The Federal Open Market Committee (FOMC) meets this week for the first of this year’s eight formal meetings to discuss whether to keep policy as is or adjust interest rates. It is largely expected that they will leave interest rates unchanged. The struggle they are facing is the difference of opinion between the potential impact of a weakening labor market, which would incentivize easing policy by lowering the Fed Funds rate, and t

he risk of inflation reigniting, which might prompt a desire to raise the Fed Funds rate to slow its effects.

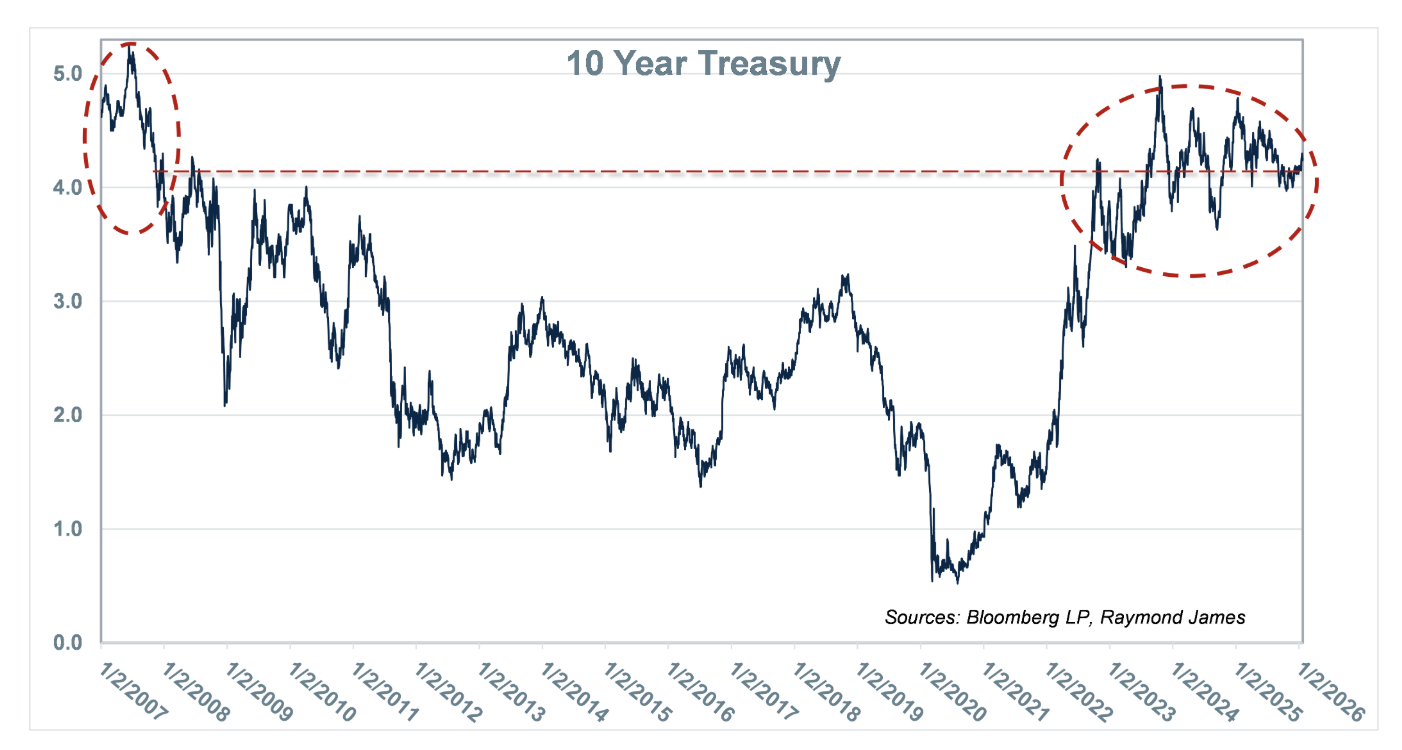

Fed Funds are the rate at which banks lend to one another for reserve balances. This rate strongly impacts the US short-term rate environment and is set by the US central bank, the Fed. There can be collateral influences on longer-term interest rates; however, longer-term interest rate changes rarely run parallel with changes in short-term interest rates. History will attest to this.

Two influences of long-term interest rates are inflation and economic growth expectations. Inflation remains a concern. Core Personal Consumption Expenditure (PCE) is the Fed’s favored inflationary measure.

Although it has fallen considerably from its pandemic-driven peak, it remains elevated (2.8%) from the desired 2.0% goal. Economic growth is measured by the Gross Domestic Product (GDP). The latest quarterly GDP release showed the 3rd quarter of 2025 at 4.4%, an impressive reflection of US economic growth. Other influences exist, including savings rates, demographic effects, perceived future risks, and, of course, central bank actions. All of these influencers are fluid and very challenging to predict their ultimate effect on future rates. The takeaway is not to solely align long-term investment plans with potential FOMC policy actions, nor to rely on outsmarting directional rate changes.

Forget the noise and the desire to outmaneuver the masses; focus on what we do know. Trying to time the market based on Fed actions can be difficult. It is equally difficult to know how long-term rates may be influenced. For the past three years, intermediate- and long-term rates have been hovering at elevated levels relative to the previous decade. This means that lower-risk individual bonds provide investors with an opportunity to lock in strong, long-term income levels, which can help preserve accumulated wealth. This may be highly appreciated by investors nearing or in retirement. Economic cycles can run for long periods. Should interest rates fall and or equity prices level off, there is no assurance of how long the economic cycle takes to return to today’s levels. Take advantage of what we know and how today’s interest rate levels can provide positive long-term security to your portfolio.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

J.D. Power 2025 U.S. Investor Satisfaction Study, which measures overall investor satisfaction with investment firms, was released 3/20/25, based on investors surveyed 1/24-12/24, who may be working with a financial advisor. Based on 7,876 responses from Advised Investors, 1 company out of 24 was chosen as the winner. The award is not representative of any one client’s experience, is not an endorsement, and is not indicative of an advisor’s future performance. The study is independently conducted, and the participating firms do not pay to participate. Use of study results in promotional materials is subject to a license fee. J.D. Power is not affiliated with Raymond James. For J.D. Power 2025 award information, visit jdpower.com/awards.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

© 2026 Raymond James Financial, Inc. All rights reserved.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - September 2025 (PDF)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Raymond James

Read more commentaries by Raymond James