Iran Conflict Continues to Pressure Markets as Oil Surges and Growth Risks Rise

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- Oil briefly surged above $100 per barrel, moving the Iran conflict’s impact from market volatility into the realm of macroeconomic risk.

- Growth risks are now assessed as moderate, with headwinds expected in the U.S. and more notable drags across Europe and Asia.

- The Fed is unlikely to cut rates proactively, given upside inflation risks.

- Market sentiment has still not reached a panic.

- Strategic positioning remains unchanged while tactical flexibility is prudent.

The ongoing conflict involving Iran and the disruption to energy markets has moved beyond headline risk and is now influencing expectations for growth, inflation and policy. As of March 9, oil prices briefly breached the $100 per barrel threshold — a development that shifts the macro conversation compared to last week.

What happened in the first week of the conflict?

During the first week, energy markets absorbed the most visible impact. Crude oil briefly rose above $100 per barrel amid continued uncertainty surrounding flows through the Strait of Hormuz — a critical corridor for global crude and liquid natural gas (LNG) shipments.

Leadership dynamics inside Iran have also evolved. The country’s newly announced leader, Mojtaba Khamenei, is widely viewed as a hard-liner and seen as potentially extending the conflict, suggesting the risk of a protracted disruption to energy supplies has increased.

Our measure of investor sentiment moved from overbought to directionally slightly pessimistic last Friday for the first time since November. Even so, current conditions do not reflect panic or forced repositioning. Overnight selling pressure eased somewhat following reports that Saudi Arabia may offer additional crude supply via the Red Sea, though uncertainty around energy flows remains elevated.

How is this impacting markets going forward?

Sustained oil prices above $100 would shift the impact from a volatility event to a growth consideration.

At current levels, the drag on U.S. growth is estimated at approximately 0.5 percentage points. The impact is likely more pronounced outside the United States — particularly in Asia — where roughly 80–90% of crude and LNG transiting the Strait of Hormuz flows. In that context, growth risks have moved up from low to medium.

The ongoing conflict involving Iran and the disruption to energy markets has moved beyond headline risk and is now influencing expectations for growth, inflation and policy. As of March 9, oil prices briefly breached the $100 per barrel threshold — a development that shifts the macro conversation compared to last week.

What happened in the first week of the conflict?

During the first week, energy markets absorbed the most visible impact. Crude oil briefly rose above $100 per barrel amid continued uncertainty surrounding flows through the Strait of Hormuz — a critical corridor for global crude and liquid natural gas (LNG) shipments.

Leadership dynamics inside Iran have also evolved. The country’s newly announced leader, Mojtaba Khamenei, is widely viewed as a hard-liner and seen as potentially extending the conflict, suggesting the risk of a protracted disruption to energy supplies has increased.

Our measure of investor sentiment moved from overbought to directionally slightly pessimistic last Friday for the first time since November. Even so, current conditions do not reflect panic or forced repositioning. Overnight selling pressure eased somewhat following reports that Saudi Arabia may offer additional crude supply via the Red Sea, though uncertainty around energy flows remains elevated.

How is this impacting markets going forward?

Sustained oil prices above $100 would shift the impact from a volatility event to a growth consideration.

At current levels, the drag on U.S. growth is estimated at approximately 0.5 percentage points. The impact is likely more pronounced outside the United States — particularly in Asia — where roughly 80–90% of crude and LNG transiting the Strait of Hormuz flows. In that context, growth risks have moved up from low to medium.

Elevated energy prices also introduce renewed upside risks to inflation. That dynamic limits central bank flexibility. The Federal Reserve (Fed) is unlikely to come in proactively with rate cuts, similar to its approach during the April 2025 drawdown. We think policymakers would need to be convinced of imminent risks to growth before easing, especially given the possibility of a more sustained inflation overshoot.

Markets, therefore, face a backdrop of higher energy costs and limited monetary policy support. While investor sentiment has softened, it has not reached levels historically associated with systemic stress.

Updates to our positioning

At this time, we remain close to our strategic asset allocation targets. While growth risks have increased with oil near $100, the current environment does not show signs of disorderly market functioning. The key variable remains the duration of the conflict. If oil prices stabilize, the macro drag is likely manageable. If higher prices persist, the cumulative growth impact would become more significant, particularly in non-U.S. markets.

At this stage, we believe maintaining discipline while preserving tactical flexibility remains the most appropriate course.

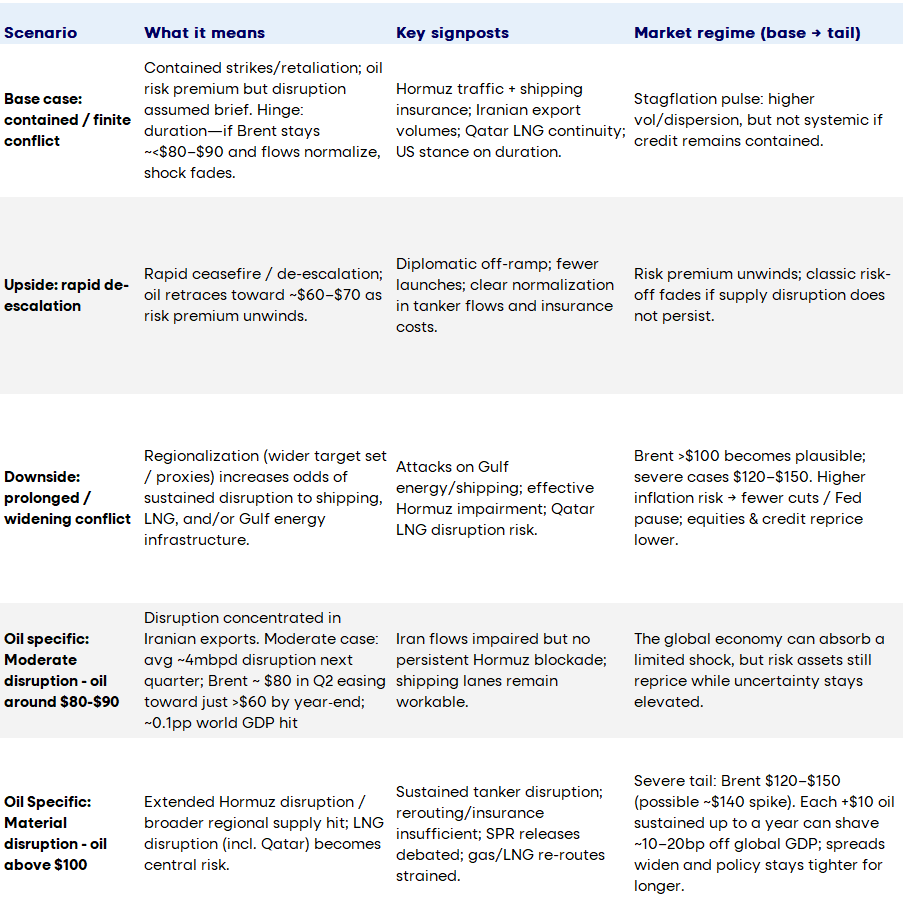

High-level scenarios

-

Base case

Oil prices remain elevated but do not move materially higher, and disruption through the Strait of Hormuz is not sustained at levels that severely impair global supply. Growth slows, inflation risks linger, and markets remain volatile but contained.

-

Bull case

Supply channels stabilize — including incremental output and rerouting — allowing oil prices to moderate. Growth concerns ease and sentiment improves.

-

Bear case

Disruption persists and oil remains well above $100 for an extended period. The resulting energy shock leads to a more significant global slowdown, with Asia particularly exposed given its reliance on Hormuz flows. Inflation pressures intensify, limiting policy flexibility and weighing further on markets.

Regional watchpoints

-

North America: Estimated 0.5 percentage-point growth drag at current oil levels.

-

EMEA: Sensitive to both crude oil and natural gas disruptions from the Middle East with sustained inflation pressure and external demand effects weighing on the outlook.

- APAC: Most exposed given concentration of energy flows through the Strait of Hormuz.

Manager perspectives

As of March 6, we surveyed managers through the initial week of the conflict. Across 30 manager research reports, the prevailing view remains that disruption is likely to be contained, though risks have risen alongside oil prices.

Managers consistently emphasize the importance of the duration of energy disruption, Asia’s exposure to Hormuz flows and the constraint on central banks given renewed inflation risks. While caution has increased, managers do not characterize current conditions as panicked.

Chart 1: Scenarios

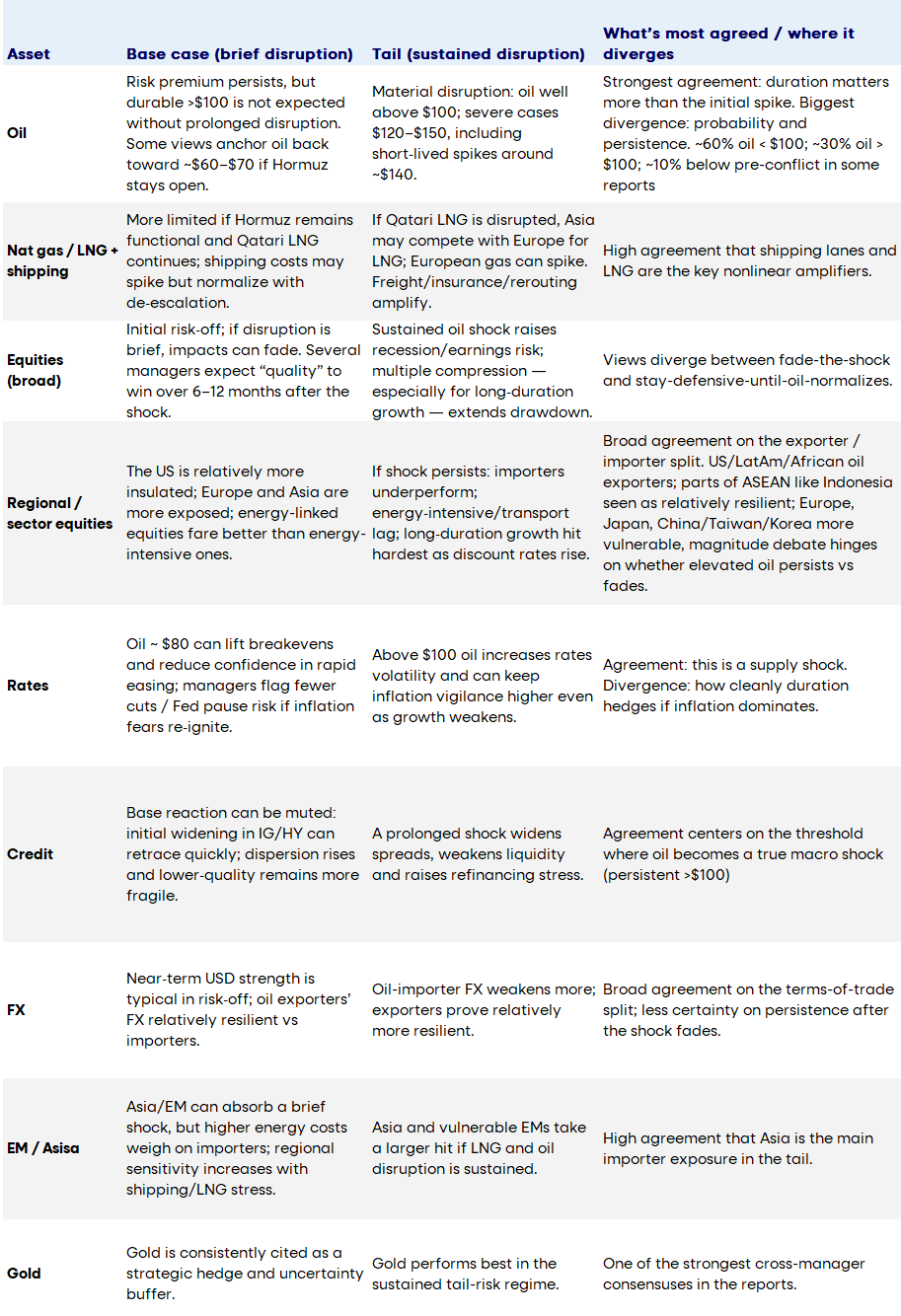

Chart 2: Investment implications by asset class (base vs. tail)

![]()

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important information pertaining to the hypothetical example: Past performance does not predict future returns. Return level is proportionately scaled in line with cash level to be overlaid. Source: Russell Investments. Assumptions: Average cash level 1.0%, 10-year history from 12/31/2023, gross of fees. Opportunity cost from not securitizing cash varies by asset allocation and time period, and is represented by horizontal bars as marked within the chart legend. Target asset allocation used: 0% cash, 74% MSCI World, 26% Global Aggregate (GBP Hedged). For illustrative purposes only. Does not represent any actual investment. Indexes are unmanaged and cannot be invested in directly. Performance benefit (net) of overlaying cash by last 5 individual calendar year is as follows: 2023:20 bps, 2022:-17bps, 2021:16bps, 2020:14bps, 2019:23bps.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Diversification and strategic asset allocation do not assure a profit or guarantee against loss in declining markets.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The Russell Investments logo is a trademark and service mark of Russell Investments

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2026. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All