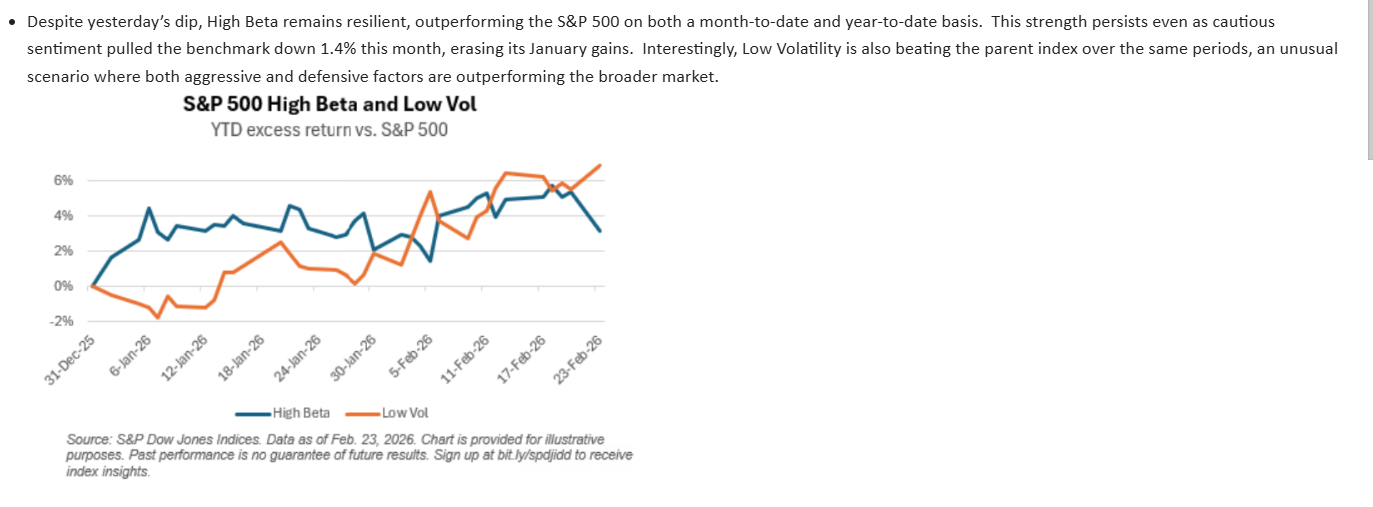

In a notable shift for the start of 2026, the S&P 500 is experiencing a divergence in factor performance. Typically, high beta (aggressive, high-risk) and low volatility (defensive, safe-haven) factors sit on opposite sides of the seesaw. When one goes up, the other usually comes down.

However, as of late February 2026, both the Invesco S&P 500 Momentum ETF (SPMO) — which currently overlaps heavily with high beta — and the Invesco S&P 500 Low Volatility ETF (SPLV) are outperforming the broad benchmark, the iShares Core S&P 500 ETF (IVV).

SPMO and the “Winner-Takes-All” AI Cycle

The outperformance of high beta (captured by SPMO’s current basket) is a continuation of the AI Supercycle that dominated 2025. While the broader S&P 500 felt the sting of a 1.4% dip in February, the top-tier momentum names — predominantly NVIDIA, Broadcom, and Meta — have remained resilient. These companies aren’t just trading on hype; they are delivering the 13–15% earnings growth that investors are desperate for in a “sticky inflation” environment.

Interestingly, because the S&P 500 has become so concentrated in tech, the index itself now behaves like a high beta vehicle. SPMO simply supercharges this effect by weeding out the 400+ laggards that are weighing down the parent index.

Why SPLV Is Surging

The rise of low volatility (SPLV) appears to be the insurance policy investors are buying in real-time. After several rate cuts in late 2025, the Federal Reserve paused in early 2026. This has created a “simultaneous hold” at relatively high interest rates. When the market realizes rates won’t hit zero anytime soon, capital flows into stable sectors like consumer staples and utilities — the bread and butter of SPLV.

With a recession probability looming for later in 2026, institutional smart money is quietly rotating into low-beta stocks to mitigate potential downside, even as they keep their momentum moonshot bets active.

The “Unusual Scenario”: A Barbell Market

The chart shows an “unusual scenario” because we are seeing a barbell market. Investors are effectively abandoning the “middle” of the S&P 500.

The current market regime has created a “hollowed-out” S&P 500, where the broad index (IVV) is effectively being squeezed by its own extremes. On one end of the barbell, momentum (SPMO) is winning by capturing the pure, high-octane alpha of the AI infrastructure boom. By concentrating exposure in high-performing technology and communications names, SPMO bypasses the broader market’s dead weight to ride the winners-take-all earnings cycle.

On the other end, low volatility (SPLV) is thriving as a sophisticated hedge against “sticky” inflation and the Federal Reserve’s unpredictable policy path. Investors are flocking to the relative safety to protect capital as recessionary signals flicker.

Meanwhile, the broad S&P 500 (IVV) is caught in the crossfire. It is currently being dragged down by a “diversification penalty” — weighted heavily with struggling mid-caps and zombie companies that possess neither the explosive growth of momentum nor the defensive moats of low volatility. In this environment, the “middle of the road” is proving to be the most dangerous place to park capital.

For now, the winning play isn’t buying the market. Rather, it appears to be picking a side. Whether you want SPMO or SPLV, the data shows that staying in the middle of the road is currently the slowest way to travel.

Originally published on ETF Trends

For more news, information, and analysis, visit ETF Trends.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi