Key Takeaways

- For the better part of the last three years, technology stocks have outperformed their peers. More recently, the sector has been showing signs of struggle.

- Amid concerns around growth going into 2026, investors have begun rotating out of the heavily concentrated mega-cap tech names and into more economically sensitive sectors, such as energy, materials and industrials.

- However, as most tech companies continue to deliver strong quarterly earnings growth, Russ cautions that holding – not abandoning – these names is still warranted.

After more than three years of stellar gains, technology companies, or more specifically their stock prices, are struggling. Expectations for economic acceleration and overly concentrated portfolios have led investors to re-allocate to many previously ignored parts of the market. While I believe there are interesting non-tech opportunities and some re-allocation is justified. I don't think investors should abandon the sector.

It was a very good run while it lasted. Between October of 2022 and last November’s market bottom, the S&P Technology sector gained roughly 130%, outperforming the market by approximately 50%. For the leaders, the gains were far larger. The semiconductor industry advanced 275%, while market leader Nvidia surged by more than 1,500%. Given the length and magnitude of these gains, a little catch-up by the rest of the market appears warranted.

Beyond bargain hunting, there are at least two factors driving the broadening out of the equity rally and the recent underperformance by technology companies. The economy is accelerating, and the earnings gap between tech and the rest is narrower than a few years ago.

Following a brief collapse in confidence last spring, economic expectations are rising. According to Bloomberg, a consensus of economic forecasts for 2026 real GDP has risen from 1.4% last May to 2.1% today. As investors discount faster growth on the back of capital spending and tax refunds, they are more inclined to rotate towards economically sensitive sectors, notably energy, materials and industrials.

The second catalyst for the rotation is a shift in earnings expectations. To be more precise, investors are now expecting a narrowing gap between mega-cap tech and the rest of the market. This marks a significant shift, as the large tech companies were one of the few bright spots during the earnings slowdown of 2023 and 2024. Today, with more sectors expected to post positive earnings growth, the differential between mega-cap tech and the rest of the market is much smaller.

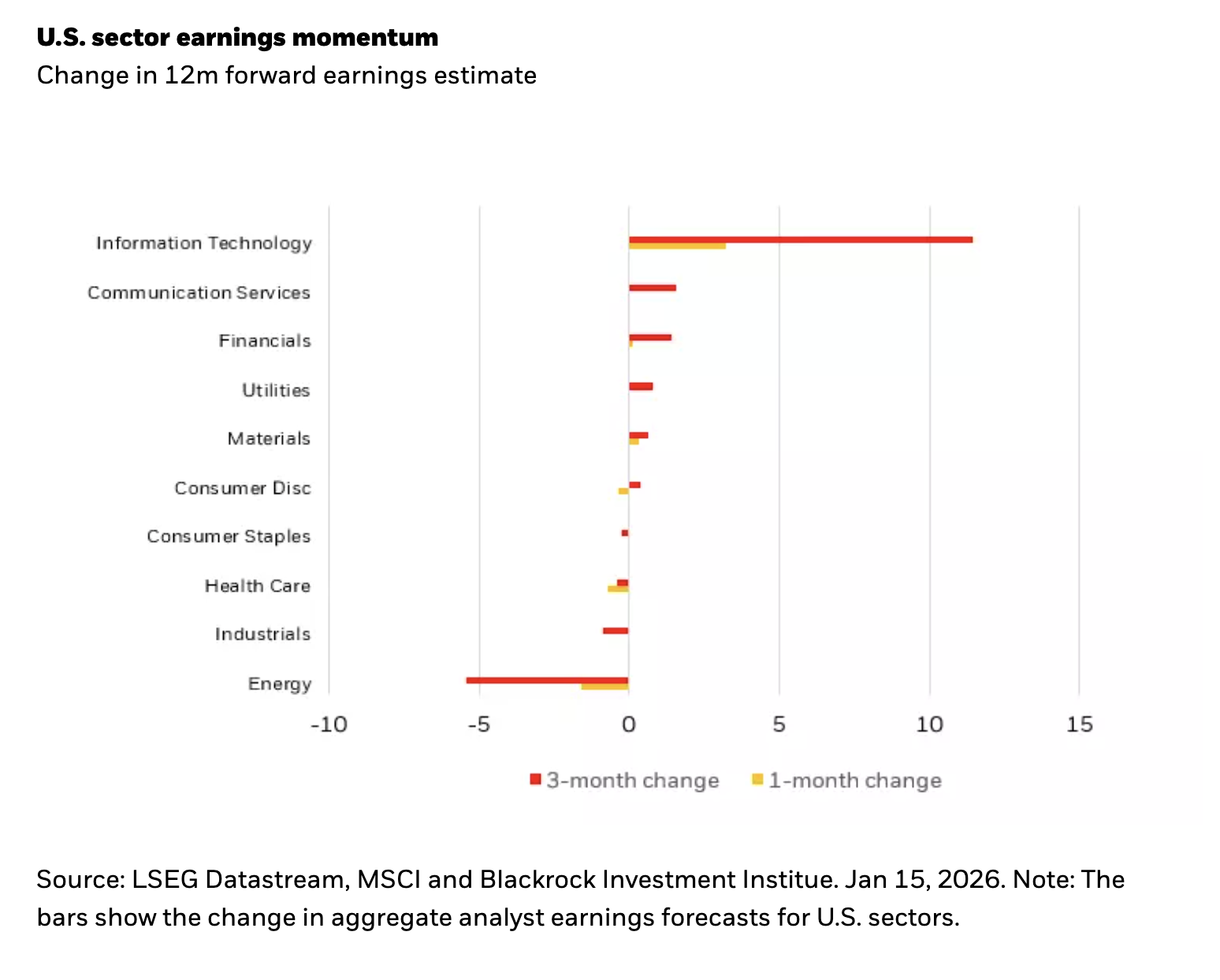

However, the rush out of technology names, particularly the mega-cap variety, ignores the sector’s earnings momentum. For Q4 the tech sector is expected to post approximately 25% year-over-year earnings growth, far ahead of the 8% for the broader market. Earnings momentum is also strongest in the tech sector, with by far the most positive changes in earnings expectations (see Chart 1). Finally, the superstar companies are still the big driver of earnings growth. Nvidia is expected to be the single largest contributor to this quarter’s earnings growth.

Diversify don’t abandon

Given the economic outlook, value differentials and the lingering impact of too much crowding, some sector re-allocation makes sense. Large banks, consumer discretionary and select industrials offer leverage to what is likely to prove an accelerating economy. That said, the valuations of many mega-cap tech names have normalized, while the sector is likely to continue to deliver unusually strong earnings growth. The sector is still very much worth holding.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month end, please click on the fund tile.

The Morningstar RatingTM for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure (excluding any applicable sales charges) that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Russ Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and Lead Portfolio Manager for BlackRock’s Global Allocation (GA) Selects Model Portfolios and is a regular contributor to Market Insights.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risks, including possible loss of principal.

Investments in technology industries may be affected by limited product lines, markets or financial resources. Technology industries are rapidly changing and stocks of these companies may be more volatile than the stock market in general.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

There can be no assurance that performance will be enhanced or risk will be reduced for funds that seek to provide exposure to certain quantitative investment characteristics ("factors"). Exposure to such investment factors may detract from performance in some market environments, perhaps for extended periods. In such circumstances, a fund may seek to maintain exposure to the targeted investment factors and not adjust to target different factors, which could result in losses.

The Fund is actively managed and does not seek to replicate the performance of a specified index, may have higher portfolio turnover, and may charge higher fees than index funds due to increased trading and research expenses. There is no guarantee the fund will meet its investment objective.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the value of debt securities. Credit risk refers to the possibility that the debt issuer will not be able to make principal and interest payments.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may be subject to federal or state income taxes or the Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 2026 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Prepared by BlackRock Investments, LLC, member FINRA.

©2026 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK and iSHARES are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

FFI0226-5172339-EXP0227

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© BlackRock

Read more commentaries by BlackRock