Valuing AI: Extreme Bubble, New Golden Era, or Both

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPart 1

At GMO, we have always defined a bubble as a two-standard deviation divergence of the price of any asset class above its long-term real price trend. The U.S. stock market has now been in bubble territory for a prolonged period. Sooner or later, the bubble will burst and the price will return to its historic level.

In our study of over 300 two-sigma bubbles across all asset classes for which we had good history, we identified a few genuine paradigm shifts in resources (why wouldn't there be, since all are finite?) including in oil after 1970, as well as in developing markets, such as India, as their economies became more capitalist. But in large developed equity markets, two-sigma bubbles had always broken and retreated all the way to the pre-existing trend. We saw this play out in the U.S. equity market in 1929, 1972, and 2000, and in the U.S. housing market (a three-sigma bubble, the largest in any important U.S. asset class) in 2006.

But unlike every bubble before it, we have yet to see this from the December 2021 peak in the U.S. equity market, despite all the classic signs of a historic bubble top: crazy speculation, such as meme stocks, followed by a collapse of the most speculative stocks; and significant outperformance of quality stocks against the market. Yes, there was a handsome bear market in 2022 right on cue (-25% in the S&P 500, -35% in growth stocks, and almost -50% in the Magnificent 7), but this quite painful bear market was nipped in the bud, so to speak, by the introduction of ChatGPT in December 2022.

AI is a fast-moving and awe-inspiring invention that seems highly consequential—even world-changing—to almost everybody, myself included. It had an effect on what was then a deflating market of something like a multi-stage rocket. The rule from history is that great technological innovations lead to great bubbles. Especially when the technology is so obviously impressive—the science-fiction dream of a computer that can talk to you fluently, and that anyone with a phone can access anytime—that absolutely everybody will want to put their money in. This pattern of highly visible and self-evidently significant innovations leading to market euphoria, then to over-investment, and thus to severe market decline has repeated again and again throughout history, from railways to electricity to radio to the internet. AI is maybe the most visibly impressive innovation of the last 100 years, perhaps of a magnitude equal to the railways of the 19th century. It should not be surprising that it appears to be moving through the same pattern both rapidly and powerfully.

AI is certainly still an immature technology. Possibly the biggest problem with current large language models (LLMs) is that their mistakes, or “hallucinations,” are so plausible. As we searched through the scientific literature on toxicity and fertility, they made up multiple reasonable-sounding studies with agreeable and convenient results, complete with realistic-looking citations, and mixed them in among real scientific papers. They make exactly the kind of errors that you would not catch at a casual glance, or indeed, errors you would prefer not to catch. But current LLMs are hopefully (hopefully for investors, certainly) just an opening phase in AI progress—just as in the past, similarly amazing innovations had bubbles and busts before reaching a maturity in which, after digging out of their earlier collapses, they often surpassed the wildest dreams of the early speculators. If AI can start to make advances in biotechnology, materials, and energy, or even to start improving itself, the future could be very interesting indeed.

As to what happens if (or when) AI becomes far more intelligent than us, the recent book, If Anyone Builds It, Everyone Dies (Yudkowsky and Soares 2025), is a chilling and very persuasive read. The authors’ analogies and detailed examples serve as powerful reminders of our innate optimistic bias. And optimism is perhaps the most central and critical of our biases. It may indeed be that optimism has been a real help to our survival and success as a species. Now, however, with the last saber-toothed tiger long gone, our optimism causes us humans to have trouble with bubbles and financial crises, as well as other unpleasant but powerful developments, such as climate change and toxicity. When in doubt, we assume the best—despite history telling us repeatedly that things have turned out badly all too often. Over the whole of history, for example, more technologically advanced civilizations have crushed less advanced ones mercilessly and often casually, as if the damage was all incidental. And not just human history, but biological history too: no invasive species has yet made friendly allowances for other species. I’m sorry, Dave (as HAL said), I’m afraid that’s the way it is.

On the other hand, in the last century or so, as we have advanced scientifically and culturally, we've come to value other groups, tribes, and even species, more and more. So there is a chance that an even more advanced intelligence than ours may follow us in this regard. As wishful thinkers, most of us will certainly expect that. But if we were much more intelligent, we would have done a much better job of dealing with long-term problems than we have so far. With just our intelligence and self-interest, we should have done a much better job than we have done so far of preserving our commons—clean air, clean water, fertile soil, and 2.1 healthy children per family. AIs may have some chance of concluding that it is we, the humans, who are the biggest danger to life on earth! And they would be quite justified in doing so.

But as far as risks like that go, markets very seldom even try to predict important change. In complete contrast, markets extrapolate today's conditions into the distant future. Thus, in a deep recession, the market's PE ratio is extremely low. Consider the December 1974 bear market bottom, at 7.5 times earnings. Not only were the then-current earnings crushed, but their predicted recovery—reflected by the PE—was remarkably slow despite a long history of quite rapid mean reversion to the contrary. Conversely, in economic booms with peak earnings, high PE ratios signal continued abnormally strong long-term economic growth. So in October 1929, wonderful earnings were multiplied by the then-record PE of 21 times, not matched until 1972, which had similar peak earnings. More recently, in March 2000, we saw an all-time record PE of 35 times, multiplying record earnings once again. And here we are today, with investors extrapolating record earnings, continued rapid advances in AI technology, and a strong recent economy, discounting the future as if these conditions are guaranteed forever.

What is more likely, instead, is that when investor confidence sooner or later reaches its limits, the deflating of the AI bubble will lead to a major stumble for the economy, a plunge in profits, and a severe decline in valuations. For now, though, the key signs of a major bubble top—a collapse of the most speculative stocks, pronounced outperformance of quality stocks, and usually, a slowing of the rate of rise of the broad market—are not yet evident.

My former colleague, Edward Chancellor, has helped write our new book, The Making of a Permabear: The Perils of Long-Term Investing in a Short-Term World (Atlantic Monthly Press 2026). Edward is also a world-leading expert on historical bubbles. As a final favor, he has offered to write a detailed classification of the features of a bubble, comparing the current AI bubble to past innovation bubbles throughout history. (It’s economical, he says, because he will reuse most of it in an upcoming update to his seriously useful classic, Devil Take The Hindmost: A History of Financial Speculation (1999).)

Part 2

Anatomy of a Technology Mania

Edward Chancellor

Over recent months, there have been a fair number of papers, investment letters, and press articles addressing the question of whether current interest in artificial intelligence constitutes a “bubble.” The verdicts are mixed. This essay adds to the burgeoning literature on the topic. Our aim is to provide an anatomy of a technology mania, constructed from historical and more recent experience. And then to compare the current AI boom with earlier precedents. To jump to the conclusion, we believe that we are in a U.S. stock market and AI bubble, and that at some stage in the future, most investors will be nursing very large losses.

There have been countless technology bubbles over the past couple of centuries, ranging from the British railway mania of the 1840s to the SPAC bubble of 2020-21. As a rule of thumb, the more revolutionary the innovation, the greater the accompanying bubble. In his book, Engines That Move Markets: Technology Investing from Railroads to the Internet and Beyond (2001), Alasdair Nairn describes their common characteristics, which provide a useful template to gauge the market’s current embrace of AI. (Incidentally, Nairn is a former colleague of Sir John Templeton, the author of that immortal warning engraved on the heart of every value investor: “‘This time it’s different’ are the four most expensive words in the English language.”)

1. The emergence of a new technology about which extravagant claims can be made with apparent justification.

The arrival of railways generated tremendous and well-founded excitement in the early Victorian period. For the first time in history, people could travel much further and faster than on horseback. Goods could now be moved greater distances, at a lower cost and in less time. The ensuing euphoria had as much to do with the impact of railways on civilization as the economics of steam and iron. One paper jubilantly declared that “the length of our lives, so far as regards the power of acquiring information and disseminating power, will be doubled, and we may be justified in looking forward to a time when the whole world will become one great family, speaking one language, governed in unity by like laws, and adoring one God.”

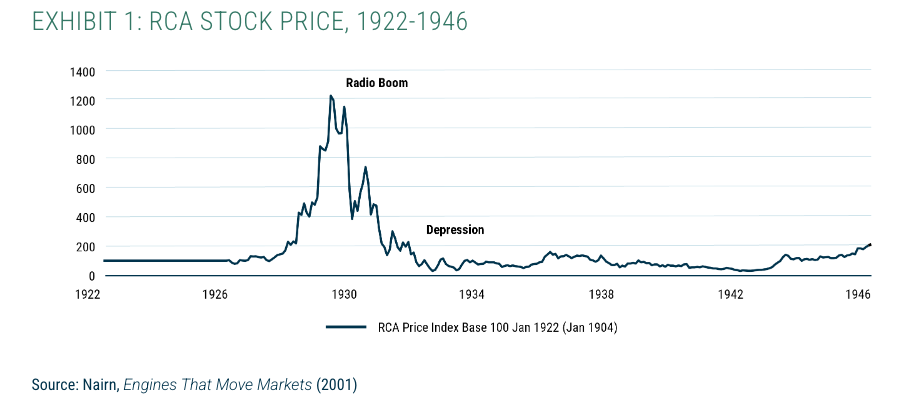

Similarly, in 1904 Nikola Tesla evangelized about the prospects for wireless technology: “the entire earth will be converted into a huge brain, as it were, capable of response in every one of its parts.” Wireless caught the imagination of the American public during the Jazz Age, when Radio Corporation of America (RCA) became the hottest stock on Wall Street.

When the internet took off in the mid-1990s, many were quick to spot the transformational nature of this novel communications medium. Nicholas Negroponte, the author of Being Digital, claimed in 1995 that “digital living” would reduce man’s dependence on time and place, close the generation gap, and contribute to world unification. The futurologist George Gilder, the author of the widely followed Gilder's Technology Report, described a "new epoch of spirit and faith" created by what he called the “telecosm” in which people would experience the "majestic cumulative power, truth, and transcendence of contemporary science and wealth." Gilder predicted in 1996 that, thanks to online learning, within five years "the most deprived ghetto child in the most benighted project will gain educational opportunities exceeding those of today's suburban preppy." Harvard would be driven out of business.

Narratives, says William Bernstein, author of The Delusions of Crowds: Why People Go Mad in Groups (2021), are “the pathogens that spread the bubble disease throughout a society.” It helps that the new technologies—railways and telegraphs in the nineteenth century, telephones and wireless in the 1920s, and the internet in the 1990s—often serve both as the object of speculation and the medium for spreading the fever.

No technology in history has been accompanied by such a compelling narrative as AI. It will cure poverty and cancer, display the creativity of Shakespeare and the inventiveness of Nobel laureates—so we are told. Sam Altman, CEO of chatbot market leader OpenAI, says that "astounding triumphs—fixing the climate, establishing a space colony, and the discovery of all of physics—will eventually become commonplace." Facebook co-founder Dustin Moskovitz's foundation, Coefficient Giving, published a report arguing that advanced AI could lead to "the economy doubling every 2-3 years." Mark Zuckerberg of Meta says AI will lead to a "new era for humanity."

There is enormous fear of AI as well as hope. Elon Musk says AI could be “one of the biggest dangers to humanity.” Two of the three main founding scientists of the science of AI are afraid. Nobel Prize winner Geoff Hinton predicts that AI is "going to create massive unemployment and a huge rise in profits. It will make a few people much richer and most people poorer." Meanwhile, his colleague, Turing Award winner Yoshua Bengio, says that AI has a chance of "causing the extinction of humanity," analogizing it to the nuclear bomb.

Never before have leading opinions on a technology been so strong and so polarized: AI promises to deliver us heaven or hell. If AI succeeds, its impact may turn out to be comparable to electricity—a general-purpose technology that significantly reshaped the economy. Whether the fears of Musk, Bengio, and others will be realized is another question, but as they say, in markets you should always sell asteroid insurance, because if it ever pays out, no one will be left to collect.

2. A climate of relatively easy money and credit conditions.

Great speculative manias usually take place during periods of easy money. This is not a coincidence. Valuation multiples increase when the discount rate is low. Likewise, a low discount rate encourages investment in companies whose profits lie in the distant future: growth, which by definition is long duration, trades at a larger-than-average premium to cheaper, short-duration, value. Easy money creates the illusion that capital is infinite.

Ready access to cheap loans encourages both companies and investors to take on leverage, facilitating capital spending and amplifying valuations for as long as the boom lasts. Excess liquidity boosts stock market turnover. Moral hazard appears when the central bank creates the impression that it will act to support the market in periods of turbulence. Speculators acquire an aura of invincibility, encouraging further recklessness.

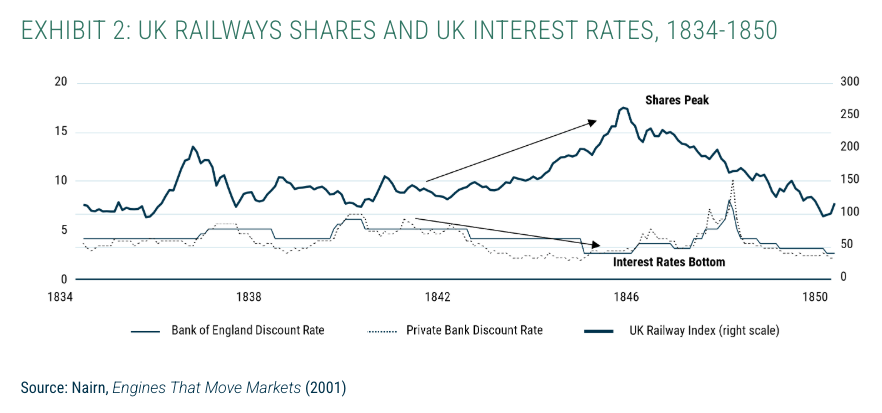

Once again, the British railway mania is instructive. Toward the middle of the 1840s, the Bank of England reduced its lending rate to 2%, which at the time was a record low. A contemporary John Fullarton observed that periods of easy money engender “a wild spirit of speculation and adventure.” The dotcom mania took off after Federal Reserve Chairman Alan Greenspan reduced interest rates in the fall of 1998 in response to the near-failure of the over-leveraged hedge fund Long-Term Capital Management. It was around this date that people on Wall Street first began to talk about a “Greenspan put” that protected investors against losses.

More recently, the Everything Bubble of 2020-2021—what the late Charlie Munger called “the most dramatic thing…in the entire world history of finance”—took place while interest rates were pegged at zero and the Federal Reserve was acquiring trillions of dollars worth of securities. Subsequently, interest rates have risen, but compared to GDP growth or inflation, they still remain historically low. Meanwhile, fiscal deficits at a scale previously only seen in wartime provide support for corporate profits and domestic spending.

3. General investor and consumer optimism.

“We find whole communities suddenly fix their minds upon one object, and go mad in its pursuit,” wrote Charles Mackay in Extraordinary Popular Delusions and the Madness of Crowds (1841), which contains descriptions of early speculative manias. Compelling narratives corrode the analytical process, says Bernstein. A group mentality takes hold. Dissonant information is ignored. Sceptics are met with vehemence.

Their warnings attract scorn and ridicule. During the first railway mania of 1836-37, one press report proclaimed, “It is not the promoters, but the opponents of railways, who are madmen. If it is a mania, it is a mania which is like the air we breathe.” Railway stocks duly fell by half shortly after this comment, but viewed over a longer timeframe, the author was obviously correct.

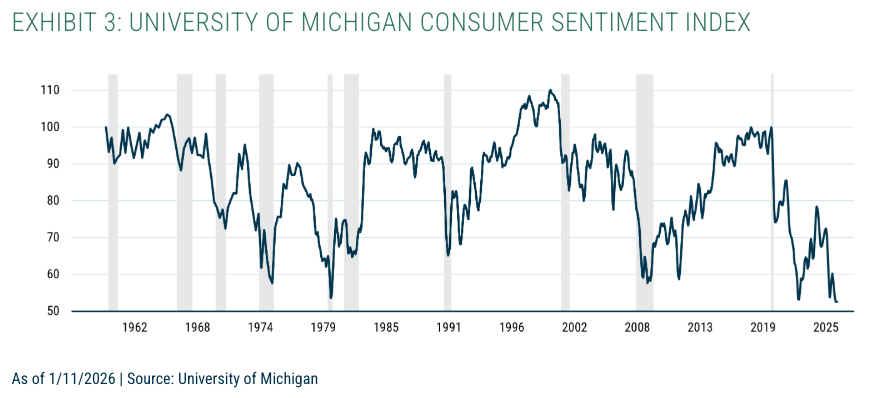

Today, American investors are optimistic, but the general public is not—a gap driven by excessive inequality. The University of Michigan's consumer sentiment index is near all-time lows, with inflation now rising and a near-record high proportion of consumers still worried about high prices. Meanwhile, investor sentiment surveys show historically high readings, NYSE margin debt is at record highs, and the share of U.S. household wealth held in equities is at its highest level ever.

With commission-free trading available on smartphone apps, plentiful cheap margin loans, and an array of leveraged ETFs, it has never been easier to speculate. There has been a surge in aggressive speculative behavior in the last several years. The Wall Street Journal claims that in 2025, "small-dollar day traders and other everyday investors played a bigger role in more markets than ever before." From 2022 to 2025, the assets of leading retail brokerage Robinhood Markets more than quadrupled. The last five years saw the GameStop meme stock craze, the explosion of zero-day options used for day-trading—which now make up over 60% of all options on the S&P 500—and the rise and rise of cryptocurrencies.

4. A wave of new publications promoting the merits of the new technology.

“New technology and overpromotion have always gone hand in hand,” says Nairn. By the early 1840s, there were three railway journals, led by the authoritative Railway Times, and during the “mania” year of 1845, new railway papers appeared nearly every week, including fourteen weekly papers (which were issued twice a week at the height of the fever), two daily papers, and both an evening and morning paper. Both The Economist and The Times of London added extensive railway supplements to their publications. Naturally, the railway journals were enthusiastic and uncritical supporters of the new railway schemes and “puffed” dubious new railways in their editorial pages, receiving in return some of the hundreds of thousands of pounds spent weekly on advertising prospectuses for new ventures.

Likewise, the arrival of the motor car was touted in a number of specialist publications, including The Horseless Age in America and Autocar in Britain (still in publication today). Wired magazine was the totemic publication of the internet mania, along with a number of other short-lived technology magazines, including The Industry Standard, Red Herring, and Business 2.0. The Financial Times restyled itself the “newspaper of the new e-conomy.” Online investment forums, such as the Motley Fool and the Waaco Kid Hot Stocks Forum, proliferated.

The AI bubble has The Information, The Rundown AI, AI Magazine, and more. Platforms such as X, TikTok, Facebook, and Substack are flooded with content about AI, made by AI, or both. Leading podcasters and influencers such as Lex Fridman, Dwarkesh Patel, Steve Bartlett, and the All In podcast heavily feature AI themes. There are a hundred new academic papers about AI being published daily on arXiv (many, no doubt, written by AI). And, of course, the discourse has escaped containment, with all the world's major media running leading stories on AI progress, AI risk, and the various shenanigans of key protagonists such as Altman, Zuckerberg, and Musk.

5. An efficient and productive supply machine, capable of creating a host of new companies to meet investor demand.

“When the ducks quack, feed them” is an ancient Wall Street adage. During the South Sea Bubble of 1720, nearly two hundred “bubble companies” sprang up, including, notoriously, a company “for carrying on an undertaking of great advantage but no one to know what it is.” A handful of these promotions involved new spurious technologies, including Puckle’s Machine Gun Company. Speculators were only required to make a small down payment on their shares.

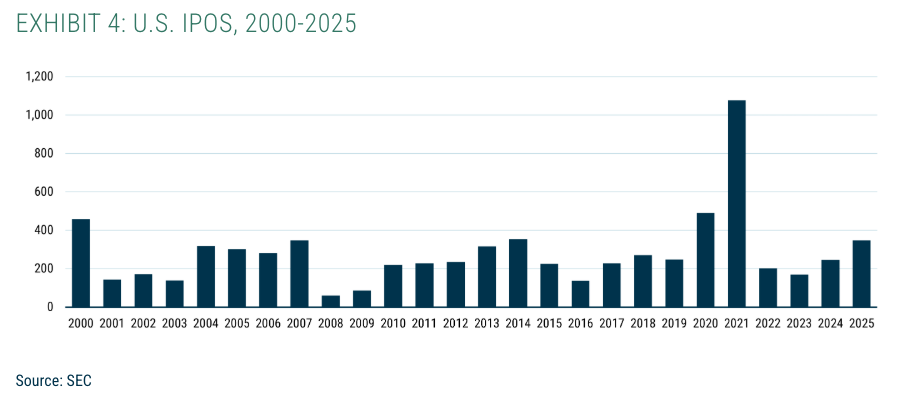

Over the course of the British railway mania, hundreds of new railway companies were established. Once again, the shares were issued on a partly paid basis, with only one-tenth of the capital paid up. The railway “scrip” could be traded immediately. Thousands of automobile companies were founded in the United States and Europe in the 1890s. A century later, a tsunami of IPOs accompanied the dotcom boom. A new record for public flotations was achieved in 2021 during the SPAC craze.

By contrast, most capital-raising for AI is largely taking place in the private markets, where the ducks are quacking very loudly.

In 2025, 60% of all U.S. venture capital investments went into AI, with AI startups raising a total of over $200 billion. Ilya Sutskever, the former chief scientist of OpenAI, raised $1 billion dollars immediately upon leaving OpenAI, solely on the basis of his past accomplishments. Anthropic, the presumptive runner-up in the consumer chatbot race today, was founded in 2021, raising $124 million in seed funding; a further $580 million in 2022, $450 million in 2023, $750 million in 2024; then a staggering $16.5 billion in 2025. It is reported to be raising another $10 billion currently. OpenAI was founded in 2015 with $1 billion, raised a further $1 billion in 2019, then $6.6 billion in 2024, and $40 billion in 2025.

While the AI start-up craze has not yet hit public equity markets, with companies choosing to stay private longer and longer, OpenAI and Anthropic are now both widely rumored to be preparing for their IPOs. On the other hand, the massive capital costs of AI expansion have started to reach more deeply into debt markets. Reuters reported in December 2025 that annual issuance of debt tied to AI and data centers had risen from $166 billion in 2023 to $625 billion in 2025. The machinery of modern finance—SPVs, private credit, asset-backed securities—is being deployed in full force to build out AI infrastructure. SoftBank borrowed its first $10 billion commitment to the $500 billion Stargate data center project; Meta's $30 billion data center, Hyperion, is financed by an off-balance-sheet SPV managed by Blue Owl Capital. ABS tied to data centers rose 19 times between 2022 and 2025.

6. Suspension of normal valuation and other assessment criteria.

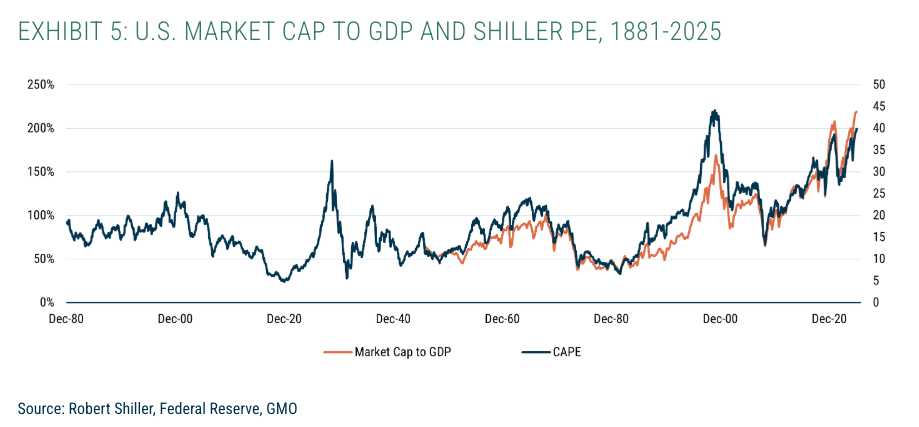

Bubbles often involve a sharp upward movement in asset prices above their real long-term trend. The cyclically-adjusted price-to-earnings multiple (CAPE) for the U.S. stock market has averaged 17.6 times since 1880. Over the course of the 1920s, the CAPE went from under 5 at the start of the decade to a peak of 32.6 shortly before the October 1929 crash. U.S. stocks didn’t surpass their 1929 valuation level until mid-1997, and continued upward reaching 43.5 times in early 2000—a record unsurpassed to this day. In late 2021, at the height of the Everything Bubble, the CAPE climbed to 38.6 times, at the time the second-highest point it had ever reached.

In the long run, the return on stocks is inversely correlated with their valuation. High valuations are on average followed by low returns, and vice versa. During the bubble period, however, investors enjoy outsized gains, but they fail to adjust downward their expectations for future stock market returns. The only way this could be rational is if they believe the market will deliver faster earnings growth in the future. That’s why great bubbles are accompanied by excited talk of New Eras.

In fact, in the late 1990s, securities analysts were projecting much faster-than-average growth in earnings-per-share. At GMO, we didn’t buy into the New Paradigm. Instead, we based our forecast for the S&P 500 on the assumption that both the market’s valuation and corporate profit margins would revert to the mean. In January 2000, we predicted that the S&P 500 would deliver real returns of -1.9% a year over the next decade. This forecast seemed outlandish at the time. In fact, U.S. stocks delivered negative returns of -3.5% a year over the following 10 years. We hadn’t been pessimistic enough!

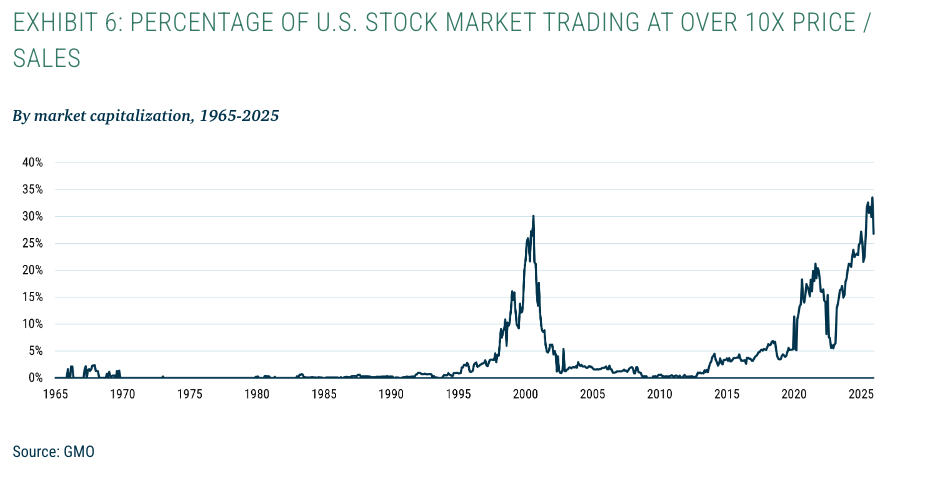

By every historically effective valuation metric, U.S. equities are now extremely overpriced. Their CAPE of 40 is above any level seen outside the very peak of the internet bubble. The U.S. market cap to GDP ratio, the so-called Buffett Indicator, is at all-time highs. A record proportion of the U.S. stock market trades at over 10 times sales; AI-enabled surveillance company Palantir trades at over 100 times sales. Tesla, Musk's flagship company, trades at over 300 times earnings, with earnings down 61% year over year and negative revenue growth.

The United States, whose companies are at the center of the AI boom, now makes up more than 70% of the MSCI World index. J. P. Morgan estimated last September that 44% of S&P 500 capitalization—over a quarter of total world market capitalization—was accounted for by just 30 AI-linked names. In January 2000, 7 of the top 10 companies by market cap came from the technology, media, and telecoms (TMT) sectors. At the time of writing, the eight largest companies in the world were Nvidia, Apple, Google, Microsoft, Amazon, Meta, Broadcom, and TSMC. Of those eight, Apple is the only one that is not a highly active participant in or apparent beneficiary of the AI race (although doubtless there will be synergies between AI and Apple's products). Saudi Aramco, the producer of 10% of all the world's oil, is down in ninth place.

Valuations in private markets are frothiest of all. OpenAI was recently reported to be valued at $750 billion, up from $30 billion in January 2023. Anthropic has been valued at $350 billion, up from $4 billion in April 2022. Mark Zuckerberg supposedly offered OpenAI's former CTO, Mira Murati, a billion dollars to join Meta's AI effort, which she turned down to start her own "company of great advantage," which was worth $12 billion before revealing to investors what it was working on. It seems that fear of missing out far overwhelms any fear of loss as a motivation for AI investors.

7. Immature technology.

Just about every technological revolution has attracted naysayers at the early stages. When Alexander Bell displayed his telephone at the Philadelphia Centennial of 1876, it was dismissed by the president of Western Union as “an electrical toy.” Ken Olsen, the cofounder of Digital Equipment Corporation, declared a year after the launch of the first Apple computer that “there is no reason for anyone to have a computer in their home.” In 1998, the economist Paul Krugman predicted that the internet’s economic impact would be “no greater than the fax machine.”

To be fair to the sceptics, nascent technologies have sometimes been vaunted despite being in an undeveloped state. In the 1880s, there was great enthusiasm for carbon arc lamps, which were viewed as a viable alternative to gas lighting. In 1880, the Anglo-American Brush Company was established and its stock climbed sevenfold. But the “Brush Bubble” burst after it became clear arc lighting was uneconomic relative to gas. At around the same time, Thomas Edison told the press that his alternative electric lighting technology would soon replace gas. The great inventor-entrepreneur implied that all the theoretical issues had been resolved and that his new invention was ready for practical demonstration, when in fact this was not the case.

“It is likely,” writes Nairn, “that he was simply proselytizing based on his earlier successes in transforming theoretical breakthroughs into commercial reality. It is also likely that his difficulties in raising funding for these breakthroughs convinced him of the need to give out only positive information.” In other words, the Wizard of Menlo Park (New Jersey) was the progenitor of “fake it till you make it” philosophy—a dictum that many later denizens of Menlo Park (California) have embraced.

At the outset of the automobile revolution, it remained unclear which motor technology would succeed. In 1900, steam-operated (“steamers”) and electric vehicles massively outsold cars powered by the internal combustion engine. Electric vehicles, championed by Thomas Edison, fell out of favor owing to their high cost and limited range—problems that have not been fully resolved a century and a quarter later.

Another feature of the major innovations is that contemporaries often fail to predict the eventual profitable applications. The early railways were used for transporting coal from the mines. Dionysius Lardner, a professor at University College, London, asserted at the time that “rail travel at high speed is not possible because the passengers, unable to breathe, would die of asphyxia.” Guglielmo Marconi envisaged that his wireless would mostly be used by the military and failed to anticipate the development of broadcast radio. During the dotcom bubble of the late 1990s, social media had yet to take off. (Facebook was only founded in 2004.)

Generative AI is an immature technology. No one can be sure how it will develop. Many experts now say that large language models (LLMs) will not lead to artificial general intelligence (AGI). Yann LeCun, the third of the three godfathers of AI along with Hinton and Bengio, argues that fundamentally new architectures need to be developed for AGI to be achieved. OpenAI co-founder Sutskever recently declared that "the age of scaling," the principle which has powered the growth in capabilities of AI models in recent years, is over. Terence Tao, the legendary mathematics professor who is by popular acclamation the smartest man in the world, wrote last December that he doubted “that anything resembling genuine ‘artificial general intelligence’ is within reach of current #AI tools.”

Nairn makes an important observation that “with technology, its use, not its wonder, is vital.” There’s no doubt about the wonder of AI. But what of its use? LLMs continue to be beset by hallucinations and lack the ability to form long-term memories or retain feedback. A widely cited MIT study in July 2025 claimed that only 5% of corporate generative AI pilot schemes showed any measurable improvement in either revenue or profitability. The real progress in AI capabilities in the last decade has been astonishing, but many major players' business and investment plans require that this pace of progress continues for years to come. If AI developments start to sputter now—or next year, or the year after—many of the promises made by the cheerleaders, and the companies built on those promises, will appear vaporous.

8. Huge overcommitment of capital, forcing down potential rates of return.

Great technological bubbles are accompanied by vast amounts of new investment. Investors become so enthused by the new opportunity that they fail to consider the full extent of competition or the probability that huge capital investments won’t generate an adequate return. Investment in the new technology is often supported by debt, which makes the situation even more perilous. Expectations of market growth become overblown even when data are readily available that, in a rational world, should temper expectations. Instead, a Field of Dreams mentality takes hold: “If you build it, they will come.”

The first railways established in Britain in the 1820s faced no competition and enjoyed monopoly-like profits. Two decades later, the competitive situation had transformed. Hundreds of new railways were proposed. Investment peaked at around 7% of Britain’s national income, according to Andrew Odlyzko of the University of Minnesota. As the country’s entire savings were directed into rail investments, The Times questioned, “whence is to come all the money for construction of the projected railways?” The newspaper later pointed out: “there does not exist the capital, the labor, or even the material, for more than a certain amount of railway production.”

A contemporary calculated that if the 8,000 miles of newly authorized railways were to deliver their expected 10% return, then the industry’s total revenue and passenger traffic would have to climb fivefold or more (from an existing base of 34 million) within the space of just five years. “This should have alarmed observers by itself,” writes Odlyzko. “But they were deluded by the collective psychology of the Mania, and distracted by concerns about the immediate problems of funding railway construction.” By the time the mania abated, there were three railway lines between London and Peterborough and another three between Leeds and Manchester. It is hardly surprising that the returns on railway investment declined dramatically.

High capital spending and destructive competition characterized the early stages of subsequent technological revolutions, most recently, the internet. In 2000, massive investment in fiber-optic cable was justified by the telecoms companies doing the spending on the grounds that internet traffic was doubling every hundred days. Yet Odlyzko and a colleague at AT&T Labs observed at the time that traffic was, in fact, only doubling every twelve months. In other words, the consensus forecast exaggerated annual growth by a factor of eight. The end result was massive excess capacity in the telecoms network that lingered for years, accompanied by a wave of business failures, including that of WorldCom, which at the time was the largest bankruptcy in U.S. history.

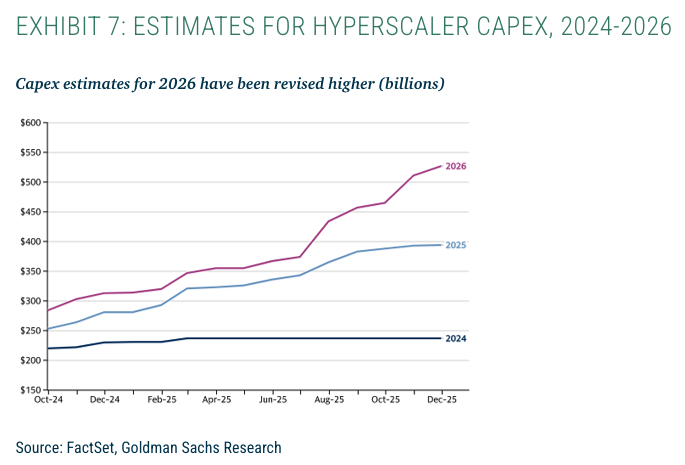

The AI boom may turn out to be the greatest capital investment bubble of all time. Amazon, Alphabet, Meta, and Microsoft alone spent nearly $300 billion on capital expenditures in 2025. AI investment accounts for an increasingly large proportion of U.S. economic activity; the collective capital expenditures of the "hyperscalers"—the biggest players in AI—are estimated to be 1.3% of U.S. GDP, the vast majority of which is going into AI hardware and infrastructure. For 2026, it is projected to rise to 1.6% of U.S. GDP.

The hyperscalers are trapped in a prisoner’s dilemma: if they hold back from the AI arms race, there’s a danger that one of their competitors will emerge triumphant. This situation more or less guarantees that they collectively over-invest. Google CEO Sundar Pichai has said that "the risk of under-investing is dramatically greater than the risk of over-investing." Meta’s Zuckerberg made a similar comment. Morgan Stanley estimates that cumulative spending on U.S. data centers will reach $3 trillion, 10% of U.S. annual GDP, by 2029; McKinsey estimates $5 trillion by 2030. Already, AI investment far surpasses that spent by the TMT sectors in 1999 and 2000.

Yet so far, the cash flow that’s needed to pay for this investment hasn’t appeared. OpenAI is projected to have $12 billion of revenue and an $8 billion operating loss for 2025. According to its own forecasts, the company expects annual losses to double again to $17 billion in 2026, then again to $35 billion in 2027. Meanwhile, AI still does not have a clear path to profitability. As happened with the internet, one will likely emerge in time as AI spreads through the economy, but for now, total revenue for AI this year is estimated at less than $50 billion against a trillion dollars or more of investment. Enormous revenue growth and profitability are required soon to fulfill the expectations implied by OpenAI's $750 billion valuation. And it now seems plausible, thanks to DeepSeek and other new Chinese entrants into the field, that AI will not be a monopoly, but may even become a commodity product—like internet broadband and mobile telephone services are today.

9. Unscrupulous and fraudulent behavior.

“In every episode,” writes Nairn, “alongside the genuine entrepreneurs and innovators there have been examples of unscrupulous investors, dishonest stock promoters and earnings-fiddling corporate executives.” The original meaning of the word “bubble” was a fraud or scam.

“The good times too of high price almost always engender much fraud,” wrote Walter Bagehot in Lombard Street: A Description of the Money Market (1877). “All people are most credulous when they are most happy; and when much money has just been made, when some people are really making it, when most people think they are making it, there is a happy opportunity for ingenious mendacity." In his book, The Great Crash 1929 (1955), the American economist J.K. Galbraith coined the term “bezzle,” which he defined as “an inventory of undiscovered embezzlement in—or more precisely not in—the country’s businesses and banks.” The bezzle grows, says Galbraith paraphrasing Bagehot, “in good times [when] people are relaxed, trusting and money is plentiful.”

During the South Sea Bubble year of 1720, not only was the leading object of speculation—the South Sea Company—in essence a fraud, but the vast majority of bubble companies were outright scams. A quarter of a century earlier, the first technology bubble appeared in London’s Exchange Alley, which involved the flotation of a number of semi-fraudulent “diving engine” companies whose ostensible purpose was to salvage sunken treasure ships, but whose real purpose was to fleece (“bubble”) gullible investors.

It is hard to think of a significant bubble that hasn’t involved a sizable bezzle. After the railway bubble burst, the “Railway King” George Hudson, head of the largest railway company, York & North Midland, was found to have capitalized expenses and paid dividends out of capital. One of the earliest accounts of the internet mania was titled “Dot.con,” as if the scandals that erupted during the bust (accounting irregularities at WorldCom, Enron, etc.) were the defining feature of the boom.

It’s important to note that the bezzle doesn’t simply describe illegal corporate behavior, but also includes dubious accounting that doesn’t strictly contravene the law. For instance, during the dotcom boom, several telecom equipment providers (including Nortel and Lucent) engaged in a practice known as vendor financing, which involved providing loans to their cash-strapped customers. The lenders got to book sales and profits up front, but later were forced to realize losses when their customers defaulted. Some telecom firms engaged in circular financing, selling fiber-optic capacity to each other in order to boost their reported revenue.

By its nature, the bezzle is only revealed in full after the fall. There are a few clear cases today of evident bezzle in the AI ecosystem. But we can find traces in the half-lies of overoptimistic projections from the boosters. The leading hyperscalers have stretched their depreciation schedules for servers and AI chips as their investment has ballooned—Meta from 3 years in 2020 to 5.5 years in 2025, Google and Microsoft both from 3 years in 2020 to 6 in 2025—even as ongoing progress in chip technology, as required for superhuman AI, will likely shorten the useful lives of chips.

The round-tripping of investment from the various biggest players in the AI ecosystem is reminiscent of the circular financing of the internet bubble. Nvidia, an investor in OpenAI stock, made a $100 billion commitment to OpenAI in 2025 that would not just support the price of its own holdings, but be spent on its own products. Amazon is a major investor in Anthropic, with Anthropic in return having committed to use Amazon Web Services as its primary cloud provider. Meanwhile, OpenAI is committed to Microsoft as its cloud provider, driving Microsoft Azure revenue—which is then invested in Nvidia chips—while Microsoft is the 27% owner of OpenAI.

10. The shakeout.

The investment that accompanies bubbles inflates both corporate revenues and profits. When the bubble eventually pops, earnings contract along with valuations. Investors face large losses: British railway stocks declined by more than 65% in the second half of the 1840s. The stock of Edison Electric round-tripped from under $200 in early 1879 to over $3,000 in 1880 and back below $200 the following year. The share prices of both General Motors and RCA followed a similar trajectory before and after the Great Crash. The Nasdaq index lost nearly 80% of its value in the dotcom bust. An index of SPAC companies dropped roughly the same amount between March 2021 and February 2023.

There usually follows a surge in corporate bankruptcies and scandals. The bezzle shrinks. As Galbraith says, “Money is watched with a narrow, suspicious eye… Audits are penetrating and meticulous.” The damaging effects of excessive competition become evident. Price wars break out. Industry consolidates. The eventual corporate winners from the new technology appear. Firms with weak balance sheets are most likely to fail during the shakeout, while those with strong balance sheets generally come out on top. All new technologies go from capital starvation to capital surplus and back again, says Nairn. Winning the technology battle is no guarantee of commercial success; the best technology does not always win, he adds.

As with the bezzle, the story of the shakeout phase of the bubble has yet to be written. It is clear that U.S. corporate profits growth is being driven by massive AI investment. Strategist Gerard Minack writes, “as in the TMT cycle… a positive feedback loop [exists] between rising investment spending and rising profits: the firm selling capital goods immediately reports its profits in full, while the firm buying the capital good depreciates its cost over time.” A very large share of Nvidia's earnings comes from data centers being built now that will only pay off if AI continues to improve and takes over the economy.

A change of sentiment toward the sector could bring down valuations, which in turn would sharply curtail investment and bring down profits. After the market peak in March 2000, the revenues for internet hardware companies, such as Cisco, collapsed.

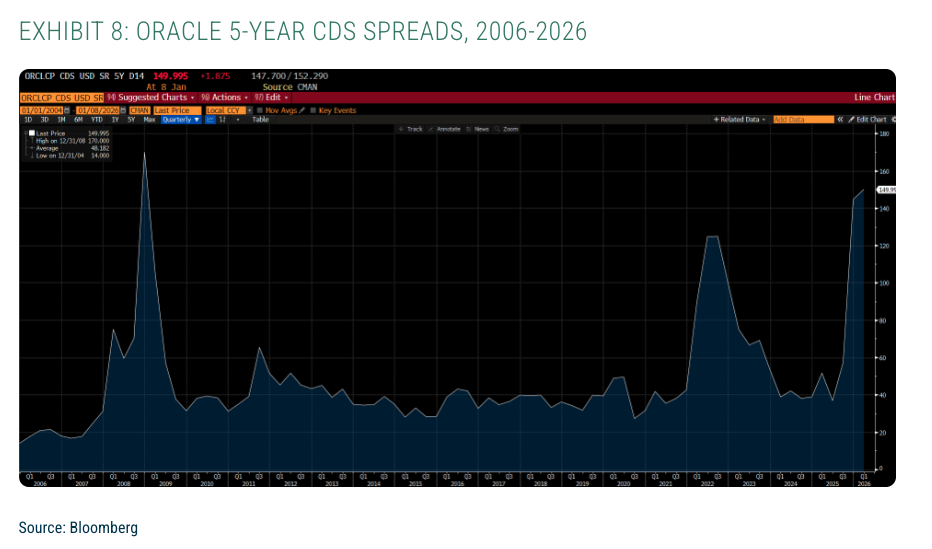

Our hunch is that we may be close to the end of the investment boom. Meta's AI spending frenzy has taken the company from a net cash position of nearly $30 billion in 2023 to minus $7 billion today. Overexposed data center operators or “neoclouds” have begun to be pressured by markets. For instance, the stock price of CoreWeave, which floated last March, is down more than 50% from its peak. Oracle, with over $100 billion in net debt and having burned $12 billion of cash in the third quarter of 2025 alone, saw its CDS spreads rise from a low of 40 basis points in September to 140 in December. Oracle’s stock is down around 40% over the same period. The stock price of Blue Owl, lender to Oracle and OpenAI's Stargate and Meta's Hyperion data center projects, has lost a fifth of its value since last summer.

The scale of the AI investment is now beginning to limit itself, as it has started to drive up the prices of other computer components such as DRAM (used in every laptop and phone as well as in data centers)—the price of which was reported up 172% year over year in the third quarter of 2025 and further since—as well as the prices of commodities, including copper and silver, and the price of electricity (which is up 39% in the last five years in the U.S., substantially ahead of inflation). BlackRock expects that extravagant AI investment may push up long-term interest rates. Bubbles often collapse after interest rates rise.

Conclusion

Edison is remembered as the man who brought electricity to the United States. But his company ran into trouble in 1890 after the heavy capital costs involved in constructing hundreds of power stations. Edison Electric was merged with another firm in 1890 to form General Electric, whose share price collapsed over the following years, despite strong sales growth. Henry Ford only succeeded on his third attempt. General Motors was forced into two corporate reorganizations. The personal computer industry ran into difficulties in the early 1980s. Apple’s market capitalization currently exceeds $4 trillion, but cofounder Steve Jobs was forced to leave the company in 1985 after losses mounted (he returned to the company more than a decade later). Amazon today is worth nearly $2.5 trillion. Nevertheless, its stock price dropped over 90% in the dotcom crash.

Bubbles have long tails. It took Cisco, the leading provider of internet equipment and briefly the world’s most valuable company, a quarter of a century and another technology bubble to regain its peak. Today, Nvidia is the world’s most valuable company. Its market capitalization currently exceeds the entire Japanese stock market. Japan’s stock market, of course, took an incredible 35 years to recover its losses after its bubble peaked in late 1989.

Every past technology bubble has been identified in real time in the mainstream press. Yet warnings were ignored. In the bust, the crowd mentality dissipates, and the extravagances of the boom—absurdly optimistic forecasts, heavy investment, ruinous competition, a lack of cash flows to justify sky-high valuations, high debt burdens, dodgy accounting, etc.—become evident to all. The ensuing losses appear not so much unsurprising as inevitable.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All