In recent editions of Macro Signposts (here), we’ve emphasized how U.S. policy changes coinciding with the emergence of a new general-purpose technology (AI) may be accelerating adoption and diffusion of that technology – while also driving economic adjustments. So far, those adjustments have supported relatively stable real GDP growth in the U.S., but we see fragilities under the surface.

AI-driven productivity gains have buoyed asset prices and supported consumption through wealth effects, while investment has been narrowly concentrated in AI implementation and infrastructure. As a result, near-term U.S. economic performance will likely depend heavily on how the AI transition progresses.

AI is a relatively new technology. Large language models (LLMs) as general-use systems for the broader public became available in 2022, with widespread U.S. business adoption only starting to accelerate in 2025, according to U.S. Census Bureau data.

There are a lot of unanswered questions around how the economic adjustment will play out. Whether AI will primarily be a substitute or a complement for labor, how quickly it diffuses across the economy, and ultimately who wins versus loses are all very difficult to forecast. Unlike past general-purpose technologies, which took decades to diffuse, AI use is spreading fast, with divergent consequences across the economy. Recent sharp declines in equity and loan valuations across AI-exposed sectors underscore these risks.

Given the uncertainty, comparisons to historical economic transformations that followed the introduction of general-purpose technologies are natural. Specifically, the late-1990s diffusion of personal computers, networking, and the internet, which drove a productivity boom, is a potentially useful study for today. However, there are important differences between the late 1990s and what is happening today. If 2025 is a preview, AI might not be a productivity tide that lifts all boats. Indeed, the risk is that much of the value AI creates will accrue primarily to capital holders – not workers.

Lessons from the 1990s …

In 1994, Nobel laureate economist Paul Krugman remarked that while productivity isn’t everything in the long run, it’s “almost everything.” Productivity-enhancing new technologies have tended to raise living standards by augmenting both supply and demand over time – a tide that lifts all boats. Achieving greater output with the same level of input (whether through technological innovation or any means) increases productive capacity simply by definition. As part of this trend, more productive workers tend to earn higher real wages, and more productive capital tends to earn higher returns. Higher real wages and profits should in turn encourage consumption and investment, and support demand.

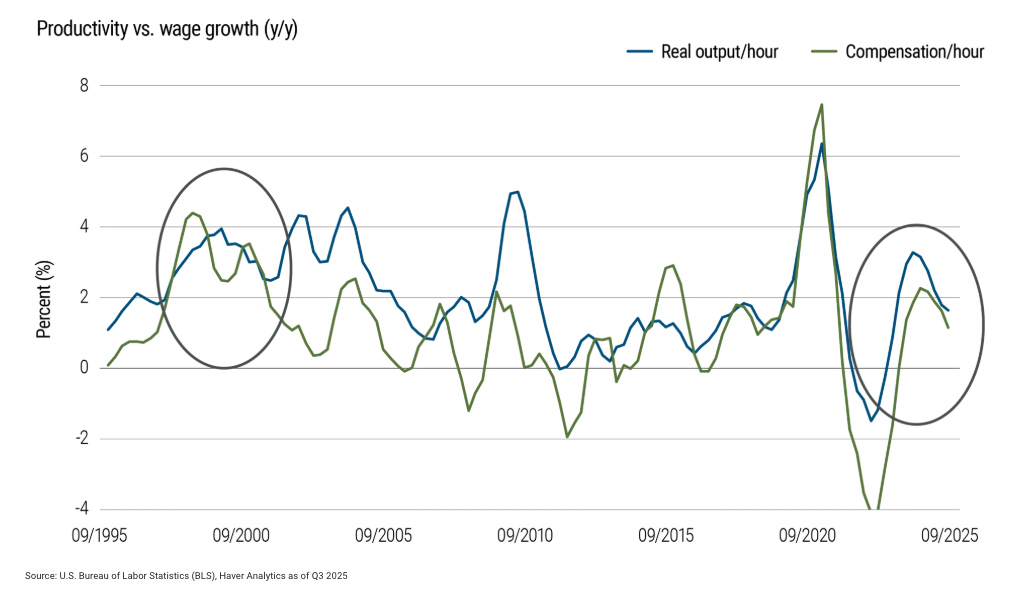

The late 1990s, when widespread adoption of personal computers and the internet transformed the economy and service work in particular, illustrate this dynamic: As U.S. productivity accelerated, real wages grew in line with productivity growth; workers were able to capture the economic value of their greater output (see Figure 1).

Figure 1: U.S. productivity growth and wage growth in two different tech booms

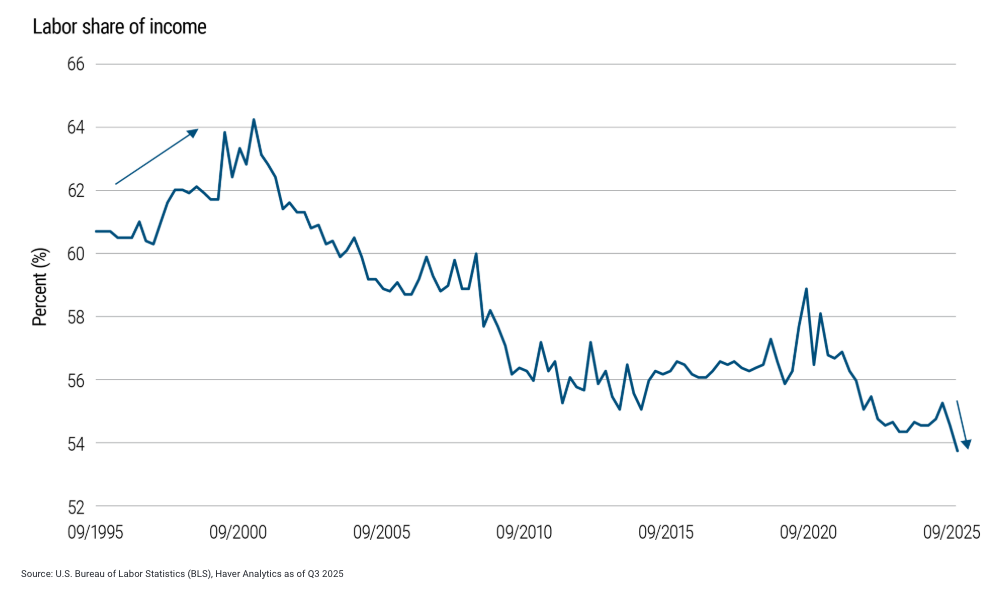

Labor’s share of income also increased over this period (see Figure 2), as did the labor input costs of the products and services sold (i.e., unit labor costs) – computers and networking made white-collar professionals more productive and better paid. Capital holders also benefited. From 1995 to the stock market peak in mid-2000, total returns from investment in the S&P 500 Index were over 200% in nominal terms.

Figure 2: U.S. labor market’s share of income rose in the late 1990s but hit a record low in 2025

Perhaps counterintuitively, stronger demand from higher real wages, combined with wealth effects from rising equity prices and greater capital relative to savings demands, likely contributed to the acceleration in U.S. inflation in 1999–2000 (and likewise the potential for higher real neutral interest rates). Monetary policymakers responded: The U.S. Federal Reserve, after initiating an easing cycle in the latter half of 1998, reversed course and hiked the policy rate 175 basis points from 1999 to 2000 in an effort to manage inflation risks.

… with implications for today

At first glance, today’s AI adoption shares similarities with the 1990s tech trends: productivity growth (which was especially sharp in 2023–2024; look back at Figure 1), rising (albeit narrow) investment, and notable wealth gains. The critical difference is the distribution: In 2025, workers as a group captured very few, if any, of those benefits. Workers’ real wage growth in 2025 slowed to a pace barely above 1%. This helped drive down labor’s share of U.S. income to the lowest level in decades of reported history (look back at Figure 2). For details, read our recent Macro Signposts, “Why U.S. Productivity Gains No Longer Reach Workers.”

The flip side of labor’s inability to capture the benefits of greater AI-related productivity is higher profits and capital returns. This difference between the 1990s and today may matter for near-term inflation and central bank policy. AI may spur both demand and supply sufficiently to put upward pressure on inflation and eventually prompt the Fed to hike rates. However, if the gains remain largely concentrated among capital holders – higher-wealth and higher-income individuals and households with lower propensities to consume – then the demand impulse may be weaker. This means the adjustment to a more AI-suffused economy could be more disruptive than we saw in the mid-1990s period.

Greater labor displacement is a key risk

Compare a couple of well-worn sayings: “History never repeats, but it rhymes,” and “This time is different.” Which saying is better applied to AI’s impact on the economy? Throughout history, new general-purpose technologies displaced jobs, while also creating new ones. However, whether displacement and new job creation happens simultaneously is far from clear. If 2025 is any indication, the risk is that labor displacement is the dominating force, at least at first.

Which jobs are more likely to be displaced? AI specifically disrupts tasks that are key for occupations across sectors. Nevertheless, some occupations and sectors appear more exposed: By nature, more of their tasks could be disrupted (or displaced) by AI. A 2023 research study by Eloundou et al.Footnote1 suggests that sectors most at risk for task disruption are data processing, information services (e.g., software), and publishing/broadcasting, followed by financial, professional, and technical services, and then retail. In contrast, construction, manufacturing, transportation, and personal/social services appear less at risk.

A detailed look at the labor market data suggests that AI-related job displacement is already happening, although so far it’s been relatively limited. Entry-level hiring stalled in 2025 in the most AI-exposed sectors. And since 2022, we estimate (based on the same Eloundou et al. study) that cumulative U.S. employment in the most AI-exposed sectors has already declined by over 1% versus a 4% increase in employment across other sectors.

Beyond the most AI-exposed sectors, it’s estimated that approximately one-third of tasks performed by workers across the U.S. economy could be handled by the current LLMs. Most workers, even those in highly exposed occupations, also complete more “AI-immune” tasks – but if AI hypothetically were to displace only a small 2% share of these workers, it could lead to nearly one million fewer U.S. jobs and the unemployment rate rising by 0.5 percentage points (assuming none of these workers leave the labor force).

Equity market dynamics could amplify the economic risk. Price declines of AI-disrupted firms could dent CEO confidence and trigger layoffs. A recent research paperFootnote2 suggests that firms seem to adjust employment by roughly 1% for every 10% change in their stock prices. If we apply this math to the top 37 U.S. companies with the greatest potential AI exposure and that have recently seen their equity prices decline by at least 10%, we can estimate that their most recent one-year net stock price declines could result in a negative employment shock of nearly 90,000 U.S. workers alone.

Bottom line for investors

Innovation-driven productivity growth is often described as a tide that lifts all boats. The 1990s largely fit that narrative, when a productivity boom lifted real wages, increased supply and demand, and ultimately generated inflationary pressures.

While an AI-led productivity boom could generate similar outcomes, the risk is that the economic adjustments seen in 2025 foreshadow more to come – that AI will likely create winners and losers, with capital holders the net winners. Although workers generally were more productive in 2025, labor’s share of income fell, and we may see more net labor displacement ahead.

AI could still end up benefiting most players in the U.S. economy over time, but the transition could be uncertain and perhaps disruptive for companies both within and across sectors.

In this environment of divergence, we see a strong argument for investment diversification. As equity markets reprice both winners and losers and downside risks skew toward labor disruption, high quality bonds may provide an effective hedge alongside attractive return potential.

Footnotes

1 Tyna Eloundou, Sam Manning, Pamela Mishkin, and Daniel Rock, “GPTs are GPTs: An Early Look at the Labor Market Impact Potential of Large Language Models,” arXiv .org paper 2303.10130, revised August 2023. Return to content↩

2 Bryan Seegmiller, “Valuing Labor Market Power: the Role of Productivity Advantages,” SSRN abstract ID #4412667, revised October 2025. Return to content↩

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0218-5232040

© PIMCO

Read more commentaries by PIMCO