Markets stand at the intersection of opportunity and divergence in 2026

In our 2026 Outlook, we examine three themes that we believe will shape the economy in the coming year and impact the U.S. and global markets.

Theme 1: Everyday Impacts of an Uneven Recovery

The U.S. economy continues demonstrating impressive strength on the surface, yet beneath these robust headlines lies a notable divergence. The K-shaped recovery has created distinct realities: households and regions with stronger balance sheets are holding up well, while those with tighter budgets face strain from persistent costs.

Theme 2: AI From Hype to Real-World Results

Companies are investing heavily in AI to boost productivity, improve customer experiences, and reduce costs. The benefits will take time and will not be equal. We expect more differentiation in 2026 as focus shifts from pure infrastructure toward AI platform stocks and productivity beneficiaries across sectors.

Theme 3: Adding Private Income and Diversification

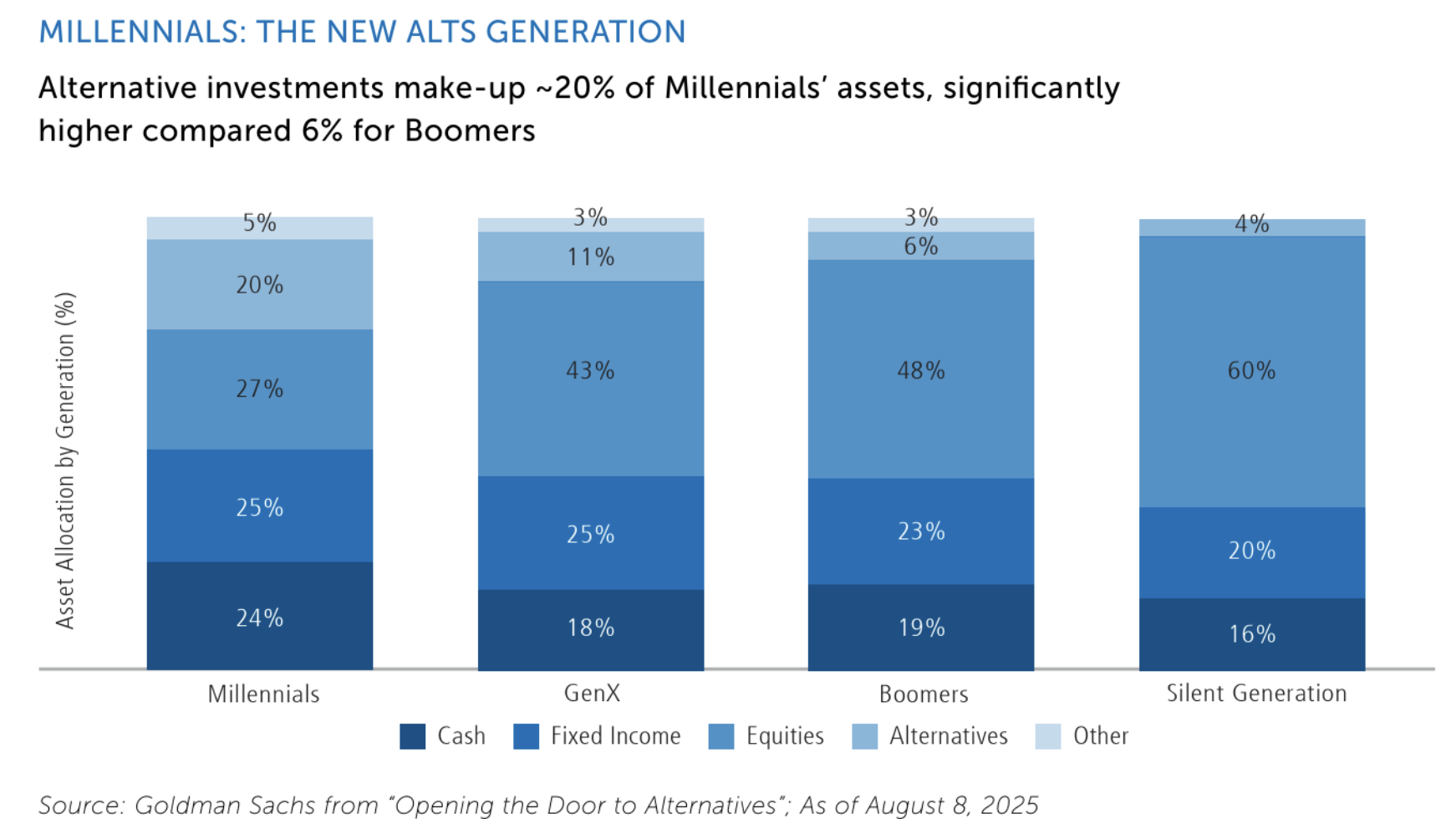

More investors are looking beyond traditional public stocks and bonds toward private credit, infrastructure, real estate, and secondary funds. With elevated public market valuations, periods like this have historically represented attractive entry points to private markets.

Theme 1: Everyday Impacts of an Uneven Recovery

The U.S. economy continues to demonstrate impressive strength on the surface—Q4 GDP is tracking at potentially 4-5% growth. But beneath these robust headlines lies a notable divergence in economic experiences. The K-shaped recovery has created two distinct realities: households and regions with stronger incomes, savings, and home equity are holding up well, while those with tighter budgets feel more strain from everyday costs.

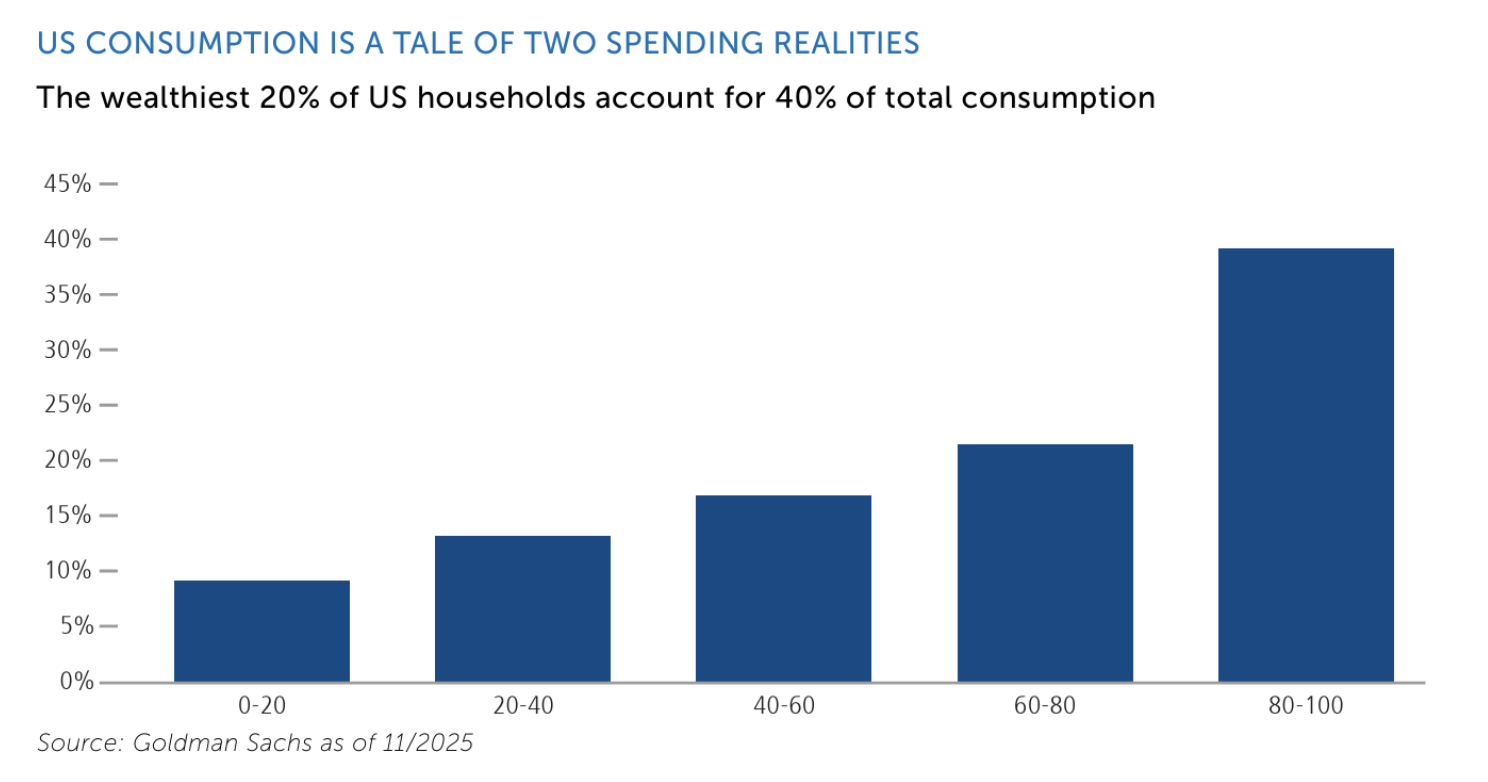

The wealthiest 20% of households account for 40% of total consumption, and their strong balance sheets should continue supporting spending. Meanwhile, we are seeing concerning signs of stress among lower-income households, with auto and credit card delinquencies increasing, particularly among subprime consumers.

Wage growth continued to outpace inflation and household wealth reached record levels, supporting consumer spending, particularly among more wealthy households.

Although the overall economy remains resilient, we are seeing important shifts in consumer behavior. Credit card defaults hit 4.23% in late 2024 – the highest rate in 13 years – signaling financial strain among lower-income households. This contrasts sharply with higher-income consumers, who continue to drive much of America’s economic growth through strong spending. Their ability to maintain this spending will be crucial for the economy in 2026.

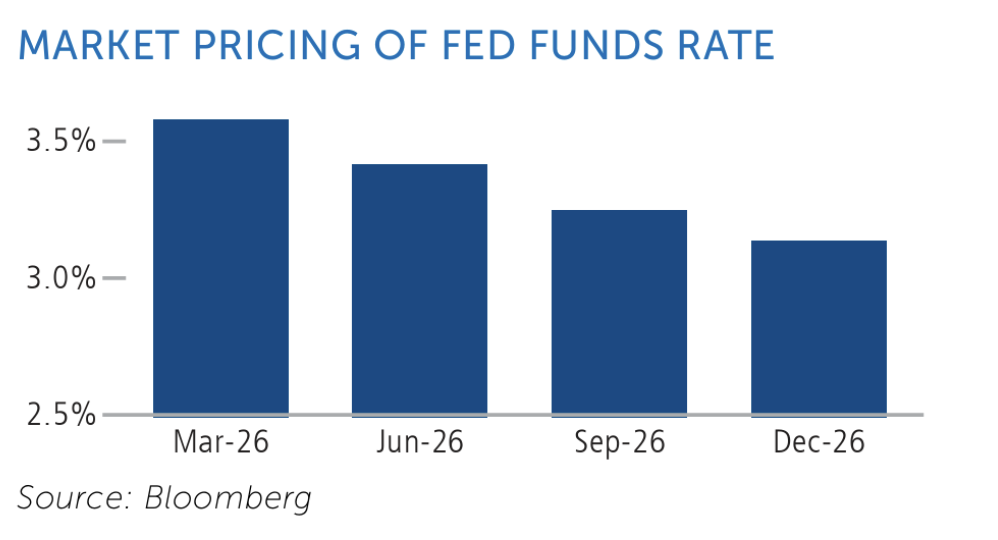

Recent CPI data showed headline inflation at 2.7% and core inflation at 2.6%—above the Fed 2% target, but only modestly so. The consensus has baked in 2-3 more Fed rate cuts this year, though there is an unusual level of dissent on the FOMC and we expect continued pressure from the White House as we head toward the midterms.

Labor Market Spotlight The labor market will be absolutely key to the Fed decisions this year. We have moved into what we call a “slow hire, slow fire” environment—companies are not laying off workers en masse, but they are also not adding headcount. Unemployment has crept up to 4.4%, particularly pronounced among younger workers aged 16-25.

Tax Refund Boost There is about $150 billion of incremental aid awaiting consumers in early 2026 via tax refund season, thanks to the OBBB legislation—representing a 44% increase over typical refund levels. “Affordability” appears to be the key word in the march toward the midterms

Theme 2: AI From Hype to Real-World Results

We are coming off three exceptional years for stocks. Despite being down 15% at its lowest point, the S&P 500 rebounded to finish 2025 with about an 18% gain. Such a dramatic recovery has only happened three times in the past 80 years.

The market concentration is undeniable. The top 10 U.S. companies represent 40% of the S&P 500 market cap. The top five tech companies alone have a collective value of $17.6 trillion—exceeding the combined GDP of Japan, India, the UK, France, and Italy. But here is the key: earnings growth among big tech has delivered. Overall profit margins remain at 12.8%, above historical averages, with the IT sector running at a 28.5% profit margin.

Here is what we think changes in 2026: we will see more differentiation. The market has shifted from a “rising tide lifts all ships” view to a more nuanced perspective on who is relatively better positioned. Early AI enthusiasm was concentrated on a narrow group—we expect this to broaden in 2026. This is a transition year where focus shifts from pure infrastructure toward AI platform stocks and productivity beneficiaries.

Which sectors should we be watching? Semiconductors remain the clearest winners. But after two decades of flat demand, utilities are now in a massive capex cycle. Natural gas is expected to provide nearly 40% of data center power in 2026. Energy is another sector we are watching closely.

AI Infrastructure Investment About 60% of hyperscalers operating cash flow is now dedicated to capex, and 27% of S&P 500 capex comes from just five companies. Most AI infrastructure spend has been funded from cash, but companies are increasingly turning to debt markets.

Theme 3: Adding Private Income and Diversification

More investors are looking beyond traditional public stocks and bonds toward private credit, infrastructure, real estate, and secondary funds. These markets can offer different sources of return and income, but they come with trade-offs like limited liquidity, longer holding periods, and manager selection risk. This is a great time to look at private markets, particularly given elevated equity valuations.

Valuations in public markets remain at lofty levels. Persistent inflation could keep interest rates higher for longer. High valuations and an elevated rate environment could create challenges for investors relying solely on traditional 60/40 allocations. Periods of high public equity valuations have historically represented attractive entry points to private markets.

We want to address concerns around credit events directly. We view these as isolated occurrences, not indicators of broader systemic risks. In fact, several of these events were in the public market, not private. Concerns around private credit have been somewhat overdone. We are seeing signs of a recovery in dealmaking, and we expect this to continue, which should fare well for both private equity and private credit.

2026 PORTFOLIO RECOMMENDATIONS WHY THIS MATTERS FOR YOU

-

Fed Policy and Market Expectations With market expectations for interest rate cuts varying widely, a disciplined investment approach becomes crucial. We recommend building a portfolio that can perform well across different rate scenarios. Consider combining growth investments with defensive positions, and look at sectors that historically perform well during rate transition periods.

-

Uneven Economic Recovery The K-shaped recovery means quality and liquidity matter more than ever. Consider strategies focused on high-quality balance sheets and companies with pricing power. We favor premium and value segments that are better positioned than the middle market.

-

AI Differentiation We expect more differentiation in 2026 as the market shifts focus from infrastructure to practical applications. Look for companies that can translate AI investments into tangible productivity gains while maintaining a balanced approach that does not overconcentrate in mega-cap technology.

-

Private Market Opportunities With elevated public equity valuations, this presents an opportune time to evaluate private market allocations. Our best thinking is to incorporate 10-30% in private alternatives for suitable clients, with careful attention to manager selection, liquidity planning, and diversification.

Our Investment Positioning – Core Investment Strategy

- Strong emphasis on U.S. stocks, particularly companies with proven track records

- Focus on industry leaders that can maintain strong profits even when costs rise

- Strategic bond investments to take advantage of potential rate environment

- Select private market opportunities in innovative, fast-growing areas

- Careful balance across different types of investments to protect and grow your wealth

Our Investment Positioning – Which Industries We Favor

- Technology and energy companies

- Semiconductors, utilities, and data center-related infrastructure

- Small and mid-cap equities positioned to benefit from AI adoption

- Companies with strong balance sheets and pricing power in an uneven recovery

- The U.S. market leads in high-growth tech sectors, driving stronger earnings potential.

Why This Matters for You

This balanced approach aims to capture growth opportunities while protecting your wealth in an evolving market. We are focusing on American companies with proven strength, while staying flexible enough to adjust as conditions change.

The economy remains robust overall, though labor market data will be key to watch. We think it is possible the Fed could cut rates up to three times this year. We are coming off three exceptional years for equities—mid to high single-digit returns would be viewed positively this year.

Core fixed income may not return another 7% this year, but we still find value here—it provides ballast for portfolios. We expect bonds to outperform cash, and we like active management in fixed income.

We have maintained international exposure, which delivered over 25% returns year-to-date in 2025. The value of global diversification remains clear.

Our investment philosophy has always emphasized quality over speculation, diversification over concentration, and long-term fundamentals over short-term noise.

Private Alternative investments may not be suitable for all investors, and the risks of alternative investments vary based on the underlying strategies used. Private investment funds generally involve various risk factors, including, but not limited to, potential for complete loss of principal, liquidity constraints and lack of transparency. Unlike liquid investments, private investment funds do not provide daily liquidity or pricing. Each prospective client investor will be required to complete a Subscription Agreement, pursuant to which the client shall establish that he/she is qualified for the investment in the fund and acknowledges and accepts the various risk factors that are associated with such an investment.

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Calamos Wealth Management, LLC [“Calamos”]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Calamos.

Please remember that if you are a Calamos client, it remains your responsibility to advise Calamos, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by Calamos Wealth Management