Today we continue anticipating 2026, this time shifting for the first part of the letter from economic issues to geopolitics before making some of my personal general forecasts.

Economics and geopolitics are closely related. Geopolitics is about the way national leaders interact with their counterparts, but economic trends also define and constrain their goals.

The most obvious intersection is in international trade. Last week President Trump threatened new tariffs on several European countries who were resisting his (inexplicable, at least to me) desire to buy Greenland. I have no idea where this is going but it’s a good example of why we can’t ignore geopolitics. Their words and actions have direct impact on the economy, the financial markets and our investments.

Below I’ll share the latest thoughts from some of the best thinkers I know. For geopolitics, that means George Friedman, Ian Bremmer and Ray Dalio. But I want to whet your appetite with a brief comment from Peter Boockvar.

“The world is changing big time in front of our eyes, the direction of global trade flows is morphing and diversifying, and investors need to have a global lens when investing in the coming 5-10 years as it’s not going to be just about the US, the S&P 500 and the Mag 7. At the same time, gold is now becoming the most important global reserve currency.”

Peter’s point is well taken. The US now accounts for something like two-thirds of global stock market capitalization. Naturally, many investors worldwide have most of their risk assets here – especially passive index investors. And many non-US stocks depend on US markets. The results have been pretty good but may not remain so. Both trade flows and capital flows are changing.

Ray Dalio has an interesting point on that, which we’ll talk about below. But let’s start with George Friedman, who expects a major change in what is probably today’s most important international rivalry.

Radical Change

George Friedman’s Geopolitical Futures is one of my best sources. (I have known George for well over 20 years. He is a close friend.) He’s been tracking world trends for decades and isn’t afraid to make specific forecasts. George also has a fascinating theory of socioeconomic and institutional cycles. Both are set to peak in the next few years, with likely major effects on the world order.

But George also sees another big change coming even sooner. In short, he thinks 2026 will be the year when the US and China set aside their economic and military rivalries. In his view, the two governments really have no choice. They need each other too much to let the current disputes fester.

In his 2026 Forecast, George describes how China emerged as a great power in the wake of Russia’s post-Soviet decline. The US no longer had to resist Russia but had a new imperative to challenge China’s growing power, both economic and political.

George calls this “a normal process” but thinks it will evolve further in 2026.

“China and the U.S. are already engaged in military and economic competition. Although both have substantial military capabilities, neither benefits from going to war with the other because, ignoring the fact that neither can be assured of victory, they depend on each other economically. China needs the U.S. to buy its products, and it has always relied on Western investment to fuel its economic growth. The U.S. needs to import cheap products for consumers and downstream industries to control inflation, and it needs to divert investment into more innovative and profitable economic sectors.

“Put simply, the U.S. can’t maintain hostilities with a country on which it depends economically. Neither can China. Given this reality, Washington had to rationalize its relationship with Beijing without engaging in outright conflict. Its method for doing so was tariffs, the imposition of which created a serious weakening of the economy in China, raised unemployment and created severe weaknesses in its real estate and financial sectors.

“It also created economic problems in the U.S. by increasing the price of consumer goods. The effect on the Chinese economy was more significant than on the American economy. The solution, then, will be two-fold. First, the United States and China will reach an agreement to ease military tensions. Second, the U.S. will remove or at least moderate tariffs.”

He goes on to describe a potential compromise that would let the US and China resolve their different positions on Taiwan. I know, hard to imagine, but George sees a way it could happen.

With Taiwan off the table, the world could see major changes in the near future.

“This would establish a radical new global geopolitical system: a bipolar world with two powers not engaged in either economic or military confrontation. (Considering what happened after World War II, this kind of change isn’t unprecedented.) If such an agreement was reached between the U.S. and China, there would be serious challenges to overcome, but the world would be anchored again, and the risk of conflict would be dramatically reduced.”

This redefined relationship between the world’s two largest powers would have follow-on effects in various countries and regions. George describes many of them in the rest of his 25-page annual forecast, which I highly recommend reading. You can get your own copy by subscribing to Geopolitical Futures. It is well worth the very reasonable price.

Before we move on from China, let’s recognize that it is an economic powerhouse, and in much the same way that the rest of the world looks at the US because we have significance, we need to pay attention to China because they are important in the global economy. My friend Dr. Michael Pettis who is an economics professor for the last few decades in Beijing summarizes his latest longer report this way:

“China’s economy ended 2025 much as it began—with an overreliance on a growing trade surplus and non-productive investment to drive growth. A sharp decline in the latter over the year saw quarterly GDP growth decline steadily from a very strong 5.4% in the first quarter of the year to 4.5% in the last quarter.

“Beijing will almost certainly do everything it can to revive growth in fixed asset investment in early 2026, but because property investment is almost sure to continue declining, and because it has become harder than ever to justify a surge in infrastructure investment, I expect much of this investment growth to occur in the non-involuted manufacturing sectors. These are the sectors in which foreign competitors are going to be under intense global pressure in 2026.

“The biggest question mark in 2026, as it was in 2025, is the evolution of China’s trade surplus. If it continues to grow strongly, this will reduce pressure on Beijing to increase investment and, with it, China’s high and rapidly rising debt burden. If, on the other hand, external pressures force a contraction in China’s trade surplus, Beijing will set off an even faster rise in China’s debt burden as it unleashes even more investment to prevent growth from slowing.

“If all of this sounds like it might be the same story I have been discussing in my reports all last year, that’s because it is. In spite of rising worries about how an unsustainable reliance on debt and trade surpluses is needed to keep growth at targeted levels, nothing fundamental has changed in the way Beijing manages the Chinese economy.

“In the end, we are still stuck with the same old set of conditions. If the US is able to stabilize and reduce its trade deficit, either surplus countries (which mainly means China) will have to go through the very painful process of reigning in their trade surpluses, or someone else (and this mainly means Europe) will have to go through the very painful process of replacing the US as the main absorber of global excess saving. I don’t know which it will be, but this is just arithmetic.”

As I’ve been saying for years, China is increasingly important in the global economy. But it is not a one-way street. They have significant debt, demographic and “domestic tranquility” issues. Not unlike the US. Both countries are constrained and both need to work with each other because of their own internal issues. Not doing so is a real problem.

Iranian Effects

Next, we’ll turn to Ian Bremmer. His Eurasia Group’s Top Risks 2026 report describes the geopolitical risks they think most likely to play out this year. Here are the provocatively titled top 10.

-

Risk 1: US Political Revolution

-

Risk 2: Overpowered

-

Risk 3: The Donroe Doctrine

-

Risk 4: Europe Under Siege

-

Risk 5: Russia’s Second Front

-

Risk 6: State Capitalism with American Characteristics

-

Risk 7: China’s Deflation Trap

-

Risk 8: AI Eats Its Users

-

Risk 9: Zombie USMCA

-

Risk 10: The Water Weapon

It’s important to note these are risks, not predictions. They are things Ian and his team could prove important in 2026, and which are likely enough to justify preparation.

You can read the full report for more details. I want to think about another topic Ian recently mentioned in his recent client letter: Iran. We had a little flurry of activity this month which first suggested the US was closer to forcing a regime change there. That’s now out of the headlines, though it’s possible things are happening behind the scenes.

Many analysts (including Ian and George) think the Iranian opposition is too fragmented to successfully challenge the government. But what if they aren’t? What would be the effects of Iranians, maybe with US help, forcing a change to a more secular, freely elected government?

When that thought comes up, we usually think about effects on the oil market. Those could be significant, but there are second and third order effects, too. For one, the various terrorist and anti-Israel groups that Iran presently supports might shrink or disappear. The Middle East could quickly become a more peaceful place as a freed Iran tries to become a good neighbor. Then what?

The closest analogy I can imagine is 1989, when the Iron Curtain fell in Eastern Europe. West Germany made giant investments to raise East Germany’s dilapidated infrastructure and living standards. This raised interest rates, which within a few years demolished Europe’s currency mechanisms. Not entirely good news, in other words. But then, all things change over time.

Hard Currency

Global elites gathered in Davos this week for their annual pow-wow. News headlines were about Trump repeating his demand to acquire Greenland, and the united opposition from Europeans. But that wasn’t the only topic. They are seriously discussing the kind of sweeping change Peter Boockvar described in the quote above.

Ray Dalio, who was there, appeared in a CNBC interview from Davos. I’ve written before about Ray’s “Big Cycle” idea. He thinks the wheels are turning faster to a climactic conclusion faster than I do. But we agree that we are close to that point. The situation is evolving from trade wars to what he calls “capital wars.”

Here’s Dalio, via CNBC:

“On the other side of trade deficits and trade wars, there are capital and capital wars. If you take the conflicts, you can’t ignore the possibility of the capital wars. In other words, maybe there’s not the same inclination to buy at U.S. debt and so on.

“We know that both the holders of U.S. dollars are denominated ... and those who need it, the United States, are worried about each other. Right? So, if you have other countries who are holding it, and they’re worried about each other, and we’re producing a lot of it, that’s a big issue.

“When you have conflicts, international geopolitical conflicts, even allies do not want to hold each other’s debt. They prefer to go to a hard currency. This is logical and it’s factual, and it’s repeated throughout world history.”

Let’s talk about this word “trade.” The classical use is about countries buying and selling goods from each other. Governments have always tried to regulate this (and usually tax it) but almost everyone sees the benefits. Trade is good, though it does have side effects that have to be managed. More recently we’ve see growing trade in intangible goods – software, for example – and also services. This raises different issues but again, it’s mostly beneficial.

All these forms of trade are bi-directional. Goods and/or services flow one way, then payment flows the other way. This can happen in many ways but ultimately everyone’s books have to stay balanced. Problems arise when they don’t.

The US, as issuer of the global reserve currency, benefits from world trade by being able to borrow at low rates. The countries whose exports we buy use the dollars we pay to purchase US assets, including our Treasury debt. Dalio says we should not assume this will continue.

When Dalio says investors in other countries are losing the desire to own US debt and “prefer to go to a hard currency,” I’m sure he means gold.

Now scroll up and re-read that Peter Boockvar quote in my opening: “Gold is now becoming the most important global reserve currency.” This is gold’s classic role, of course. It is the only “currency” not issued by a government, so it doesn’t have the kind of potential conflicts Dalio describes.

In a world of growing conflict and diminishing trust, it makes perfect sense for everyone to seek some neutral payment mechanism. Is this why precious metals have been rising in price? At least partially, for sure. But I agree with Ray that big changes are afoot.

Up, Down, or Muddle Through?

Just like in the beginning of 2025, 2026 is a difficult year forecast because the data is inherently mixed. As Wolf Richter says: “Consumers may be in a foul mood, but they’re making money and are spending it, and are still saving some.”

If you have only been reading the mainstream media, you would think that consumers are falling behind inflation. Actually, consumer income is up for the last two years over inflation, and that doesn’t even include government transfer spending or benefits like Social Security. And while Americans have never been big savers, the actual savings number is 3.5%.

All that said, consumer spending is skewed to the top 50% in terms of income of the US population. Which of course makes sense, as that is where the money is. But it is even more skewed to the top 20% and 10%. If you pay attention to the earnings calls from various large corporations, they echo this theme of a two-speed economy.

And this will have significant consequences in the 2026 election. As we all know by now, “It’s the economy, stupid!” And your individual perception of the economy influences you.

It reminds me of the old somewhat risqué joke of the wife walking in and finding her husband with another woman in his bed. After swearing he did nothing, he says “Who are you going to believe, me or your lying eyes?” That will be the political question for the third quarter of 2026.

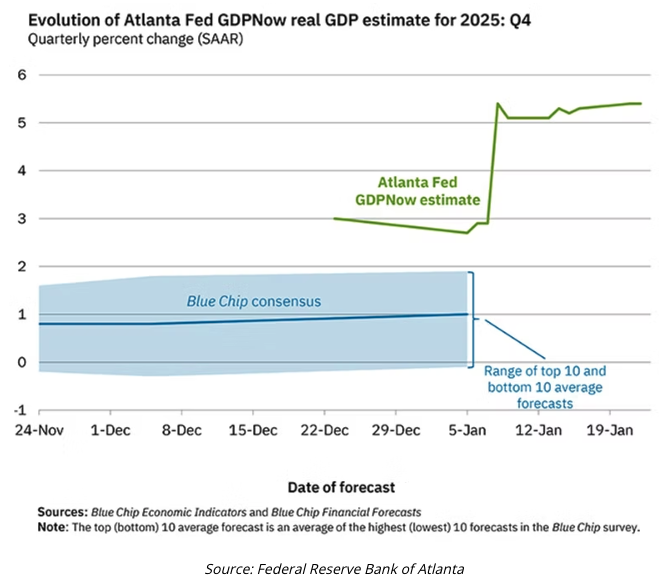

Let’s look at GDP by quarter for the last few years. Note the significant drop in first-quarter GDP, which happened because of the front running of companies buying goods and services in advance of tariffs in the US. Then GDP rebounded substantially.

We won’t know initial fourth-quarter GDP estimates for another few weeks, but the Atlanta Fed GDP Now estimate is, wait for it, 5.4% for the quarter.

Obviously, most economists see a lower rate but that has been the case for the last year or so. In the last few days, we’ve seen several top analysts increase their projections, though not as a enthusiastically as the Atlanta Fed.

Going to a somewhat neutral source, the CBO projects the first quarter to be 2.9% GDP growth. Nonetheless, when we get official first quarter GDP data, that negative anomaly from the first quarter of 2025 will go away and annual GDP could easily be in the +4% range. The Trump administration will be telling the country that the economy is doing great and they are the reason for it.

The Democrats will be talking about “affordability.” Which is a very important issue for most consumers and voters. The Republican counter is, “Who are you going to believe? Me or your lying prices at the checkout counter?” doesn’t have the emotional impact.

I think, sadly, this is an argument the Republicans will find difficulty winning. Consumers don’t “eat” or buy with GDP forecasts.

While we are nine months away from the election, it is highly likely that the Republicans will lose control of the House. And given the particulars of the various races, it is likely they keep control of the Senate. Whatever Trump really wants to do in terms of significant change, needs to be done in the next nine months. If Ray Dalio is right, and we see a crisis before 2029-30, it will be a very challenging time for everyone in DC but especially the president.

A few final thoughts. I read a great deal of material every week. While some of it is from new sources readers and friends put in my inbox, I have come to rely on two handfuls of regular independent analysts to keep me up-to-date. I have gotten to know them over the years. Some are decidedly bearish in their views, some are always optimistic and some can change on a moment’s notice.

There is certainly enough reason to be pessimistic. Unemployment is trending up, although slowly. Inflation is certainly not under control, although I expect it to trend down this year. Whoever Trump appoints as Fed chair will have room for a few rate cuts but not many more.

The reality is that the large GDP numbers are the result of spending on data centers and artificial intelligence. That’s a good thing. I think it will continue. I expect that the Supreme Court will reign in Trump’s rather expansive use of tariffs. How much? TBD. I have no idea why they are taking so long on this decision. Hopefully, that sentence will be obsolete on Monday.

At 3% GDP growth, it’s hard to say “Muddle Through.” 3% is gangbusters. Except not for the bottom 50% of the country. For them, Muddle Through would be an improvement.

Flies in the ointment? Certainly, we have to watch unemployment. And healthcare costs could become a very real election hot button. Inflation as measured by PCE is significantly weighted to healthcare costs. Those could actually rise enough to increase PCE significantly, making it difficult for the Fed to cut rates. That is a very, very real risk.

For all the talk about the end of globalization, global trade will continue to increase. Technology improvements will continue to astound. Global poverty will decrease and most measures of economic life will improve.

Until of course, we reach the final reckoning with sovereign debt, not just in the US but in the entire developed world. Japan is still searching for that windshield and getting closer. As is Europe. We will pay attention to them as what happens there will be a precursor to what happens here.

And as has been the case for the last 26 years, I will be here in your inbox every Saturday morning talking about the world of economics and finance. Stay tuned…

Up in the Air with Zoom?

While I know this will change, perhaps quickly, I have no travel plans on my calendar for the first time in a long time. I have various meetings and conferences in the future, but no actual flights set.

One reason for that is Zoom and its various competitors. While I prefer face-to-face (a generational thing), online meetings have seriously reduced my travel. As it has for a lot of people. Remember when analysts projected that air traffic would decrease because of online meetings? Yet, airline traffic is up. The planes I get on are packed.

One downside to living in Puerto Rico is that very few planes have Internet service while over the ocean, and almost all travel requires 2 to 4 hours over the ocean. I expect that to change in the next few years as more and more airlines adopt Starlink. Despite the silly Ryanair chairman comment, Starlink does not increase air travel cost over other competitors.

Next week I will be getting my next Therapeutic Plasma Exchange treatment here in Puerto Rico as we finally (!) open our clinic. It has been an interesting business adventure. And with that, I will hit the send button. You have a great week with friends and family and maybe think about your own personal healthcare as well as healthcare costs for the country. And don’t forget to follow me on X!

Your relatively optimistic on 2026 analyst,

John Mauldin

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Mauldin Economics

Read more commentaries by Mauldin Economics