The Fed’s new economic projections are fraught with even more uncertainty

The Middle East conflict is unlikely to derail growth in a meaningful way

Soft jobs and soon‑to‑be hot inflation put the Fed in a difficult position

March came in like a lion, but will it go out like a lamb? That’s the question facing investors as markets contend with rising risks. The conflict in the Middle East, surging oil prices with gasoline prices up to $3.63 per gallon, and February’s continued trend of weaker than expected jobs reports have revived stagflation-like concerns just ahead of the Fed’s March 17-18 meeting.

While the Fed funds rate is widely expected to remain at 3.50% to 3.75%, geopolitical uncertainty and renewed tariff impacts following last month’s Supreme Court International Emergency Economic Powers Act ruling complicate the outlook. The Fed’s updated economic projections and dot plot, which illustrate the potential path and dispersion of interest rates over the foreseeable future, should give insights into how policymakers are balancing these forces and whether recent volatility gives way to calmer markets in the weeks ahead. Below, we outline what to watch at next week’s Fed meeting.

A Fed pause is all but certain, but the message will matter more

The Fed’s usual playbook is to “look through” oil shocks, but the post‑COVID lesson that inflation wasn’t as transitory as expected still looms large. That caution showed up in the January meeting minutes, where several Federal Open Market Committee (FOMC) members suggested rate hikes could be on the table if inflation fails to return to the 2% target. Against that backdrop, fresh geopolitical risks and their inflationary potential are arriving at a particularly inopportune time given this hawkish shift.

New economic projections face elevated uncertainty

The Federal Reserve is navigating another tricky stretch, with incoming data pulling its dual mandate – price stability and full employment – in different directions. Adding to the challenge, the war in the Middle East and lingering tariff uncertainty have made the macro outlook even murkier than usual. We expect the Fed’s March statement to acknowledge this heightened uncertainty, echoing language used in March 2022 after Russia’s invasion of Ukraine, a theme Chair Powell is likely to reinforce in his press conference. Even so, the Fed’s updated projections should remain broadly in line with the December 2025 outlook with only modest adjustments at the margin.

The war is unlikely to derail US growth

Heading into the conflict, the US economy was on solid footing supported by fiscal tailwinds, strong household balance sheets and continued momentum in AI‑related capital spending. While the Middle East conflict represents the most significant geopolitical oil shock since the 1970s – with the potential to disrupt growth – the US enters this period from a position of relative strength.

First, the US is a net energy exporter, producing more energy than it consumes, which reduces vulnerability to global supply shocks. Second, the economy is far more energy efficient today, using less oil per unit of GDP than in prior decades. Finally, the US and its allies hold ample strategic petroleum reserves to cushion temporary supply disruptions.

With our base case assuming a short‑lived conflict measured in weeks rather than months, we don’t expect lasting economic damage. As a result, we maintain our 2.4% GDP forecast for 2026 and expect the Fed to keep its current 2.3% growth estimate broadly unchanged.

The Fed’s dilemma: soft jobs, soon-to-be hot inflation

After three rate cuts late last year, Fed officials had begun to coalesce around the view that the labor market was stabilizing, supporting a wait‑and‑see approach. February’s disappointing jobs report, however, puts that narrative to the test. While a healthcare strike and bad weather likely distorted the data, the 92,000 decline – the fifth contraction in nine months – along with a rise in unemployment to 4.4%, highlights lingering fragility and suggests additional support may be needed.

At the same time, inflation risks are building. The war in the Middle East and a renewed surge in oil prices, now back near $100 per barrel despite a record 172 million barrels expected oil storage release, could push prices higher. Any renewed acceleration would come at a difficult moment, as inflation, which had been easing, remains uncomfortably above the Fed’s 2% target for a fifth straight year. While policymakers typically look through geopolitical shocks, the Fed’s updated projections may show modest upward revisions to its 2026 unemployment and core PCE inflation forecasts, last set at 4.4% and 2.5% in December.

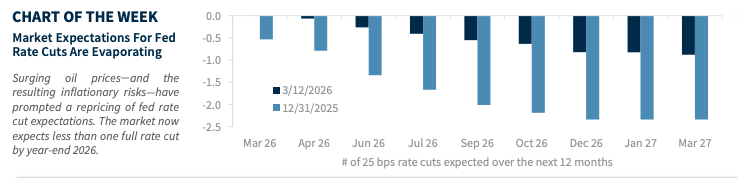

Fed rate cut delayed, not derailed

The Fed is facing a tough set of trade‑offs. Even a temporary rise in inflation makes near‑term rate cuts less likely, pointing instead to a longer pause. Markets have increasingly embraced that view, with expectations for a full quarter-point rate cut in 2026 getting pushed further out amid fears of a prolonged conflict. While we expect military action to ease in the coming weeks and do not anticipate lasting disruptions in the Strait of Hormuz, policymakers are unlikely to signal meaningful changes to their 2026 outlook until there is greater clarity on the conflict’s duration and how the data evolves.

Although dispersion in the dots may widen as views diverge across the FOMC, we do not expect material shifts in the median path. The dots should continue to point to one rate cut in 2026, another in 2027, and a long‑run neutral rate near 3.0%. Chair Powell’s press conference will also be important, with markets looking for reassurance and a steady hand.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.