Why Bitcoin’s Capitulation Event Sets Up a Contrarian Buy

Membership required

Membership is now required to use this feature. To learn more:

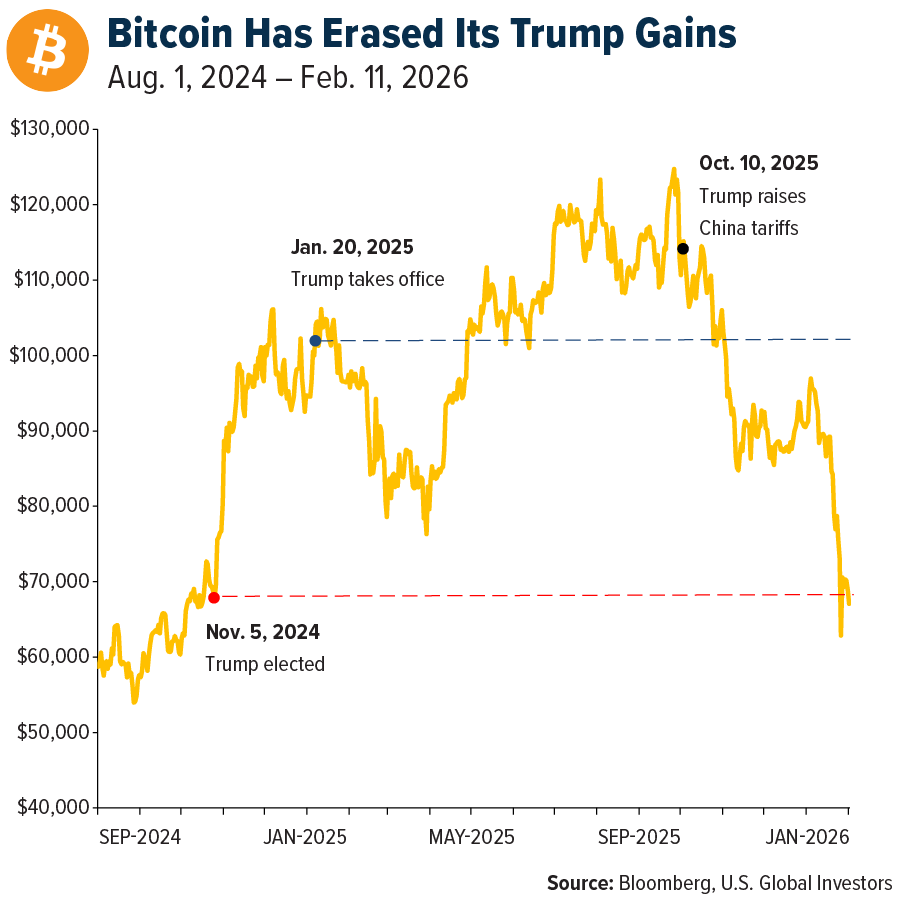

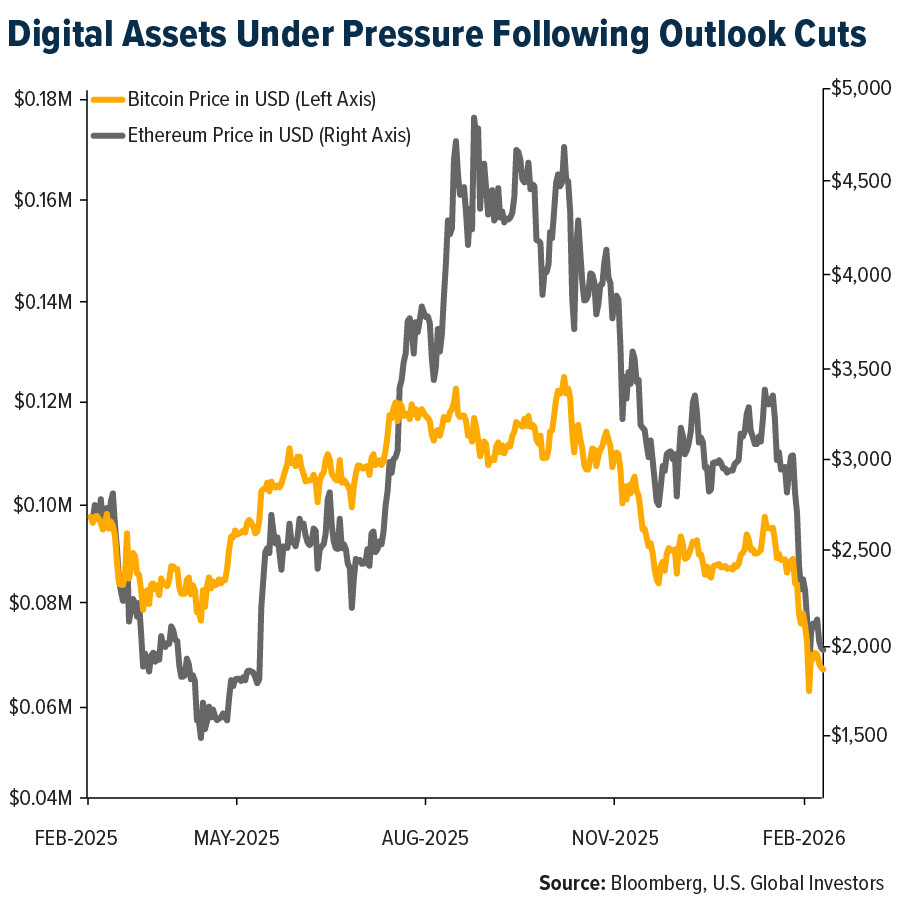

View Membership BenefitsFour months ago, digital assets underwent what I believe was the most consequential liquidation event in their history. On October 10, 2025, over $19 billion in leveraged positions were wiped out within hours. Bitcoin plummeted from roughly $122,000 to $105,000. More than 1.6 million trader accounts were liquidated.

The 10/10 crypto crash, as it’s sometimes called, did more than just rattle the market. It fundamentally altered the psychological landscape of crypto investing.

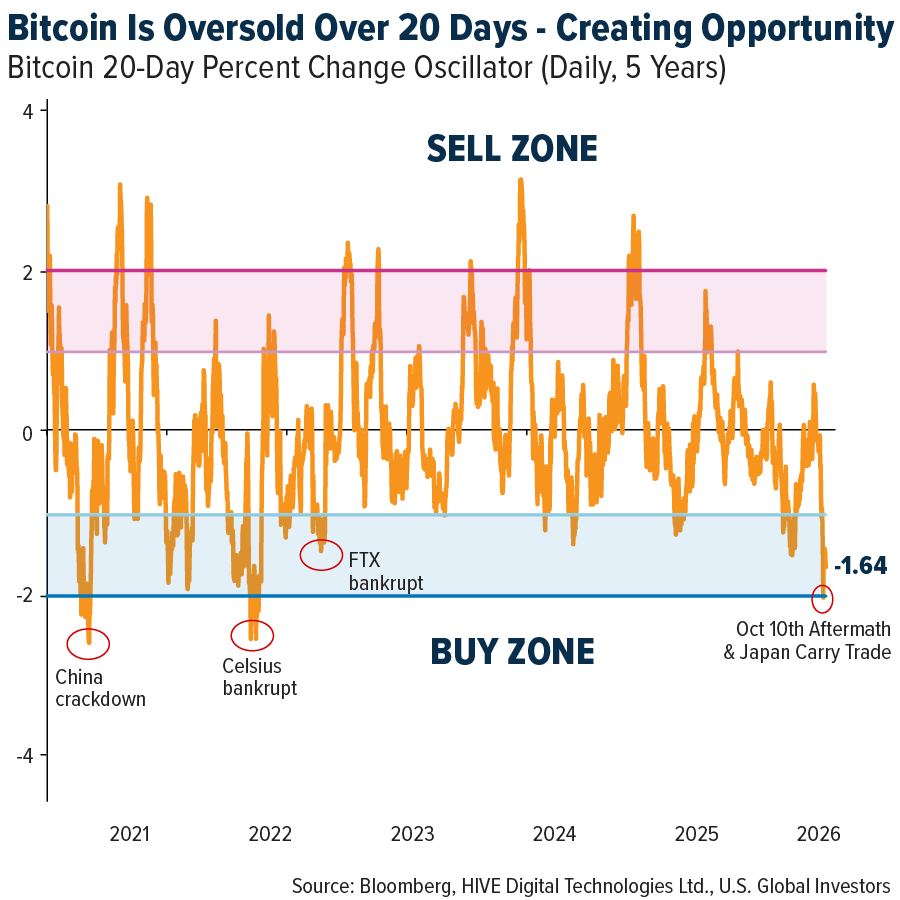

As I told Consolidation Station this week, from a technical standpoint, Bitcoin is now roughly two standard deviations below its 20-day trading norm. This is a level we’ve seen only three times in the past five years. Historically, such extremes have favored short-term bounces over the subsequent 20 trading days.

The Japanese carry trade unwind—estimated at around $500 billion—likely exacerbated the weakness we saw in January and this month, but I believe that pressure is largely behind us now.

Now, with Bitcoin still trading under $70,000—down 45% from its all-time high—some investors might be wondering if October 10 is the reason this weakness has persisted.

The short answer is yes. But the full story is more nuanced and, I think, my important for your portfolio decisions going forward.

What Actually Happened

To put things in perspective, the 10/10 crash was larger than the FTX meltdown in absolute dollar terms. Think about that. It dwarfed the collapse of what was then the second-largest crypto exchange. Binance alone had to tap its insurance fund for $188 million to cover bad debt. Several other exchanges faced similar pressures.

The immediate trigger? Many believe it was President Donald Trump’s announcement of a 100% tariff on Chinese imports, stacked on top of the existing 30% tariff.

That geopolitical shock spooked markets broadly, but crypto’s highly leveraged structure turned what should have been a correction into a full-blown massacre.

The crash exposed fundamental structural weaknesses in how exchanges were managing risk, and one platform in particular might bear significant responsibility.

The Binance Factor

Star Xu, the founder and CEO of OKX, recently took to X with a detailed explanation of how he understands the 10/10 event unfolded.

According to Xu, Binance launched an aggressive user-acquisition campaign offering 12% annual percentage yield (APY) on USDe, a synthetic dollar on the Ethereum network. At the same time, Binance was allowing USDe to be used as collateral with the same treatment as established stablecoins like USDT and USDC.

What Binance created, Xu says, was a dangerous incentive structure. Users were encouraged to convert USDT and USDC into USDe to earn attractive yields, not realizing it was a much riskier asset.

Then came the leverage loop. Sophisticated users figured out they could covert USDT into USDe, use that USDe as collateral to borrow more USDT and convert that borrowed USDT back into USDe Wash, rinse, repeat. According to Xu, APYs artificially rose as high as 24%, 36% and even 70%+.

When volatility hit, USDe depegged quickly, and cascading liquidations followed. The sell-off triggered a classic doom loop where forced selling led to more margin calls, which led to more forced selling.

To be fair, Binance claims no responsibility. Speaking at a crypto event this week, the firm’s co-CEO, Richard Teng, placed the blame solely at Trump’s feet. All I know is that when you allow highly leveraged contracts in an environment where stop-losses can be exploited and risk controls are inadequate, you’re building a powder keg. All it takes is a spark.

The Psychological Damage

October 10 wiped out more than just positions. It wiped out confidence. The event marked the top of Bitcoin’s move near $126,000 and triggered fear among investors that we’re still working through today.

We saw significant ETF redemptions in the weeks that followed. Retail investors who had piled into futures and margin loans as Bitcoin hit all-time highs earlier that week were the first casualties. Over 1.6 million individual accounts were liquidated, a vast number of them small players.

The subsequent sell-off this month, which delivered Bitcoin’s largest realized loss in history as prices fell from $70,000 to $60,000, was characterized by one analyst as a “textbook capitulation event.” It occurred rapidly, on heavy volume, and crystallized losses from the lowest-conviction holders.

Why I Remain Bullish

Despite the ongoing market jitters, I remain bullish in the long term because the fundamentals still look strong.

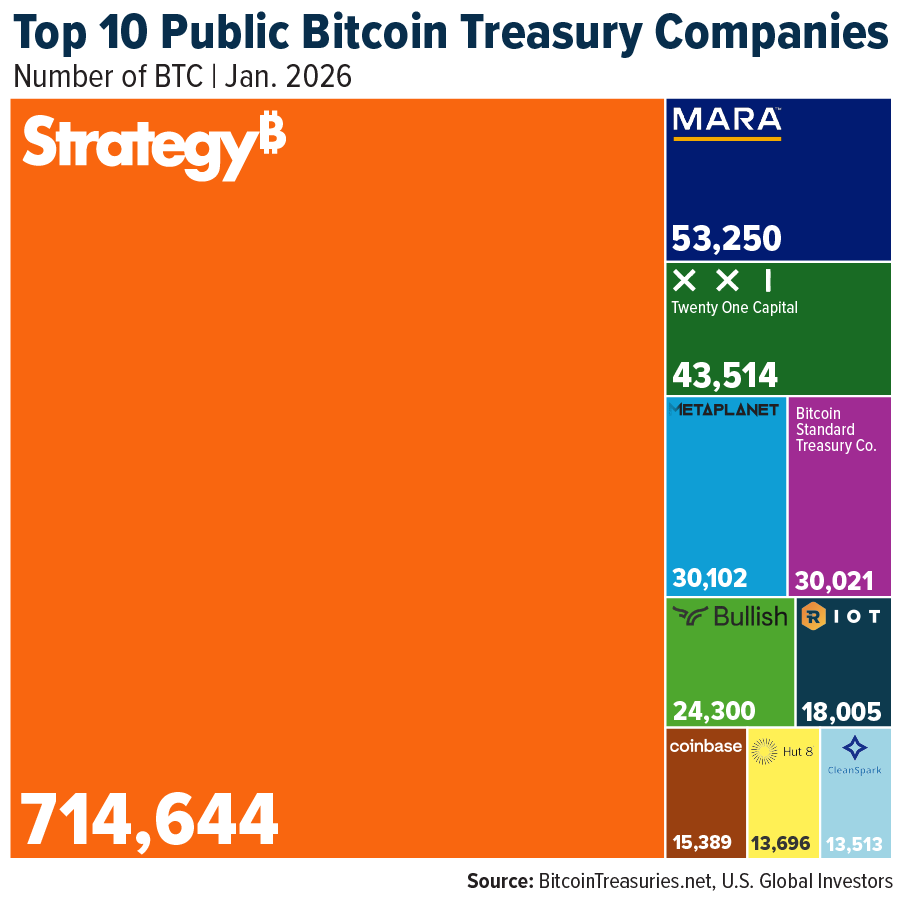

Institutional adoption has accelerated. Corporate Bitcoin treasuries—what we call Digital Asset Treasury (DAT) companies—now hold more than 1.1 million BTC, representing 5.7% of total supply and valued at roughly $90 billion. Strategy (formerly MicroStrategy) alone has built a position amounting to 3.5% of total Bitcoin supply. In January, institutions added approximately 43,000 Bitcoin to their portfolios despite the challenging price environment.

The U.S. Strategic Bitcoin Reserve now holds over 325,000 BTC, the most in the world at 1.6% of total supply. Nation-states are accumulating, as they are with gold. Major corporations are accumulating.

The Bottom Line

I’ve often called Bitcoin “digital gold,” but I don’t think it’s fully matured yet as a true safe-haven asset. Institutions still treat it as risk-on, not risk-off. That tells me it’s still finding its role in institutional portfolios.

Was October 10 the reason Bitcoin’s weakness has persisted? I believe yes. The crash was a major structural shock that wiped out leveraged positions and forced necessary, but painful, deleveraging across the digital asset ecosystem.

Did irresponsible marketing campaigns by certain platforms contribute to the crash? Again, I believe yes. When you incentivize users to treat a tokenized hedge fund like a stablecoin and then allow unlimited leverage on top of that, risk is amplified.

As massive as the crash was, it may have been necessary medicine. Sometimes excess leverage needs to be flushed from the system before the next move higher can begin. I believe we’re in the last stages of that process.

Watch my interview with Consolidation Station:

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Airports of Thailand, up 10.4%. According to Raymond James, Elliott Management reduced its combined economic exposure/voting share from 13.1%/9.9% in the mid-December filing to 10.7%/9.0%, with sales in the low-$40s.

- According to JP Morgan, Hapag-Lloyd reported preliminary fourth quarter 2025 results today, which came in well ahead of consensus, with Group EBITDA of $0.8B (versus Bloomberg consensus of $0.5B) and EBIT of $0.2B (versus Bloomberg consensus of -$230MM), driven by container volumes up 5% year-over-year (YoY), while unit freight rates declined 6% quarter-to-quarter.

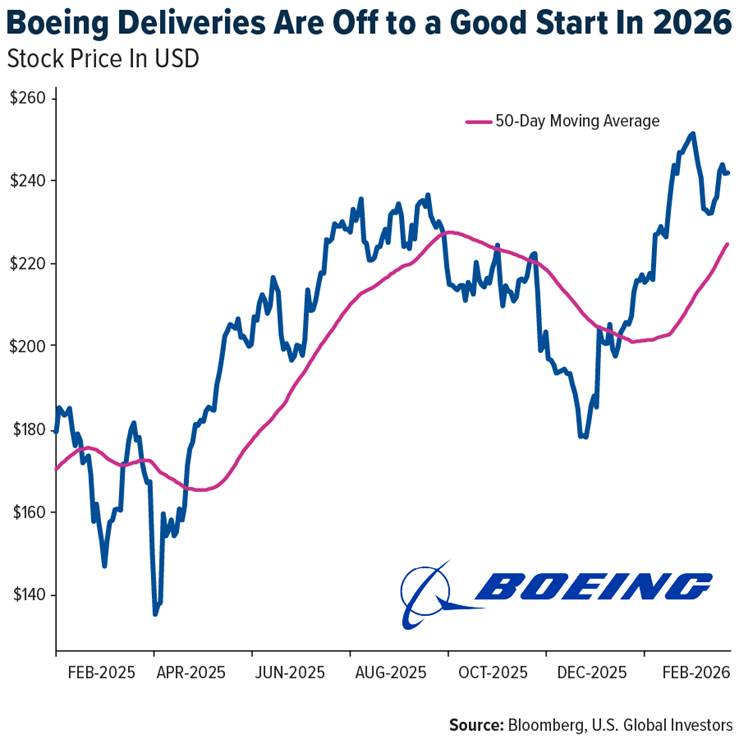

- Boeing delivered 46 aircraft in January, a positive start to the year in RBC’s view. The company delivered 37 MAX aircraft, one 767, three 777s, and five 787s during the month. The 46 aircraft deliveries were up 2% from January 2025. RBC views the company’s 37 MAX deliveries as sustaining positive momentum and maintaining a production rate of 42 per month throughout the first half of 2026.

Weaknesses

- The worst-performing airline stock for the week was Tripadvisor, down 24.9%. According to UBS, active job listings for the air transportation sector are down 9% year-over-year (YoY) on average for January 2026 versus last year. Active job listings for flight attendants have recently surged to match post-COVID highs, while pilot job postings showed a pullback in January.

- UBS notes further softening in container spot freight rates, as the pre–Lunar New Year rush appears to be ending. The overall Shanghai Containerized Freight Index (SCFI) spot box freight index fell an additional 4% this week to its lowest level since mid-October and is down 24% from the late-December high.

- RBC views Air Canada’s suspension of Cuba service as neutral to sentiment, despite the 4% move in the shares following the announcement. Based on published schedules, Cuba represented 0.3% of total capacity at Air Canada for February.

Opportunities

- Morgan Stanley expects a 1–2 point improvement per year in Chinese load factors, implying greater pricing power for airlines. The firm remains bullish on Chinese airlines’ multi-year, supply-driven upcycle and sees margin upside if pricing performance is stronger than expected. It expects largely flat passenger yields in 2026, followed by 3–4% price increases in 2027.

- FedEx announced plans to acquire a 37% stake in InPost for approximately $2.6B, according to BMO. BMO understands the industrial logic, noting that outsourcing a greater share of last-mile business-to-consumer volumes in Europe could improve the segment’s economics.

- Southwest issued a press release announcing that the company will install Starlink’s Wi-Fi offering across its fleet. The first aircraft equipped with the service will enter service this summer. The company expects more than 300 aircraft to be equipped by year-end 2026, according to TD.

Threats

- Tripadvisor management indicates that first quarter revenue should be down 3-5%. Experiences should be up in the low teens and the Fork should be up 20%. However, hotels should be down 23%. EBITDA margins should be down at Experiences and Hotels.

- Sea-Intelligence’s 2026 outlook suggests volume growth may struggle to absorb new vessel capacity, potentially putting renewed pressure on freight rates. The firm notes that projected trade growth is heavily reliant on the technology sector, masking weaker underlying demand for volume-dense goods.

- Lufthansa Germany pilots are set to strike this Thursday following several rounds of failed pension negotiations. The level of cancellations remains unclear, but Lufthansa expects “extensive” disruptions across its network. Based on historical precedent, BMO estimates a €10–30MM daily impact from the strikes.

Luxury Goods and International Markets

Strengths

- The hotel sector showed clear strength this week, with major operators reporting better-than-expected results. Marriott, Hilton, Hyatt, and Melco Resorts all beat earnings-per-share expectations, reflecting resilient demand and strong pricing power, especially at the high end of the market.

- Ferrari reported solid results, highlighting continued strength in the ultra-luxury segment. Revenue and earnings growth were supported by robust demand, disciplined pricing, and a well-controlled order book.

- Shiseido, the Japanese cosmetics maker and distributor, was the best-performing stock in the S&P Global Luxury index over the past five days, rising 19.9%. Shares jumped after better-than-expected earnings and signs of improving demand, particularly in domestic and Asian markets.

Weaknesses

- L’Oréal reported weaker-than-expected revenue growth, mainly due to softer sales in China, a key market for the company. Lower-than-anticipated demand in the region raised concerns about near-term growth in the luxury and beauty sector, causing L’Oréal shares to sell off over the past five days.

- Financial stocks were the weakest performers in the S&P 500 as investors worried about slowing loan growth, tighter profit margins, and interest-rate uncertainty. Concerns over the economic outlook and potential credit losses also weighed on bank and financial sector shares.

- RealReal, the online luxury retail platform, was the worst-performing stock in the S&P Global Luxury index over the past five days, down 17.8%. Shares fell after weaker-than-expected results raised concerns about profitability and near-term demand.

Opportunities

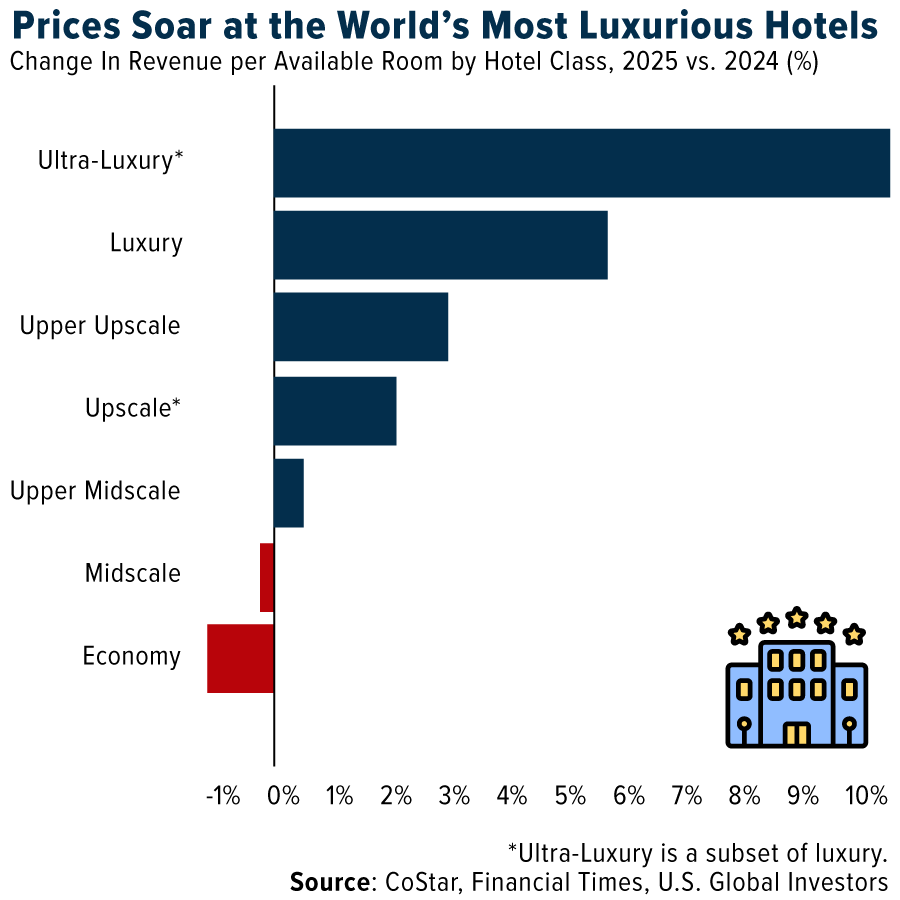

- Ultra-luxury hotels continued to thrive last year, defying the broader luxury slowdown as wealthy travelers paid record prices for exclusive amenities like hyperbaric oxygen therapy and sound baths. Revenue per available room at these properties rose 10.6%, more than three times the growth of the wider hotel industry, according to CoStar data shared with the FT. Average daily rates reached a record $1,245, up over 8%.

- Hermès reported strong results, showing continued momentum in the luxury sector. Revenue and cash flow grew across all regions, supported by resilient demand and strong brand pricing power, with the Middle East as the top-performing market.

- Kering beat expectations with fourth-quarter revenue of about €3.9 billion, down only 3%, driven by a smaller-than-expected decline at Gucci. Shares rose on signs of stabilization and potential turnaround under new leadership.

Threats

- Mercedes-Benz was weak this week after reporting a sales decline, largely due to softer demand in China. The company also highlighted intensifying competition and potential tariff risks, which are weighing on volumes and margins and raising concerns about near-term growth, especially in key international markets.

- Several companies reporting fourth-quarter results noted softening demand in China, a key growth driver for many luxury brands. Weaker-than-expected traffic and sales in Greater China pressured share prices and raised concerns about near-term growth.

- Key U.S. economic figures, including GDP and consumer sentiment, will be released next Friday. Weaker-than-expected readings could signal slowing momentum and softer consumer confidence, potentially pressuring consumer discretionary and luxury stocks.

Energy and Natural Resources

Strengths

- Uranium showed continued strength this week and led commodities with a gain of about 3.49%. Cameco Corp. posted fourth-quarter revenue, but earnings per share (EPS) was below consensus. The results reinforce the tight supply backdrop where Cameco lowered their 2026 production guidance by 7%. The physical market for uranium, where utilities are competing for long-term material amid thinning secondary supplies and limited near-term production growth remains tight.

- Arabica coffee rose about 3% this week — its first weekly gain in a month — as lower prices sparked renewed buying and hedging activity, signaling resilient global demand often viewed as a barometer of consumer and trade strength. The rebound, despite expectations of a large Brazilian crop, suggests firm underlying consumption and improving free-trade flows as roasters lock in supplies amid tightening inventories Bloomberg cites.

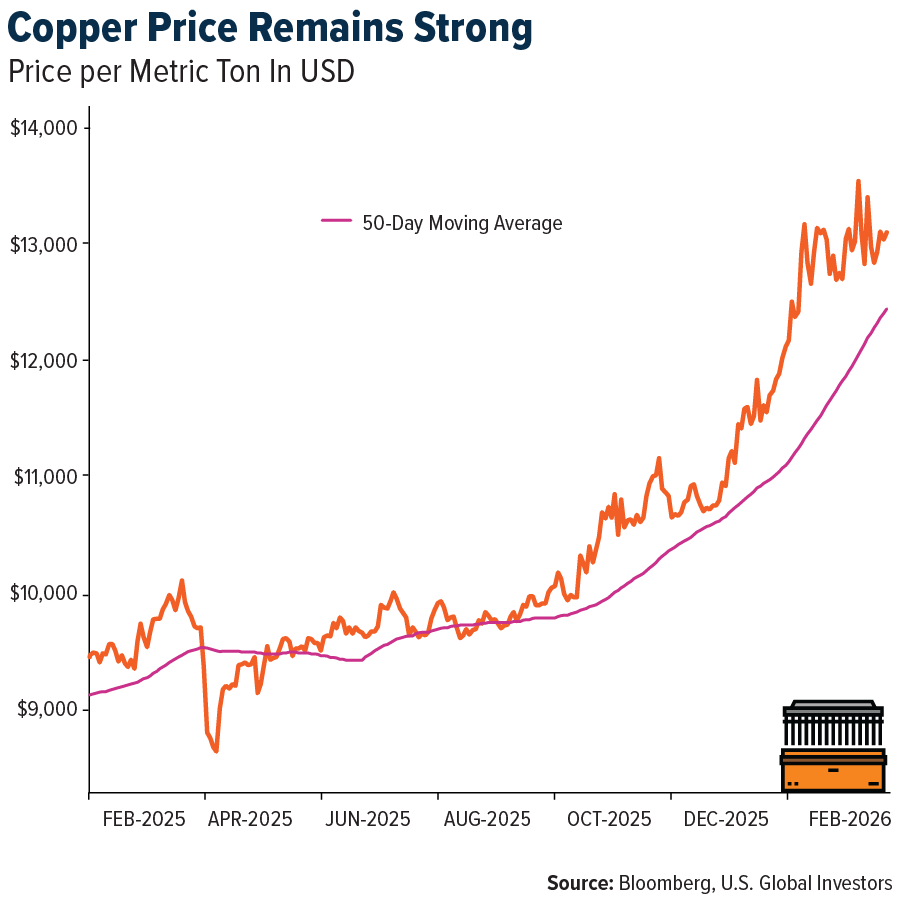

- Copper remained a relatively bright spot this week, with only a modest pullback that does little to disrupt its longer-term uptrend supported by structural demand from electrification and energy transition investment. Even as the Democratic Republic of Congo lifted exports nearly 10% in 2025 to 3.4 million tons — reinforcing global supply growth — the market continues to reflect tight medium-term fundamentals and durable consumption strength.

Weaknesses

- Natural gas was the weakest performing commodity of the week again, continuing from last week’s selloff, declining approximately 5.87%. BlueCrest Capital Management’s senior natural gas trader Alex Watson and several analysts have departed after losses tied to UK–European March gas spread positions amid extreme price swings, according to people familiar with the matter. The volatility — fueled by freezing northern hemisphere weather and surging heating demand that more than doubled implied volatility in Europe’s benchmark gas futures since early 2026 — has compounded a difficult start to the year for hedge funds.

- Iron ore weakness this week highlights pressure on the US dollar as commodity-linked flows retreat, with futures dropping below CNY 770 per ton to a seven-week low amid rising supply and seasonally soft demand ahead of China’s Lunar New Year. Near-record port inventories and continued stockpile builds at steel mills, combined with paused furnace operations for maintenance, underscore near-term demand challenges and add to the dollar’s pressure in commodity markets.

- The U.S. coal fleet’s surge in generation during Winter Storm Fern—burning 10% more coal than expected—exposed vulnerabilities in the grid during periods of peak demand, highlighting how extreme weather and fuel-price volatility can strain electricity supply. The episode foreshadows potential stress on the system if data centers and other high-demand loads continue to be added to the grid without sufficient resilience measures according to the Energy Information Administration (EIA).

Opportunities

- UBS analysts predict 2026 will be a breakthrough year for energy storage system installations, citing growing importance for grid stability after recent outages in Spain and London’s Heathrow Airport. The firm identifies Contemporary Amperex Technology, LG Energy Solution and Samsung SDI as market leaders best positioned to benefit from increased government funding and advancing battery technologies, signaling accelerating demand for critical grid infrastructure.

- Octopus Australia’s $14 billion plan to expand wind, solar and battery projects over the next five years, alongside Cnooc’s 40% increase in offshore wind capacity in China this year, highlights a global surge in clean energy investment. These initiatives not only accelerate the transition away from fossil fuels but also support ambitious national targets—Australia’s goal of 82% green electricity by 2030 and China’s push to double combined wind and solar capacity by 2035—while attracting both domestic and international capital into the sector Bloomberg reports.

- China plans to increase electricity trade to 70% of total consumption by 2030 as part of a unified power market strategy, up from 64% in 2025 when power trade reached 6.6 trillion kilowatt hours. The government aims to expand regional spot trading to 4% of transactions by 2027 to overcome transmission bottlenecks hindering renewable energy penetration, while relaxing price controls to allow large industrial and commercial users to buy power directly from all sources including renewables, creating substantial opportunities for power trading infrastructure and renewable energy integration.

Threats

- Tongaat Hulett Ltd., the 134-year-old South African sugar producer, faces an immediate threat to its survival as administrators prepare to place the company into provisional liquidation following the collapse of its rescue plan with Vision Group. With Vision demanding repayment of 11.7 billion rand in debt and aiming to seize pledged assets, the company’s solvency is at risk, endangering thousands of jobs and regional sugar production Bloomberg writes.

- UK aluminum futures retreated toward $3,100 per tonne after hitting a three-year high of $3,270 on January 28, as traders trimmed speculative positions despite constrained global supply. Output growth remains limited following China’s 45-million-ton cap and ongoing smelter disruptions in countries including Iceland, Mozambique and Australia.

- Oil is heading for its first back-to-back weekly loss of the year, pressured by expectations that OPEC+ could resume output increases in April and by the prospect of progress in US-Iran nuclear talks that may ease supply risks (Bloomberg). The renewed downside momentum, alongside broader market weakness and forecasts for global supply to outpace demand, poses a near-term threat to crude prices despite lingering geopolitical tensions Bloomberg reports

Bitcoin and Digital Assets

Strengths

- The UK Treasury’s partnership with HSBC’s Orion platform marks a significant technological advancement in modernizing sovereign debt markets. By leveraging a proven blockchain infrastructure that has already handled more than $3.5 billion in issuances, the DIGIT project ensures high credibility and technical reliability. This move establishes a strong foundation for faster, cheaper, and more efficient bond settlement.

- Asia is demonstrating operational leadership by leapfrogging Western markets in the real-world application of blockchain technology. While the West focuses on institutional exchange-traded funds (ETFs), Asian hubs such as Hong Kong and South Korea are driving mass-market adoption through high-frequency retail use, evidenced by Lotte Group’s 5 million on-chain vouchers and efficient cross-border stablecoin payments for small and medium-sized enterprises (SMEs). This pragmatic approach, supported by proactive regulation in the United Arab Emirates (UAE) and Hong Kong (HK), cements Asia’s position as a leader in integrating digital assets into the global economy.

- The recent accumulation of 53,000 BTC by “whale” wallets represents a key structural support amid broader market volatility. This approximately $4 billion in institutional absorption effectively shifts supply from short-term retail sellers to high-conviction, long-term holders. By absorbing significant sell-side pressure and stabilizing prices near the $70,000 mark, these large-scale participants signal institutional confidence in Bitcoin’s fundamental value, even during periods of market stress.

Weaknesses

- Standard Chartered cut its 2026 Bitcoin price target to $100,000 from $150,000 (previously reduced from $300,000), citing weaker sentiment and demand, and warned prices could fall toward $50,000. Bitcoin is down more than 40% from its $127,000 peak, with roughly $8 billion in U.S. spot ETF outflows and holdings down 100,000 BTC since October.

- The “Ghost Bitcoin” incident at Bithumb, South Korea’s second largest exchange, represents a significant weakness for the industry. A manual entry error that mistakenly credited $40 billion in nonexistent Bitcoin to users highlights a systemic lack of automated safeguards and multi-level approvals. This failure in internal ledger management allowed the trading of ghost assets far exceeding actual reserves, triggering a 17% local price crash and exposing the operational fragility of centralized digital asset platforms.

- JPMorgan’s 27% price target cut on Coinbase, from $399 to $290, underscores the exchange’s high sensitivity to market cycles. Lower crypto trading volumes and declining USDC growth are expected to drive a year over year revenue decline, highlighting the firm’s vulnerability in weaker operating environments and the ongoing challenge of diversifying revenue away from volatile retail transaction fees.

Opportunities

- The European Parliament’s support for a dual online and offline digital euro strengthens EU monetary sovereignty and reduces reliance on non-EU payment firms. This legislative progress creates a significant opportunity for market integration and digital asset resilience. If finalized, this framework will modernize the single market’s payment infrastructure by 2029.

- At Consensus Hong Kong 2026, the Chairman of the Pakistan Virtual Assets Regulatory Authority (PVARA) announced the country’s transition from a gray market to a formal Strategic Bitcoin Reserve. The initiative uses surplus electricity for Bitcoin mining and AI data centers, converting unused energy into productive capacity while providing a regulated financial system for 100 million unbanked citizens.

- Intercontinental Exchange (ICE), parent company of the NYSE, launched the Polymarket Signals tool in partnership with Polymarket, the leading decentralized prediction platform. The $2 billion investment, valuing Polymarket at $9 billion, allows institutional firms to integrate decentralized market data into professional risk modeling and global alpha strategies.

Threats

- The recent legislative impasse at the White House threatens the U.S. digital asset market. On February 10, major banks, including JPMorgan and Goldman Sachs, pushed to ban yields or rewards on stablecoins, stalling the CLARITY Act and maintaining regulatory uncertainty that discourages long-term institutional capital.

- A new cybersecurity threat emerged this week as the FBI and CISA issued an emergency alert on February 10 regarding “Zardoor,” a sophisticated malware targeting institutional digital asset custodians. This backdoor allows unauthorized access to private key infrastructure, forcing institutions to increase security spending and maintaining a high-risk profile for digital asset custody.

- The American Bankers Association (ABA) is pushing the OCC to freeze new national trust bank charters. In a February 11 letter, the ABA argued that approvals for firms like Ripple, BitGo, and Paxos should be delayed until the GENIUS Act is fully implemented, restricting use of the word “Bank” and limiting stablecoin rewards to preserve traditional bank monopolies.

Defense and Cybersecurity

Strengths

- Cloud and hyperscale capital expenditure is set to remain strong in 2026, with memory and storage emerging as key drivers alongside compute, as pricing for DRAM, HBM, and enterprise storage accounts for a growing share of total data center costs. This shift directly benefits memory and storage leaders such as Micron, SanDisk, Western Digital, and Seagate, positioning them at the center of the AI infrastructure build-out rather than at its edge.

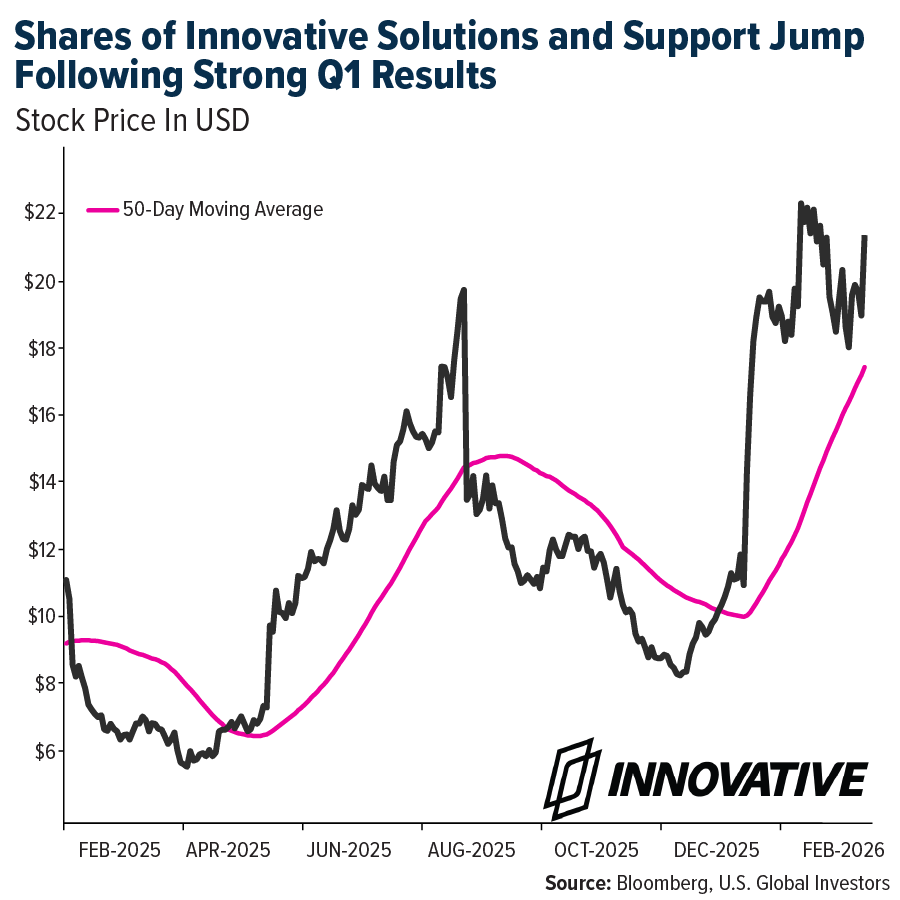

- Innovative Solutions and Support shares jumped after the company reported strong first-quarter results that exceeded expectations. Revenue rose 36.5% year over year to $21.8 million, while adjusted earnings increased to $0.25 per share from $0.09 a year earlier. Adjusted EBITDA grew 141%, and free cash flow increased more than fourfold, highlighting operating leverage and margin improvement. The stock rose about 14% following the report, reaching a new 52-week high.

- The best performing stock this week was Howmet Aerospace Inc., rising 11.58% after fourth‑quarter revenue increased about 15% year-over-year to $2.17 billion and adjusted EPS jumped to $1.05 from $0.74. Both results exceeded expectations, alongside stronger-than-expected 2026 guidance.

Weaknesses

- Alphabet expanded its bond offering to $20 billion amid overwhelming demand and announced plans to tap the sterling and Swiss franc markets to diversify its funding base. As part of this global issuance, the company is preparing a rare 100-year sterling bond, the first such move by a tech firm since the late 1990s.

- Palo Alto Networks disclosed a critical vulnerability in the PAN-OS firewall’s Advanced DNS Security feature that could allow unauthenticated attackers to trigger endless reboot loops, urging customers to upgrade immediately to fixed releases.

- The weakest stock this week was Karman Holdings Inc., declining 20.5% after investors took profits and reassessed the stock’s stretched valuation. Concerns lingered that earnings execution may not fully justify expectations following a sharp rally.

Opportunities

- The U.S. Department of Energy has decided not to restrict American companies’ access to Nvidia’s advanced AI chips, preserving Microsoft’s ability to scale state-of-the-art accelerator infrastructure.

- RTX’s BBN Technologies secured a significant contract from the US Department of Defense to lead the Advanced Spectrum Coexistence Demonstration program, enhancing its role in electromagnetic-spectrum operations by developing a smart spectrum manager for military and commercial use.

- Apollo Global Management finalized a $3.4 billion loan to purchase Nvidia AI chips that will be leased to xAI following its merger with SpaceX. This marks Apollo’s second major chip-leasing vehicle for xAI and highlights Wall Street’s interest in Nvidia-based AI infrastructure.

Threats

- Hackers exploited vulnerabilities in SolarWinds Web Help Desk to gain unauthorized remote code execution access in a recent campaign targeting at least three organizations.

- Cloud and hyperscale capital expenditure in 2026 increasingly highlights a risk for AI compute names, as rising memory and storage pricing consumes a larger share of data center budgets, leaving less room for incremental GPU and accelerator spending. As DRAM, HBM, and enterprise storage gain pricing power, the economics shift away from pure compute vendors, potentially pressuring volumes, returns, and long-term pricing leverage for AI-focused hardware names.

- The Trump administration has deployed a second U.S. aircraft carrier to the Middle East, escalating pressure on Iran and raising the risk of a direct military confrontation. Any disruption in the region could immediately impact energy flows, shipping routes, and defense posturing, forcing markets to reprice geopolitical risk.

Gold Market

This week gold futures closed at $5,035.00, up $55.20 per ounce, or 1.11%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.88%. The S&P/TSX Venture Index came in off 1.82%. The U.S. Trade-Weighted Dollar fell 0.81%.

Strengths

- The best performing precious metal for the week was gold, up 1.11%. Despite a sharp selloff on Thursday, gold still finished the week higher, reclaiming the $5,000 level as cooler U.S. inflation data lifted expectations for Federal Reserve rate cuts and pressured Treasury yields lower. The rebound highlights resilient underlying demand for bullion, with easing rate expectations continuing to support the metal even after January’s volatility according to Bloomberg.

- China continued to purchase gold for its official reserves to hedge geopolitical and U.S. dollar risks, the official securities newspapers report. China central bank’s small-scale gold purchases through several months help with asset diversification while cushioning volatile price moves in gold, Securities Times reports, citing Pang Ming, Distinguished Research Fellow at National Institution for Finance and Development. The purchases will continue, Pang says.

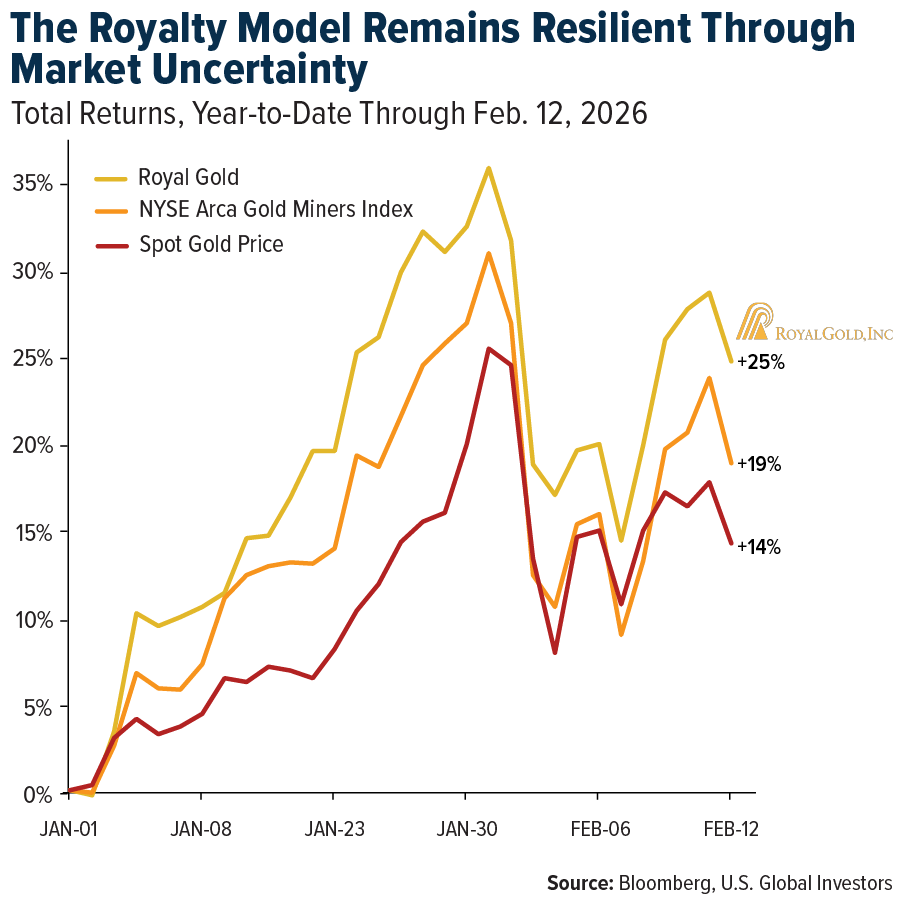

- Royal Gold (RGLD) showed notable strength this week despite heightened volatility in gold prices, as investors positioned ahead of the company’s February 18 earnings report with expectations running high following its transformational October 2025 acquisitions. CIBC’s bullish $330 price target—raised from $250 on February 4—reflects optimism that the expanded portfolio from the Sandstorm Gold and Horizon Copper deals will deliver accelerated growth in gold equivalent ounces (GEOs), with the capital-light royalty model providing defensive cash flow generation even during commodity price turbulence.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.62%. Palladium faced renewed downside risk this week after the Commerce Department backed preliminary anti-dumping duties of nearly 133% on Russian imports, escalating trade uncertainty in a market already grappling with volatile demand. While intended to support domestic producers, the move adds pricing instability and highlights palladium’s vulnerability to geopolitical shocks and uneven automotive-sector consumption Bloomberg reports.

- Ten silver miners working for Vizsla Silver were found dead in a Mexican mass grave after being kidnapped on January 23 from a mining project near Concordia in Sinaloa state—a cartel-controlled area—with media reporting that as many as 2,000 military personnel have been deployed to the region with heightened security measures in response to the tragedy. The incident underscores the severe security risks facing Mexican mining operations in high-risk jurisdictions, hopefully the security response by the government will bring some stability to the region.

- Titan Co., India’s top jewelry maker, sees shoppers turning cautious as record-high gold prices weighed on demand in the world’s second-largest bullion market. Sales growth is being driven more by price increases than by volume, with customer growth remaining “muted,” Chief Financial Officer Ashok Kumar Sonthalia told Bloomberg TV on Wednesday.

Opportunities

- According to BMO, Franco Nevada is providing $250 million in royalty financing to i-80 Gold in exchange for a 1.5% LOM NSR royalty across i-80’s Nevada portfolio, increasing to 3.0% in 2031. The transaction supports i-80’s recapitalization and phased redevelopment plan and secures Franco’s position on prime Nevada “gold” real estate.

- Stifel believes underlying gold fundamentals are supported by four themes: (1) monetary easing cycles; (2) strategic central bank accumulation; (3) increasing institutional asset allocation; and (4) gold’s role as an essential hedge against fragmentation in regional economic and financial markets and as a necessary defensive hedge against “Big Tech” cyclical growth exposure in 2026.

- Stifel notes that, unlike previous cycles when pro-cyclical behavior was defined by aggressive and dilutive mergers and acquisitions (M&A), pursuit of marginal internal rate of return (IRR) projects and vast underestimation of the fluidity of unit operating costs, sustaining capital requirements and capital intensity of new projects, which effectively neutralized the benefits of a rising gold price, the current environment reveals a gold sector prioritizing margins and return on invested capital (ROIC) over production growth.

Threats

- Cost drift has been a feature in recent gold markets, with producers increasingly chasing incremental, lower-margin material and production growth albeit at higher unit costs. With margins overall remaining strong given elevated gold prices, the sector appears steadfastly focused on growth with cost control a lower priority, according to UBS.

- Indian module manufacturers who rely on Chinese solar cells are facing difficulties as prices from China continue to rise. Unstable silver prices, along with the upcoming Chinese New Year holiday, are causing suppliers to either hesitate in providing quotes or demand higher rates. As a result, module makers and solar developers may need to postpone projects or temporarily shut down their plants until costs decrease.

- Newmont, a partner with Barrick in its most important mines, wants the Canadian company to improve the operations before it spins off the assets and believes it has the power to potentially block the initial public offering, according to people familiar with the matter. Barrick last week announced plans to sell 10% to 15% of those operations through a late-2026 IPO, according to Bloomberg.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2025):

Marriott

Hilton

Ferrari

L’Oreal

The Real Real

Hermes

Kering

Mercedes-Benz

Boeing

Air Canada

FedEx Corp

InPost

Southwest Airlines

Deutsche Lufthansa

Micron Technology

Western Digital Corp.

Seagate Technology

Innovative Solutions and Support

RTX Corp.

Cameco Corp.

Royal Gold Inc.

Vizsla Royalties Corp.

Franco-Nevada Corp.

Newmont Corp.

Barrick Mining Corp.

Airports of Thailand PCL

TripAdvisor Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Standard deviation is a statistical measure of the amount of variation or dispersion in a set of data values, indicating how far, on average, the data points spread from their mean.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All