If trade policy were like a boxing match, the U.S. had hoped tariffs would be a decisive, knockout blow. While many of America’s trading partners reeled, they stayed on their feet and are wearing down their opponent.

Last Friday, the U.S. Supreme Court moved to curtail the use of emergency economic powers to enforce tariffs. The ruling does little to change the broader trade posture as alternative legal pathways remain, but it underscores a deeper point: policy has become a source of uncertainty as much as leverage. Tariffs are looking more like a drawn‑out exchange in which all sides will be bruised.

Despite this, growth across major economies has proven more resilient than expected, carried by domestic demand and easier policy settings.

Following are our thoughts on how top markets are faring.

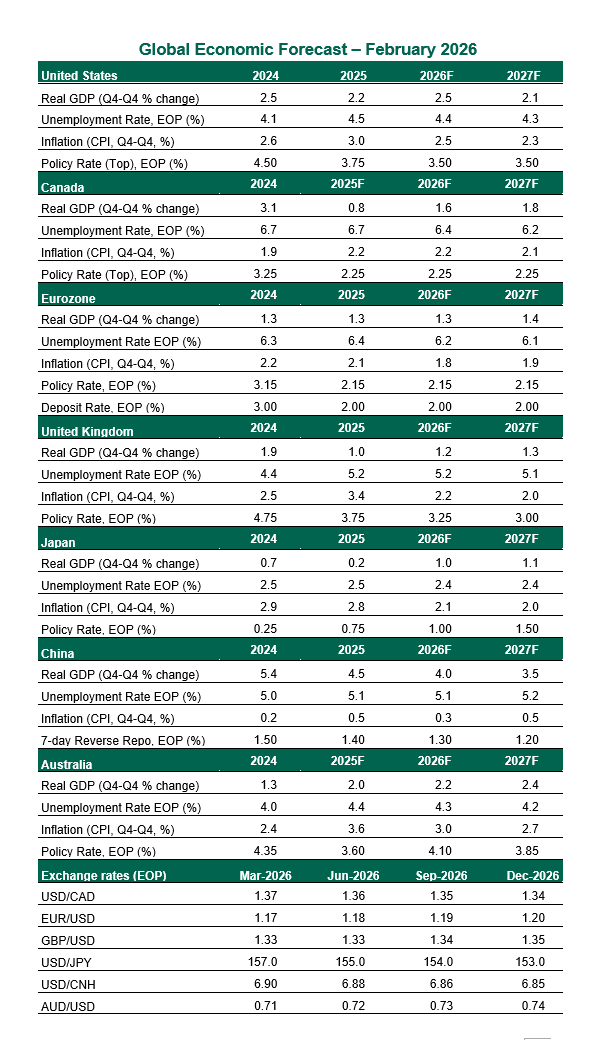

United States

- After two quarters of outperformance, U.S. growth downshifted in the fourth quarter, with real gross domestic product (GDP) expanding at a 1.4% annualized pace. The slowdown was driven largely by a sharp pullback in government spending tied to the October–November shutdown. Consumer spending remained the economy’s main engine. The economy clocked a solid 2.2% expansion last year, demonstrating resilience which should remain on display this year. The Supreme Court tariff decision does not alter our growth outlook for the year ahead.

- At its January meeting, the Federal Open Market Committee left the federal funds rate and balance sheet policies unchanged. Two dissents in favor of a rate cut suggest additional easing is likely later this year, though there is little urgency. We expect one further rate reduction around midyear. The nomination of Kevin Warsh as Fed chair does little to alter that outlook. While Warsh has expressed firm views on the Fed’s role in financial markets, any move toward balance sheet reduction would likely be cautious and incremental.

Canada

- The Canadian economy lost momentum late in 2025 as tariffs, trade uncertainty, and slower population growth weighed on activity. The labor market reflects that cooling: employment fell at the start of the year. The Canadian unemployment rate dipped to 6.5%, largely owing to a shrinking labor force, pointing to persistent slack rather than renewed strength. Growth this year will be supported by sizable federal fiscal measures, but Canada’s outlook remains tightly linked to the upcoming US‑Mexico‑Canada Agreement (USCMA) review.

- The Bank of Canada appears comfortable that current interest rate settings are sufficiently restrictive to keep inflation anchored while the economy works through excess slack. We expect the central bank to stay on hold at the lower end of its neutral range over the forecast horizon. However, a renewed softening in growth or a more pronounced deterioration in labor market conditions would likely reopen the door to a modestly more accommodative stance.