Five Catalysts for International Value Stocks in 2026 and Beyond

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

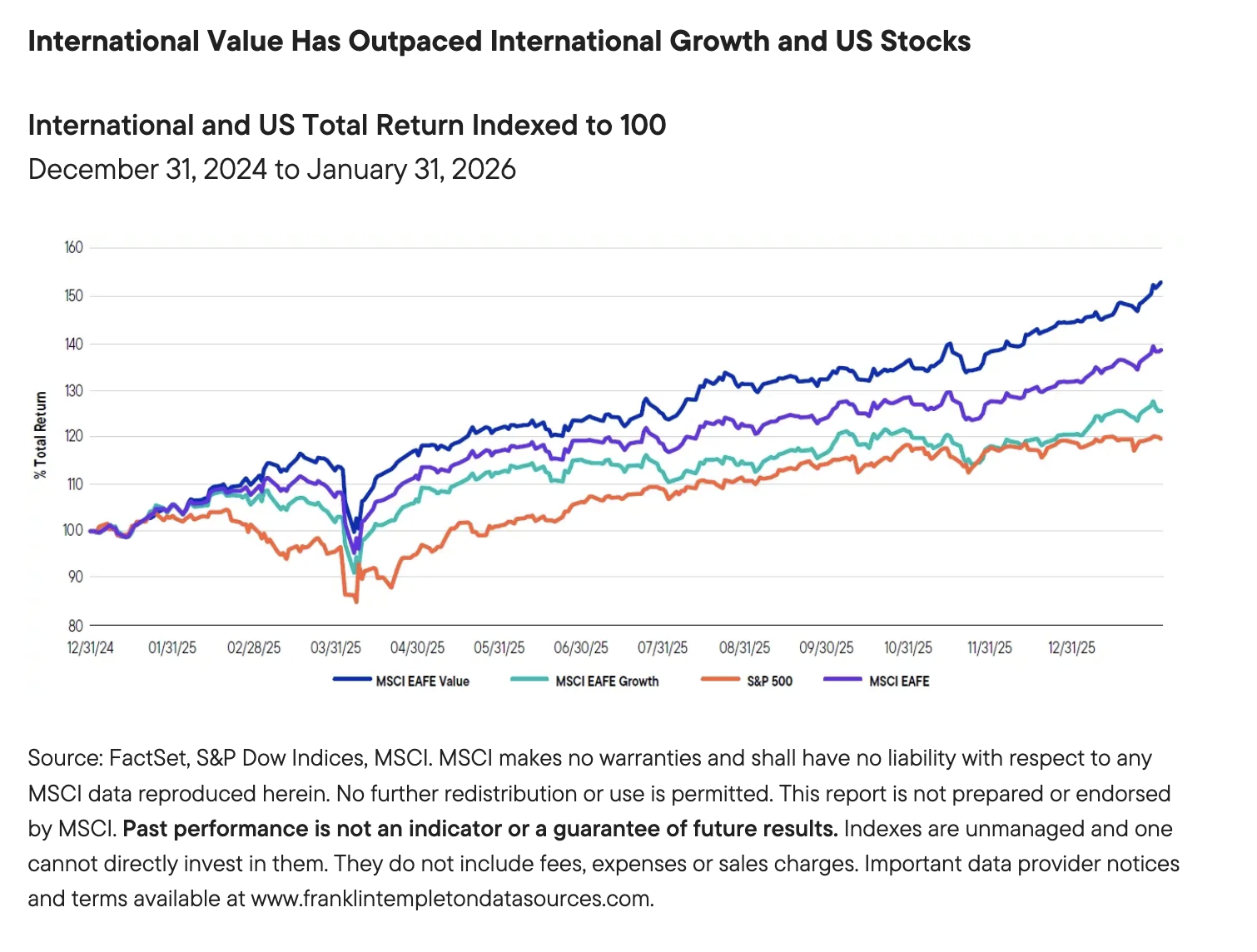

While the artificial intelligence trade (AI) has commanded the spotlight, international value stocks steadily advanced in 2025, outperforming US stocks.

Last year’s renewed momentum is not an anomaly, in our view, but rather the early stages of a durable, long-term transformation.

Here are five catalysts that we think will continue to drive international value stocks in 2026 and beyond and why allocating to international value may help to diversify investors’ hefty US equity exposure.

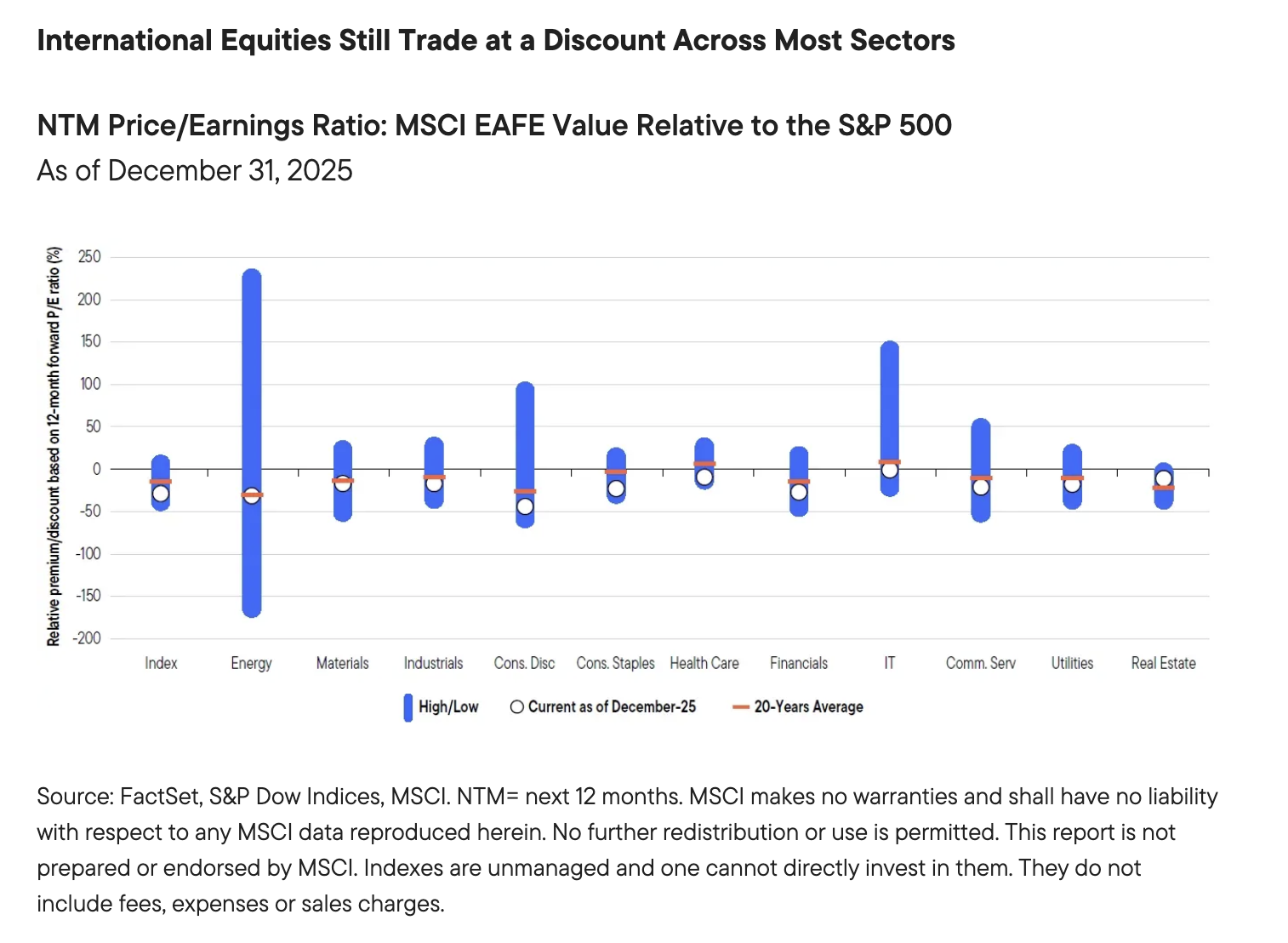

1. Fundamentals set the stage

Valuations for international equities remain historically attractive relative to US stocks across sectors, even after 2025 gains. But it’s not just about being “cheap.” At current prices, we see room for substantial re-rating, with policy shifts and structural reforms acting as catalysts for corporate earnings growth.

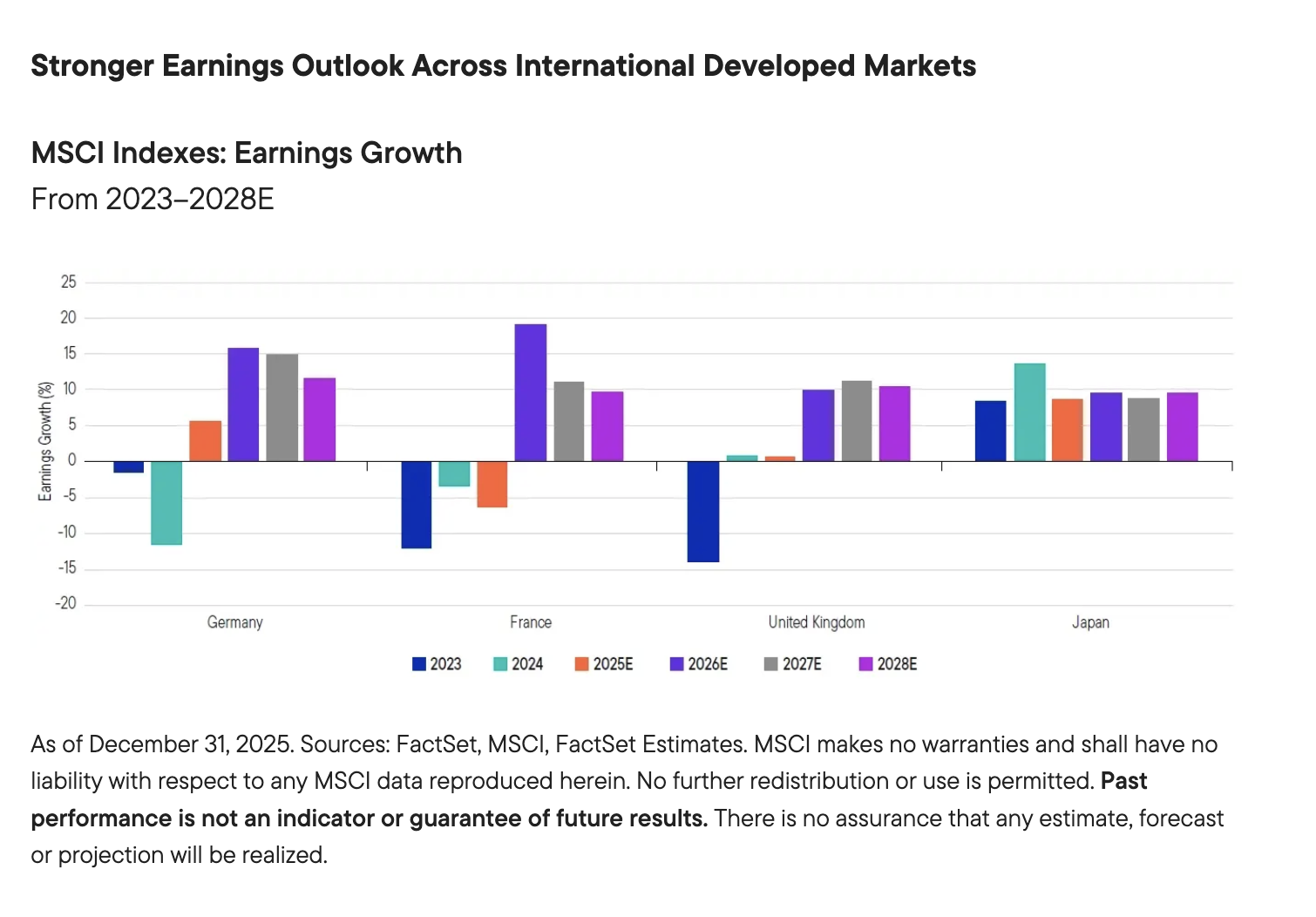

2. Earnings growth should accelerate for international value companies

International stocks are often associated with sectors like financials, industrials, materials and energy—industries that tend to see earnings and revenue accelerate as economic activity strengthens. Rising capital investment and government and corporate reforms across key markets point toward a broad-based pickup in earnings growth. Furthermore, we expect trade uncertainty to abate as companies and countries adapt, through negotiations or supply-chain realignment, to reduce their exposure to US tariff risks, providing more fuel to propel earnings growth in the coming year.

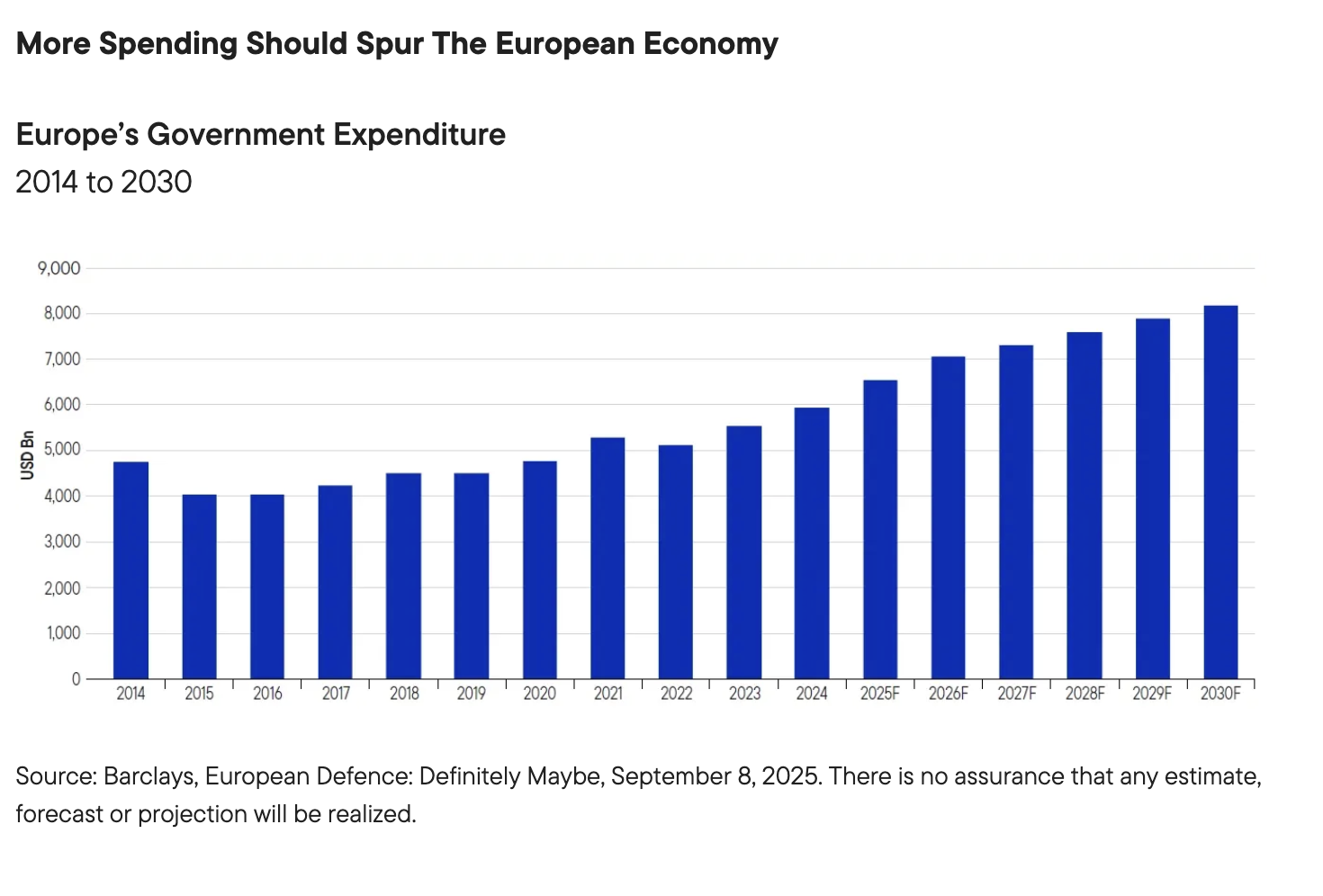

3. Fiscal tailwinds in Europe

After years of fiscal restraint, efforts to strengthen Europe’s economic resilience and competitiveness are driving increased investment in infrastructure, technology modernization and stronger defense capabilities. We believe these forces will continue to support select European companies positioned to benefit in an era of reinvestment.

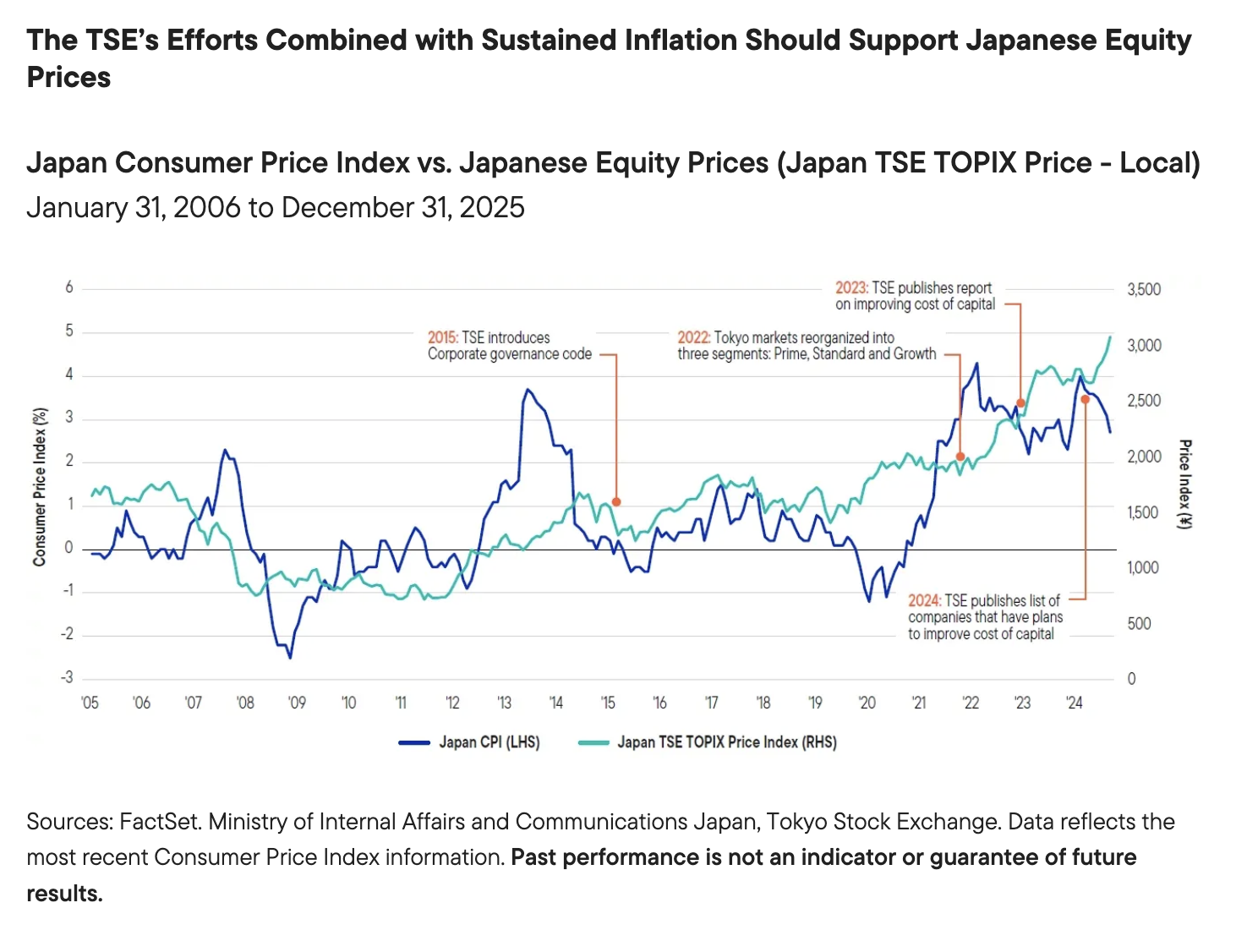

4. Transformation in Japan

Japan’s long-planned structural reforms are bearing fruit. And despite political shifts, new Prime Minister Sanae Takaichi’s policies are geared toward supporting growth. Coupled with efforts already pushed forward by the Tokyo Stock Exchange, the country seems committed to attracting investors. We think this persistence will help to unlock value in long overlooked Japanese stocks.

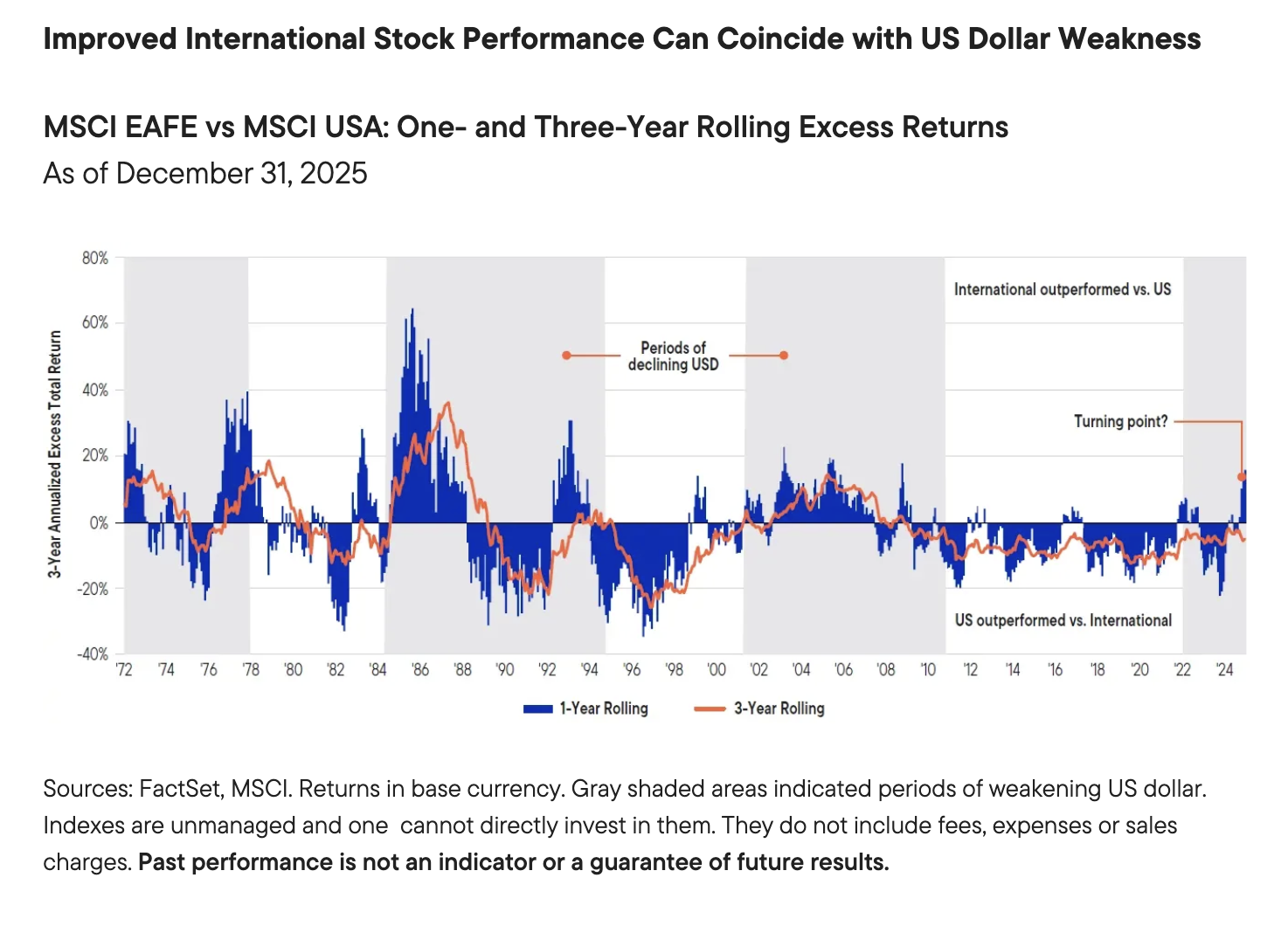

5. Currency dynamics could offer a boost

If the US dollar (USD) continues to soften, international companies could see an added boost to returns. A weaker dollar enhances the value of foreign earnings for US-based investors and often coincides with stronger global economic activity—both supportive of international equity performance.

Long-term transformation taking shape

Taken together, solid fundamentals, rising fiscal support in Europe, ongoing structural reform in Japan, improving corporate earnings and a weakening US dollar suggest to us that the conditions for international equity performance are grounded in tangible, transformative forces. While risks remain, we see a multi-year environment in which international markets could continue to narrow the performance gap relative to the United States.

INDEX DEFINITIONS

Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges.

The MSCI EAFE Value Index captures large and mid cap securities exhibiting overall value style characteristics across Developed Markets countries around the world, excluding the US and Canada.

The S&P 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

The MSCI EAFE Growth Index captures large and mid cap securities exhibiting overall growth style characteristics across Developed Markets countries around the world, excluding the US and Canada.

The MSCI EAFE Index captures large and mid cap securities across Developed Markets countries around the world, excluding the US and Canada.

The MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market.

The MSCI Europe Index captures large and mid cap representation across Developed Markets (DM) countries in Europe.

The MSCI Germany Index is designed to measure the performance of the large and mid cap segments of the German market.

The MSCI France Index is designed to measure the performance of the large and mid cap segments of the French market.

The MSCI United Kingdom Index is designed to measure the performance of the large and mid cap segments of the UK market.

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market.

The Tokyo Stock Price Index (TOPIX) is a comprehensive, free-float adjusted market capitalization-weighted index tracking nearly all domestic common stocks on the Tokyo Stock Exchange (TSE) Prime Market.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

The investment style may become out of favor, which may have a negative impact on performance.

Equity securities are subject to price fluctuation and possible loss of principal. There can be no assurance that multi-factor stock selection process will enhance performance. Exposure to such investment factors may detract from performance in some market environments, perhaps for extended periods.

Active management does not ensure gains or protect against market declines.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

Large-capitalization companies may fall out of favor with investors based on market and economic conditions

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Investments in companies engaged in mergers, reorganizations or liquidations also involve special risks as pending deals may not be completed on time or on favorable terms.

Dividends may fluctuate and are not guaranteed, and a company may reduce or eliminate its dividend at any time.

WF: 9001562

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All