Not long ago, CLO ETFs were niche vehicles only talked about at credit conferences and in sophisticated bond manager circles. But fast forward to 2026, and they’ve entered the mainstream – drawing meaningful interest from both institutions and retail investors.

The numbers tell the story. CLO ETFs have attracted roughly $4 billion in net inflows in the first six weeks of 2026 alone. As of February, assets have surpassed $35 billion, more than doubling in just over a year. The bulk of these flows has funneled into AAA-rated CLO ETFs.

What’s Driving the Surge?

-

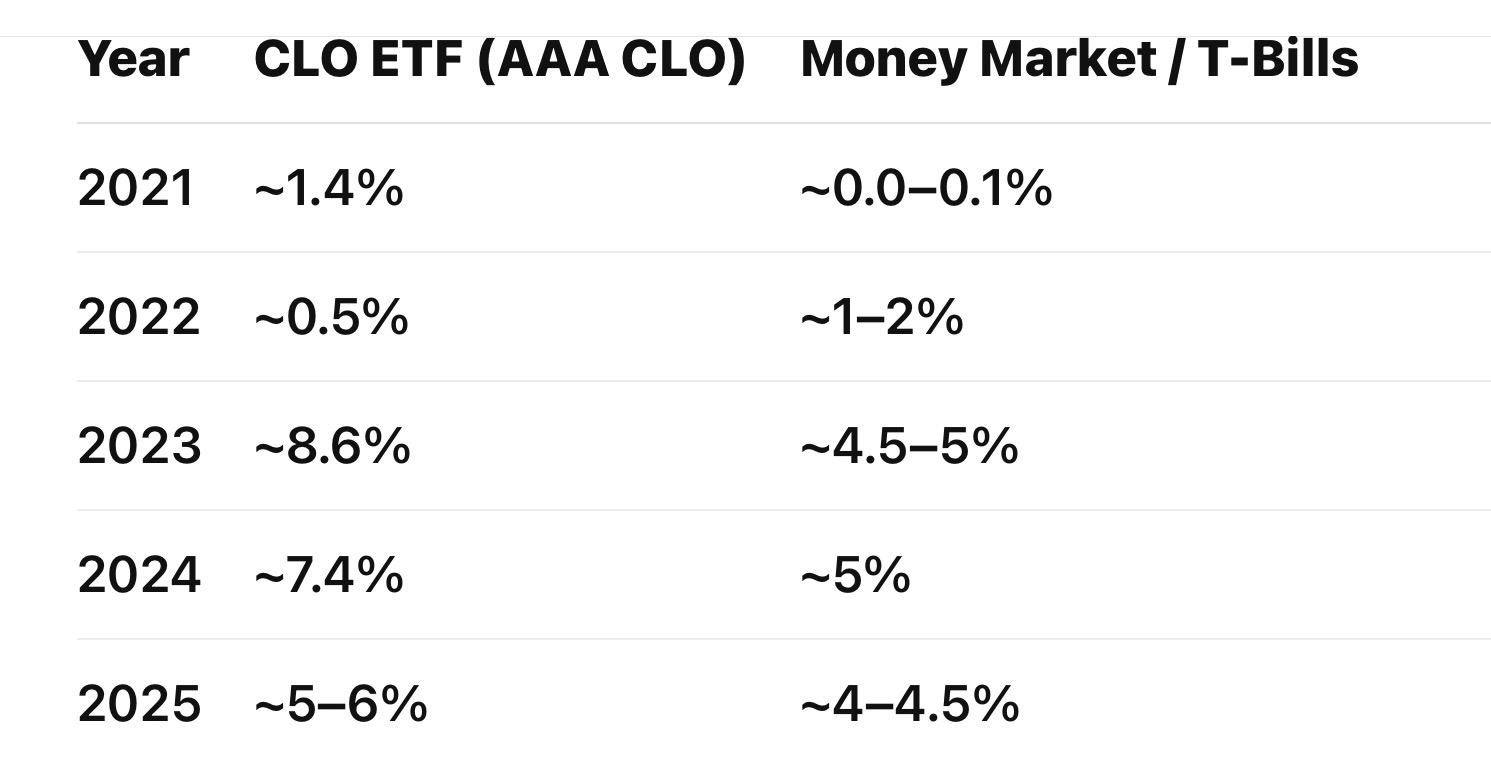

Enticing yields. With money market yields drifting down toward 3%-4%, floating-rate loan exposure has become more compelling. Investment-grade CLO ETFs are currently offering 30-day SEC yields in the closer to 5%-6% – a notable premium over comparable Treasuries.

Source: VettaFi, Barron’s

-

Credit resilience. AAA-rated CLOs have never defaulted in their 30-year history, including through the dot-com crash, the Global Financial Crisis and the COVID-19 pandemic. Historically, while lower-rated tranches have experienced some defaults, loss rates have still been exceedingly low relative to corporate bonds. Leveraged loan default rates also remained near historic lows through late 2024 and early 2025.

-

Strong performance. CLOs have delivered some of the best risk-adjusted returns in fixed income over the past decade. In 2025, investment-grade CLO ETFs posted total returns between 5.7% to 6.3%. Mezzanine-focused ETFs (those holding AA to BBB tranches) often exceeded 7%, as credit spreads tightened and hold near historically tight levels today.

Making Strides in the CLO ETF Space

Despite rapid growth, the CLO ETF market remains concentrated. Janus Henderson dominates the space, with the Janus Henderson AAA CLO ETF (JAAA) alone boasting $27 billion in assets and gathering $2.5 billion in net inflows year-to-date.

Fidelity, which has climbed the ranks as an active management powerhouse, just launched two new active strategies – the Fidelity AAA CLO ETF (FAAA) and the Fidelity CLO ETF (FCLO). To gain traction, Fidelity is waiving management fees for the first 12 months.

FAAA allocates at least 80% to AAA-rated CLOs, while FCLO reaches further down the capital stack, investing in tranches rated BBB+ down to B- in pursuit of higher yield. The launches underscore how quickly CLO ETFs have shifted from a niche allocation to a competitive battleground among major legacy asset managers.

“FAAA and FCLO enhance our ETF lineup, delivering straightforward access to an often complex market — reinforced by Fidelity’s proven investment capabilities and active management experience,” said Robin Foley, Head of Fixed Income at Fidelity Investments.

A Tax-Efficient Twist

Issuers are also differentiating themselves through structure — particularly around tax efficiency and enhanced yield.

Reckoner Capital Management, a newer ETF entrant specializing in alternative credit, recently expanded its lineup with four additional CLO ETFs. The New York-based firm introduced reinvesting and annual distribution versions of its strategies, designed to reduce monthly payouts and defer taxable income.

The Reckoner Yield Enhanced AAA CLO Reinvesting ETF (RAAR) and the Reckoner Yield Enhanced AAA CLO Annual ETF (RAAY) provide leveraged exposure to the senior-most tranches, with net expense ratios of 0.40% and 0.35%, respectively. The structural leveraged aspect of these ETFs may lead to minor price volatility but the senior tranche is still heavily protected. Meanwhile, the Reckoner BBB-B CLO Reinvesting ETF (RCLR) and the Reckoner BBB-B CLO Annual ETF (RCLY) focus primarily on BBB- and BB-rated CLO bonds, charging 0.60% and 0.55%. All four funds aim to minimize monthly payouts to compound value.

John Kim, co-founder and CEO of Reckoner, said the funds should appeal to investors who want exposure without the immediate tax hit of monthly income.

“Our new suite of CLO ETFs is designed to provide investors with a range of options to achieve their investment objectives, whether they are focused on current income or reinvestment,” he said. “These four new funds complement the AAA and BBB-B CLO ETFs that we introduced last year by adding reinvesting optionality for investors who seek compounding value through distribution minimization, as well as annual distribution options for those who prefer a single yearly dividend.”

From Fringe to Fixture

CLO ETFs were once relegated to the fringes of fixed income markets. Today, they are firmly part of the income toolkit. Part of that shift is structural: ETFs have made complex credit exposures easier to access, trade, and scale. But the shift is also behavioral. As investors grew more comfortable with alternative income strategies — and as floating-rate exposure proved valuable in higher-rate environments — CLO ETFs began to look less exotic and more practical. And with spreads near historical tights and assets surging, competition among issuers is intensifying. Fee waivers, structural innovation and differentiated exposure are all signs that the space is entering a more mature phase.

What was once a quiet corner of credit markets is now an arms race — and the battle for assets is only heating up.

For more news, information, and analysis, visit VettaFi | ETFDB.

Originally published on ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi