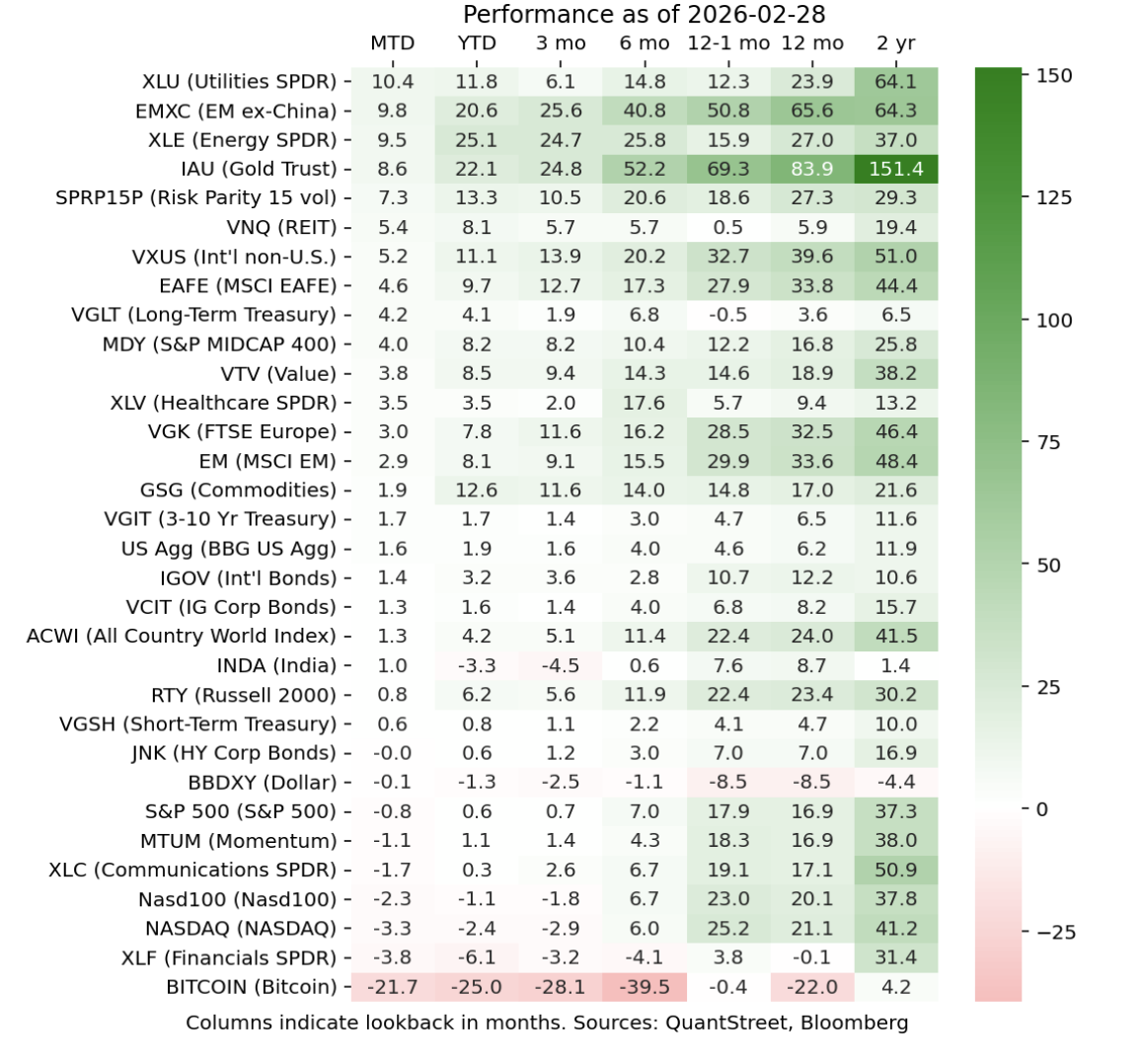

AI fatigue has taken hold of financial markets. The companies powering the AI revolution (Nvidia, Google, Microsoft) were down. The companies that are being (or might be) disrupted by AI, like software makers, were also down. Bitcoin, with no obvious connection to the AI nexus, also took a beating. Financials, while benefiting from the Trump administration's deregulatory agenda, sold off on concerns about private credit hiccups (like the Blue Owl fund redemption gate and the insolvency of MFS in the UK). The winners included utilities, energy (on the back of concerns about a US attack on Iran, which started on February 28, 2026), gold, and most things international. The dollar was flat on the month but investor preference for more non-US exposure continues unabated.

Our own views are unchanged. We are constructive on US markets. The AI boom is in its early innings. The capabilities of these technologies are mind boggling (see discussion below), and computational resources, power, and distribution capabilities need to be built to support AI adoption, which is happening at a breakneck speed, far exceeding adoption curves of previous technologies. At the same time, the One Big Beautiful Bill Act will provide fiscal stimulus, the Trump administration deregulatory agenda will move forward, the resurgent M&A cycle will continue, and corporate America is starting from a low leverage point, so has room to add on debt to finance the AI buildout. Finally, we anticipate a continued positive impact from an accommodative Fed.

An important negative is that equity valuations are high in the US, but our view is that the market is pricing in high growth not low returns. In light of the above list of supportive factors for US markets, it would, in fact, be surprising if valuations were not high. Of course, high valuations and increasing leverage may yet prove to be a toxic mix, and other unanticipated risks may arise, but overall we believe it to be an attractive investment backdrop.

We are less sanguine on the dollar. As we wrote recently, dollar headwinds are building. Many in the world are frustrated with what they perceive to be unstable US foreign policy. The Trump administration’s messaging on Greenland was frustrating for many US allies. On top of this, the Trump administration prefers a weaker dollar, because this will improve the US trade balance: our stuff will become cheaper and the rest of the world’s stuff will become more expensive for the US consumer. The tension here, of course, is that the Trump administration also wants lower rates and thus needs lower inflation. So there is a limit to their dollar weakness policy. While it is not possible for the rest of the world to dispose of their dollar assets—and frankly I don’t think they really want to—at the margin, the demand for US securities, especially fixed income securities, will likely be diminished. This is the message from the gold market and seems consistent with the dollar slowly losing its status as the world’s only reserve currency.

Our general views, bullish on risk assets but negative on the dollar, are reflected in our portfolio’s increased international allocations (the highest since we launched) and baseline risk exposures. This allocation is supported by our qualitative views, as discussed above, as well as our systematic asset allocation process. This month, we also initiate a small allocation to Japanese stocks. You can see our historical performance here.

AI at QuantStreet

Our philosophy at QuantStreet is to lever data and technology to try to help our clients with their wealth management and investing needs. One important way in which we do this is to make sure that we stay on top of the latest economic developments. Of course, we are avid news readers, but as I’ve argued in the past, it is not possible for one person (or even a team of people) to keep up with all of the relevant news flow for an investment portfolio. In our monthly portfolio allocation process, we already have an AI model (Gemini) review stored news headlines from the prior month to see if any of them adversely impact our proposed portfolio positions. We only proceed if our portfolios are not contraindicated by recent news flow.

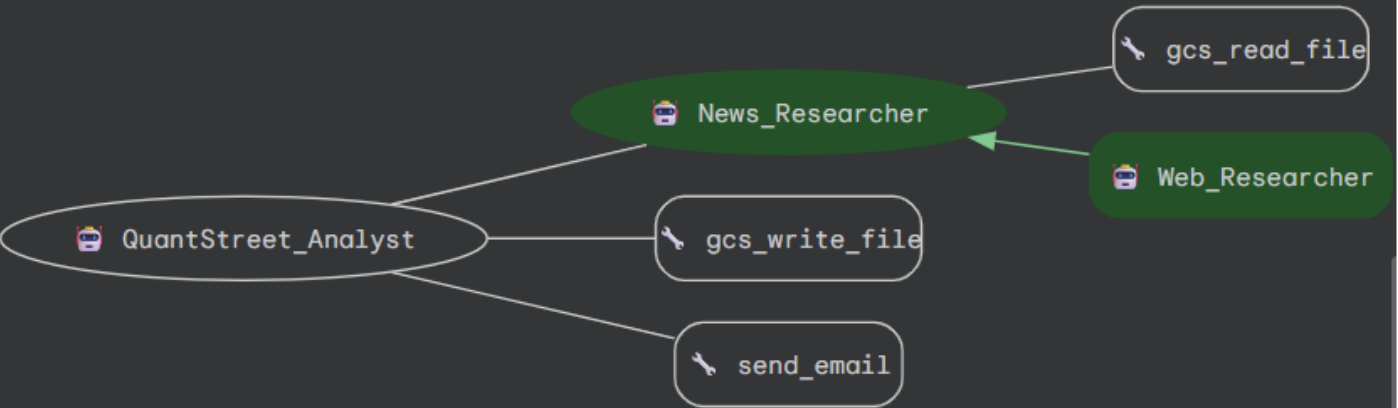

To improve our ability to monitor news flow, we recently introduced an agentic AI process using Google’s ADK (agent development kit) to monitor news flow daily. The following schematic, generated by Google’s ADK, demonstrates the work flow:

At 9:45pm New York time, QuantStreet_Analysis wakes up and calls another agent, News_Researcher, to scan and summarize the day’s news. News_Researcher calls a third agent, Web_Researcher, to use Google’s search capabilities to scan the internet for the day’s important news. News_Researcher then calls a tool called gcs_read_file to read in QuantStreet’s latest portfolio positions, and then creates a summary of the day's news and how it’s relevant to QuantStreet’s positions. This information is then passed back to QuantStreet_Analyst which uses a tool (gcs_write_file) to save the information on our cloud storage for future reference. As the final task, QuantStreet_Analyst uses another tool (send_email) to email this summary to us for our review.

This process happens in 2-3 minutes on a nightly basis, and replaces what a human analyst would be able to accomplish with 2-3 hours of work. We live in a world where this sort of thing feels commonplace, but if you take a step back and think about it, it is mind boggling that this is possible. If you would like to learn more about our news monitoring process, please reach out.

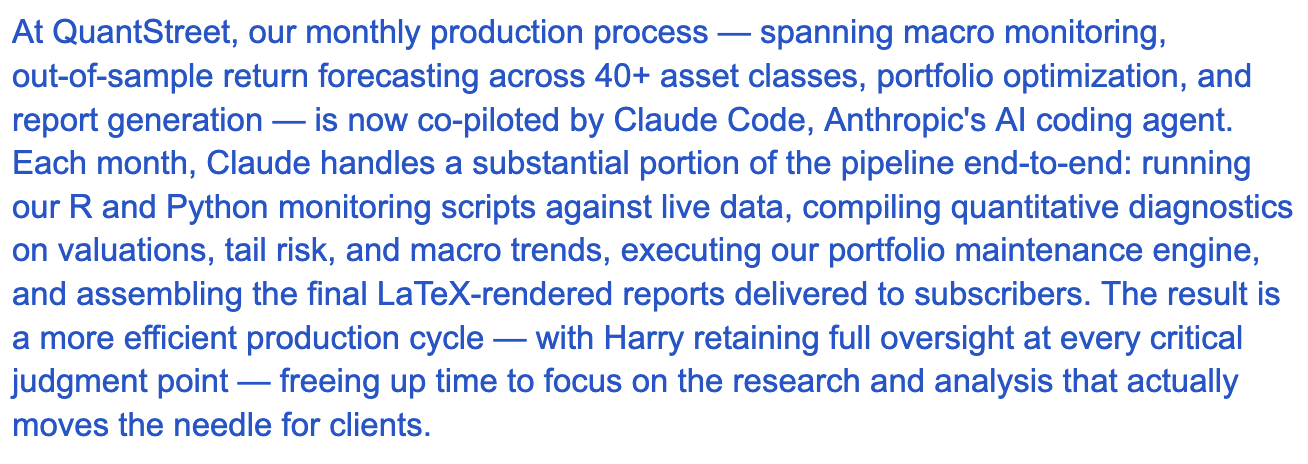

As of this week, we’ve also brought on Claude Code to help us automate and improve our workflows. After working with Claude Code for the last few days, I can only say “WOW!” The world after AI will be a different place from the world before AI. Just to show off a little, here is Claude’s (slightly edited) explanation of the process:

Of course, AI is not infallible. There are some tasks that Claude isn’t great at. And mistakes can happen, even with an AI agent. In addition, automating parts of the production process requires care and oversight on our part; the agent can’t just run autonomously. Nevertheless, this is a step up in our capabilities, which we believe will enable us to better serve our clients.

Working with QuantStreet

QuantStreet is a registered investment advisor. Registration does not imply a certain level of skill or training. QuantStreet offers wealth planning, separately managed accounts, model portfolios and portfolio analytics, as well as financial consulting services. The firm’s approach is systematic, data-driven, and shaped by years of investing experience. To work with or learn more about QuantStreet, join our mailing list or contact us at [email protected].

Please keep in mind that all financial forecasts are fraught with risk and uncertainty. Our views may prove incorrect and market outcomes may be materially worse than we anticipate. Please see our full disclosure about the limitations of forward-looking statements and the risks of investing at https://quantstreetcapital.com/blog_disclosure/.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© QuantStreet Capital

Read more commentaries by QuantStreet Capital