A combined exposure to gold mining stocks and physical gold appears attractive

The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy or position of an employer or its affiliates.

As geopolitical tensions reshape global trade, capital flows and investor risk appetite, gold is once again surfacing as an important component of asset allocation. Some investors and central banks are arguably viewing gold as a risk hedge, supplanting US Treasuries as a safe-haven asset. Gold is no longer just a hedge against inflation, it is also about diversification.

In addition to the exodus from USD-denominated assets flagged by some commentators, private wealth is slowly relocating beyond “Safe Haven Europe” in response to concerns like regulatory overreach, tax policy, as well as political, cultural and economic uncertainty. Hence, it is not surprising that with some private capital moving elsewhere, the very question of the reference currency for trade and investments arises. Novel investment ideas surface, new payment ecosystems form, and new methods of exchange beyond the “London fixing”.

Gold remains a solid hedge against uncertainty and physical gold has the benefit of not really carrying with it any sizable counterparty risk, unlike other asset classes. In periods of conflict, gold is also a useful tool for central banks to stabilise their currency and navigate a world of tariffs and sanctions.

“All of the factors that helped to drive the record-breaking run for the gold price in 2025 […] look likely to continue this year,” said John Reade, senior market strategist at the World Gold Council, the trade association representing gold mining companies.

While demand from the jewellery industry might continue to stay muted in 2026 in terms of volume, and industrial applications where copper and silver are more widely used are unlikely to grow rapidly above historical trend1, there are good tailwinds for use cases like investing and central bank purchasing in periods of geopolitical and economic uncertainty. Furthermore, investors remain underallocated to gold compared to their average positioning over the past couple decades.

A touch of bullishness on the industrial side: experts we spoke to at industry conferences are seeing signs of increased use of gold due to its unique properties in fields like quantum computing, space/satellite and even medical procedures. Gold is a great conductor, it does not tarnish and is even highly biocompatible.

Meanwhile, some investors are also looking beyond bullion to the equity side of the value chain for additional return potential. Gold mining equities have risen by more than 150% over the past 12 months2. Gold mining companies are often considered a “leveraged play” on rising gold prices, benefiting from stable all-in sustaining costs (AISC) regardless of supply and demand.

Sustaining Margin = (Gold Price – All-In Sustaining Costs) x Production Volume

This “operating leverage” can result in profit margin expansion when gold prices rise. These elevated profit margins also translate into improved financial health, allowing miners to pay down debt, strengthen their balance sheets, or initiate or increase dividend payments to shareholders.

Often a lag effect can be observed between the price of gold and gold miners’ performance due to capex delays, operational leverage parameters, and cost management. Capex deployment in mining still takes years post-exploration and production costs can fluctuate over time and impact company profitability.

Industry practitioners we have spoken to also consider additional inputs when analysing the theme such as: lower grade mining deposits which might become viable with higher prices, gold recycling momentum as well as new specialised mire exploration projects.3

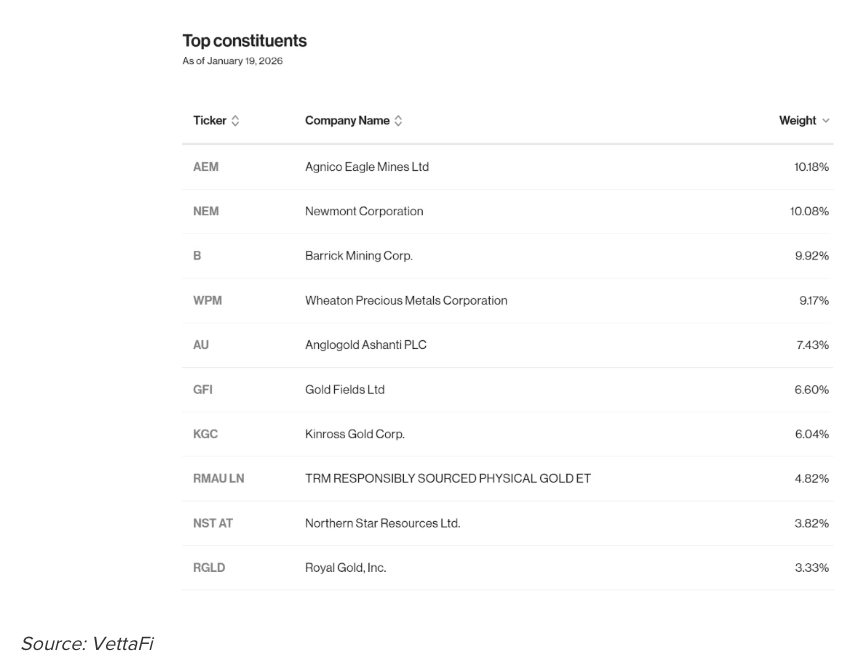

A combined exposure to gold mining stocks and physical gold thus appears attractive and represents a go-to allocation to gold providing diversification and potentially smoother returns over time. This approach is adopted by the VettaFi Gold Miners Screened Index tracked by the HANetf Gold Miners Screened UCITS ETF (ESGO).

The strategy tracks the performance of the largest 30 gold mining and royalty companies including a position in The Royal Mint Responsibly Sourced Physical Gold ETC. The index rulebook has been designed to ensure high weighted revenue purity to the theme through the combination of a clearly defined sub-sector and market cap weighting. The latter reduces the allocation to potential pre-revenue companies expected to generate less than 50% of revenue from gold.

Given the importance of running smooth operations and avoiding risk and health and safety events across the mining industry in general, and to ensure alignment with European SFDR Article 8 parameters, the index incorporates ESG screens which provide a solid complement to the Gold ETC holding backed by physical gold sustainably sourced by the Royal Mint. 50% of the equity constituents of the index are Canadian, with the remainder primarily spreads across South Africa and the US (at 15% each), and Australia.

The industry is seeing encouraging progress in terms of respect for widely accepted ESG norms and good governance principles. In the past month we have spoken to at least one central bank of an emerging nation exporting gold and have witnessed the roll out of clearer processes to grant mining, aggregator and offtaker licenses.

However, mining metal does generally represent a strain on local ecosystems (gold mining included). We are hopeful to see miners increasingly leverage the benefits of data integration and operational AI deployment to optimise their operations, their productivity while reducing this environmental strain: progress can be delivered with novel techniques at all stages from smarter deposit finding with sub-surface map analysis, to enhanced ore separation leveraging AI and machine vision and general disaster or contamination risk management through better leveraging sensor data.

As central bank purchasing is likely to remain strong, investors who might be concerned by the impact of lower rates and geopolitics on the USD are also aware that an estimated 70%-80% of known global gold reserves have already been extracted, while gold production has remained relatively stable.

1 Our expectations

2 VettaFi indices

3 VettaFi

Originally published on ETF Stream.

Originally published on ETF Trends

For more news, information, and analysis, visit VettaFi | ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi