Our most pointed advice for investors in 2026 is simple: Expect the unexpected.

Barely a month into 2026, markets have already weathered multiple bouts of rolling, event‑driven volatility. Geopolitical surprises and policy pivots have triggered sharp price moves from the U.S. to Japan to Europe, from sovereign bonds to currencies to mortgages. Often, markets quickly reacted to headlines – and then just as quickly reversed course.

In prior cycles, geopolitical foundations seemed more steady and central banks telegraphed moves quarters in advance. Today, fundamental uncertainty around discretionary government actions is driving volatility. We expect the pattern of surprises, price swings, and fast‑changing market narratives to persist – and investors will need to adapt.

The Fragmentation Era

For decades, investors relied on a stable global system built on open markets and shared policy norms. That framework is breaking down. Indeed, Canadian Prime Minister Mark Carney, a former member of PIMCO’s Global Advisory Board, warned of “a rupture in the world order” at January’s World Economic Forum. Long-held assumptions about trade, fiscal discipline, institutional independence, and global alliances are all being tested – a transformation we anticipated in our 2025 Secular Outlook, “The Fragmentation Era.”

A more fragmented, mercantilist world changes how markets work. Capital may be allocated less efficiently as nations prioritize strategic interests over purely economic ones. New risks – as well as new opportunities – can arise in markets historically viewed as stable. Gaps between winners and losers are likely to widen among countries, sectors, and companies.

Fragmentation expresses itself through higher dispersion and a greater sensitivity to policy shocks. Such conditions reward active security selection over broad market exposure.

Case study: The U.S.

U.S. policy communication has been at the center of recent volatility. A partial list of what markets had to digest in January:

- A military operation in Venezuela

- Uncertainty around U.S. intentions regarding Greenland

- An unanticipated proposal to cap credit card interest rates at 10%

- A Medicare proposal to keep payments to insurers almost flat in 2027

- A directive to government-sponsored housing agencies Fannie Mae and Freddie Mac to buy $200 billion in mortgage bonds

The ensuing volatility has been a source of risk – witness the respective share-price drops for banks and insurers on the credit card and Medicare proposals, and the U.S. dollar’s volatility.

It has also led to opportunities. We have long found mortgage-backed securities (MBS) attractive, while U.S. policy has been broadly aligned toward making housing more affordable (for more, see our September 2025 PIMCO Perspectives, “A Fed Housing Fix That’s Hiding in Plain Sight”). The day of the policy announcement, MBS spreads tightened by about 15 basis points.

As seen in the housing and Medicare proposals, affordability has become a broader U.S. political theme. Investors don’t want to be caught on the other side in sectors where affordability policies might be enacted.

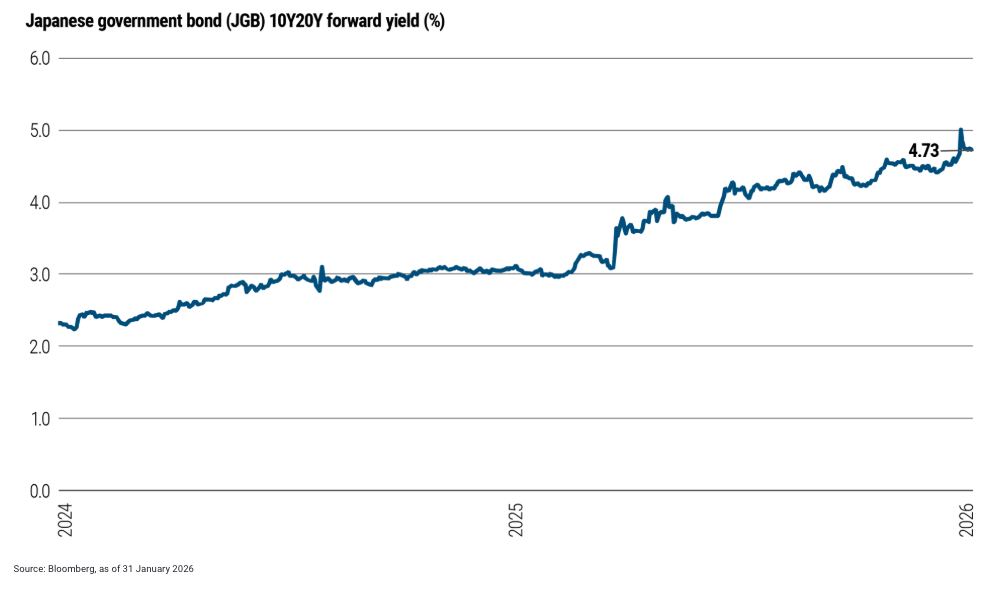

Case study: Japan

That said, policies aimed at affordability can also backfire, particularly when they run into concerns about rising government debt levels (for more, see our December 2024 PIMCO Perspectives, “Thoughts From the Bond Vigilantes”). In Japan, a proposed consumption tax cut triggered a bond market sell-off (see Figure 1) against a backdrop of loose fiscal policy.

Figure 1: Japan yields spiked in January amid fiscal concerns

It was reminiscent of the UK in 2022, when a proposed tax cut sparked a bond market rout. Policies may move markets, but at extremes markets can also adjust and even reverse policy initiatives.

The experiences in the U.S. and Japan underscore a broader shift: The skills investors have long needed to navigate policy shocks in emerging markets (EM) – rapid sovereign credit analysis, real-time assessment of fiscal credibility, positioning for currency volatility – are now increasingly required across developed markets (DM) as well.

A playbook for volatility

Markets may appear calm during stretches today even as vulnerabilities build beneath the surface. Traditional volatility measures such as the VIX and the MOVE Index can signal complacency in both equity and bond markets even as risks rise.

Investors have enjoyed a years-long bull market in stocks, fueled in large part by technology. But as AI continues to disrupt industries and the economy more broadly, the equity-market volatility seen in recent days – particularly in tech-related sectors – shows just how uncertain the outlook remains.

This isn’t a year to sit on one’s hands and hope volatility disappears. Instead, 2026 calls for an agile mindset built for uncertainty:

- Be cautious and disciplined on valuations. U.S. equity valuations continue to appear stretched, leaving little cushion and greater susceptibility to sudden swings.

- Watch out for signs of market complacency.

- Make greater use of relative value strategies rather than directional bets.

- Stay flexible across regions, not just sectors, with the ability to move capital decisively and find value – particularly when attractive yields are available in many countries.

- Be nimble enough to react quickly when volatility creates dislocations – whether in Japanese government bonds, U.S. agency MBS, or EM sovereigns – leveraging global scale and local presence to identify opportunities.

In a world of frequent surprises, the greatest risk may be static positioning. Portfolios built for adaptability – global, liquid, actively managed across both DM and EM – stand to capture opportunities that passive, domestically focused strategies can miss.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

Pacific Investment Management Company LLC (“PIMCO”) is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). PIMCO Investments LLC (“PIMCO Investments”) is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (“FINRA”). PIMCO and PIMCO Investments is solely responsible for its content. PIMCO Investments is the distributor of PIMCO investment products, and any PIMCO Content relating to those investment products is the sole responsibility of PIMCO Investments.

The information provided herein is not directed at any investor or category of investors and is provided solely as general information about our products and services and to otherwise provide general investment education. No information contained herein should be regarded as a suggestion to engage in or refrain from any investment-related course of action as none of PIMCO nor any of its affiliates is undertaking to provide investment advice, act as an adviser to any plan or entity subject to the Employee Retirement Income Security Act of 1974, as amended, individual retirement account or individual retirement annuity, or give advice in a fiduciary capacity with respect to the materials presented herein. If you are an individual retirement investor, contact your financial advisor or other fiduciary unrelated to PIMCO about whether any given investment idea, strategy, product or service described herein may be appropriate for your circumstances.

Check the background of this firm on FINRA's BrokerCheck.

Account Managers Compensation

PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2026 PIMCO. All Rights Reserved. Investment Products: NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED.

© PIMCO

Read more commentaries by PIMCO