Key Takeaways

- Income rather than price is the primary driver of FRN returns.

- As policy rates and SOFR move, FRN coupons adjust accordingly, allowing income to rise in higher-rate environments and decline when rates fall.

- Credit spreads influence yield and spread-related volatility.

- FRNs can help manage interest rate risk within a fixed income allocation.

What Drives Returns in Floating Rate Notes?

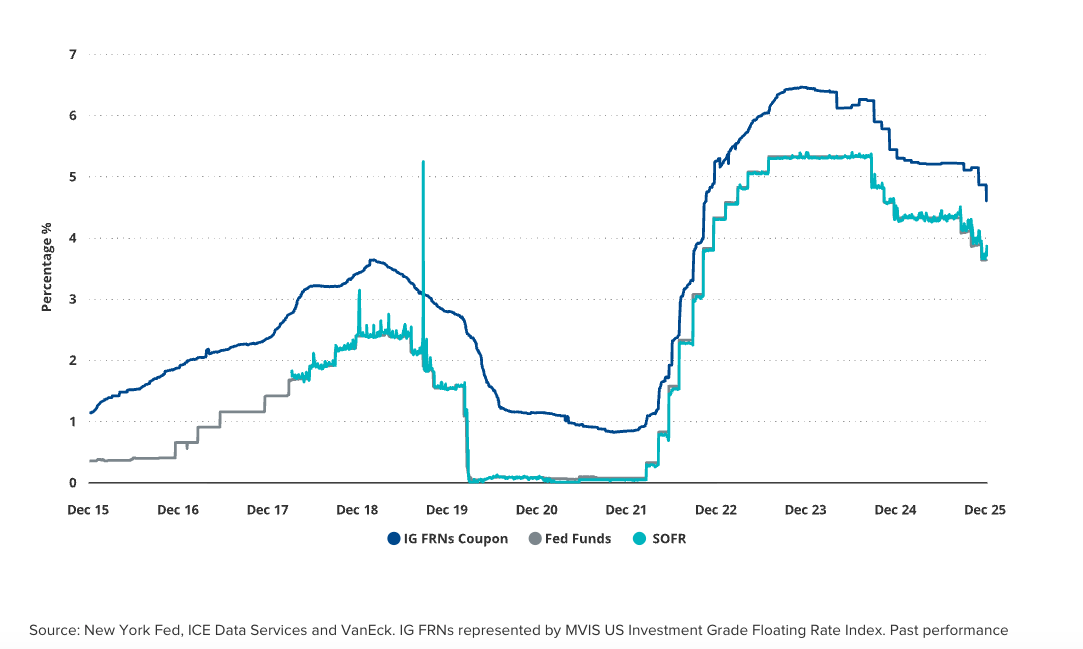

Corporate floating rate notes (FRNs) are often used to help manage interest rate risk. Unlike fixed-rate bonds, FRNs are structured so that income adjusts with changes in short-term interest rates. As a result, their returns are driven primarily by income rather than price movements, making them potentially attractive when rates are rising or expected to remain elevated.

What Are Floating Rate Notes (FRNs)?

Corporate floating rate notes are bonds that pay a coupon linked to a short-term reference rate (usually SOFR), plus a fixed credit spread. The coupon resets periodically, allowing income to rise when short-term rates increase and decline when rates fall. Because coupons adjust regularly, FRN prices exhibit minimal sensitivity to changes in interest rates. Investors therefore avoid the duration-related price declines associated with traditional fixed-rate bonds, although they also do not benefit from falling rates through price appreciation.

Key Drivers of FRN Returns

Returns in corporate FRNs are driven by two main components: short-term interest rates and credit spreads.

Short-Term Interest Rates and Coupon Income

The primary source of FRN returns is coupons. As reference rates such as SOFR move in response to monetary policy, FRN coupons reset accordingly. When short-term rates rise, income increases; when rates fall, income declines. Given the low interest-rate duration of FRNs, price volatility from rate movements is minimal, leaving income as the dominant driver of performance.

Credit Spreads and Spread Duration

While interest rates drive the level of income, credit spreads determine how much additional yield investors earn for taking on issuer credit risk. Higher credit spreads generally result in higher income but also introduce sensitivity to changes in market credit conditions. This sensitivity, measured by spread duration, is distinct from interest-rate duration and reflects exposure to changes in credit conditions rather than policy rates. In general, a longer time to maturity is reflected in a higher spread duration.

How Interest Rate Environments Affect FRNs

FRNs in Rising Rate Environments

When short-term rates rise, corporate FRN coupons reset higher, increasing income. Because price sensitivity to rates is limited, rising yields do not create the same headwinds for FRNs as they do for fixed-rate bonds. Instead, higher income becomes the primary contributor to returns, as seen during recent “higher for longer” rate cycles.

FRNs When Rates Fall

The same dynamic works in reverse. During the period leading into the COVID-19 pandemic, rapid Federal Reserve rate cuts drove reference rates sharply lower, resulting in declining FRN coupons. While income fell, FRN prices remained relatively stable, reflecting their limited exposure to interest-rate-driven price volatility.

Short-Term Rates as the Primary Driver of FRN Income

Over time, corporate FRN returns reflect the combined effect of prevailing short-term rates and credit spreads. As policy rates and SOFR move, FRN coupons adjust accordingly, allowing investors to earn income that evolves with the rate environment while maintaining low interest-rate risk.

Why Floating Rate Notes May Help Manage Interest Rate Risk

Corporate FRNs offer a way to generate income while reducing sensitivity to rate changes. Although investors remain exposed to credit risk and spread volatility, FRNs allow returns to adjust with prevailing short-term rates rather than remaining locked into a fixed yield.

FRNs can serve as a low-duration income allocation for investors seeking yield with limited sensitivity to interest rate movements.

How to invest in FRNs

VanEck IG Floating Rate ETF (FLTR) delivers access to investment grade corporate floating rate notes. FLTR’s underlying index has a bias towards longer-maturity notes, which tend to have greater yield while maintaining relatively low interest rate sensitivity.

To receive more Income Investing insights, sign up in our subscription center.

By Nicolas Fonseca, CFA

Originally published February 18, 2026

Originally published on ETF Trends

For more news, information, and strategy, visit the Beyond Basic Beta Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

IMPORTANT DISCLOSURES

Index Descriptions:

MVIS® US Investment Grade Floating Rate Index (MVFLTR): iA modified market capitalization-weighted index that consists of U.S. dollar-denominated floating rate notes issued by corporate issuers and rated investment grade.

This is not an offer to buy or sell, or a recommendation to buy or sell any of the securities, financial instruments or digital assets mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, tax advice, or any call to action. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results, are for illustrative purposes only, are valid as of the date of this communication, and are subject to change without notice. Actual future performance of any assets or industries mentioned are unknown. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. VanEck does not guarantee the accuracy of third party data. The information herein represents the opinion of the author(s), but not necessarily those of VanEck or its other employees.

An investor cannot invest directly in an index. Returns reflect past performance and do not guarantee future results. Results reflect the reinvestment of dividends and capital gains, if any. Certain indices may take into account withholding taxes. Index returns do not represent Fund returns. The Index does not charge management fees or brokerage expenses, nor does the Index lend securities, and no revenues from securities lending were added to the performance shown.

An investment in the Fund may be subject to risks which includes, among others, foreign securities, foreign currency, credit, interest rate, floating rate, restricted securities, financials sector, special risk considerations of investing in United Kingdom, European, and Australian issuers, market, operational, sampling, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount and liquidity of fund shares, non-diversified, and index-related concentration risks, all of which may adversely affect the Fund.

The VanEck IG Floating Rate ETF, which is based on the Floating Rate Index, is not issued, sponsored, endorsed, sold or marketed by ICE Data, and ICE Data makes no representation regarding the advisability of investing in such product.

Investing involves substantial risk and high volatility, including possible loss of principal. Bonds and bond funds will decrease in value as interest rates rise. An investor should consider the investment objective, risks, charges and expenses of the Fund carefully before investing. To obtain a prospectus and summary prospectus, which contains this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.

© 2026 VanEck Securities Corporation, Distributor, a wholly owned subsidiary of Van Eck Associates Corporation.

VanEck Bitcoin ETF (“HODL”), VanEck Ethereum ETF (“ETHV”), VanEck Solana ETF (“VSOL”), and VanEck Merk Gold ETF (“OUNZ”) (collectively, the “Trusts”): This material must be preceded or accompanied by a prospectus: (HODL: Prospectus, ETHV: Prospectus, VSOL: Prospectus, OUNZ: Prospectus). An investment in the Trusts involves significant risk and may not be suitable for all investors. Loss of principal is possible. Before investing, you should carefully consider each Trust’s investment objectives, risks, charges, and expenses. Please read the prospectuses carefully before you invest.

The Trusts are not investment companies registered under the Investment Company Act of 1940 (“1940 Act”) or commodity pools for the purposes of the Commodity Exchange Act (“CEA”). Shares of the Trusts are not subject to the same regulatory requirements as mutual funds. As a result, shareholders of the Trusts do not have the protections associated with ownership of shares in an investment company registered under the 1940 Act or the protections afforded by the CEA.

The Sponsor for HODL, ETHV, and VSOL is VanEck Digital Assets, LLC. The Sponsor for OUNZ is Merk Investments, LLC. The Marketing Agent for HODL, ETHV, VSOL, and OUNZ is Van Eck Securities Corporation. VanEck Digital Assets, LLC and Van Eck Securities Corporation are wholly-owned subsidiaries of Van Eck Associates Corporation.

The principal risks of investing in VanEck ETFs and mutual funds include, but are not limited to, sector, market, economic, political, foreign currency, world event, index tracking, active management, social media analytics, derivatives, blockchain, commodities and non-diversification risks, as well as fluctuations in net asset value and the risks associated with investing in less developed capital markets. VanEck ETFs may also be subject to authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount risk and liquidity of fund shares risks. VanEck ETFs or mutual funds may loan their securities, which may subject them to additional credit and counterparty risk. ETFs or mutual funds that invest in high-yield securities are subject to subject to risks associated with investing in high-yield securities; which include a greater risk of loss of income and principal than funds holding higher-rated securities; concentration risk; credit risk; hedging risk; interest rate risk; and short sale risk. ETFs or mutual funds that invest in companies with small capitalizations are subject to elevated risks, which include, among others, greater volatility, lower trading volume and less liquidity than larger companies. Please see the prospectus of each Fund for more complete information regarding each Fund’s specific risks.

Investing involves risk including possible loss of principal. Bonds and bond funds will decrease in value as interest rates rise. An investor should consider the investment objective, risks, charges and expenses of a fund carefully before investing. To obtain a prospectus and summary prospectus, which contain this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.

This website is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this website. Nothing on this website should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

VanEck mutual funds and ETFs are distributed by Van Eck Securities Corporation, Distributor, a wholly owned subsidiary of Van Eck Associates Corporation.

666 Third Avenue | New York, NY 10017

© 2026 VanEck. VanEck®, VanEck Access the opportunities®, and the stylized VanEck design® are trademarks of Van Eck Associates Corporation.

© VanEck

Read more commentaries by VanEck