Private credit has been in the news lately. That’s nothing new. For years, investors have read about the potential opportunities the asset class offers and how it works. Let’s dig a little deeper into what private credit is, what it isn’t and how it can fit into a diversified investment portfolio.

First things first: We consider private assets—and private credit in particular—a core building block of a diversified asset allocation. Adding it to an investment portfolio has the potential to increase return and reduce volatility. Recent media headlines have warned of hidden risks. That might be true in some parts of the market, but not every part. To understand why, it can help to get back to basics.

Demystifying the World of Private Credit

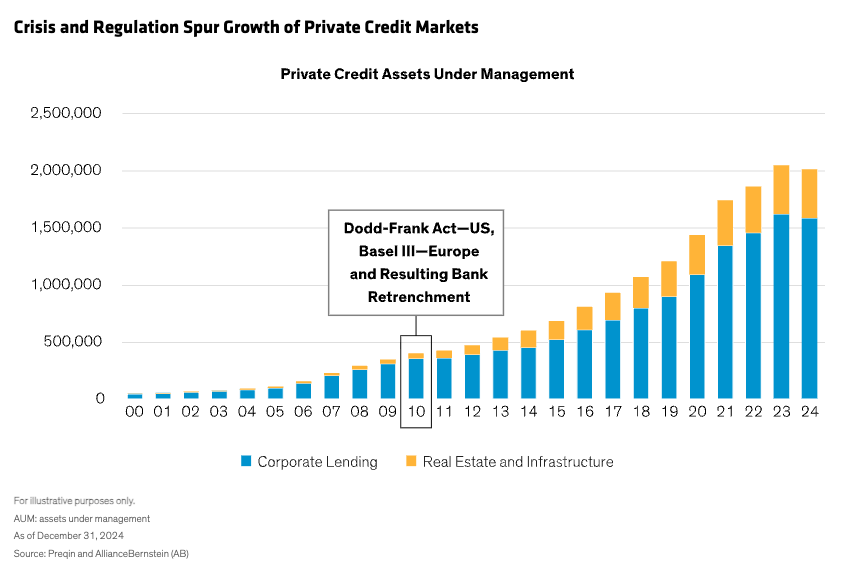

In simple terms, private credit is lending outside the banking system. Once a small portion of total credit extended to non-financial companies, it started to grow after the global financial crisis as regulators increased restrictions on banks’ risk-taking. When the Dodd-Frank Act in the US and global Basel III bank capital requirements took effect, banks pulled back while asset managers, insurance companies and other private lenders leaned in to fill the void (Display).

Banks still lend, but more selectively. A bank might refuse to make a loan above a certain multiple of a company’s earnings before interest, taxes, depreciation and amortization. These restrictions are often applied universally: A profitable tech firm with steady revenues might be treated as cautiously as an oil-field services firm exposed to oil price fluctuations, regulatory risk and geopolitical risk.

Diverse Opportunities in Private Corporate Lending

This led to the rise of direct corporate lending. Here’s how it usually works: A private equity fund buys a company and provides 60% of the purchase price, financing the rest with private debt. That 40% comes from a private loan that puts a lien on all assets. That legal structure puts the private lender first in line to be repaid if the company is sold—important protection for lenders.

These investments are less liquid than those in public high-yield corporate bonds or syndicated bank loans, so they offer a floating interest rate and higher yields. We see the most attractive opportunities in core middle-market companies with enterprise values between $100 million and $1.5 billion. In the US, that’s about 200,000 firms with nearly 48 million jobs—roughly one-third of total private-sector employment. If the middle market were a country, it would have the world’s third-largest GDP (Display).

Individually, these companies are usually not large enough to access the broadly syndicated loan market, which usually means more attractive pricing and better terms for lenders—and investors. Terms can include protective covenants such as caps on the amount of leverage a borrower can have, which may improve downside risk mitigation.

Beyond Direct Lending: Financing the Real Economy

But there are other flavors of private credit with diverse levels of return potential and risk. For example, much consumer and small-business spending is financed privately, and we think investment strategies focused there offer attractive return and diversification opportunities.

The $6-trillion-and-growing asset-based finance market offers consumer, residential and small-business lending that fuels the real economy. The financing usually comes from purchases of existing loans for autos, homes and commercial properties, credit cards, and more. Private lenders can also agree to buy pools of future loans from the non-bank financial institutions that make them. Sometimes, loans are backed by income-generating physical assets, such as energy infrastructure or leased airplanes.

The loans are highly diversified, given the underlying assets’ diverse economic drivers. Pools of consumer loans often include thousands if not tens of thousands of loans in each deal. The loans are also self-amortizing—they repay their principal gradually over time, becoming less risky as they do.

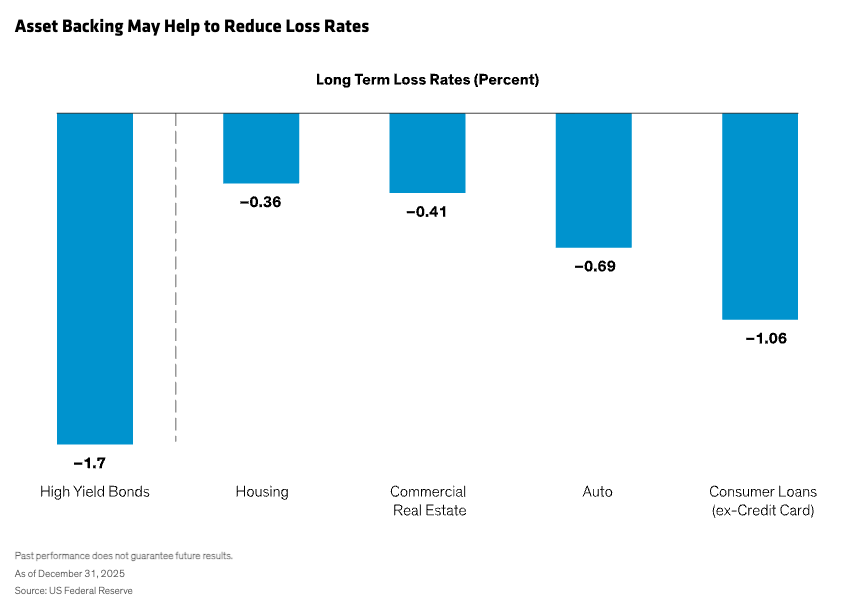

And like direct corporate loans, they too come with important structural protections that may help to mitigate losses. For one thing, the loans are backed by physical collateral. As a result, recoveries in the event of default have historically been strong.

We see asset-based finance as a strong complement to direct corporate lending. And we expect the market to keep growing. The massive amount of capital needed to finance the energy transition and the digital infrastructure and data centers that power AI rely heavily on private lenders that can customize loans and provide other benefits. Borrowers increasingly include firms that also tap public debt markets.

How Private Credit Handles the Credit Cycle

What about when things go wrong, as can happen sometimes in lending? For example, there were a few bankruptcies last year at companies partly financed by private credit, though their long list of creditors also included major banks. Some of these cases involved allegations of fraud and misappropriating collateral. If nothing else, this is a good reminder that defaults are natural in credit investing—public and private. And they’re more likely in the later stages of an economic cycle.

But as we see it, the real question isn’t whether defaults happen. It’s how they’re handled when they do—and whether they translate into losses.

The keys to navigating private lending, as mentioned earlier, are experience, strong underwriting and structuring loans in ways that may reduce losses in defaults. Negotiated covenants and reporting obligations enable lenders to be proactive.

Other built-in features may help reduce risk. Loans are usually made at the senior levels of a firm’s capital structure, the first in line for full or partial repayment in a default. Private loans to middle-market firms typically benefit from a large equity cushion that’s first to absorb losses tied to declines in a borrower’s value. Lenders, borrowers and private equity firms interact often, giving lenders insight into borrowers’ performance. That level of influence isn’t possible in broadly syndicated loans, often with 50 to 80 lending participants or more. And in rare cases where all avenues of redress have been exhausted, private lenders can seize assets, including real estate and equipment, to pay off the debt.

Private credit, like public debt, isn’t immune to economic cycles, which can bring stress and potential defaults. Different market segments go in and out of favor. But we believe that experienced managers with a track record of identifying, executing and managing attractive private credit investments have the potential to uncover real value for investors while providing robust downside mitigation potential.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Brian Resnick is a Director and Senior Investment Strategist for Alternatives.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein