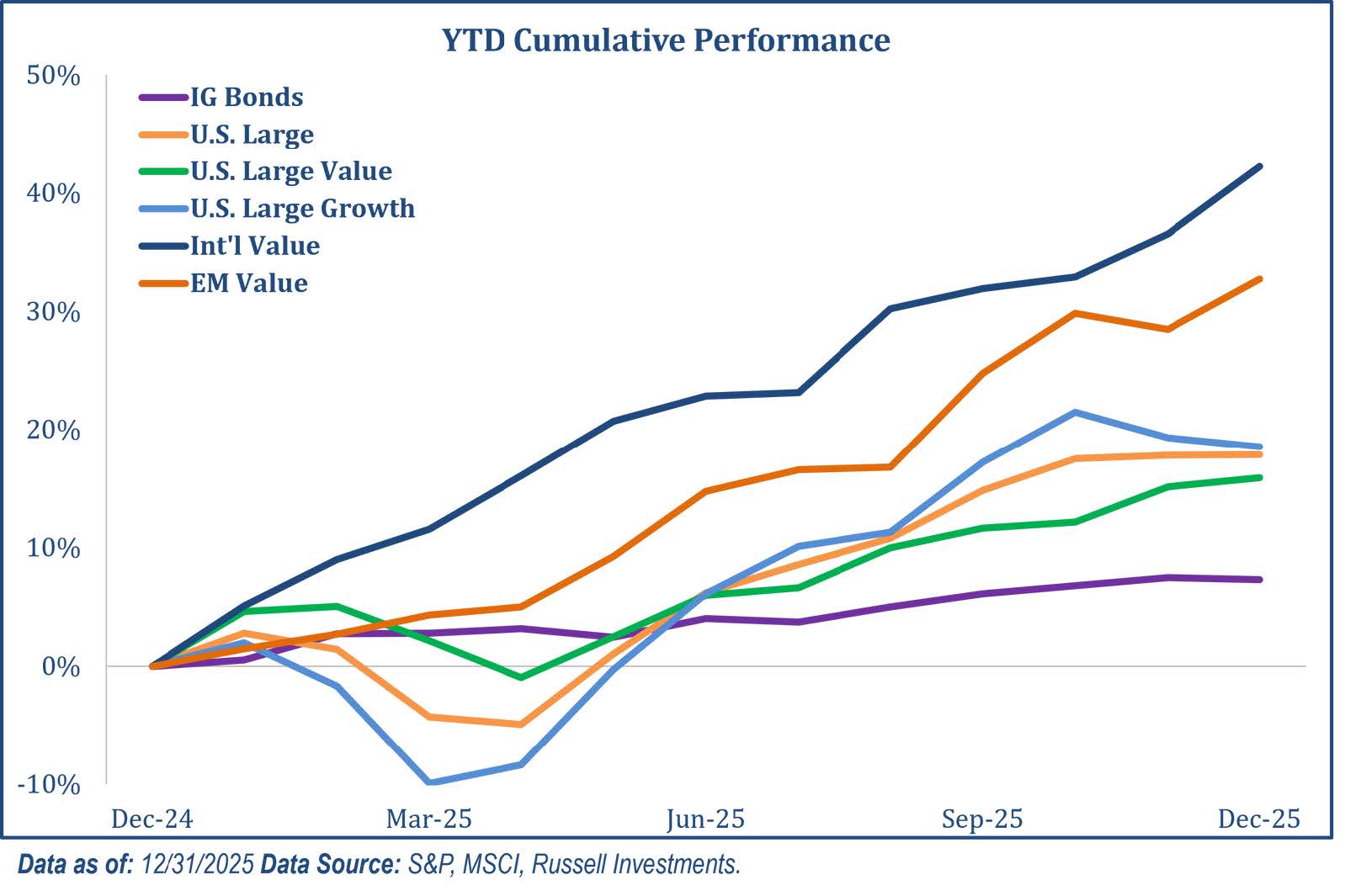

2025 was an excellent year for investors. While just about all major assets did very well, ironically it was not US equities leading the way. Both developed markets international stocks and emerging markets stocks handily outpaced the US with foreign developed stocks gaining 31% and emerging markets stocks gaining 34% vs a not too shabby 18% for large cap US equities. US Investment grade bonds turned in a solid year gaining 7%, bringing the three-year total for the conservative anchor to most portfolios to 4.65%.

Now, outside the US it paid to be price conscious. By focusing on undervalued foreign names in the developed world, you would have gained 42% in 2025. Not so for US investors where gains continued to be more robust for growth stocks which gained 19% vs 16% for their value counterparts. AI and the AI trade were still very much en vogue with companies like NVIDIA, (+39%), Palantir (+135%), Alphabet (+66%) and Broadcom (+50%) all having phenomenal years.

Chart 1

The AI Dilemma

Artificial Intelligence has been a buzzword for several years now but particularly so in 2025. For those who may not be fully familiar with what it is, AI is ultra sophisticated computer processing where machines are trained to think, act or even reason like humans. It has a nearly infinite learning capacity and speed. While AI has yet to surpass the general intelligence level of humans, most predict that this is an inevitable conclusion and only a matter of time.

While the concept of AI evokes a range of emotions from hope to fear, it does offer several meaningful benefits for the economy and capital markets. From an economic perspective, AI has the potential to substantially accelerate productivity by automating repetitive tasks, enhance decision-making, and improve efficiency across nearly every industry. This productivity boost effectively expands the labor force at a time when most developed economies (the US, Japan, Europe and China) face aging demographics and worker shortages. AI can also spark innovation creating entirely new industries ranging from advanced robotics and digital health to personalized medicine, while simultaneously reducing operating costs through process improvement and reduced error rates on both new and existing businesses. In research-heavy sectors such as biotechnology, AI can shorten development cycles, allowing new products and solutions to reach markets faster, fueling long-term economic growth.

From a capital markets standpoint, AI has the potential to serve as a powerful tailwind for corporate earnings through cost savings, margin expansion, and the creation of new revenue streams. It is also driving one of the largest capital expenditure cycles in decades, particularly in areas like semiconductors, data centers, cloud infrastructure, and electrical grid upgrades. These investments have broad spillover effects, benefiting not only technology companies but also industrials, energy providers, utilities, and real estate.

Now while all these things are well-known benefits, there is some fine print with regards to these benefits. Productivity growth (output per hour worked) and growth of the labor force combine to explain more than 90% of real GDP growth. As these two go, so goes the economy. Therefore, all the efficiency created by AI must be used to fill unmet demand or unfilled labor. To the extent that AI displaces labor, the benefits of productivity enhancements are offset all or in part by a contracting labor force. In simple terms, jobs provide income which is then spent into the economy. Society can theoretically become really efficient and productive but have no one to sell products to because everyone is out of work and has no money.

The second item in the fine print is that this hope for enhanced productivity has yet to materialize in any economic data nor has any company utilizing AI come even remotely close to turning a profit from those specific investments, which we’ll get to momentarily. The most recent release by the Bureau of Labor Statistics for the 2q of 2025, productivity grew at 1.5%. For perspective, average YOY productivity growth is about 2%. The most productive 5-year periods in US history were the post WW-II era of 4%, the early 1960’s of 3.76% and the years following the millennium where productivity gains averaged nearly 3.5% for 5 years. The most recent 5 years, at least 3 of which include the AI boom, have averaged 1.8%. Now it is not only possible but likely that some enhanced efficiency will be forthcoming. But, there isn’t much concrete that AI companies or our economy has realized to date. Most if not all of this is based on projections and hope, albeit life altering transformative hope, but hope nonetheless.

Broad US Market Valuations & Concentration

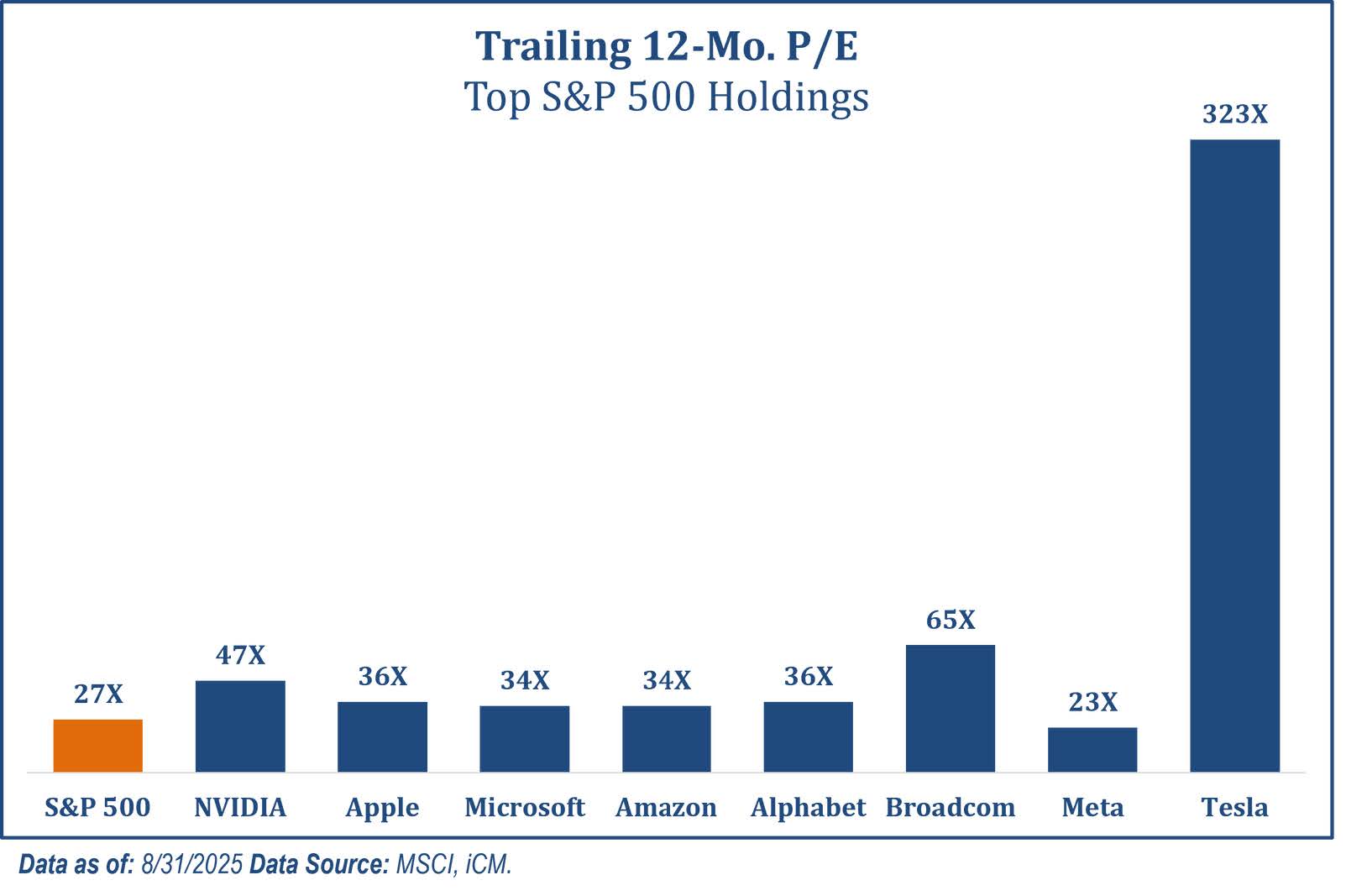

The S&P 500 Index is, of course, an index of 500 of the largest stocks in the US market weighted by market capitalization, meaning the bigger companies have a larger index weight. This weight is directly proportional to each company’s size relative to the size of the overall market. It’s basically a prorata calculation where the company’s market cap is divided by the total capitalization of all companies to determine the weight. Theoretically, the bigger more successful companies are more meaningful to the overall market and the economy so therefore they deserve a larger weight. Cap weighting is also self-adjusting and for the purposes of passive management and is the only way for all dollars to be invested without any shares being left over.

Now, while there are benefits of cap weighting there are some notable flaws, the main among them being potential concentration in the most overvalued names in the index. It’s not often that this occurs but does arise during euphoric times or market bubbles. As of early December, the top ten names for the S&P 500 account for almost 40% of the index. So, when you buy an S&P 500 index fund, you do get a piece of all 500 companies. But, almost half of any dollar invested in the S&P 500 is invested in just 10 companies.

This concentration has worked well over the past several years as many of these names were top performers. The top 10 companies in the S&P 500 are NVIDIA, Apple, Microsoft, Amazon, Alphabet Class A (Google), Broadcom, Alphabet Class C, Meta, Tesla, and Berkshire Hathaway. Nine of those top ten names are AI or AI adjacent companies. The average TTM P/E ratio for the top ten was 65x as compared to 27x for the index as a whole. For comparison purposes the average P/E for the past 50 years is 20x while the 10- year average was 25x.

Chart 2

There are three issues we see. First, there is concentration in the top ten names of the index, 40%. A somewhat obvious issue. Second, and perhaps not so obvious, nine of the ten names are part of, or impacted by, the same thing, AI. Investors in the S&P are not nearly as protected by diversification as they were in years past or as many anticipate that they are now. Third, there is a valuation concern. These names are expensive by historical standards.

Now, in investing, we use these long-term averages to estimate fair value. Fair value is a somewhat subjective concept, no one knows the precise level, but valuations have historically and very reliably reverted to their long-term averages over time which is what makes our current environment troubling. Is it possible that fair value is at the higher end of the range? Certainly, even though it isn’t likely. But even if that possibility causes us to exhale a collective sigh of relief, we must realize that with a higher fair value comes with it a lower implied future rate of return. There is no free lunch. If fair value is higher, your future return is reduced. It works like this. If you buy a business that generates $100 in annual earnings and you pay $1000 for it, your annual ROI is 10% (100/1000). What if you paid $2000 for the same $100 in profit? Your return is then 5%. The consequence of high valuations is either the potential for a sharp and immediate correction that will restore higher future returns immediately or the solace of a higher fair value and reduced future returns vs what we’ve experienced historically. Needless to say, elevated valuations extoll either a sharp but immediate, or a more gradual long-term consequence.

AI Circular Growth & Finance (The Feedback Loop)

If high valuations based on yet to be met promises of enhanced productivity and high ROIs for the AI companies are not concerning enough, the rather large elephant in the room is the whole AI, private credit, vendor financing arrangement that has emerged. The issue, in short, is that AI companies are creating their own demand by vendor financing their products to start up AI companies. Now, vendor financing isn’t exactly new and there’s nothing specifically wrong with it. I mean companies extend credit all the time. The issue here is the massive dollars being financed, relatively low ability to service that obligation without massive growth by the buyers, as well as the self-reinforcing nature of these relationships. I’ll give you an example.

NVIDIA and OpenAI recently announced a partnership under which NVIDIA intends to invest up to $100 billion in OpenAI as part of a massive AI infrastructure build-out. Put simply, OpenAI does a private stock offering which NVIDIA buys, sending the money for the shares of stock to Open AI. Open AI in turn sends that money right back to NVDIA to buy their chips. Completely circular. Open AI issued $100B in stock; they only make $4B in revenue and are upside down in profits. This is all hope and it’s pervasive. In the case of Open AI, little is debt on their balance sheet. Instead, they made “contractual commitments,” which they are obligated to repay, to the tune of $1.4T. While not exactly debt, it’s pretty close. Instead, the immediate funding is left to the vendor supplying the project. It isn’t on Open AI’s balance sheet. But, they are the lynchpin. If they fail to deliver, the dominos begin to fall. Oracle ($300B) and Microsoft ($250B) are the largest commitments. For Microsoft this represents about 7% of their total market cap. For Oracle, it represents 60%.

Now in other cases, finance is extended through more traditional arrangements of credit. Companies seeking to purchase AI components for their business go borrow the money. Traditionally, this has occurred through public bond markets. More recently private credit (non-publicly traded bonds) has become the go to space for both investors and companies alike. Again, using the Open AI situation as an example, you just replace the stock offering with money borrowed from private credit markets. Meta, for example, has borrowed some $29B from private credit. What does this do? Well, the risk of Open AI or some other company not being able to repay these loans is now born by the bondholder who can be an individual investor, a pension fund or an insurance company. According to a 2025 industry survey[1] of 101 insurance company asset allocators covering $4.5T in general account assets, this represents about 17% of FI investments in general accounts with some 62% of insurance companies investing in private credit. While it’s hard to trace private credit exactly because categorically it is lumped in with some genuinely benign investments, many commercial banks have extended credit lines to private credit companies with some estimates reaching 10% of capital for some of the more aggressive banks (Federal Reserve).

Now, why private credit not public markets? The main reason is due to the lending standards being more relaxed than public markets because of a lack of covenants. Therefore, in the event of an issue, it’s easier for the borrower to beg forgiveness or get an extension on a missed payment because these are not readily marked to market nor do they contain many of the restrictive covenants that protect public bond market investors. That’s why you can see a situation like the Blackrock Renovo issue occur. This was a private credit loan that was booked at 100% value just a month or two ago and was written to zero in one step. All the bodies were hidden.

Now, the last issue I’ll discuss relates to a typical asset liability mismatch. Most loans in private credit space are made with 5+ year terms. In fact, more than 30% of existing private credit has maturities extending to 2028 and beyond. The remaining ~55%+ mature prior to that but were issued in older vintage years, meaning that they themselves were issued with longer terms but are simply approaching maturity. Here’s the problem…the technology that they are purchasing with loan proceeds evolves so rapidly its obsolete in 18 months. By the time you need the newest version, you still haven’t paid off the outdated version. So, you have a classic asset liability mismatch. In all accounts, this seems to be this all-in win at all cost race, where many AI companies have pushed their chips in (no pun intended) in an effort to be first with the cost being potentially catastrophic if they aren’t.

Conclusion

While there are many life-altering possibilities that come from AI, signs of excess have become apparent to those who look. As I said, this appears to be a win at all cost race. What complicates this further is the degree of index concentration in these names, lofty valuations as well as the feedback loop of financing obligations, vendor contracts and earnings impact, all of which elevates the risk. Despite this, and perhaps ironically, I don’t see this as a 2026 item. Typically, the tide needs to go out to see who is swimming naked. In this case, capital needs to dry up. For that to happen either the economy needs to faulter, or there needs to be some high-profile idiosyncratic event, or a series of these events like Renovo to cause investors to really reconsider their appetite for these risky loans. Economically, 2026 should be strong, especially considering some of the expense provisions in the Big Beautiful Bill and the corresponding impact on growth.

Now when we speak of bubbles, investors conjure memories of 2000, 2008 or even 2022. Perhaps surprisingly, I will refer to the Internet Bubble as the best of the bunch and the most similar to our current scenario. While it is true that the ensuing market decline was very sharp, the Nasdaq declined by over 70% from peak to trough, there were places to hide. Within the US, small cap stocks and REITs looked quite cheap prior to the bubble bursting as did broad investment grade bonds. Non-US stocks, particularly emerging markets, were historically cheap. Investors not only had choices, but they also had some very good ones. In 2022 by contrast, both stocks and bonds, broad assets, were overvalued. It was difficult for investors to remain invested at their risk tolerance and earn a reasonable long-term return. In my opinion, even though it was shorter and the equity market decline less spectacular, 2022 was worse. Broad US stocks were down -18%, US bonds down -13%. Tricky to escape.

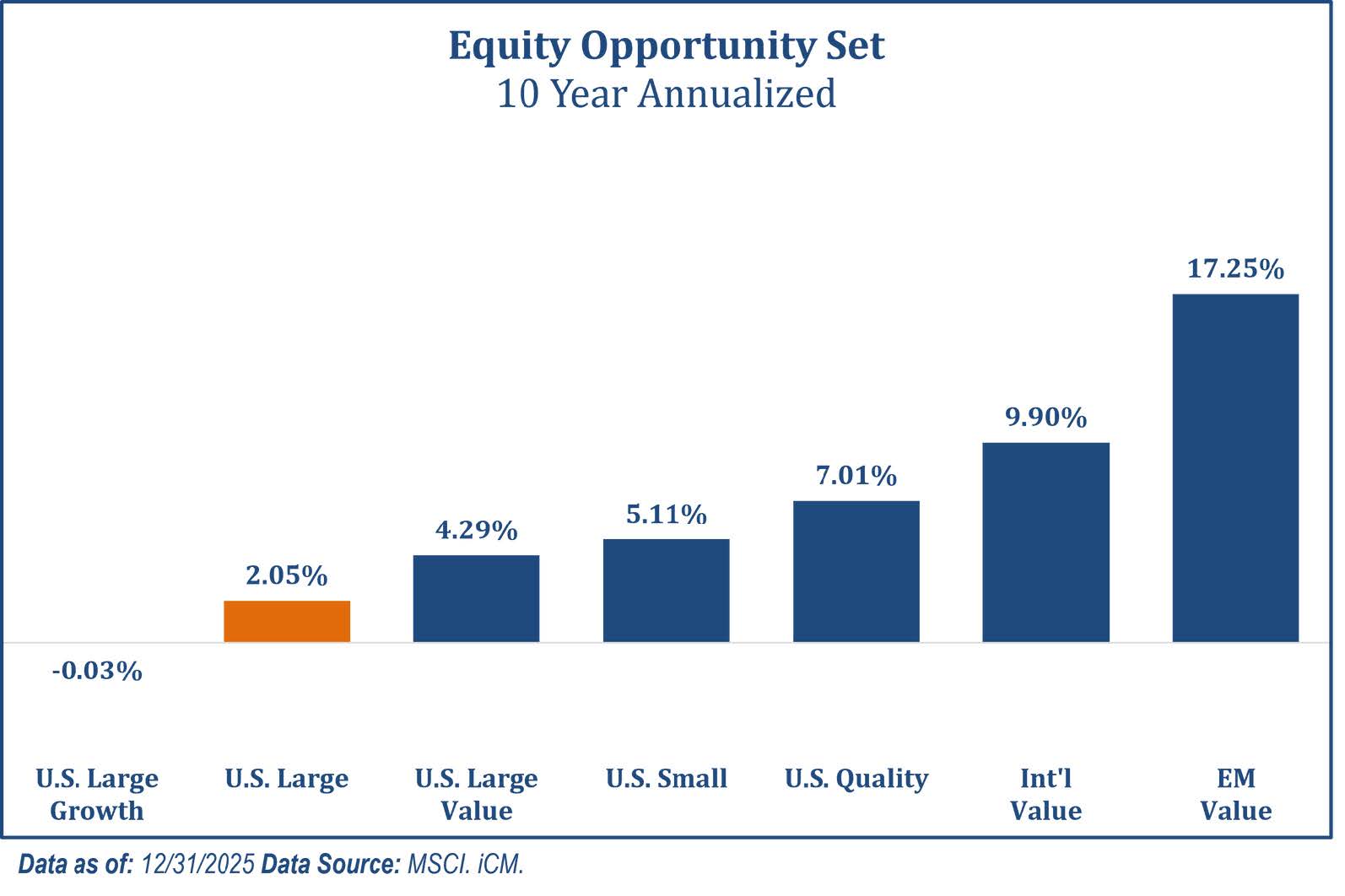

Unlike 2022 or even 2008, this isn’t an everything bubble. Domestically, quality US value stocks, a very specific definition of value, are as cheap as they’ve ever been. Small value names and REITs also show promise as do investment grade bonds. Outside of the US, developed market equities despite their gangbuster year in 2025 remain attractively valued. What’s more, if there is a benefit to excess spending and debt by the US, it should weaken the dollar further. This directly benefits non-us investments in stocks, bonds, and real assets (commodities). Emerging Markets stocks, particularly emerging value stocks, also coming off an impressive performance year, trade just above single digit valuations. Lower valuations combined with potential for higher earnings growth make emerging markets a compelling complement to developed-market portfolio.

Additionally, many emerging nations, in stark contrast to the developed world, are benefiting from positive demographics and structural growth with younger populations and a rising middle class fueling demand in sectors such as technology, consumer goods, healthcare, and financial services. This combined with pro-growth reforms as well as fiscal stimulus really makes for a compelling case for the emerging world.

Chart 3

As we conclude 2025, we reflect on and celebrate both the success we’ve had as investors as well as the path ahead. While AI provides life altering promise, its potential has caused some to reach farther than they should. This is concerning, no doubt. Aside from that, we remain optimistic, as there are many compelling investment opportunities that make our current landscape much different than even the one we lived through in 2022. Our focus remains on acquiring inexpensive assets from across the globe while seeking to avoid those that are most expensive and overvalued. That has been our mandate for the 17 years I’ve been letter writing at iCM, and the 5 or so that occurred before that and is something we believe to our core provides the best long-term path for investors. Embrace the undervalued and avoid the landmines. Pretty compelling. As always, I want to wish each of you a happy and healthy holiday season as well as a joyful and prosperous new year. Thank you as always for your trust and confidence.

By Michael Paciotti, CFA

Originally published on Integrated Capital Management

For more news, information, and strategy, visit the ETF Strategist Content Hub.

[1] Insurance asset managers boost private market allocations – Value of public assets held by insurers using external managers continues to decline, The Asset July 7, 2025

All data as of 12/31/2025 unless otherwise noted.

Market Insights is intended solely to report on various investment views held by Integrated Capital Management, an institutional research and asset management firm, is distributed for informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. Integrated Capital Management does not have any obligation to provide revised opinions in the event of changed circumstances. We believe the information provided here is reliable but should not be assumed to be accurate or complete. References to specific securities, asset classes and financial markets are for illustrative purposes only and do not constitute a solicitation, offer or recommendation to purchase or sell a security. Past performance is no guarantee of future results. All investment strategies and investments involve risk of loss and nothing within this report should be construed as a guarantee of any specific outcome or profit. Investors should make their own investment decisions based on their specific investment objectives and financial circumstances and are encouraged to seek professional advice before making any decisions. Index performance does not reflect the deduction of any fees and expenses, and if deducted, performance would be reduced. Indexes are unmanaged and investors are not able to invest directly into any index. (MMXXVI)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi