By the end of 2025, the US equity market was narrower for longer than during the Technology Bubble. One might think that an extreme market for such a long time might result in some strange valuations and interesting investment opportunities, and it indeed has.

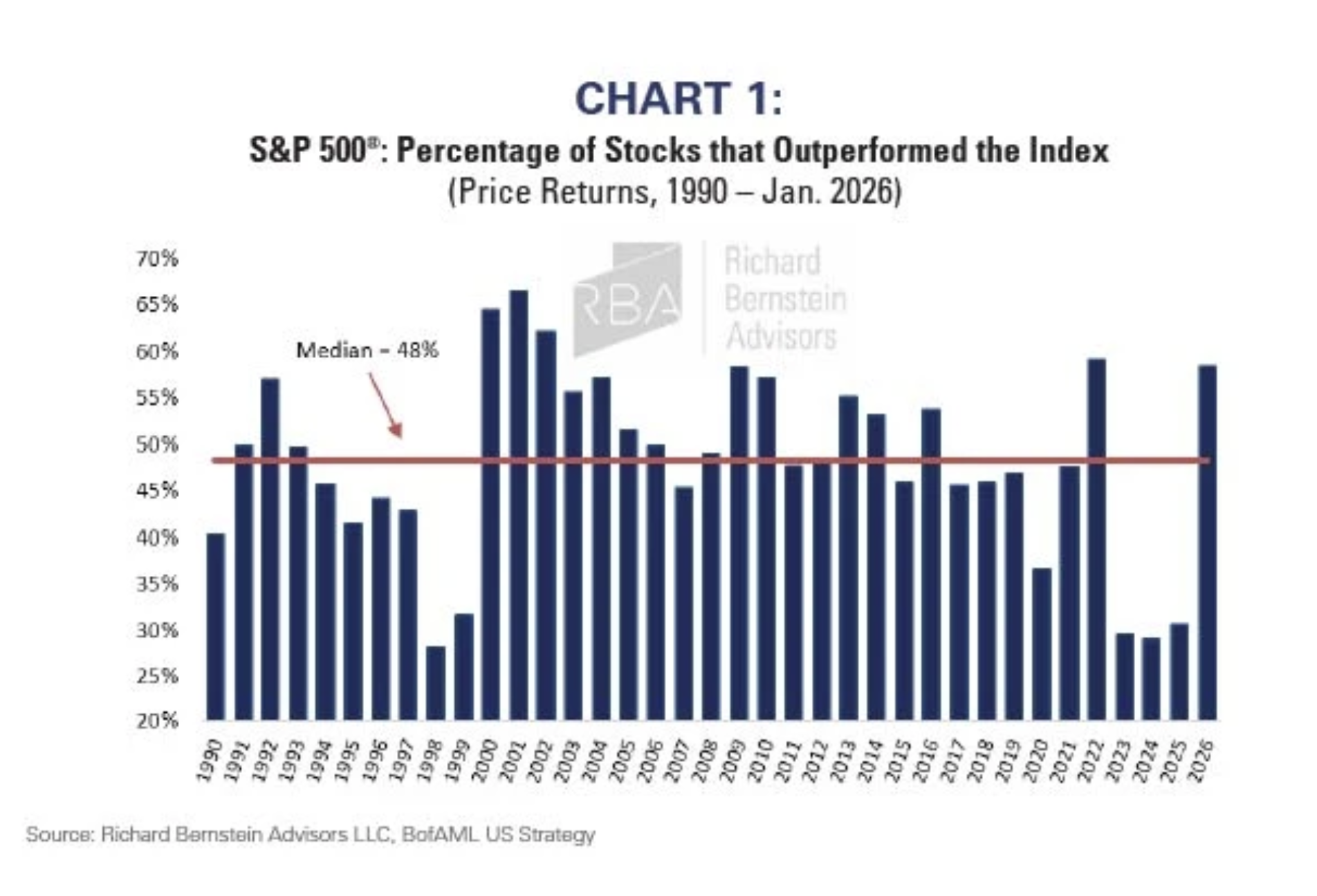

Chart 1 shows the percentage of stocks within the S&P 500® that outperformed the market by year. The period from 2023 to 2025 was the longest stretch of narrow leadership in the chart’s history. Leadership has finally begun to broaden in 2026.

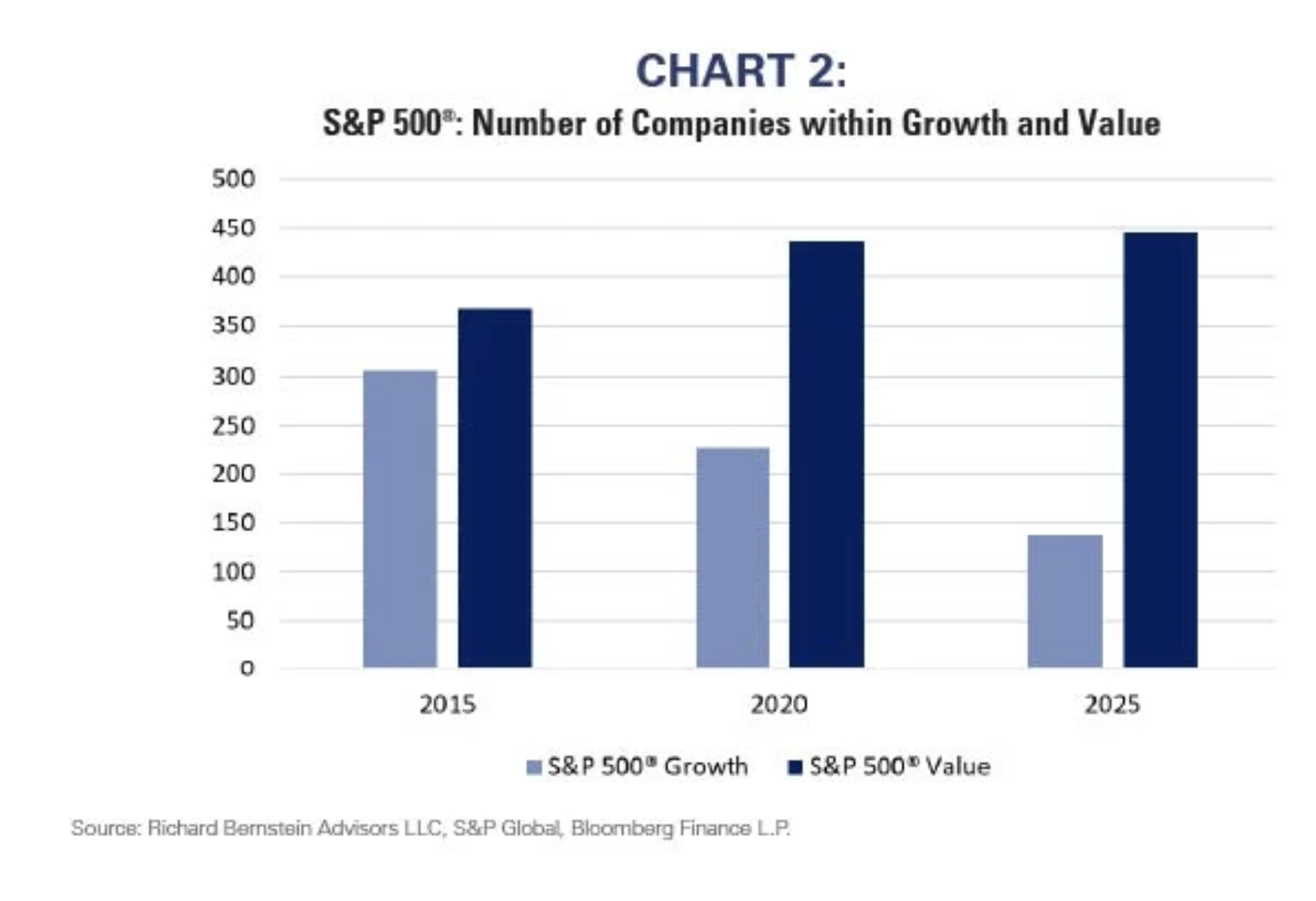

The extended period of narrow leadership has skewed the number of companies within the S&P 500® Growth and Value Indices. Chart 2 highlights that in 2015 roughly 300 S&P 500® companies were in the Growth Index (Note: companies can be in both indices so the combination of the Growth and Value indices will not sum to 500). By 2020, the number of growth companies had fallen to roughly 225. The narrow leadership of the past several years has led to under 140 companies in the current growth index.

On the other hand, nearly 450 of the S&P 500® companies are now included in the value index.

Historically narrow leadership means that about 90% of the S&P 500® companies now qualify as value stocks!

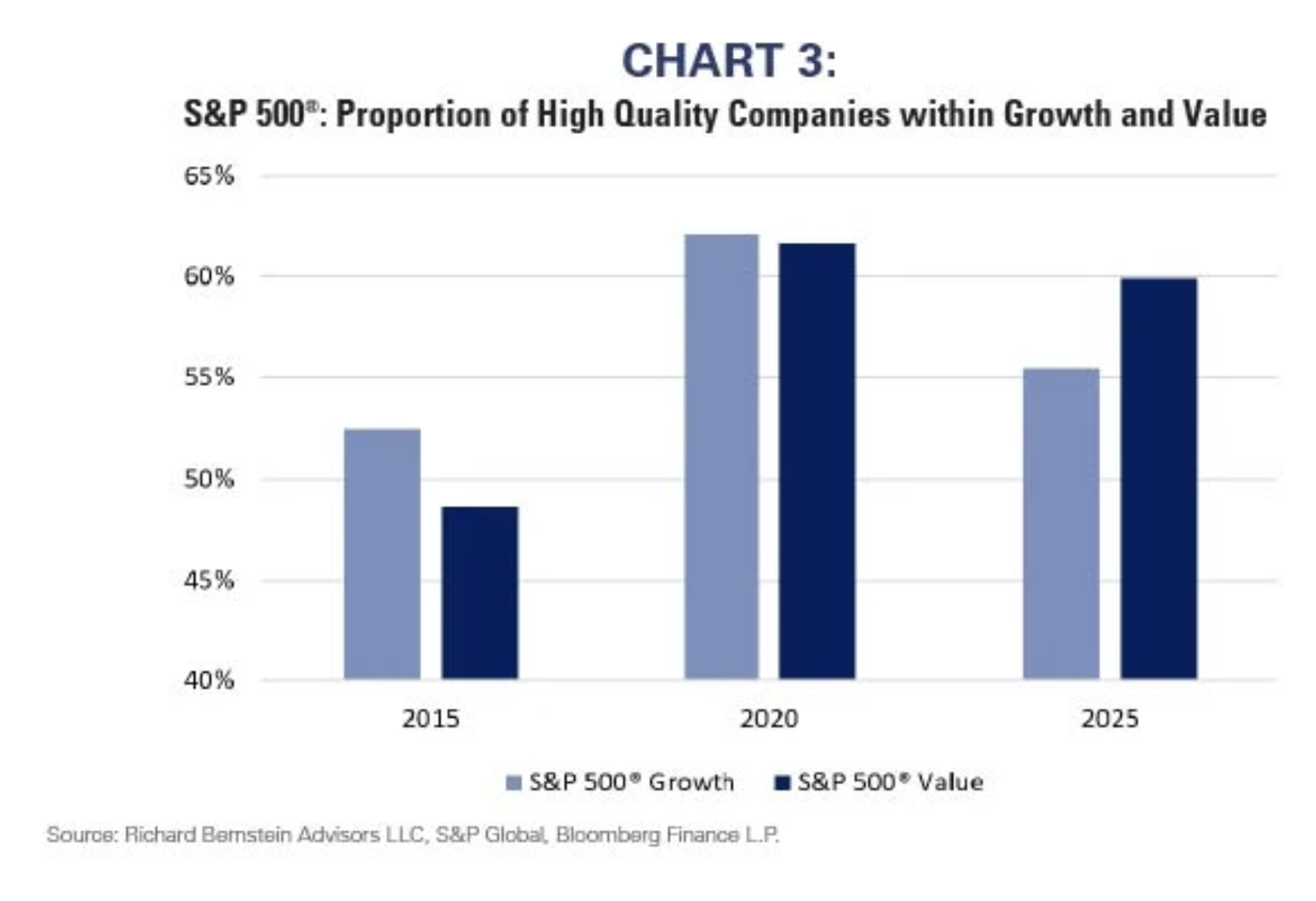

More high quality companies are now value

Normally, investing in the highest quality companies requires paying a premium valuation for those companies’ superior balance sheets and cash flows. However, as one might expect when 90% of the S&P 500® qualifies as value, many high quality US companies qualify as undervalued. No longer does one have to pay a premium price for superior balance sheets.

Chart 3 demonstrates that Growth contained a larger proportion of higher quality stocks than Value did in both 2015 and 2020, but today that has been reversed. About 60% of the Value universe is now comprised of higher quality companies.

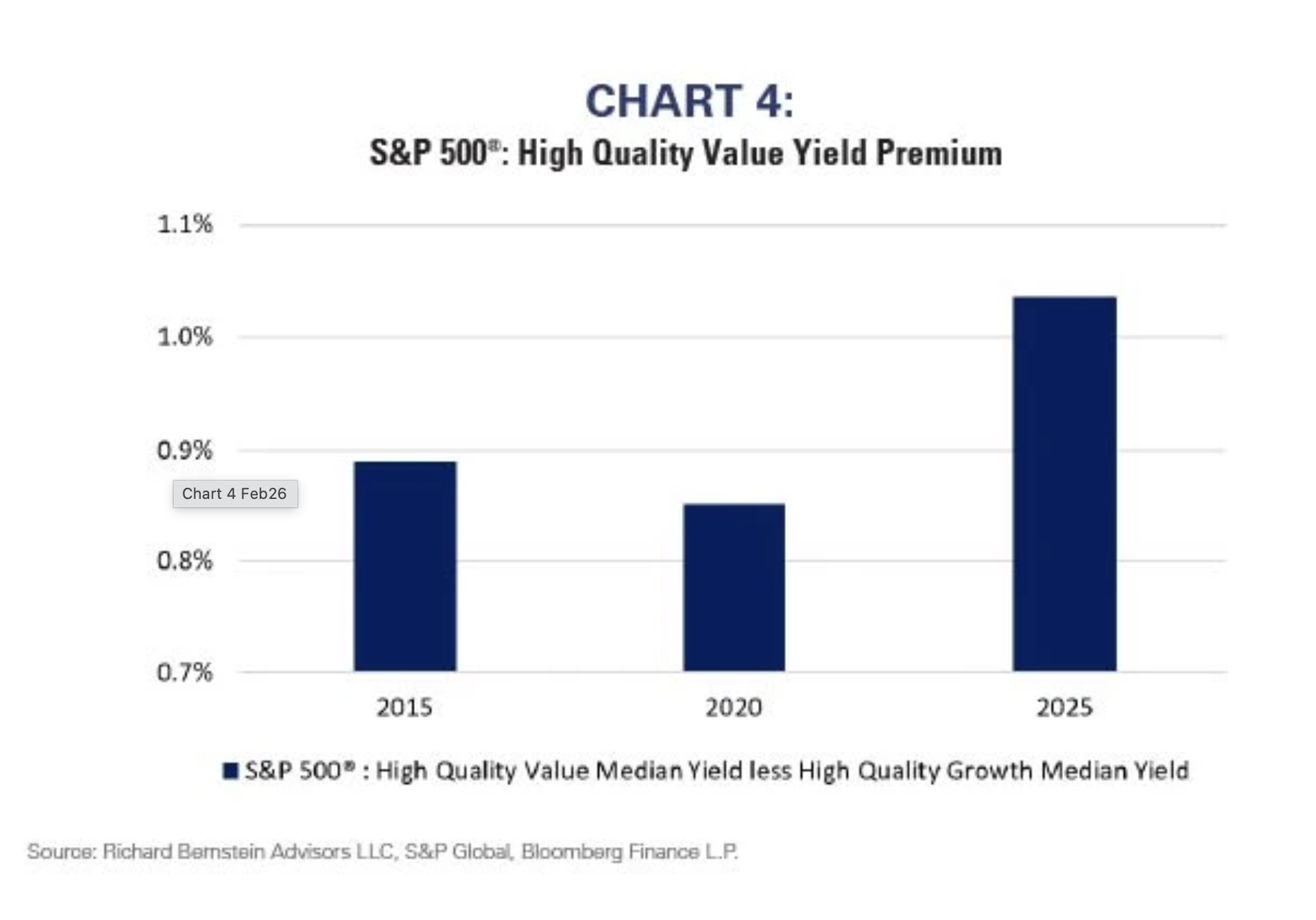

Quality = Yield

Financial theory says that companies must decide between paying out profits to shareholders as dividends or reinvesting cash flows back into their business through capital spending or share buybacks. As a result, investors prefer that slower growing companies pay dividends so investors can reinvest in other companies with superior growth opportunities.

This tends to result in a trade off between quality growth and dividend yield with the stocks of higher quality, faster growing companies tending to have lower dividend yields. The opportunity to invest in a high quality stock with above average dividend yield is not the norm.

Because of the historically long period of narrow leadership, investors today do not have to decide between quality and dividends! Chart 4 shows that high quality stocks in the value universe currently have a meaningfully higher dividend yield than high quality stocks in the growth universe. Although there is generally a yield premium for value-oriented, higher-quality stocks, the premium is currently higher than it has been over the past decade.

Shifting portfolios

RBA’s portfolios have been geared to the market broadening, and our shifts toward US quality, dividends, value, and non-US reflect some of the opportunities presented in these charts, and our general belief that profit fundamentals increasingly support a broadening of the global equity markets.

The historically narrow equity market clearly ignored the breadth of earnings data, which showed many more than seven growth stories in global equity markets. That narrowness became so extreme that quality now seems quite undervalued. The recent broadening of the global equity markets might be signaling that investors are starting to agree.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors