Gold Advances to a New Record High as Questions Over Fed Independence Grow

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Bank of Japan’s recent policy shift is sending shockwaves through global markets.

Headlines this week highlight the dollar’s tumble against the yen and renewed chatter of an unwind to the massive yen carry trade, estimated at over $500 billion.

With Japanese borrowing costs rising and the yen gaining strength, leveraged bets are being reevaluated across asset class. Risk assets are wobbling. Bitcoin just topped $91,000, while gold is breaking out.

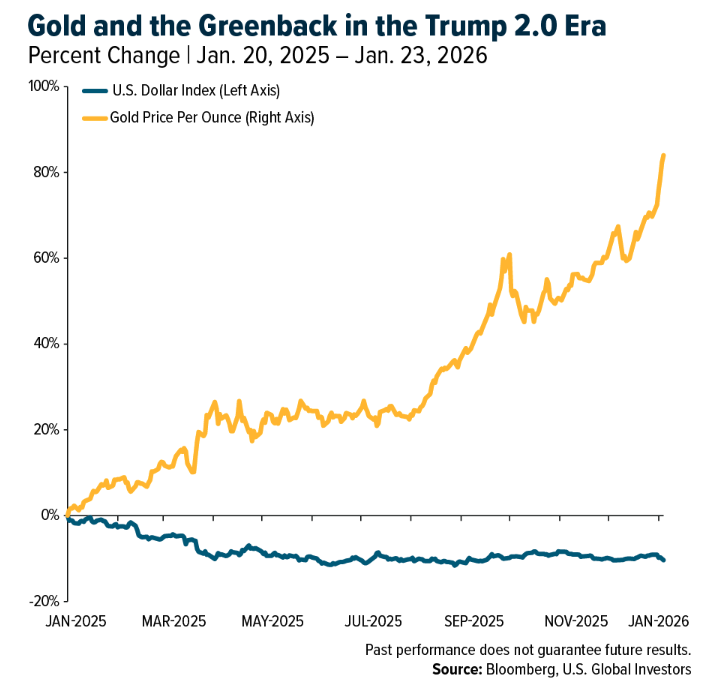

Indeed, the yellow metal is on a historic run. After hitting more than 50 new all-time highs last year, the yellow metal has surged to a new all-time high above $4,900 an ounce.

Meanwhile, silver, the “poor man’s gold,” is not so poor any longer, having smashed through $100 an ounce.

Many analysts are making some bold forecasts. Goldmans Sachs just raised its year-end gold price target to $5,400 an ounce, citing strong demand from both institutional and retail buyers. The London Bullion Market Association’s (LBMA) most recent survey reported bullish forecasts as high as $7,150.

If you recall, back in September, I projected that gold could hit $7,000 by the end of President Trump’s second term on the growing mountain of debt and a cornered Federal Reserve.

Is this the Perfect Storm?

The surge in gold prices is the result of multiple tailwinds converging all at once, including monetary, fiscal, geopolitical and even psychological.

For one, we have runaway government spending and ballooning national debt. The U.S. is on track to add trillions in new deficits over the next few years, and with debt levels approaching 125% of GDP, the government can’t afford significantly higher interest rates.

That puts the Fed in a bind. Raising rates would risk a fiscal crisis, while cutting rates would risk an even weaker dollar, which is down about 10% since the start of Trump 2.0.

And speaking of the dollar, there’s a growing crisis of confidence in fiat currencies and central banks, especially the Fed. More on that later.

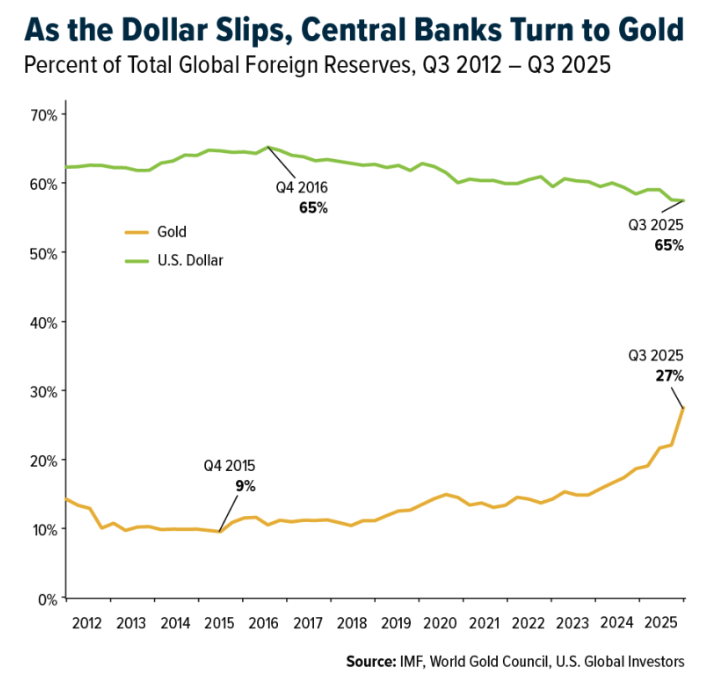

And finally, central banks around the world are buying gold at a historic pace. China, India, Turkey and others are stockpiling bullion, diversifying away from the dollar and U.S. Treasurys.

Fed Independence Under Fire

One of the most underappreciated forces driving gold’s meteoric rise right now is, I believe, the growing concern about the independence of the Fed.

President Trump has made no secret of his frustration with Fed Chair Jerome Powell. This year, that frustration has escalated into something more serious and potentially dangerous for the credibility of monetary policy.

In an unprecedented move, the Justice Department issued a criminal subpoena to the Fed, targeting Powell over alleged cost overruns in building renovations. The Fed chairman responded with a rare video statement, warning that the investigation could be a pretext to force rate cuts.

To my knowledge, this is the first time a sitting Fed Chair has essentially accused the White House of trying to strong-arm monetary policy.

This should raise some red flags. The whole point of an independent central bank is to ensure long-term economic stability, even when it’s politically inconvenient. When that independence is undermined, markets take note, as they are now.

Turkey’s Cautionary Tale

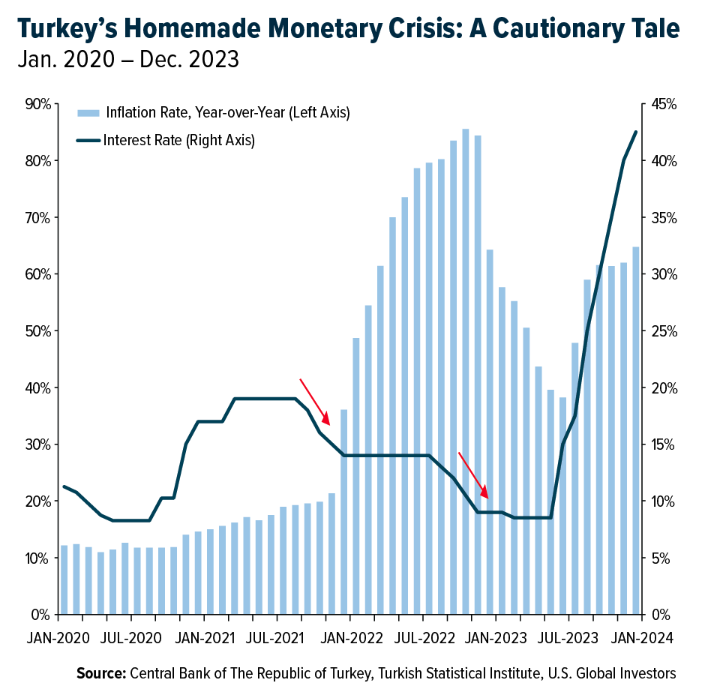

To understand where this road leads, look no further than Turkey.

Over the past decade, Turkish President Recep Erdogan has systemically undermined his country’s central bank, firing governors who refused to cut interest rates and replacing them with political loyalists. He embraced the unorthodox belief that higher, rather than lower, rates cause inflation, a theory that runs counter to centuries of economic history.

The result? Turkey’s inflation soared past 80%, the lira collapsed against the dollar and the economy teetered on the edge of catastrophe. Only after the damage was done did Erdogan finally reverse course, bringing in traditional leadership and allowing rates to be hiked (to exorbitant levels).

Like China and India, Turkey has a deep-seated affinity to gold, and many Turkish investors increased their purchases of the metal as a hedge against soaring prices. It all added up! Back in October, when gold surpassed $4,000, the country’s central bank estimated that households’ total gold holdings had increased to $500 billion.

A Crisis of Confidence in the Dollar

It’s not just Turkey, though, and it’s not just individual investors.

Central banks from China to Switzerland have been steadily increasing their gold reserves. At the same time, they’re scaling back exposure to U.S. Treasuries and reducing dollar holdings.

This global diversification away from the greenback is part of a broader “debasement trade,” a strategy rooted in the belief that the dollar, like other fiat currencies, is losing its long-term value.

Gold Stocks Still Have Room to Run

What if you want exposure to gold but don’t want the hassle of storing it? If you’ve been following my work, you know I’m a big believer in gold mining stocks as a leveraged play on rising gold prices.

These companies tend to move two to three times faster than the metal itself—both on the upside and downside.

But what’s different about this cycle is that many miners have cleaned up their balance sheets, reduced debt and focused on shareholder returns. That means they’re in a stronger position than in past gold bull markets.

Also worth watching are royalty and streaming companies, like Wheaton Precious Metals, Franco-Nevada and OR Royalties (formerly Osisko). These firms generate revenue based on production and price, without the same operational risks as traditional miners. OR, for example, just posted 100% earnings growth, and analysts are forecasting more upside ahead.

Stay the Course

If you’ve been investing in gold or gold stocks, congratulations! You’ve been on the right side of history.

If you’re still on the sidelines, I wouldn’t wait for $6,000 to start participating.

We’re living through a period of profound global monetary transition. The cracks are starting to show in the fiat currency system, and investors are waking up to the need for real assets in their portfolios.

As I said back in September, $7,000 gold is no fantasy. I believe it’s a logical destination in a world where confidence in central banks is eroding, debts are exploding and governments are increasingly reaching for control.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was LATAM Airlines, up 7.7%. According to Morgan Stanley, Lufthansa management continues to see robust demand trends, with International Air Transport Association (IATA) traffic tracking above gross domestic product (GDP) growth. At the same time, persistent supply constraints and industry consolidation have encouraged greater discipline, which has become a key driver of profitability. The firm has, however, been impacted by an older fleet and delays in seat certifications. Reassuringly, cost and booking trends now appear more encouraging heading into the first quarter of 2026, underpinning optimism for 2026.

- Container throughput at key ports in China recorded 8% year-over-year (YoY) growth last week. The number of international freight flights increased by 3% YoY last week, according to UBS.

- JPMorgan estimates that Ryanair’s unit costs excluding fuel (ex-fuel), adjusted for stage length, have increased by 13% versus pre-pandemic levels. This compares with Vueling at 10%, but remains well below the more than 25% increase seen at easyJet and Wizz, and the roughly 20% increase at the European flag carriers. JPMorgan estimates Ryanair’s relative cost gap versus the industry has widened from 48% in 2019 to 51% today.

Weaknesses

- The worst-performing airline stock for the week was United Airlines, down 5.1%, after reporting Q4 earnings per share. The Trump administration will halt the processing and issuance of immigrant visas for applicants from certain countries. Last Wednesday, a State Department spokesperson stated that the U.S. administration is stopping processing for immigrant visas for applicants from 75 countries, beginning on January 21, according to Morgan Stanley.

- Bank of America believes that Maersk fully resuming sailings through the Red Sea, along with the industry orderbook-to-fleet ratio rising to 34%, will put pressure on prices. The firm expects the Red Sea route to fully reopen in the second quarter of 2026, despite rising geopolitical tensions, adding market capacity and driving a decline in earnings.

- According to Raymond James, growing capital needs and associated debt service, along with rising construction material and labor costs, are driving cost per enplanement higher. While growth in labor and maintenance costs is expected to moderate following the sharp post-COVID step-up, airport costs continue to rise at above-inflation rates.

Opportunities

- Chinese airlines are entering a multi-year upcycle supported by recovering domestic ticket prices and lower oil prices. Bank of America expects Chinese domestic ticket prices to inflect higher in 2026, supported by constrained supply, stable demand, and so-called “anti-involution,” with easy year-over-year (YoY) comparisons.

- The sector is experiencing a structural shift as intra-Asia and emerging market trades become the primary engines of growth, supported by both rerouting driven by United States trade policies and organic expansion within the Association of Southeast Asian Nations (ASEAN). Chinese manufacturers are reorganizing production bases, which is boosting local economic growth in destinations such as Vietnam and Indonesia, according to JPMorgan.

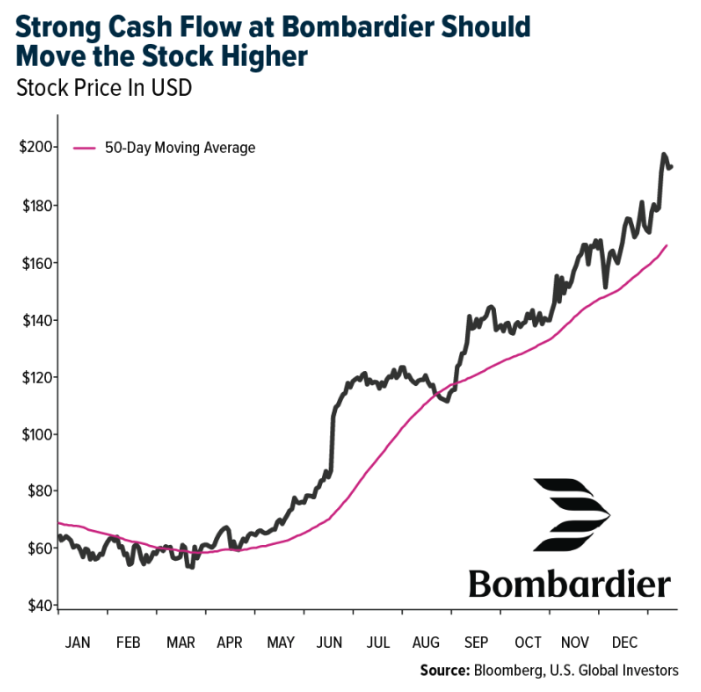

- BMO believes Bombardier will increase capital spending to support productivity initiatives, including the recently announced plant expansion, along with product upgrades and development activity, which should ramp modestly after two years of below-normal spending. That said, Bombardier remains on track to deliver approximately $900 million of free cash flow in 2026 and $1 billion in 2027.

Threats

- According to TD, American Airlines will see the most growth in Chicago at 35%. Southwest will grow in San Diego at 25%, Kansas City at 17%, and Los Angeles at 17%. Alaska Air has the most growth scheduled in San Diego at 33% and Portland at 13%. JetBlue is increasing capacity in Fort Lauderdale at 26% and Las Vegas at 39%.

- Container shipping has not yet passed the worst of the downturn, with oversupply and Red Sea reopening pressures likely to drive a slide into earnings before interest and taxes (EBIT) losses in 2026. Bank of America sees the first half of 2026 weighed down by heavy supply growth, while the second half of 2026 faces pressure from increasing prospects of a Red Sea reopening. The firm expects losses to prompt container liners to pull back shareholder returns in 2026 to preserve cash heading into the downcycle.

- CNBC reports that Spirit Airlines is in takeover talks with investment firm Castlelake. According to CNBC, Frontier did not secure any merger deal with Spirit. This news could pressure Frontier and JetBlue stocks today given their overlap with Spirit.

Luxury Goods and International Markets

Strengths

- Volkswagen delivered a much stronger-than-expected cash flow result for the year, generating roughly €6–7 billion compared with prior expectations of near break-even. The upside was driven by tighter working capital management, lower capital expenditures, and disciplined cost control, demonstrating improved financial flexibility and liquidity.

- Preliminary January Purchasing Managers’ Index (PMI) data for the euro area showed a mild divergence in momentum, with services slowing and manufacturing improving from weak levels. The flash Services PMI eased to 51.9, indicating softer growth, while the flash Manufacturing PMI rose to around 49.4, signaling factory activity is stabilizing after a prolonged downturn. The flash Composite PMI held near 51.5, suggesting modest expansion at the start of the year.

- Laopu Gold, a Chinese jewelry retailer, was the best-performing stock in the S&P Global Luxury Index over the past five days, gaining 20.5% on stronger earnings momentum and bullish analyst sentiment tied to gold demand.

Weaknesses

- JPMorgan recently cut its price target on Norwegian Cruise Line (NCLH) to $28 per share from $40 while maintaining an Overweight/Buy rating, reflecting roughly a 30% reduction in expectations. The downgrade follows heavier promotional activity across the cruise industry, which could pressure yields and near-term profitability. The analyst also removed NCLH from the firm’s Analyst Focus List, signaling more cautious sentiment.

- The latest official data show China’s consumer spending is weakening, with retail sales rising just 0.9% year-over-year in December 2025, down from 1.3% in November. Passenger vehicle retail sales fell more than 14% compared with a year earlier, highlighting cooling domestic demand amid broader economic pressures.

- Cettire Ltd., an Australia-based luxury e-commerce retailer, was the worst-performing stock in the S&P Global Luxury Index over the past five days, declining 20.2%. Shares fell on weaker sales trends, recent price target cuts, and ongoing concerns around soft demand and profitability in its core business.

Opportunities

- Burberry Group this week reported improving sales trends in its latest trading update. Comparable store sales grew about 3% year-over-year in the third quarter of fiscal 2026 (the 13 weeks ending December 27, 2025), a sequential improvement from earlier periods and a turnaround from declines a year ago. Retail revenue also rose, with particularly strong growth in Greater China and Asia-Pacific, driven by younger, Gen Z customers. Burberry described the performance as building momentum under its “Burberry Forward” strategy, even as conditions remain mixed across regions.

- Global tourism reached a new record in 2025, with 1.52 billion international arrivals worldwide, according to the United Nations World Tourism Organization. The agency expects this trend to continue into 2026, supported by a steady global economy. Strong travel demand has also bolstered consumer spending, particularly in discretionary categories tied to leisure and experiences.

- Hainan has become a major domestic hub for tourism and discretionary spending in China, supported by duty-free policies that encourage luxury purchases. Tourist arrivals grew 9.1% year-over-year to 106 million in 2025, with the province aiming for 115 million visitors in 2026. Inbound international tourism is also expected to rise, from about 1.5 million to 2 million visitors next year.

Threats

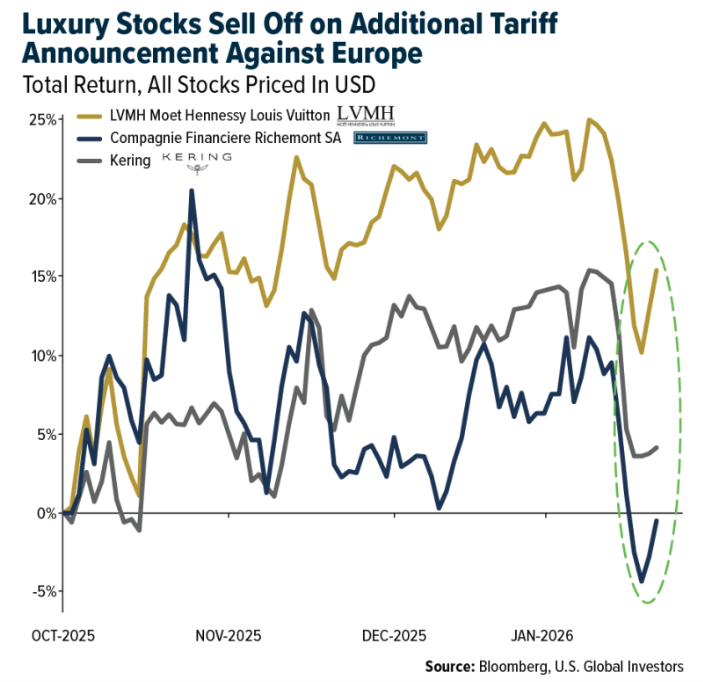

- Luxury stocks, including LVMH, Richemont, and Kering, sold off early in the week after Trump announced additional tariffs on eight European countries, raising concerns about trade tensions and potential pressure on European consumer and export names. Shares partially recovered later in the week after the announcement was reversed, underscoring the ongoing risk of market volatility from shifting U.S. trade policy and political uncertainty.

- Davos, the annual World Economic Forum gathering that brings together global political, business, and policy leaders, highlighted rising political fragmentation this year. Europe signaled greater independence from the United States and openly disagreed with Trump-era trade and security priorities, showing a shift away from automatic transatlantic alignment.

- London’s luxury car market is slumping as recent tax hikes on wealthy residents bite, with early data showing steep declines in high-end registrations; Ferrari sales reportedly down around 44%, Rolls-Royce down 26%, and Aston Martin off nearly 30% year-on-year, as affluent buyers hold back or relocate to avoid higher levies. The downturn reflects broader pressure on premium auto demand in the UK from fiscal policy targeting the rich.

Energy and Natural Resources

Strengths

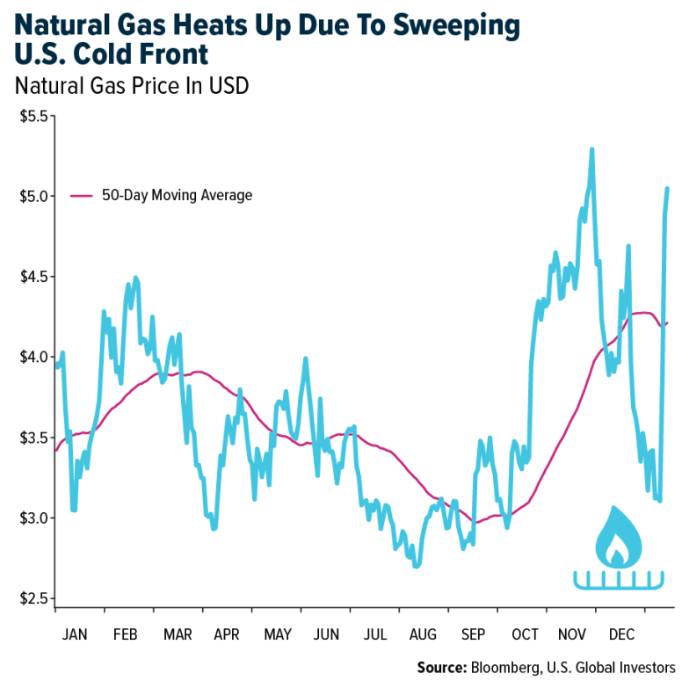

- Natural gas was the best-performing commodity this week, surging as much as 70%, as a sweeping U.S. winter storm drove a sharp spike in heating and power-generation demand across Texas, the Midwest, and the Northeast. Front-month futures jumped more than 70% at one point this week, while extreme cold sent spot prices in key regional markets to triple-digit levels, highlighting how quickly weather shocks can tighten the U.S. energy balance.

- Copper emerged as a key strength this week, breaking above $13,000 per ton as investor flows shifted from currencies and sovereign bonds into hard assets amid rising policy and geopolitical uncertainty. The move builds on an already tight fundamental backdrop, with mine disruptions, electrification-driven demand, and pre-tariff U.S. stockpiling reinforcing copper’s role as both a growth and macro hedge in the metals complex.

- Sigma Lithium stood out after decisively rebutting false negative media, confirming uninterrupted operations while selling an additional 100,000 tonnes of high-purity lithium fines at improved pricing tied to the SMM index. The update reinforces Sigma’s operational resilience and ESG-led cost advantage, with mining remobilization on track and its “Quintuple Zero” processing model generating cash through byproduct sales rather than adding operational risk.

Weaknesses

- Sugar was the weakest commodity this week, down around 1.5%. Shifting consumer preferences, particularly among Gen Z, are driving demand away from traditional sugar-sweetened products toward zero-sugar and lower-calorie alternatives, while beverage makers reformulate and market sugar-free options, creating excess supply and pressuring prices.

- Uranium supply chains remain a key risk, highlighted by over 1,000 tonnes of Nigerien yellowcake stranded at Niamey airport amid geopolitical tensions, border closures, and security challenges in the Sahel. Resource nationalism, legal disputes, and fragile transport routes could abruptly disrupt global supply as nuclear fuel demand rises.

- China’s decision to open nickel and lithium carbonate futures to global investors marks a step toward integrating its commodity markets with global capital and increasing its influence on price discovery. Expanding access to onshore futures positions Chinese exchanges to play a larger role in setting benchmark prices for critical battery and industrial metals, potentially challenging the dominance of U.S. markets.

Opportunities

- SLB raised its dividend and reported fourth-quarter earnings that beat expectations, driven by growing activity in the Middle East and expansion in its data-center segment. CEO Olivier Le Peuch expressed optimism for steady drilling growth across major regions, including OPEC nations. Adjusted earnings came in at 78 cents per share, above analysts’ 74-cent estimate, and the quarterly dividend increased 3.5 percent to 29.5 cents per share.

- Cyclic Materials’ $75 million raise highlights a strong opportunity in rare-earth recycling, providing a faster, lower-capital path to reducing dependence on China. By monetizing e-waste and co-producing metals like copper, recycling could supply a significant share of Western rare-earth demand within a decade.

- Electrification is emerging as a key climate opportunity in 2026, with EVs, heat pumps, batteries, smart grids, and software-driven technologies scaling rapidly and improving efficiency versus fuel-based systems. Regions that invest in transformers, cables, grid interconnections, and storage are best positioned to capture economic and geopolitical benefits.

Threats

- Cement consumption has stalled after decades of growth, with production down nearly 30% since 2020. China, which produces almost half of the world’s supply, is expected to see a sixth consecutive year of declining output in 2026. Prices are at ten-year lows, and capacity exceeds demand by more than double, though output remains nearly twice 2003 levels. Reduced cement use could help the environment, since the industry accounts for about 8% of global carbon emissions annually.

- Congo’s continued sale of copper from Chinese-backed projects through state miner Gecamines highlights a threat to Western supply-chain diversification. By deepening ties with Mercuria Energy Group and monetizing output from China-supported mines, the Democratic Republic of Congo strengthens Beijing’s control over copper and cobalt flows, limiting the impact of recent U.S. aid and offtake initiatives.

- Brazil’s grid-scale battery auction illustrates a growing challenge for Western energy players, as limited local manufacturing, financing, and deployment infrastructure leaves Chinese firms with integrated supply chains poised to dominate. Without faster development of domestic battery ecosystems and export-ready projects, the U.S. and Europe risk losing long-duration storage contracts and associated pricing power in key emerging markets.

Bitcoin and Digital Assets

Strengths

- Tokenization is moving from pilot projects to institutional-grade market infrastructure. Superstate’s $82.5 million capital raise, $1.2 billion already tokenized, and SEC-registered issuance model show blockchain can now support fundraising, share issuance, and settlement within existing regulations. This cuts settlement times from days to near-instant, lowers intermediary costs, and enables 24/7 capital markets—strengthening crypto’s long-term integration into global finance.

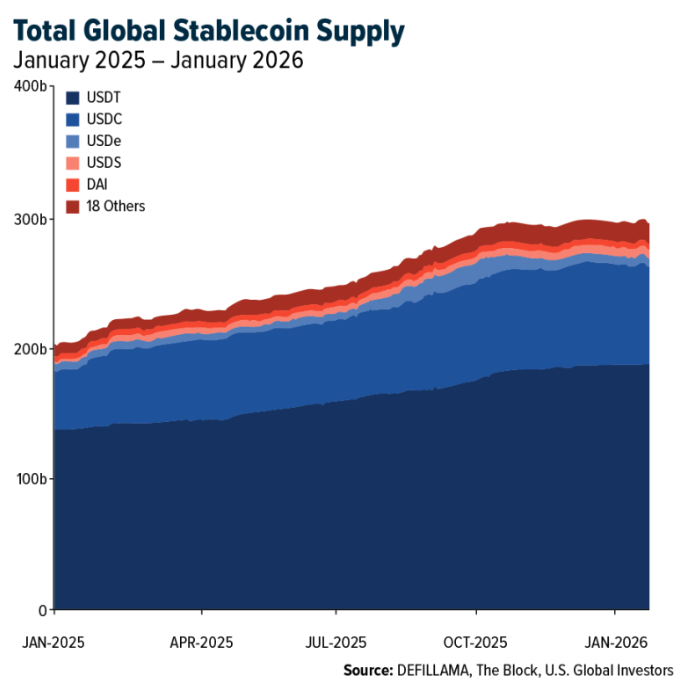

- Stablecoins have scaled beyond experimentation. Global supply exceeds $270 billion, more than double levels from two years ago, while USDC has grown approximately 80% year-over-year (YoY) for two consecutive years, according to Circle. Visa already processes around $4.5 billion in annualized stablecoin settlement, and both Visa and Mastercard are integrating stablecoins into payment rails. Circle’s CEO projects roughly 40% compound annual growth as banks move from pilots to live deployments, cementing stablecoins as a foundational layer of modern finance.

- Superstate is a regulated tokenization firm enabling SEC-registered assets, including Treasuries and equities, to be issued and settled directly on public blockchains. Its $82.5 million Series B, led by Bain Capital Crypto, brings total funding above $100 million and assets under management to $1.2 billion. The platform supports direct equity issuance and real-time settlement on Ethereum and Solana, cutting settlement from days to minutes and demonstrating scalability beyond tokenized Treasuries.

Weaknesses

- Bitcoin has fallen roughly 55% against gold since its December 2024 peak, while gold is up about 12% year-to-date (YTD) and trading near record highs. The BTC/gold ratio (18.46) is roughly 17% below its 200-week moving average, a level historically linked to prolonged underperformance. Similar breakdowns in past cycles lasted over a year, challenging Bitcoin’s role as a reliable store of value in risk-off environments.

- XRP has dropped about 19% from early-January highs, with investor sentiment in “extreme fear,” according to Santiment. Many small investors are stepping aside, and on-chain data mirrors early 2022, when prices fell for months. New buyers now hold XRP at higher prices than older holders, increasing the risk of further selling if prices don’t stabilize.

- Ethereum’s Fusaka upgrade was designed to boost data capacity and lower transaction costs by allowing more data (“blobs”) per block, mainly to support layer-2 networks. This temporarily increased transactions and active addresses but lowered fees, reducing ETH fee burn and weakening Ethereum’s revenue base. JPMorgan notes that past upgrades produced short-term activity spikes but failed to sustain growth, as value continues migrating to layer-2s like Base and Arbitrum.

Opportunities

- Sharon AI’s $500 million non-recourse on-chain loan, backed by tokenized GPU hardware, shows how blockchain can replace slow, restrictive bank financing with transparent, asset-backed credit. With $1.2 billion already deployed by USD.AI, this approach lowers capital barriers, improves collateral monitoring, and opens private credit markets to institutional investors seeking yield from AI compute.

- PwC notes that 2026 marks the shift from draft rules to live regulatory regimes across key hubs (EU MiCA, U.S., U.K. FSMA, UAE, Switzerland), accelerating institutional adoption. Stablecoins now exceed $270 billion in circulation, and regulated frameworks enabling banking access, tokenization, and cross-border products. Firms building compliant infrastructure early can capture outsized institutional flows despite higher compliance costs.

- Bermuda is emerging as a test case for on-chain public finance. Building on its 2018 Digital Asset Business Act, the country pilots stablecoin payments and tokenization with Coinbase and Circle, using USDC, which has over $30 billion in circulation globally. The initiative demonstrates live government and financial use cases, offering a scalable blueprint for modernizing payments, cutting settlement costs, and attracting digital-asset capital.

Threats

- Operational and custody risks at the sovereign level are becoming a systemic threat to crypto enforcement. South Korean prosecutors lost a “significant” amount of seized bitcoin, likely due to a mid-2025 phishing attack, exposing weak key management. Past seizure attempts of up to 24,613 BTC (~$127 million in 2024) highlight the scale of assets at risk, which could undermine trust and complicate regulation.

- Macroeconomic uncertainty is driving short-term institutional risk aversion in crypto markets. U.S. spot bitcoin ETFs saw $708.7 million in net outflows in a single day, while ether ETFs lost $286.9 million, as investors reduced exposure amid geopolitical tensions, interest rate uncertainty, and bond market volatility. Although spot crypto ETFs still hold over $116 billion, repeated macro-driven outflows could increase price swings and weigh on market confidence.

- Even with Federal Housing Finance Agency guidance, crypto adoption in U.S. mortgages remains limited. Homeownership is ~65%, and first-time buyers’ average age rose from ~39 in 2010 to ~59 in 2025. Lenders apply 30–50% haircuts to volatile assets like bitcoin, keeping most crypto-backed loans in jumbo or private-label markets. With BTC drawdowns historically exceeding 50%, timing and settlement risks keep crypto mortgages niche without clearer rules.

Defense and Cybersecurity

Strengths

- Nvidia becoming Taiwan Semiconductor Manufacturing Company’s largest customer, alongside Micron expanding capacity in the United States, Taiwan, and India, highlights how AI-driven demand is no longer cyclical but structural. Capital commitments are long-dated, politically supported, and increasingly geographically diversified, reducing single-country risk while locking in multi-year revenue visibility for key suppliers.

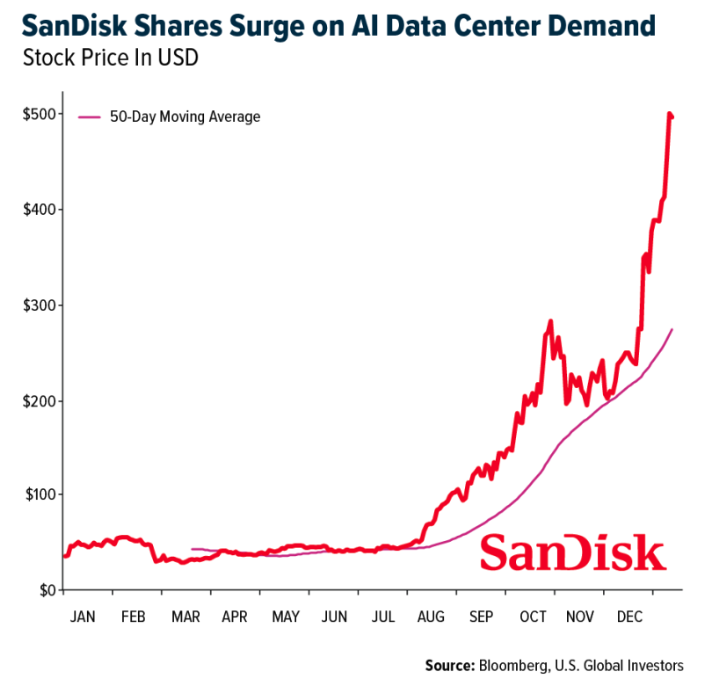

- SanDisk shares are surging as strong AI data center demand fuels a highly bullish memory market, pushing prices sharply higher and straining global supply. As a key beneficiary of rising NAND pricing and tight capacity, investors are re-rating SanDisk on improved margin and cash flow expectations.

- The best performing stock in XAR ETF this week was Redwire, up ~14%. Redwire Corporation is showing notable strength after renewed momentum around the “Golden Dome” defense initiative positioned the company as a potential supplier of critical space- and ground-based technologies. Investor enthusiasm reflects Redwire’s aligned portfolio—from orbital drones and sensors to digital engineering platforms—placing it well to benefit from accelerated defense procurement tied to the program.

Weaknesses

- The U.S. government halted work on AeroVironment’s BADGER phased-array antenna systems under the U.S. Space Force’s SCAR program, a major satellite communications initiative. The contract, awarded in 2022 and valued at approximately $1.4 billion, was effectively canceled, ending AeroVironment’s involvement and eliminating a significant expected revenue stream.

- A critical zero-day vulnerability was discovered in Cloudflare’s Web Application Firewall that allowed attackers to bypass security controls via the ACME path used for automated SSL/TLS certificate issuance. Cloudflare identified the issue through internal audits and external reports and quickly patched the flaw to prevent unauthorized access to protected origin servers.

- The worst-performing stock in the XAR ETF this week was AeroVironment, down about 19%. The decline follows a U.S. government stop-work order on its SCAR program, creating near-term uncertainty around revenue and contracts. Canaccord Genuity says the roughly 25% drop may be overdone, noting the pause is procedural, potential FY26 impact is manageable, and investors may refocus on longer-term upside from accelerated Golden Dome procurement.

Opportunities

- The U.S. Justice Department is reportedly considering easing certain firearm regulations, which could increase firearm sales and alter market dynamics, potentially creating a more supportive demand environment for Ruger’s competitors.

- Palantir has partnered with Sovereign AI and Accenture to develop and scale AI data centers across Europe, the Middle East, and Africa, using Chain Reaction software and collaborating with Dell and Nvidia.

- Micron’s $100 billion U.S. fabrication facility, Taiwan acquisition, and India production ramp demonstrate how industrial policy is translating into real assets and long-term demand visibility. Companies aligned with these initiatives benefit from subsidies, political backing, and supply chain security premiums.

Threats

- Massive AI capex places pressure on energy, cooling, and data-center infrastructure, increasing execution risk and cost inflation. Delays or bottlenecks in power availability could slow deployment timelines and cap near-term returns.

- Iran’s near-total internet and communications shutdown reflect not just internal repression, but rising risk of cyber escalation and regional destabilization. Such blackouts highlight how quickly digital infrastructure can be weaponized, increasing uncertainty for energy markets, regional connectivity, and any companies exposed to Middle East data, telecom, or logistics flows.

- Russia’s renewed large-scale attacks on Ukrainian energy infrastructure left millions without electricity and heat for weeks as temperatures fell to around –4°F. Sustained missile strikes combined with severe winter conditions highlight the growing use of infrastructure warfare, increasing humanitarian risk and reinforcing long-term geopolitical, energy, and security instability across Europe.

Gold Market

This week gold futures closed the week at $4,979.90, up $384.50 per ounce, or 8.37%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 10.32%. The S&P/TSX Venture Index came up 5.51%. The U.S. Trade-Weighted Dollar fell 1.88%.

Strengths

- The best-performing precious metal for the week was platinum, up 19.10%. Platinum is emerging as a clear strength, supported by rising online investment and growing demand for physically backed products as investors seek diversification beyond gold amid persistent macro uncertainty. Tight supply, dwindling above-ground stocks, and platinum’s dual role as both a precious and industrial metal reinforce its appeal as a scarce, under-owned asset in the 2026 metals complex.

- Hochschild Mining forecasted gold production for 2026 at 300,000 to 328,000 gold equivalent ounces, above the consensus estimate of 232,446 ounces. They project all-in sustaining costs per ounce of $2,157 to $2,320, according to Bloomberg.

- Pan American Silver reported preliminary fourth-quarter 2025 production of 7.28 million ounces of silver and 197.8 thousand ounces of gold, exceeding CIBC’s estimates of 6.82 million ounces of silver and 196.5 thousand ounces of gold. The difference was mainly driven by stronger-than-expected performance at Juanicipio, which contributed 2.5 million ounces of lower-cost silver. The price of silver also continued its rise this week, surpassing $100 for the first time, according to Bloomberg.

Weaknesses

- The worst-performing precious metal for the week was gold, though it was still up 8.37%. Gold continues to show relative strength versus Bitcoin, rallying alongside silver and equities as capital flows toward proven safe havens, while Bitcoin remains range-bound near $90,000. This divergence reinforces gold’s role as the preferred hedge during macro uncertainty, with liquidity, history, and physical scarcity rewarded over “digital gold” narratives.

- South Africa’s gold production fell sharply by 6.0% year-over-year in November, a significant drop from October’s revised 0.3% decline. Structural challenges—including operational disruptions, power constraints, and declining ore grades—continue to weigh on the country’s aging gold sector, according to Statistics South Africa. Broader mining output also disappointed, falling 2.7% year-over-year versus expectations of a 5.0% increase, down from a revised 6.1% gain in October, highlighting downside risks to supply and reinforcing tighter precious metals fundamentals, per Bloomberg.

- Pantoro Gold reported quarterly production of 22,000 ounces, below Canaccord’s 26,000-ounce consensus estimate. All-in sustaining costs were elevated at A$2,571 per ounce versus expectations of A$2,306, reflecting near-term operational and cost pressures. The miss led to a sell-off in Pantoro shares as investors repriced execution risk and margin concerns, even as the broader gold price backdrop remains supportive for producers with steadier delivery and cost control.

Opportunities

- Goldman Sachs raised its year-end gold price forecast by more than 10%, citing growing private-sector demand alongside strong central bank and ETF buying. The bank now targets $5,400 an ounce for December 2026, up from $4,900, assuming private investors continue holding gold as a hedge against macro policy risks, according to analysts Daan Struyven and Lina Thomas.

- Gold ETFs saw $5.5 billion in inflows over the past week, largely from North American investors, while European investors continued to reduce silver ETF holdings. Exchange-for-Futures (EFP) differentials remain negative for silver and platinum, reflecting strong demand from non-U.S. markets, according to BMO.

- BMO notes that the Centerra preliminary economic assessment (PEA) outlines a hybrid open-pit and underground operation with a 15-year life of mine starting in 2031. With initial capital of $771 million, the after-tax net present value is $1.1 billion with a 16% internal rate of return, using long-term gold and copper prices of $3,000 per ounce and $4.50 per pound. At current spot prices, the NPV rises to $2.8 billion with a 29% IRR.

Threats

- RBC sees rising risks from higher costs and capital spending, as the current gold price environment expands the pipeline of economically viable projects and intensifies competition for mining services. Companies with exposure to an owner-operator model are expected to be relatively more insulated.

- China’s solar manufacturers, which have struggled with a prolonged glut and price war, now face a new headwind. Silver, used in paste form for electrical contacts in solar panels, has more than tripled in value over the past year, including a 30% surge this month, according to Bloomberg.

- Ghana’s mining industry warned that a government proposal to raise the royalty on gold producers could deter investment. The Ghana Minerals Commission disclosed plans to review the fiscal regime, including a change from the current 3% to 5% fixed royalty to a sliding royalty of 5% to 12%, pegged to bullion prices, as the nation seeks a larger share of revenues from gold’s record-breaking rally, according to Bloomberg.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2025):

Deutsche Lufthansa

Ryanair

easyJet

AP Moeller – Maersk

Bombardier

American Airlines

Southwest Airlines

Alaska Air Group

JetBlue

Frontier Group Holdings, Inc.

The Goldman Sachs Group Inc.

Wheaton Precious Metals Corp.

Franco-Nevada Corp.

OR Royalties Inc.

Palantir

Micron Technology

Volkswagen AG

Laopu Gold

LVMH

Cie Financiere Richemont

Kering SA

Ferrari NV

Pan American Silver

Pantoro Gold

Centerra Gold

SLB

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The surge in gold prices is the result of multiple tailwinds converging all at once, including monetary, fiscal, geopolitical and even psychological.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Read additional important information. +

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All