Signal vs. Noise: Markets, Misconceptions, and the Case for Optimization in 2026

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe central theme of 2025 was the disconnect between market sentiment and economic reality. The year began with widespread apprehension regarding aggressive tariffs and forecasts of a recession. Yet, it concluded with global equities at all-time highs and the U.S. economy maintaining consistent growth as the anticipated economic contraction failed to materialize.

The fourth quarter reflected this broad dynamic. Markets focused on economic signals such as corporate earnings, AI productivity, and the trajectory of interest rates while largely overlooking political turbulence. Despite the longest government shutdown in U.S. history and persistent geopolitical volatility, the market demonstrated remarkable resilience. Historically, such a shutdown would have triggered a significant reaction. Instead, the market demonstrated a growing sophistication in distinguishing between political theater and genuine economic impact.

Market relationships have changed. As global policies and growth paths diverge, international markets are no longer moving in lockstep with the U.S. economy. Correlations between traditional asset classes are normalizing to healthier partial independence, and alternative asset classes are moving toward an equilibrium closer to public markets. As we look to 2026, the investment landscape requires optimizing a world where risks are more dispersed, inflation remains structurally higher, and easy sources of return have been exhausted.

Market Analysis: 2025 in Review

In 2025, globally diversified investors were rewarded as global markets gained 22%, the S&P 500 returned 17.8%, international equities outperformed the U.S. by more than 14%, and all major asset classes exceeded cash.

Equities: Market and Factor Divergence

The divergence across investment styles was notable in 2025. While U.S. growth continued to deliver solid returns, value massively outperformed growth in international markets, particularly in Europe and Japan. This supports the investment thesis that value stocks play an important role in a portfolio and that U.S. large-cap growth has been driven by its exposure to technology rather than a fundamental risk premium.

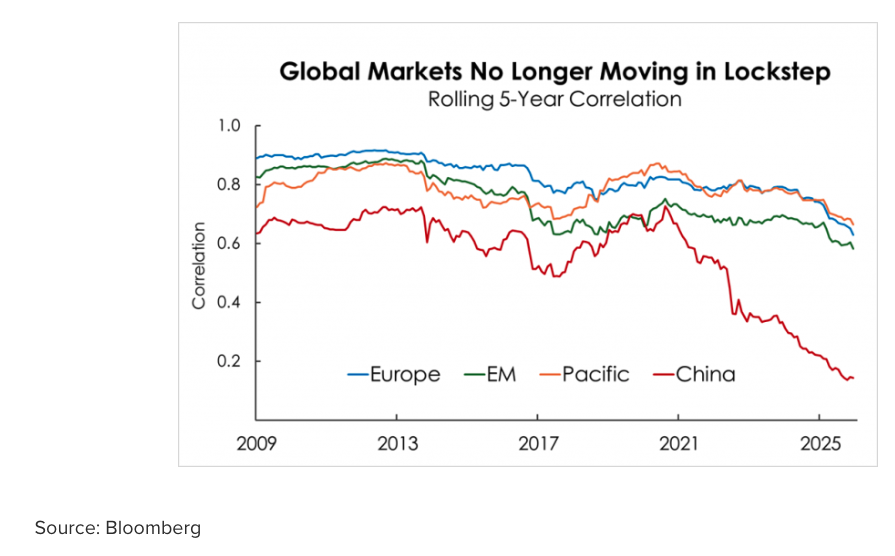

Furthermore, market correlations have shifted. For years, international markets exhibited a high correlation to the U.S., limiting diversification. Recent data shows this has drifted down, with developed markets and China nearer to 0.7 and 0.2 respectively. Both observations support the case for global diversification.

Fixed Income: Yield Curve Normalization

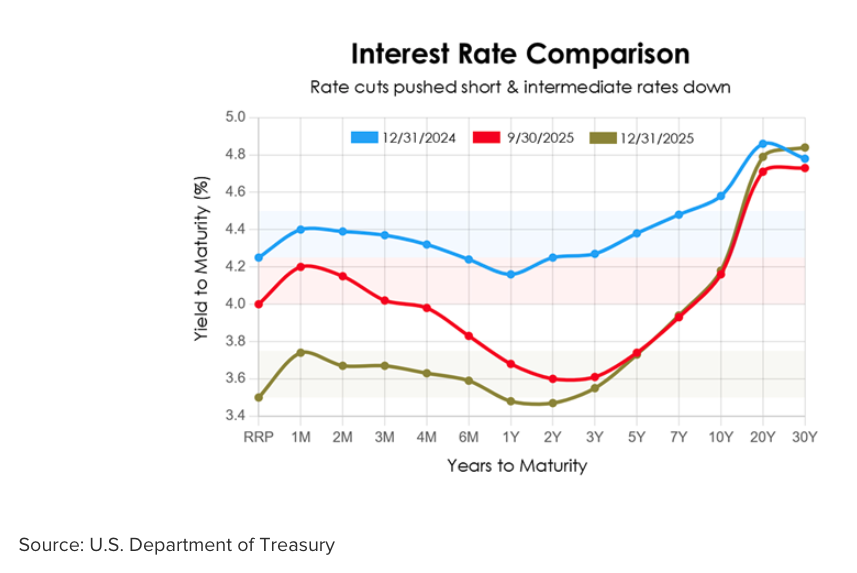

Fixed income markets delivered improved results. The Federal Reserve cut interest rates by 75 basis points in 2025, including two rate cuts in the fourth quarter. The front end of the curve moved down, but fiscal concerns and inflation expectations kept long-term yields from falling, resulting in a steeper curve. The 2-year Treasury yield fell 78 basis points year-over-year, while the 10-year yield ended at 4.18%, down 40 basis points.

The U.S. Aggregate Bond Index returned approximately 7%, finally outperforming cash (4%). International treasuries had comparable returns, but by very different means – declining in local terms as some regions hiked while the U.S. cut, but gaining far more from the weaker dollar. Emerging market debt was the fixed income standout, with returns of roughly 14%.

Gold: The Asset of the Year

Gold deserves special mention, following 4th quarter returns of 11.7% and 64% for the year – further solidifying its position as the high return asset class of the millennium. New Frontier’s published research laid the framework for a modest 2–5% allocation to gold as a means of enhancing risk-adjusted return, assuming gold had reliable risk management characteristics but no corresponding return premium. Recent events challenge both assumptions: If gold can double in less than two years, it can decline as well; and the persistence of high returns raises questions about whether gold needs to be reconsidered as a high long-term return asset. Influences such as ETF access, central bank purchases, and retail speculation factor into the outlook. For now, our forecasts are conservative for return and cautious for risk, while recognizing the asset’s unique diversification characteristics.

Gold also proved more effective than other “store of value” candidates like silver or cryptocurrencies. Silver had a spectacular return in 2025. Silver can outperform in up markets but tends to be more speculative, volatile, and equity-correlated. In contrast, Bitcoin fell 6% in 2025. Bitcoin is highly susceptible to investor flows, and during periods of market stress, large sales triggered ETF redemptions. The resulting price impact has largely persisted: higher after inflows from the successful launch of the ETFs and lower with ETF redemptions. This divergence validates our view: gold is a strategic portfolio component optimized for risk management, whereas other digital or precious assets have been less consistent portfolio contributors.

U.S. Dollar: Performance in Perspective

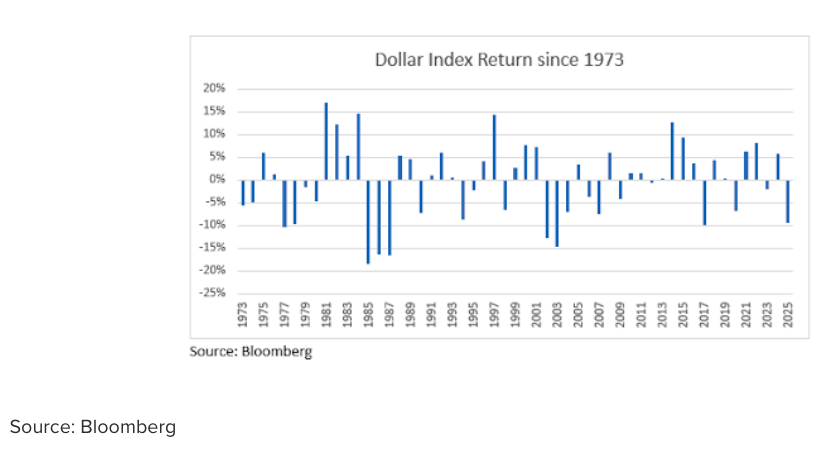

The U.S. dollar fell 9.4% in 2025. This feels large, but it is merely a 1 in 5 event—there have been 10 similar or worse declines in the last 50 years.

Rate Wrap Up

- The Fed controls short-term rates, but the economy determines long-term yields.

- The Fed reacts to economic data, so the economy indirectly determines short-term rates.

- The magnitude of 2025’s 10-year rate change (0.50%) is less than one standard deviation of historical interest rate volatility, and therefore not exceptional.

- Long-term yields stayed firm because investors demanded compensation for inflation risk and fiscal uncertainty, as recession risk faded and inflation expectations rose.

- Long yields are now slightly higher than short. Expected rate cuts may further steepen the curve modestly; excessive cuts could steepen it more if inflation risk pushes long-term rates higher.

- Mortgage rates fell roughly 70 basis points in 2025.

New Frontier Strategy Performance

New Frontier’s ETF portfolios delivered solid results in the fourth quarter and over the full year, despite notable volatility in April. Performance benefited from positive contributions across both equity and fixed income.

Global Core Portfolios posted positive returns across all risk profiles. International equities and Emerging Market debt were major contributors to relative performance, while the strategic allocation to gold proved to be the most significant contributor to risk-adjusted returns. Allocations to minimum volatility equities and U.S. REITs modestly detracted from relative performance.

Tax-Sensitive Portfolios performed largely in line with Global Core Portfolios, performing slightly better in the fourth quarter but trailing for the year. This divergence was driven, in part, by municipal bonds, which outperformed taxable bonds during the quarter but underperformed over the year. Notably, 2025 marked another year with zero realized capital gains for the ETF portfolios, reflecting a continued focus on after-tax total return.

Multi-Asset Income (MAI) Portfolios delivered on their mandate, with yields remaining attractive around 5%. Performance was driven by a diversified selection of high-dividend ETFs, particularly international dividends which outperformed U.S. dividends by nearly 40%.

Core + Alts Portfolio posted its first full year of performance. This portfolio was designed to bring institutional alternative management to individual investors taking advantage of the rapidly improving group of alternatives ETFs. The objective is not necessarily to outperform our Core Portfolios in every period, but to diversify away from core market risks. In 2025, this strategy delivered comparable returns to our standard Core Portfolios but with approximately 20% less risk. Also notable is our optimized approach to alternatives. Since alternative asset classes have different characteristics – some enhance return (e.g. private equity), some manage risk (e.g. anti-beta and gold), and others do some of both (e.g. closed end funds and managed futures) – investors are better served by dynamically adjusting the mix to meet their goals.

Across strategies, effective diversification driven by our quantitative investment process remained beneficial. The year reinforced the importance of balanced exposure across geographies, asset classes, and income sources amid concentrated equity leadership and an evolving macro environment.

OTHER DEVELOPMENTS

Model Portfolio Asset Allocations

In early December, we rebalanced the Global Core ETF portfolios. This rebalance represented a normalization of risk exposures. The previous rebalance occurred during a period of elevated tariff-induced volatility, resulting in a more defensive posture. As market volatility stabilized and equity markets rallied, the December rebalance returned the portfolios to a neutral risk stance.

Fixed Income Enhancements

The rebalance optimally allocated for tighter credit spreads and a steeper curve, reducing exposure to ultra-low duration as those securities became relatively less favorable.

We introduced a more efficient ETF, BondBloxx JP Morgan USD Emerging Markets 1-10 Year Bond ETF (XEMD). XEMD offers lower duration, lower expense ratio, with comparable yield, enabling better portfolio risk management by mitigating the “duration drift” often seen in bond funds.

Return to China

We reintroduced a dedicated allocation to China equities through Franklin FTSE China ETF (FLCH). FLCH provides differentiated technology exposure that can hedge U.S. tech concentration while maintaining similar growth expectations, adding a partially independent investment in AI that is difficult to replicate elsewhere.

Economic and Market Insights

AI Risks: Capital Depreciation and Market Concentration

While Artificial Intelligence is undoubtedly valuable, any investment ultimately needs a reasonable return on capital. The industry is in the build-out phase, characterized by massive capital expenditures, estimated at $360 billion in 2025, and accelerating to $3 to $5 trillion over the next five years. To put this in perspective, last year’s spending was more than the entire 13-year Apollo program or roughly ten Manhattan Projects, and 2026 will likely be much higher.

One risk is depreciation. Processing power has improved roughly thirtyfold over the last four years, making prior-generation data centers obsolete quickly and putting future debt-finance infrastructure at great risk. Emerging market AI infrastructure, by contrast, is generally far more capital efficient, making a shift to commoditized emerging suppliers plausible. The trillions of dollars being inefficiently allocated is a serious risk.

Market concentration presents additional challenges. Large U.S. technology companies have been the biggest source of risk even within well-diversified balanced global portfolios. As market concentration has increased and valuations have risen, the embedded risk within the passive market portfolio has grown accordingly. Investor concerns about this risk are well noted and rooted in both financial theory and historical precedent. However, Chinese tech firms have the potential to achieve similar high returns and can serve as a hedge to U.S. tech concentration. One or both may prove to be successful, so a portfolio can benefit from diversification without a reduction in future growth exposure.

The Fed and the Debt Burden

The Fed’s 2025 rate cuts signaled a willingness to prioritize growth even as inflation remained above the 2% target. While the Fed reduced rates 75 basis points, long-term yields did not fall proportionately, reflecting concern that aggressive cuts could reawaken inflation and devalue long-term bonds.

The motivation for lowering rates is complicated by the national debt. The U.S. is effectively borrowing to stimulate growth, predicated on the assumption that the economy will grow faster than the cost of servicing that debt. This works best if longer-term rates eventually fall. Higher rates slow growth and worsen deficits, tightening the boundary on how far policy can push.

Inflation: Unwinding Transitory Shadow Inflation

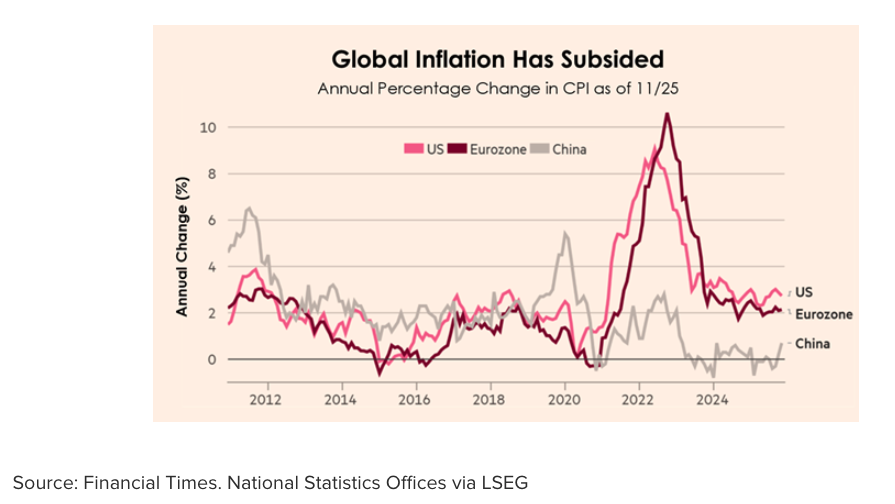

Global inflation has largely subsided, with most major economies roughly at a two-year plateau. Tariffs and a weak dollar add pressure to drive prices higher, but the U.S. economy has proven to be adaptable. For now, corporations have been willing and able to absorb much of the impact due to generally high post‑pandemic margins (evidence that the famously wrong prediction of “transitory” inflation was partially correct, though it never reached consumers). At some point, profit cushions will disappear, and companies will be forced to pass more of any price increase to consumers. Until then, the Fed will continue balancing growth and inflation through cautious cuts.

The Government Shutdown: Signal vs. Noise

The fourth quarter government shutdown was largely ignored by markets. It was widely anticipated, and investors treated it as political theater rather than an economic catalyst. Historically, shutdowns resolve with little lasting damage, and the market’s muted reaction – volatility fell during this period – suggests markets are becoming more sophisticated and discounting events with little economic impact.

Active ETFs: A Public Good

2025 saw the acceleration of mutual funds converting to ETF structures. While our investment philosophy generally favors passive funds, we view the growth of active ETFs as a net positive for market health. Active managers are the informed agents who set efficient market prices that passive investors ride for free. When institutional active managers are setting prices, rather than retail speculators, market efficiency improves. We welcome this expanded ecosystem, even as we continue to use it selectively.

Private Assets: The Victim of Its Own Success

The “endowment model,” of heavy allocation to private equity provided a simple solution for higher returns. In 2025, however, much higher flows of capital into private markets reduced the cost of capital for private companies, which in turn lowers future returns for investors. The end result is for private equity to converge towards the return profile of public markets, with more assets and greater competition among asset managers.

A Look Ahead

Asset manager outlooks are nearly uniform in their contradictory continued optimism. After three years of AI-driven market returns, pundits express caution on valuations, then advocate continued investment in the same tech companies citing continued capital expenditure, lower interest rates, and lower taxes. However these factors are widely known and therefore should be priced into already high valuations.

Revisiting Market Predictions

In 2025, we published a series of predictions for the year to demonstrate the value of understanding market structures over speculation. Looking back, the accuracy rate was much higher than predicted.

Our 2025 predictions included:

- There will be no recession in 2025.

- Stocks will go up, but not too much.

- Bonds will go up too, with fixed income premia paying off over cash.

- Bitcoin will fall by 20%; rates will go down a bit.

- Inflation won’t go down much.

- The S&P 500 will experience a correction, but not a bear market.

What’s remarkable is that all of them happened.

Possible outcomes for 2026

For 2026, these are our expectations, not predictions.

- Inflation will rise…a bit, as tariffs work through supply chains alongside a weak dollar and stimulus.

- No recession, but slower growth: there will be winners and losers, but less trade and higher prices will weigh on the aggregate economy.

- Signs of capital misallocation in AI will eventually emerge as depreciation and pricing realities catch up to ambitious build-outs.

- Global markets will rise.

- International market returns will be dispersed.

- There will be a higher dispersion in bond returns. 2025 featured strikingly little difference between risky and risk-free bonds in the US market, with returns ranging from 4 – 8%. 2026 will be different.

- Gold will be volatile and experience drawdowns as positioning shifts.

- There will be a significant amount of political noise.

- Two of the following three will do well: Value, Small Cap, and Emerging Markets.

- Active ETF conversions and flows will continue. (by the way, it won’t be a stock picker’s year)

- Bonds will barely deliver positive real returns. Interest rates will have to face the boundaries set by inflation; fixed income will return to its traditional role of income generation.

- Private assets will be fine but not spectacular as returns converge toward public markets and the illiquidity premium shrinks.

Conclusions

2025 was a year in which thoughtful investing paid off through broad diversification and returns to risky assets, alongside surprisingly high returns to risk diversifiers such as gold. In 2026 we may see big differences in performance between those who timed an AI bubble correctly and those who did not, but timing market bubbles is not a viable long-term investment strategy.

In 2025, markets dismissed concerns of inflation, tariffs, and geopolitical turmoil, focusing instead on technological progress, corporate earnings, and a resilient economy. As we enter 2026, the easy returns of the post-pandemic recovery are behind us. We are entering a more nuanced environment of higher structural inflation, diverging global growth, and significant technological disruption. In this landscape, the New Frontier philosophy remains crucial: rather than betting on a single outcome, we optimize for resilience across thousands of potential outcomes. By maintaining global diversification, managing tax efficiency, and remaining disciplined in the face of noise, we believe investors are best positioned to achieve their long-term goals.

Key takeaways

- 2025 reinforced the disconnect between market sentiment and economic reality: recession fears gave way to all-time highs and steady growth.

- Markets are getting better at separating signal from noise—Q4’s shutdown looked like political theater, not an earnings shock.

- International markets are no longer moving in lock step with the U.S.; lower correlations and wider regional dispersion strengthen the case for global diversification.

- The Fed cut 75bp in 2025 and steepened the curve: short rates fell, but long yields stayed firm as investors demanded compensation for inflation risk and fiscal uncertainty.

- Gold earned “asset of the year” status by maintaining its risk character while delivering extraordinary returns, though the magnitude of the move raises questions about long-term stability and premium.

- AI remains a durable growth theme, but the build-out has an investment risk: massive capex and fast depreciation can turn yesterday’s infrastructure into tomorrow’s distressed asset.

- Private assets are becoming victims of their own success. As capital floods in, the illiquidity premium shrinks and returns converge toward public markets.

- Portfolio implementation mattered: diversified strategies performed to mandate, our Core + Alts strategy delivered comparable returns with materially lower volatility, and year-end rebalancing normalized risk while improving fixed income efficiency and reintroducing China exposure.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Originally published on ETF Trends

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosure: New Frontier Advisors LLC (“New Frontier”) is a federally registered investment adviser based in Boston, MA. This content is intended solely for the use of investment professionals and should not be distributed or relied upon by retail investors or the general public. It is provided for informational and discussion purposes only and does not constitute an offer, solicitation, or recommendation to buy or sell any security or engage in any investment strategy. This commentary is not intended for use as a primary basis for investment decisions and is not intended to meet the objectives or suitability requirements of any particular investor.

The information presented in this commentary is believed to be accurate at the time of publication but may be subject to change without notice. No representation or warranty is made as to its continued accuracy or completeness. The investment adviser has no obligation to update this commentary to reflect changes after the date of publication.

Any forward-looking statements or projections are based on current assumptions and expectations and are subject to known and unknown risks and uncertainties. Past performance is not indicative of future results, and investing involves risks, including the potential loss of principal. Diversification may not protect against market risk. Before investing in any investment portfolio, the investor and Financial Advisor should carefully consider the investor’s investment objectives, time horizon, risk tolerance, and fees.

For Investment Professionals Only.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All