Investors have long known balance is a key aspect of portfolio design. It presents a chance to achieve long-term growth and protect hard-earned assets at the same time. Investors often debate the appropriate balance between stocks and bonds or whether the 60/40 rule is relevant. Once the decision has been made to devote a portion of the portfolio to bonds, the assessment on how to allocate among fixed income asset classes can sometimes introduce additional questions.

Municipal bonds offer opportunities on the long end of the curve to lock in nominal rates above 4% right now. For investors who are in a high tax bracket, the opportunity on the long end of the municipal curve is clear. However, there are numerous characteristics or investment goals that can make the strategy decision less obvious. For example, a retirement account or those in lower federal tax brackets may benefit from corporate bonds versus municipal bonds. Personal characteristics play a large role in dictating strategy but are not the only critical component.

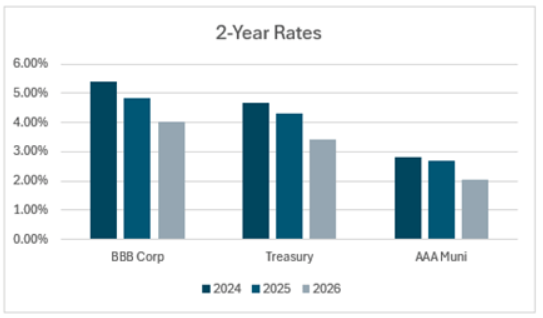

Investment goals can be just as important. A short time horizon is a common investment goal for needs such as a child entering college, a down payment on a home, or an ultra-conservative risk tolerance. These are all different reasons investors may arrive at the same investment decision. Right now, the short end of yield curves across multiple asset classes offers relatively little additional yield, or reward, over Treasuries. The consequences of this affect all investors, regardless of their individual characteristics and tax rates. If liquidity, credit quality and call protection are paramount to a short-term investor, Treasuries may be the most appealing choice. Current rates on the short end mean the highest credit quality option does not sacrifice as much yield as it may have in the past.

Crafting a fixed income strategy may require understanding an investor’s complete tax* situation. Treasuries avoid state income tax, making them more competitive relative to other bonds. This can be an important consideration, especially for those in high income tax states. When an investor is looking to lock-in rates for longer or increase their cash flow, the decision can become more complex. While the decision points are numerous when choosing a fixed income product, your financial advisor along with the Fixed Income Solutions team can assist in balancing investment goals and unique characteristics.

*Raymond James is not a tax advisor and does not give tax advice. Please consult a tax professional prior to making any investment decisions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

J.D. Power 2025 U.S. Investor Satisfaction Study, which measures overall investor satisfaction with investment firms, was released 3/20/25, based on investors surveyed 1/24-12/24, who may be working with a financial advisor. Based on 7,876 responses from Advised Investors, 1 company out of 24 was chosen as the winner. The award is not representative of any one client’s experience, is not an endorsement, and is not indicative of an advisor’s future performance. The study is independently conducted, and the participating firms do not pay to participate. Use of study results in promotional materials is subject to a license fee. J.D. Power is not affiliated with Raymond James. For J.D. Power 2025 award information, visit jdpower.com/awards.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

© 2026 Raymond James Financial, Inc. All rights reserved.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - September 2025 (PDF)

© Raymond James

Read more commentaries by Raymond James