Healthcare stocks were rattled by US policy uncertainty in 2025. But signs of resilience have surfaced as the sector reaffirms its defensive strengths and growth potential, sparking a shift in investor sentiment.

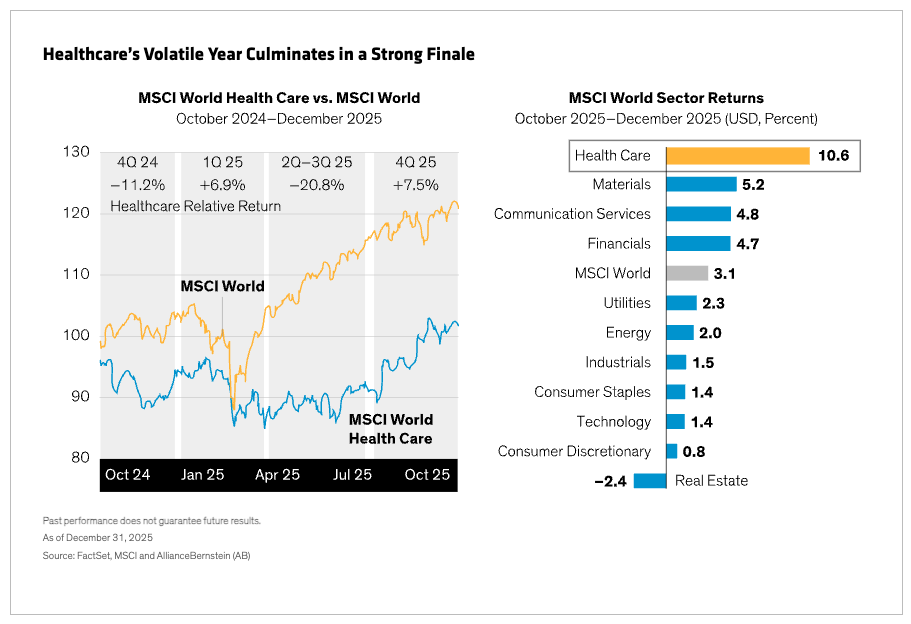

It’s been a volatile ride for investors in healthcare stocks since the US election in November 2024. The sector has seen dramatic turns in performance, at times weakened by concerns about US regulatory change, and at times outperforming a market alarmed by trade wars. Yet despite underperforming in 2025, global healthcare stocks finished the year on a high note, outpacing the MSCI World Index by 7.5% in the fourth quarter—well ahead of the pack (Display).

Policy Concerns Are Easing

After an erratic year, what can we expect in 2026? We think investors will rediscover the attractive long-term attributes of select healthcare companies as the following policy concerns continue to diminish.

-

Regulatory uncertainty: Investors initially feared an upheaval in healthcare regulations after Trump’s election. However, key agencies like the Centers for Medicare & Medicaid Services and the Food and Drug Administration are functioning similarly to previous administrations. Positive signals for innovation are emerging. While vaccines have been impacted by policy changes, they account for only a small fraction of healthcare profits.

-

Life-sciences funding: After big reductions in early 2025, funding is rebounding. Congress’s proposed budget has brought life-sciences funding back to prior-year levels.

-

Medicaid reductions: Plans to cut $1 trillion from Medicaid have grabbed headlines. But these reductions will be spread over a decade, averaging around $100 billion per year, or less than 2% of annual US healthcare spending. We expect individual states, which co-fund Medicaid with the federal government, to offset some of the federal spending cuts.

-

Pharmaceutical tariffs: Fears of a tariff hit have eased as Trump negotiates most-favored-nation (MFN) pricing agreements with major pharmaceutical companies. Most large drugmakers are building manufacturing facilities in the US, which will shelter them from tariffs. And any industry tariffs would fall under broader agreements (e.g., the EU’s 15%), which would, if enacted, only have a marginal impact on earnings.

-

MFN pricing: So far, the US administration has reached drug pricing agreements with 16 pharmaceutical companies. Although these roughly align Medicaid pricing with that of other developed countries, we believe this is only a minor challenge to drugmakers, as Medicaid’s share of pharma sales is small and already discounted. Notably, launching new drugs at MFN pricing levels could inadvertently raise US launch prices while lowering access to medicines in other countries facing budget constraints.

Back to Business Fundamentals

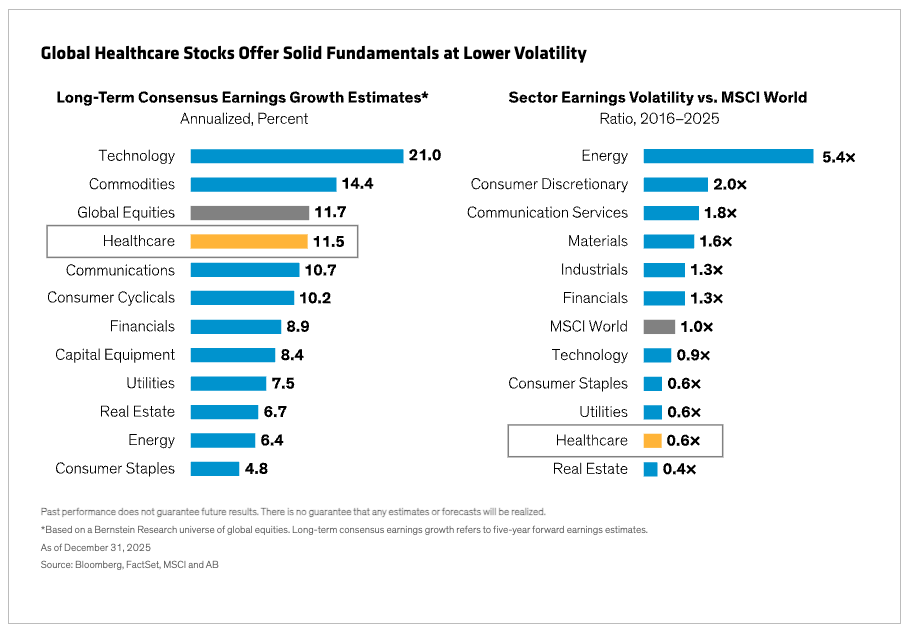

As policy concerns ease, we expect the market to refocus on fundamentals. While last year’s performance elicited questions about healthcare’s stability, we think the sector’s solid performance during the most severe bouts of trade-war volatility and AI-bubble fears shows that its traditional defensive features haven’t been compromised. Despite last year’s volatility, the healthcare sector continues to offer strong, long-term earnings growth potential of 11.5% annualized, well above most equity sectors (Display). And since healthcare growth is rooted in economically resilient businesses, the sector’s earnings volatility is much lower than the market.

Unlike other defensive sectors, healthcare provides meaningful growth and upside potential. That’s because healthcare companies sell products that can improve patients’ quality of life and longevity, and these products are backed by innovation that is often a catalyst for exceptional growth rates. During 2025, we’ve seen new product launches, such as a twice-yearly injection that prevents HIV infection—a potential game changer for global public health—and a new class of non-opioid pain medication, offering effective pain relief without addiction risk.

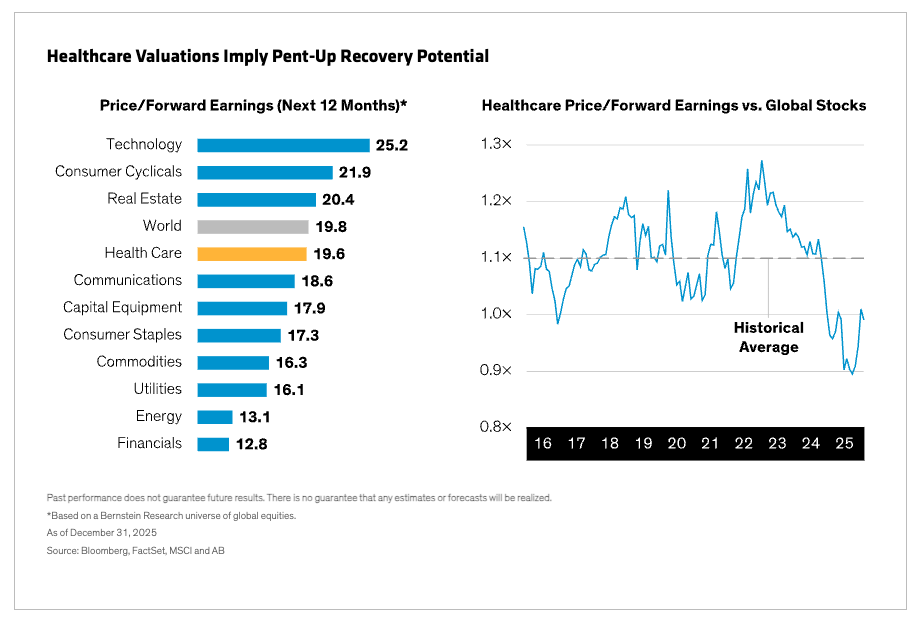

The innovative forces behind these developments aren’t fully reflected in valuations. It’s true that healthcare price-to-earnings ratios aren’t cheap versus other sectors. But given that global healthcare stocks typically trade at a premium to the MSCI World, we believe sector valuations relative to their own history are especially attractive today (Display).

AI’s Shadow—and Opportunity

Of course, healthcare stocks have been trading in the shadows of the AI-driven technology mega-caps. Technology stocks have continued to draw fund allocations away from healthcare and other industries. However, we believe investors will increasingly demand clear evidence that AI is being broadly adopted across the real economy and generating tangible productivity and profitability gains.

As this process unfolds, we think the healthcare sector is well positioned to benefit from AI adoption that fuels growth and margins, especially given the pressing need for better outcomes and the sector’s high labor intensity. In 2026, we expect to see many new AI use cases in healthcare that drive measurable contributions to the top and bottom lines of businesses.

Examples already abound, from AI-enabled surgical robots to cancer-detecting patches and systems that help healthcare facilities admit patients faster, leading to higher capacity utilization. As we see it, if AI delivers on its transformational promise, the healthcare sector will be one of the biggest winners. And if AI disappoints, the healthcare sector still wins via investor demand for diversification.

In fast-changing market conditions, we think the key to tapping into the healthcare sector’s potential is constant: focus on business, not science. That means looking beyond headline-grabbing innovations and hard-to-predict drug development, while prioritizing companies that demonstrate operational excellence, prudent capital allocation and strategic reinvestment. By targeting these enduring features of sustainable growth, we believe investors can benefit from a portfolio of durable healthcare stocks that can shine brighter as policy concerns are resolved.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein

Read more commentaries by AllianceBernstein