January reinforced our key theme for 2026 – returns must be earned. Markets moved beyond the mag 7 as solid economic growth, a more patient Federal Reserve, and widening market leadership rewarded disciplined diversification. Gold’s parabolic rally and violent reversal showed what happens when discipline breaks down.

Monthly Market Update

-

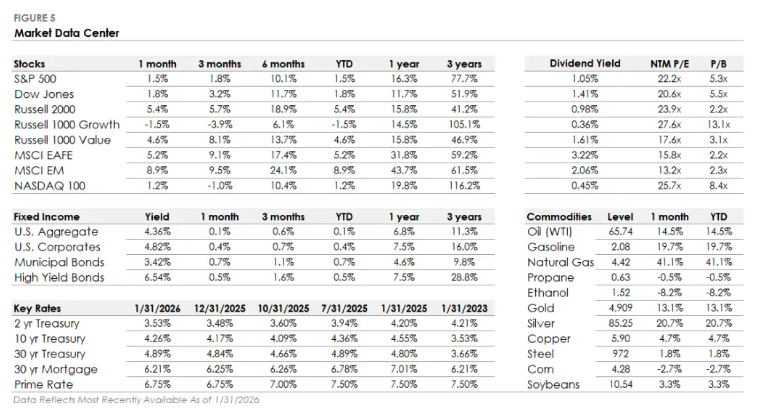

Stocks: US equities moved higher in January, with the S&P 500 gaining 1.5% and setting a new all-time high above 7,000 as leadership broadened beyond mega-cap technology..

-

US Market Leadership: Small caps and value stocks led the market. The Russell 2000 rose 5.4%, while large-cap growth declined as investors rotated toward more economically sensitive sectors.

-

International Stocks: International equities outperformed as the USD weakened. Developed Markets gained 5.2%, while Emerging Markets rose 8.9%.

-

Bonds: Bonds delivered modest gains despite rising Treasury yields, with the broad US Bond Aggregate gaining 0.1%. Corporate bonds outperformed Treasuries as credit spreads tightened and economic data remained supportive.

-

Bonds: Bonds delivered modest gains despite rising Treasury yields, with the broad US Bond Aggregate gaining 0.1%. Corporate bonds outperformed Treasuries as credit spreads tightened and economic data remained supportive.

-

Gold & Silver: Bonds delivered modest gains despite rising Treasury yields, with the broad US Bond Aggregate gaining 0.1%. Corporate bonds outperformed Treasuries as credit spreads tightened and economic data remained supportive.

The Fed Pauses, Growth Holds Up

The Federal Reserve held interest rates steady in late January, pausing its rate-cutting cycle after three consecutive reductions at the end of 2025. The policy statement leaned more hawkish than recent meetings, upgrading language around labor market stability and describing economic growth as solid rather than moderate. Fed Chair Powell emphasized that the Fed is well-positioned to remain patient as it evaluates inflation and growth trends.

Economic data supported that stance. Labor market indicators improved, unemployment declined, and consumer spending remained resilient despite lingering weakness in sentiment surveys. Several research providers upgraded 2026 growth expectations to around 2.0%, with inflation expected to remain uneven near term before moderating later in the year.

In our view the combination of stable growth and a cautious Fed means higher-for-longer isn’t a risk scenario anymore – it’s the baseline for 2026. Incoming Fed Chair Kevin Warsh remains a wildcard, but we expect he will likely be more hawkish than expected.

Gold Soars Above $5,400, then Breaks

January’s most dramatic story wasn’t in equities – it was gold’s surge to all-time highs above $5,400 per ounce before collapsing over 10% on the last day of the month. Silver reached $117 per ounce (up over 300% in the past year), before tumbling 31% Friday in its worst single-day drop since 1980. Even after the selloff, gold finished January up 13%.

The rally was driven by more than diversification. Central banks continued aggressive buying, investors concerns about rising government debt continued, and geopolitical chaos (Trump’s Greenland threats, Venezuela intervention, Iran tensions) reinforced gold’s safe-haven appeal. Topping it all off – Chinese speculators piled in, adding momentum and froth to the move.

The reversal was trigged by Trump’s nomination of Kevin Warsh, viewed as hawkish, to lead the Federal Reserve. Profit-taking accelerated after the relentless rally, and the lack of market depth, leverage (especially in Silver) meant small flows triggered violent moves. This wasn’t fundamental – it was a reset after speculation ran too far, too fast.

As we’ve discussed recently (Revisiting Gold’s Role in a Diversified Portfolio) a modest long-term allocation to gold provides meaningful portfolio benefits, especially when central banks are holding rates higher and equity valuations leave less room for error. Rather than trying to “trade” gold, we view it as a core portfolio component in a long-term, diversified portfolio. Precious metals won’t solve every problem, but they can provide differentiated returns when stocks and bonds move together.

Leadership Broadens As Diversification Pays

January also marked a meaningful shift in market leadership. After years of performance driven by a narrow group of mega-cap technology stocks, returns broadened across sectors, styles, and regions. Energy led all S&P 500 sectors as oil prices surged, while small-cap and value stocks materially outperformed large-cap growth. International markets also delivered strong relative results as the dollar weakened and global growth expectations improved.

Narrow leadership and concentrated returns has been a headline market risk for years. Broader participation is healthier – and harder to navigate for investors who got comfortable betting on five stocks. With valuations elevated in parts of the US equity market and monetary policy on pause, returns are increasingly coming from diversification rather than concentration.

Dividend-growing companies, global infrastructure, senior loans, and select real assets offer more balanced risk and return profiles than chasing last year’s winners. Infrastructure spending tied to data centers, energy generation, and reshoring trends remains a durable long-term tailwind, even as short-term market leadership rotates.

Given changing market dynamics, a new Fed later this year, and broadening returns investors relying on a single theme or sector to carry portfolios forward may find 2026 less forgiving than prior years.

Staying Disciplined as Volatility Returns

As we discussed in our 2026 Outlook, Earned Returns, Valuations are full, policy uncertainty persists, inflation progress won’t be linear, and volatility will be a feature of markets this year, not a bug.

This combination favors discipline over prediction. Chasing leadership after extended runs or abandoning diversification when it feels unnecessary creates avoidable mistakes.

Our focus remains on building resilient portfolios that adapt as leadership shifts. That means balancing growth with income, liquidity with opportunity, and conviction with risk management. January proved what we’ve been saying: diversification isn’t dead weight when markets work. It’s what keeps you in the game when they don’t.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group