Conflicting Data, Conflicting Results

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIs inflation rising or falling? Is unemployment solid or are there significant issues? Given the massive revisions of labor data, how can we base decisions on employment numbers? And what happens when the various collected data conflicts with themselves?

Given that there are no clear guidelines for policy decisions, those of us sitting in the back of the airplane can be forgiven for thinking that the policy pilots flying the plane are “winging it.” Some of us from an older generation remember the saying, “Flying by the seat-of-the-pants.” You can justify almost any decision depending on which data you want to use. Hence the wide variety of views from the recent FOMC minutes.

Today we are going to look at the recent CPI data, the PCE data and the problems in the labor market. We are coming closer to the time when the market is going to realize that whatever policy the Federal Reserve chooses, the desired results will be less than we have seen in the past, and indeed may run counter to historical comparisons.

A “Tame” CPI Inflation Number

I read a lot of analysis on the recent CPI numbers. Let’s start with some wonderful work done by Strategas Research Partners. Their work is for institutions, and therefore not cheap, but they provide value and unique insights. Quoting from their analysis of the recent CPI numbers and using a few of their charts (emphasis mine):

U.S. CPI TAME EVEN WITH THE “JANUARY EFFECT”

-

The U.S. CPI was a moderate +0.2% m/m and 2.4% y/y in Jan. The core (ex food & energy) measure was +0.3% m/m and 2.5% y/y.

-

This matters because there had been a pattern of January CPI prints popping to the upside with calendar-based resets (annual wage hikes, etc).

-

Of note, used car & truck prices declined -1.8% m/m in this report, helping hold down the headline number. Tax return prep prices were also -13.8%.

-

Bottom line: The FOMC previously indicated a desire to move slowly in early 2026. They are probably still on hold as we head toward the March meeting. But tame CPI readings keep the door open to eventual further central bank easing in 2026 as we move toward the summer (and a change in Fed leadership).

Nearly every analysis I’ve read of the CPI numbers continues to point out that the heavily weighted Owner Equivalent Rent is well behind the actual drop in rent and the downtrend has been evident for years.

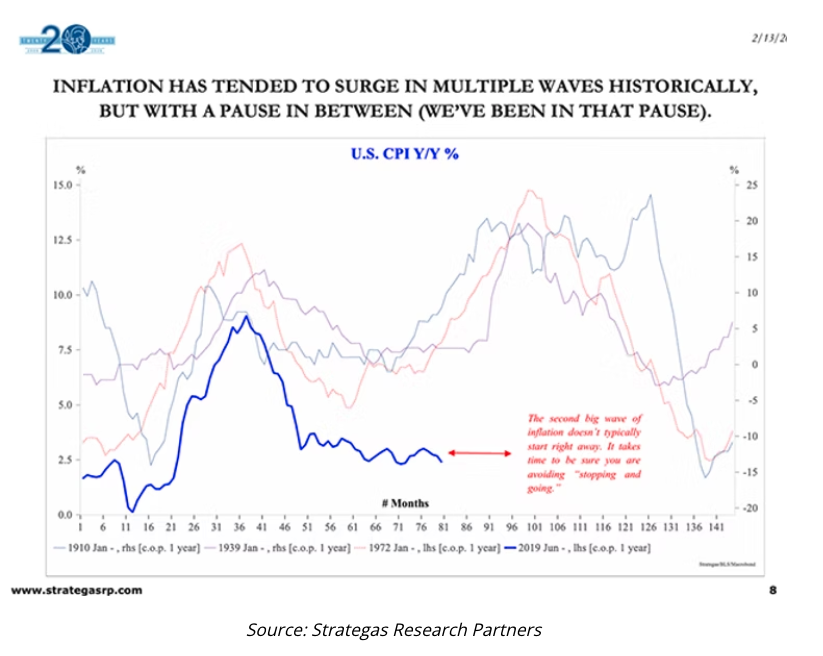

One more chart from Strategas. This provides some excellent insight on past inflationary cycles. The heavy blue line is the current cycle and as you can see after an initial surge and then a drop, inflation has tended to go sideways to down a little bit. This has some observers breathing easy and suggesting that the Fed should cut rates as inflation is getting closer to their target. But Strategas points out that in past inflationary cycles, inflation comes in “waves” with a pause between the surges. The light lines represent past inflationary periods measured in terms of months. While the correlations are not exact, the implied lesson is that without Fed vigilance, inflation can come back quicker than we would like to think.

Here is a good visual summary from my friend Barry Habib at MBS Highway. Shelter in the CPI is still way too high, and if the number is anywhere close to reality, it would take the CPI to the 2% range.

To Cut Or Not To Cut?

There are considerable differences of opinion as to whether the Fed should cut rates are not. And frankly, exactly what would a rate cut accomplish? It’s not your father’s economy, and to expect a rate cut to act like it did 40, 20 or even 10 years ago is probably not realistic.

In what I think is a little bit of irony, Dr. Lacy Hunt thinks the Fed is behind the curve and should be cutting rates. Lacy has been death on inflation for all the decades I’ve known him, and he has been in the disinflation camp for nearly all of that time (with some short-term exceptions).

Lacy thinks we are still in a disinflationary environment. Let’s look at his eight reasons he provided in a recent analysis (emphasis mine):

- The labor markets have been weak for over two years, pressuring wages and resulting in recessionary levels of consumer confidence. The BLS overcounted jobs by 1 million in 2025 after an overcount of almost 0.5 million in 2024. Last year’s gain was only 118 thousand or 10 thousand a month. The entire increase was more than accounted for by the social service and health industries, the two most non-cyclical components of the labor market as they are tied to aging demographics. Based on labor market conditions, most industries were in recession for most of 2025.

- As reported real disposable income (DPI) has been unchanged since May, a worrisome trend. These figures were based on the reported and greatly overstated job levels; that will eventually result in significant downward revisions to DPI, total personal income, GDI (gross domestic income), personal saving, total national saving that is currently reported as barely positive and resulting in an even larger discrepancy with GDP, a condition that is economically unjustified.

- Third, monetary conditions proved more restrictive than widely recognized, even as the Federal Reserve cut the Federal Funds rate in both 2024 and 2025.

- Fiscal policy unexpectedly tightened due to a notable reduction in the federal budget deficit.

- More U.S. manufacturing plants outside the AI sector became idle.

- Major economies abroad, including China, Japan, Germany, and the UK, experienced stagnation.

- A scholarly econometric study indicates that while tariff hikes initially boost inflation, their longer-term effect is to suppress demand and contribute to disinflation.

- AI is disinflationary, cyclically and secularly.

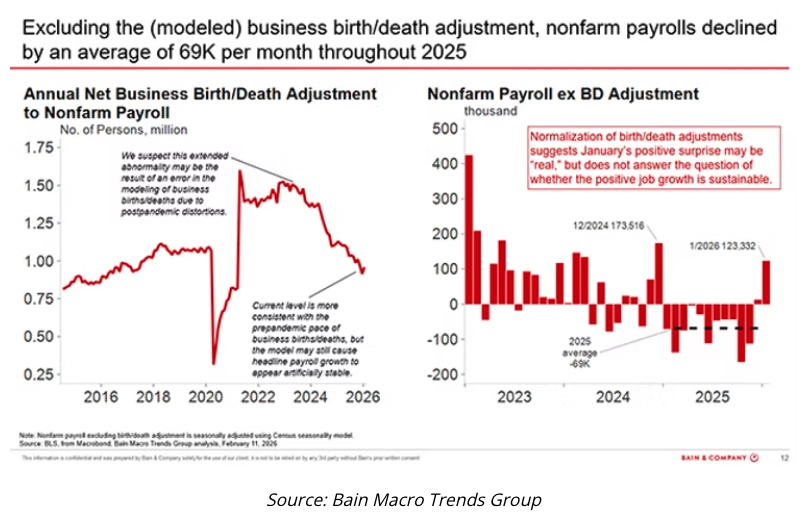

Let’s visit point number 2. As we see in the chart below, the Bureau of Economic Analysis overestimated the number of jobs in 2025 by 1,029,000. The sweeping correction follows downward revisions of 818,000 jobs in 2024 and 306,000 in 2023 [the numbers vary depending on how analysts calculate the data]. Over the past three years alone, 2,153,000 jobs have been erased from earlier reports.

No conspiracy here. The simple fact is that we have gone from over 80% of companies reporting in the first months to around 60%. Government analysis is forced to make assumptions on just over half the data. The surprise would be if there were no revisions. The model they use requires them to make assumptions on historical data as they make the projections. Since we are in a changing labor environment, and one changing to the negative, it is no surprise that the revisions are downward.

But as Lacy pointed out, this is going to require them in the future to revise gross domestic income, personal savings, personal income and more downward. This suggests that the economy is weaker than their data has been suggesting.

When I asked him about the increasing government debt, he pointed out that the deficit fell from 2024 to 2025 by $300 billion. Notwithstanding Friday mornings Supreme Court ruling on tariffs, if the Trump administration continues to reduce the deficit this is in fact disinflationary (if we can talk of disinflation and trillion dollar deficits in the same sentence).

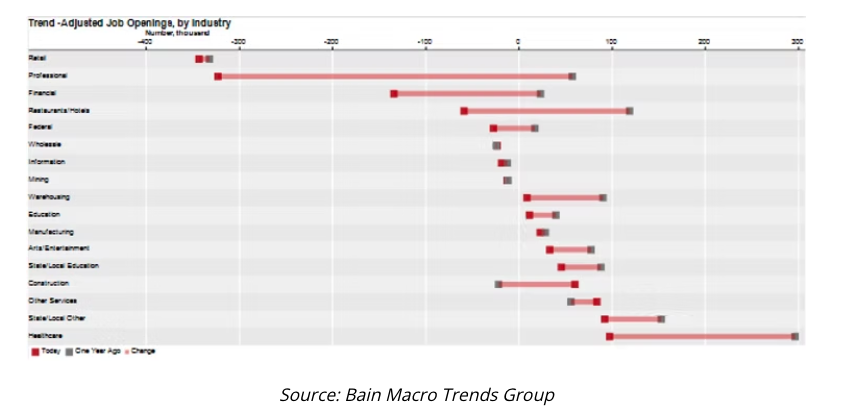

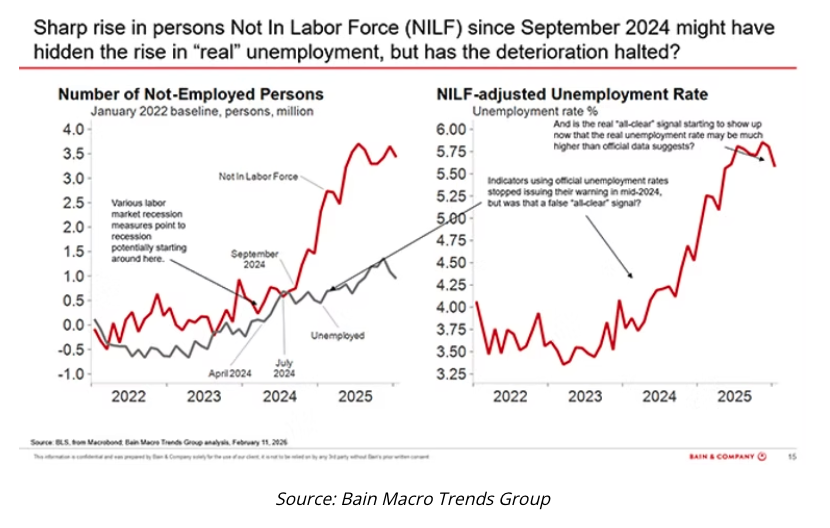

A final few charts on employment from Karen Harris of Bain and Company’s Macro Trends Group. They analyzed 16 categories of employment. Last year’s biggest job creator (healthcare) is still sharply pulling back on openings; the second-biggest job creator (state/local) is also slowing. Nearly every other category is also showing negative growth when compared to last year. Needless to say, this is concerning.

This chart doesn’t make me feel any better:

And neither does this last one. If you adjust for the number of people that have dropped out of the labor force in the last two years, the unemployment rate is closer to 5.5%. The concerning part is the significant growth of those who have dropped out of the labor force, many of them in the 25 to 54-year-old range. Most concerning.

Economic Nirvana?

Dr. Ed Yardeni has a much different view. He starts his recent essay with the question, “Nirvana: Will Somebody Tell The Fed That We Have Arrived?” Quoting:

“The Fed achieved its congressional dual mandate in January. The unemployment rate fell to 4.3%, and the CPI inflation rate was down to 2.4% y/y. Those round down to what we call “Nirvana” readings, i.e., the low unemployment level of 4.0% and the Fed’s inflation target of 2.0% (chart). Fed officials should celebrate and go on a long vacation. They can leave the federal funds rate (FFR) alone at its current 3.50%-3.75%. By their own definition, that must be the "neutral" FFR, the level that’s consistent with full employment and stable prices. Why mess with success?

“…the Fed has cut the FFR by 175bps since September 2024 (chart). It's not obvious to us that this easing was necessary to keep us in Nirvana. In the past, the Fed slashed the FFR in an emergency response to financial crises that rapidly morphed into economy-wide credit crunches, triggering recessions. That's not the scenario now.”

He has a point. 175 basis points of cuts and mortgage rates have barely dropped. Unemployment has still softened. Homebuilding and home purchases are soft. Consumer spending is only robust in the top 20% of the economy. And even that is beginning to soften.

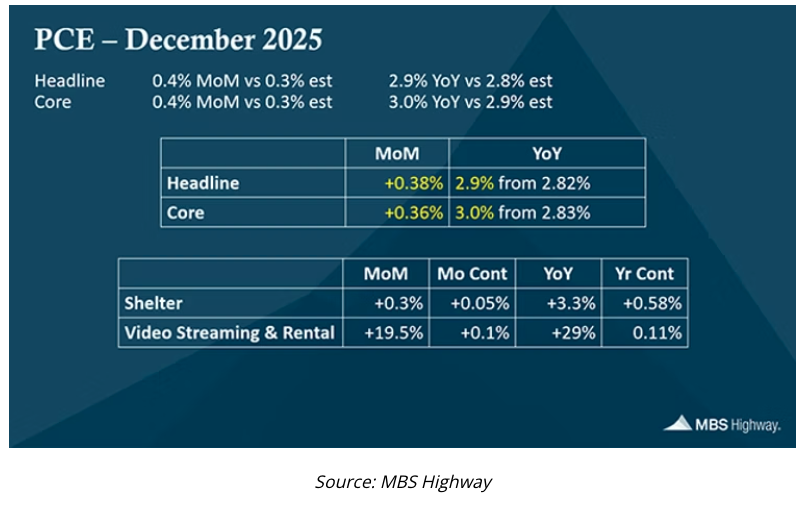

And Then PCE Rains on the Inflation Parade

As I was writing the above, I was also waiting for the PCE number to come out on Friday morning. It was disappointing. Rather than confirming softness in the CPI, we got the opposite. PCE was much higher than expected. Again, from Barry Habib at MBS Highway:

First, the high PCE number subtracted from the GDP and gave us a weak 1.4% GDP for fourth quarter 2025, well below expectations at half the estimate of 2.8% and 8 tenths of that was due to a 3.6% price deflator vs the forecast of 2.8%.

Barry notes: “They're telling us that shelter's at 3.3% year-over-year. We know that that's not the case. We know that it is truly closer to 1% year over year. You take that…the incorrect read on shelter, and you apply it to the 18% weighting in core, and the 16% weighting in headline, this is roughly 4 tenths of a percent that it is artificially juicing inflation.

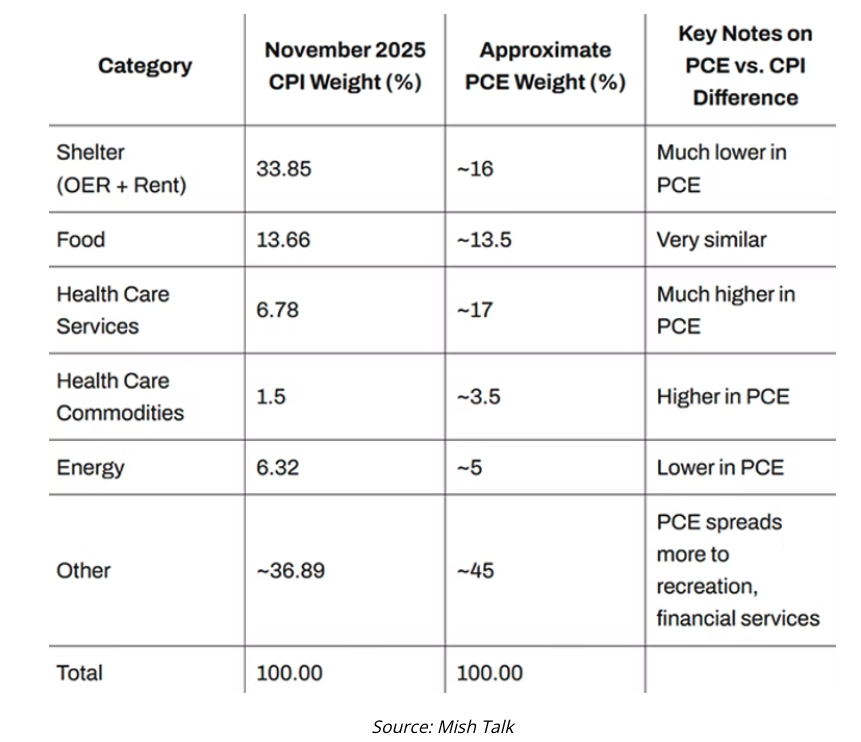

So we get a “tame” CPI number and a hot PCE inflation number. Within seven days of each other. What in the wide world of government bureaucratic data analysis is going on?

Mike Shedlock (Mishtalk) recently pointed out it is likely we will see continuing discrepancy between the BLS produced CPI and the BEA produced PCE. That is because of the significantly different weighting factors that both government agencies use. Below is a handy chart from Mish.

Note: Unlike the BLS CPI, the BEA does not publish PCE percentage weights monthly and the changes are more dynamic. Those are estimates based off consumer expenditures.

As I finalize this letter, David Bahnsen sent me this advance note on the PCE and inflation. He basically argues that the headline data will go lower due to OER (Owners’ Equivalent Rent) coming down, but that goods prices are going higher. You can (and should) read the whole thing in his Dividend Café this week. Hit the subscribe button. Quoting:

“What is most relevant to investors right now is not the thesis I have laid out above - that the reported inflation number will be ticking down in 2026 due to the impact of declining rent growth, even as other elements of the elevated price level remain sticky. Assuming all of that plays out exactly as I have said, one can easily see a political scenario where each side attempts to spin it to their advantage. And I already told you, I don't give a whit about all of that.

“But here is why I am writing this week's Dividend Cafe ... I believe the disinflation thesis may end up being more right than I have suggested, and for troublesome reasons.

“That capex narrative is a big one. There has to be robust business investment - a realization of the supply-side policy enactment that has historically been very productive in driving strong economic activity - and it is not my base case that these things will materialize. Some of these headwinds, though, are increasingly becoming more of a base case.

“First of all, the labor market. The data has been so mixed, so confusing, and so problematic, for so long, I maintain the humility of agnosticism. What I do not see, though, is any scenario where "it looks really good!" The best case appears to be that the labor data is not meaningfully worsening - that the hiring freeze and firing freeze stay in place. I don't want that - I want new job creation, and believe the economy needs it - but this "pause" is different than increased slack in the labor market (deflationary). I believe it is fair and honest to suggest that we have a "it gets worse" scenario as a possibility where unemployment picks up and the lack of hirings are foreshadowing an increase in future firings. I do not, however, believe there is much of a reason to see a scenario where it gets meaningfully better. In other words, the "best case" scenario seems to be a "status quo" which suggests increased stagnation (more disinflationary than deflationary). The major job revisions for 2025 (and 2024 before that), the extremely soft private sector indicators from ADP and Challenger Gray, and the Conference Board's labor differential being at its lowest level in four years all indicate a skew towards a worse-than-status-quo scenario in front of us.

“Additionally, one of the major arguments for improving economic activity in 2026 (from the administration, but also those who are making a plausible and serious economic argument) has been the expectation of significant tax refunds that are about to hit the checking accounts of many Americans (meaningfully above normal levels due to some of the provisions of the OBBBA). I agree that there will be greater-than-normal (one-time) tax refunds this year, mostly due to the disconnect between 2025 withholdings and actual tax rates. However, Dr. Lacy Hunt, one of my favorite living economists, has pointed out that the Personal Saving Rate (see the Chart of the Week below) being as low as it is (and even lower than reported once adjusted for the reality of spending increasing more than incomes) suggests that many tax refunds will be needed to replenish savings vs. enhanced spending.

“It is entirely possible that the lower federal funds rate we have now than a year ago, and the lower federal funds rate we are likely to get later in the year, will enhance borrowing conditions for some consumers and businesses. But that is not a guarantee. Nominal levels of lending did not move in 2025 despite easier financial conditions.”

John again. This is what I mean by conflicting data. It is equally possible to describe inflation coming down marginally, we get lower short-term rates and yet unemployment rising.

It is also difficult to see the transfer mechanism from a lower fed funds rate into increased employment. As noted above, we have seen 175 basis points of lower fed funds rates and employment is weakening. The lower fed funds rate only marginally moved mortgage rates. Housing is in the doldrums. Without the AI data center construction, it is quite possible that GDP could be flat to negative.

The scenario which concerns me most is when the market finally realizes that the Federal Reserve has lost their ability to fine-tune the economy in ways they have in the past. Once the Fed has lost the narrative, it is not clear to me that the markets, bonds or stocks, will be happy. Stay tuned…

Scottsdale, Houston, Los Angeles, West Palm Beach, Boston, New York and Cats

I will be in Scottsdale next weekend for a longevity conference with some of my associates. From Scottsdale I fly to Houston where I am on an economic advisory board for the Rice University economics department. I will be having dinner with Dr. Ken Rogoff, who along with Carmen Reinhart wrote what I think is one of the five most important economic books of this century, This Time Is Different. The title is meant to be ironic.

Then I will be in LA meeting with the Inner Circle, exploring several companies that are literally changing the technology landscape of defense and energy. Then we will be opening clinics in West Palm Beach and the DC area, hopefully in late March. Construction has begun. I will be in Boston in June. It is looking more and more like I will have to be in Cleveland for a medical procedure and I have to get to New York. The SIC will be early May and it will be our best ever.

On a lighter note, I am allergic to most cats. My wife Shane loved me enough that she gave up her cats (and dog) when we decided to join our lives. It was a struggle but she did it for me. When we moved to Puerto Rico we inherited two black cats in our backyard that Shane began to feed and dote on. They really didn’t come into the house all that much, so they didn’t bother me.

Then tragedy struck. One of the cats who was a little older and feeble just didn’t show up one day. My wife traveled the neighborhood for weeks trying to find that poor cat and basically went into mourning. A few weeks ago, she brought me a list of “hypoallergenic” cats that she maintained would not set off my allergies. I let her talk me into a cat called a Russian Blue. Not cheap. But then a week later she came to me and said, “If we get just one kitten it will be lonely and it will need a companion. Can we get another?” After my initial panic, and looking into her eyes, I said yes. She literally danced out of the room.

This week, two beautiful Russian Blue kittens arrived. They are cute even if I don’t touch them. And they really have made Shane happy. I’m such a softy.

And with that, I will hit the send button. I will be writing a special letter next week, updating my Fingers of Instability letter to our current situation. I hope you find it is fascinating as I do. Have a great week and enjoy family and friends!

Your fastening his seatbelt analyst,

John Mauldin

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All