Coming into 2026, investors face a landscape shaped by persistent inflation, evolving US monetary policy and global uncertainty. At Parametric, our systematic and customized approach is designed to help clients navigate these complexities while preserving after-tax returns.

The world economy has entered the new year at a crossroads, with growth expected to moderate and inflation gradually cooling across most regions. The International Monetary Fund (IMF), the World Bank and leading private forecasters project global GDP growth ranging from 2.6% to 3.2%—below pre-pandemic averages—as trade tensions, policy uncertainty and structural shifts weigh on momentum in 2026.

Let’s take a moment to focus on the trends shaping the investing environment.

Key global themes shaping 2026

AI Investment and Productivity. The US continues to lead in AI-driven capital spending, supporting growth and productivity. While AI adoption has been slower outside the US, its transformative potential is beginning to reshape labor markets and business models globally.

Trade and Tariffs. The new global trade order is defined less by tariff levels and more by their spillover effects. US tariffs are expected to dampen imports, limiting the transmission of US domestic strength to the rest of the world. China’s economy has become more export focused, and the basket of goods has shifted toward higher value-added products, intensifying competition for manufacturers in Asia and Europe.

Divergent Regional Growth. The US is projected to grow around 1.5% to 2.0%, supported by resilient consumption and continued AI investment. China’s growth has moderated to 4.0% to 4.6% as property sector challenges persist. Europe faces modest growth, with Germany rebounding on fiscal stimulus, while the UK and France contend with fiscal constraints. India continues its structural ascent, after surpassing Japan as the world’s fourth-largest economy in 2025.

Risks and Uncertainties. Major risks include a potential AI bubble, renewed inflation from supply bottlenecks, policy missteps and geopolitical tensions. Fiscal and monetary policy should remain in focus, with central banks cautious about rate cuts and governments balancing the need for stimulus with debt sustainability.

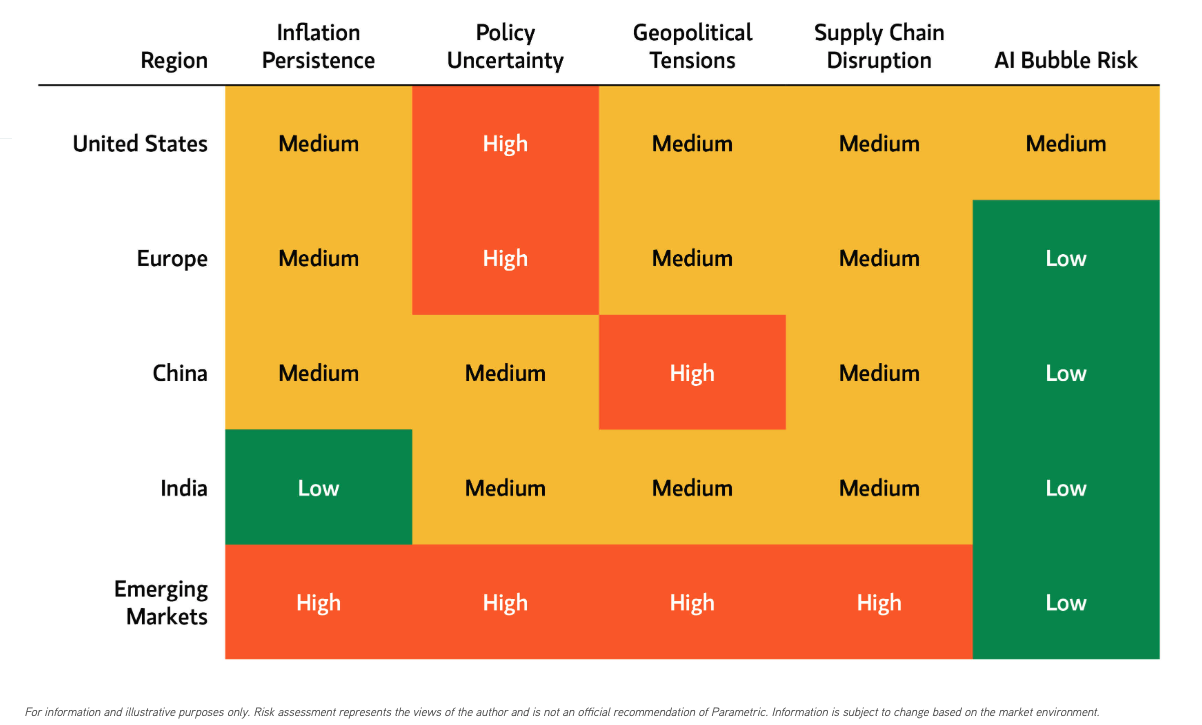

Major risks that may capture an investor’s attention can be bucketed into a few broad categories that I’ve defined. Here’s a visual summary of what I perceive to be the intensity of these risks by region, based on a qualitative assessment of recent headlines.

Current Economic Risk Map

As investors consider these risks, we think it’s important to recognize how market dynamics are shifting. Earnings growth has broadened beyond technology. In the third quarter of 2025, S&P 500® Index earnings rose 14%, with most of the acceleration coming from sectors outside tech. More industries are now showing positive growth—highlighting that opportunity and volatility extend across the market, not just in mega-cap tech stocks. In our view, diversification* remains key as sector leadership evolves over the coming year.

Focusing on the US investment environment, let’s look more closely at some major themes:

Stubborn challenge of US inflation

Despite progress since the post-pandemic peak, US inflation remains above the Federal Reserve’s 2% target, with Headline CPI for December 2025 coming in at 2.7% year over year. Structural factors—including tariffs, energy bottlenecks, housing constraints and labor shortages driven by reverse immigration and an aging population—continue to exert upward pressure on prices. These forces suggest inflation is unlikely to normalize in the near term and may possibly rise, even as headline measures decelerate modestly.

As noted in our outlook for commodities, investors tend to increase allocations to “safe-haven assets” like gold when market uncertainties like inflation persist.

New era of US monetary policy uncertainty

The Fed enters 2026 at an inflection point: Chair Powell’s term is set to expire in May, and the administration has indicated that his successor could be appointed early in the first quarter. Markets are bracing for potential shifts in the Fed’s tone and independence. Depending on how Powell’s replacement is perceived, we may see the yield curve steepen as term premiums rise. In that scenario, mortgage rates could remain elevated, adding to the headwinds faced by the US housing market.

As highlighted in our outlook for fixed income, active management may become a strategic differentiator in an environment defined by policy uncertainty and shifting interest rate dynamics.

Election-year dynamics of US fiscal policy

Ahead of the November midterm elections, the current administration may offer a flurry of fiscal initiatives—ranging from tax adjustments to targeted spending programs—aimed at shoring up voter confidence. While such measures may provide short-term stimulus, they also risk widening operating deficits, which are currently projected to exceed 6% of GDP, and add to supply pressures at the long end of the bond market.

Investment implications for 2026

Investors face a market defined by change, complexity and expanding opportunity. At Parametric, we don’t just adapt to these shifts, we aim to help our clients thrive in them. Our disciplined, systematic approach to investing leverages our experience in areas like direct indexing and tax loss harvesting that seek to capture opportunity wherever it emerges, while our commitment to customization helps to ensure that portfolios are built for each client’s unique goals.

The bottom line

In a world where sector leadership is evolving and uncertainty remains high, Parametric strives to empower investors to stay fully invested, manage risk proactively and seek positive after-tax outcomes. With customization, flexibility and innovation at the core of our philosophy, we’re ready to help clients turn uncertainty into potential advantage in the year ahead.

* Diversification does not eliminate the risk of loss.

Parametric and Morgan Stanley do not provide legal, tax, or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy described herein.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Parametric

Read more commentaries by Parametric