When investors think about risk in equity portfolios, the usual suspects come to mind: market risk, sector risk or maybe even macroeconomic risk. But lurking beneath the surface is a less obvious, often underestimated threat—style and factor risk.

In today’s rapidly shifting markets, such unintended tilts can quietly undermine long-term returns, adding volatility without delivering consistent rewards. For core equity allocations, we believe actively reducing these risks is essential to keep an investment strategy on course.

What Are Factor and Style Risks and Why Do They Matter?

Factor and style risks refer to the exposure a portfolio has to systematic factors—like value, growth, momentum or low volatility. While some style tilts are deliberate, many creep in unintentionally, even in “core” equity allocations meant to be style neutral. The problem? Style and factors go in and out of favor, sometimes violently, and portfolios with hidden tilts can get whipsawed by these rotations.

Recent market history has made style risk harder to ignore. Three trends stand out:

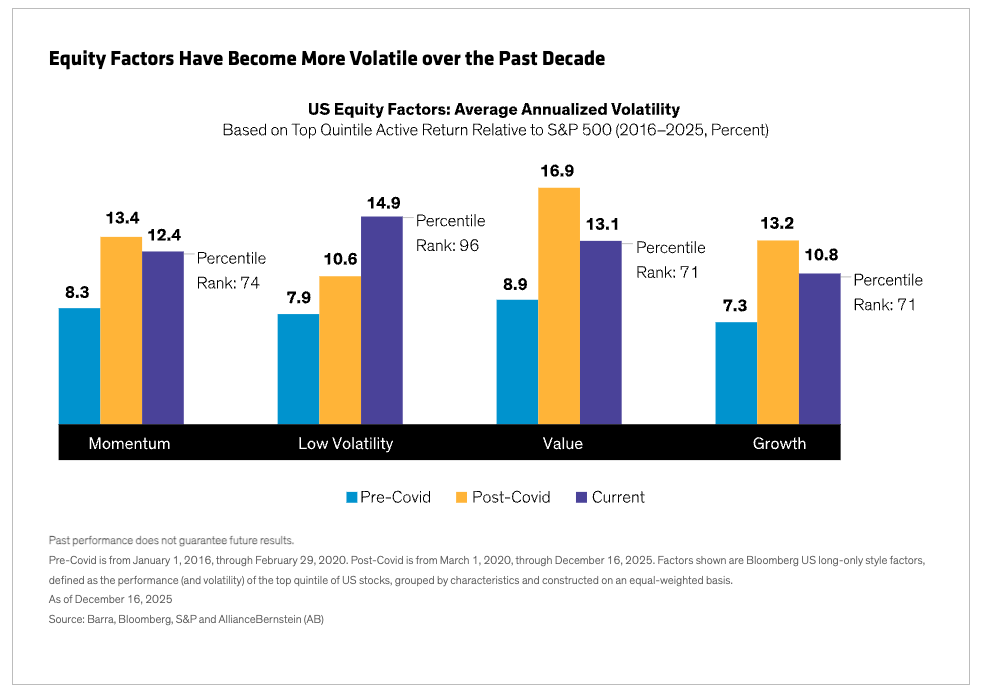

1. Factor and Style Volatility Is Rising

Factor volatility can be measured by looking at how much an equity factor’s returns swing relative to the market. Our research shows that the annualized volatility of momentum, growth, value and low-volatility factors has risen substantially since the COVID-19 pandemic (Display). That means an unintentional tilt in a portfolio can introduce more risk than in the past.

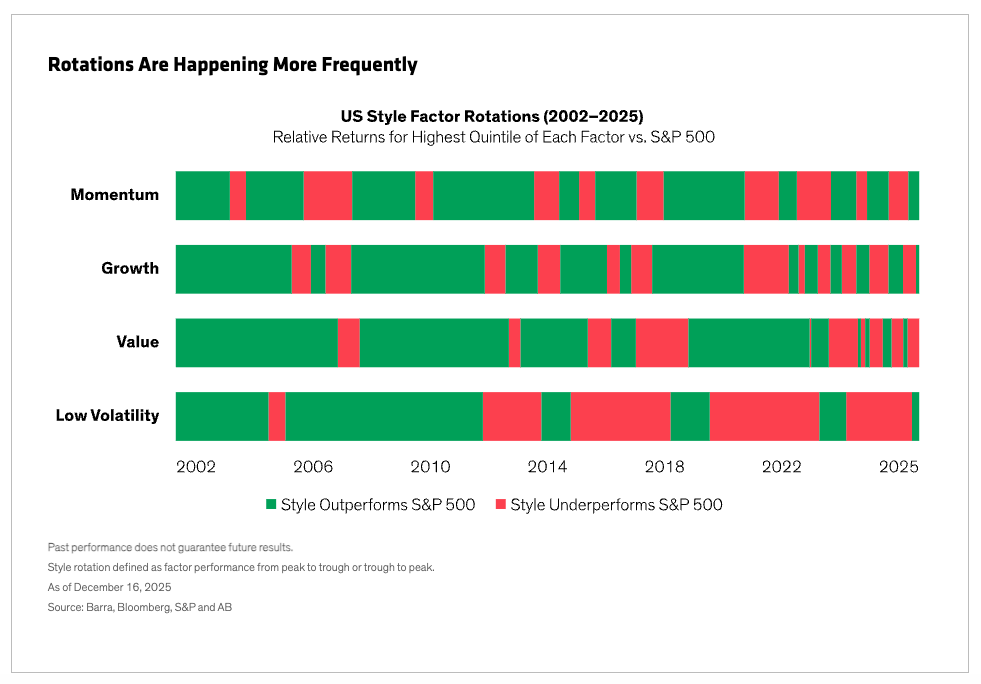

2. Rotations Are Getting Faster

Not only are style factors more volatile, but leadership among them changes more frequently than in the past (Display). Over the last five years, style performance has changed direction every 233 days on average, compared to every 796 days between 2010 and 2015. What worked last year (or last quarter) may lag badly the next.

Timing market inflection points is extremely difficult in normal market conditions. In the past, it may have seemed easier as investors could ride a sustained period of style outperformance that often lasted years. Now, with rotations happening faster than ever, we think trying to time style exposures or rely on past winners is an even dicier strategy that’s nearly impossible to execute and can have negative tax consequences.

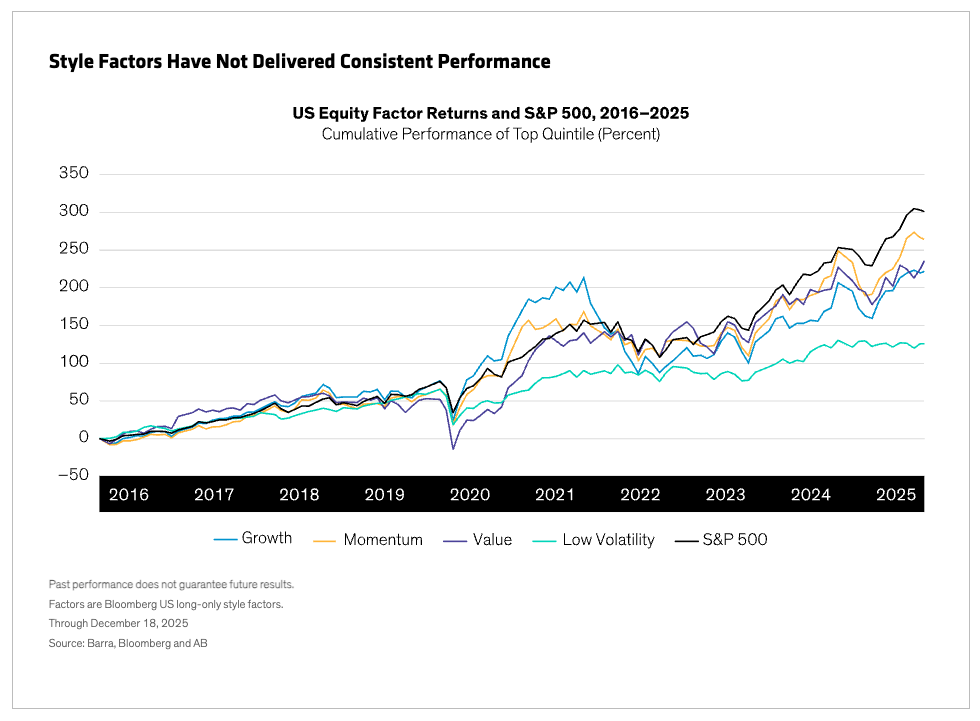

3. Style and Factor Tilts Don’t Pay Over the Long Run

Style and factor tilts haven’t consistently delivered excess returns over the long term. Of course, investors may seek exposure to growth, value or lower-volatility stocks depending on individual risk appetites, financial goals and investing philosophy preferences. These exposures have a role to play in a diversified allocation.

However, for investors seeking stability in a core equity allocation, we think these tilts can be counterproductive. A look at the last decade shows that while some factors have their moments, none reliably outperform the market over time (Display).

How to Reduce Style and Factor Risk: Practical Steps

So, what can investors do? As we see it, in a core equity portfolio, the key is to actively minimize unintended risks across the allocation. By doing so, a portfolio team can ensure that they’re taking the right stock specific risks, for which clients expect to be rewarded.

Actively Monitor and Neutralize Factor Exposures

Neutralizing tilts means balancing factor exposures so no single factor or style determines performance. We see attractive value opportunities in the US today, for example in financials and industrials. Growth-oriented sectors such as communications and healthcare also present compelling opportunities. By having both, we can harness alpha opportunities while offsetting factor risk via diversification.

But selecting stocks should be rooted in fundamental work to find companies with strong competitive positions, robust cash flows and management teams that can allocate capital wisely. We look for enduring businesses in attractive industries—what we call “good houses in good neighborhoods”—without letting style preferences override fundamentals.

Focusing on fundamentals is the foundation. Next, positions should be sized to maximize alpha while neutralizing factor and style bias at the portfolio level, which can help reduce relative performance volatility.

Quantitative risk tools are also essential to measure a portfolio’s exposure to factors. When risk models detects unintended tilts, position sizes can be adjusted to minimize factor risk and reduce relative performance volatility.

Manage Risk at Multiple Levels

Disciplined risk management goes beyond style and factors. Portfolios should also actively manage other market, sector and mega-cap risks, and use position sizing to avoid concentration. Cluster analysis is another technique for detecting hidden correlations between diverse groups of stocks that may move together for reasons unrelated to fundamentals.

Thematic analysis can also help decipher what’s driving returns in real time—whether it’s AI, inflation or policy changes. Exposures can be fine-tuned as themes shift to steer the portfolio away from fads and crowded market segments. These risk-control tools complement a factor-neutral agenda by making sure that portfolio returns aren’t being unwittingly affected by unpredictable forces that aren’t always easy to detect.

As markets evolve, so do the hidden influences that shape portfolio outcomes. Investors who understand and manage style and factor risks can avoid unnecessary detours and maintain a clearer path toward their return goals. So, take a fresh look at your portfolio’s factor profile and ask whether those exposures reflect conviction or coincidence. Portfolio managers who actively control these risks can help ensure your core equity allocation stays balanced, intentional and better positioned for a more comfortable ride through the rotations ahead.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi:Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein