An underappreciated theme shaping this year’s China story is energy resilience amid rising geopolitical risk. As conflict around Iran and the Strait of Hormuz roils oil markets, Beijing’s multi-layered energy security strategy is drawing attention for its potential to cushion vulnerability through stockpiling, diversification and strategic infrastructure.

For more than two decades, China has expanded its strategic petroleum reserves and built storage capacity as part of a hedge against supply disruption. While the country remains the world’s largest net crude importer and is exposed to sustained price spikes, its diversified sourcing and overland corridors reduce reliance on any single maritime chokepoint. These measures do not eliminate oil risk, but they may help contain spillover into China’s broader economy.

Compared with several major energy-importing economies, China is in a somewhat less precarious position. Japan relies on imports for roughly 85% to 90% of its primary energy, and the European Union imports more than half of its energy needs. India, meanwhile, imports the vast majority of its crude oil.1 While countries such as Japan also maintain sizable strategic petroleum reserves, reserves alone do not change underlying import dependence or energy mix. China remains heavily reliant on imported oil but generates most of its electricity from abundant domestic coal and has spent years building and securing diversified supply routes—moderating broader energy vulnerability even if it is not fully insulated.

That relative insulation has been visible in markets. Within the first 11 trading days following the late-February escalation of the Iran conflict, Asian equity markets diverged. While Asia’s other major markets—India, Japan, Taiwan and South Korea—declined about 6.0% to 15%, China’s broad market was roughly flat in US dollar terms—experiencing the smallest pullback among the group.2 In our view, part of the sharper declines in markets such as Taiwan and South Korea may also reflect profit-taking after strong gains last year.

Energy resilience alone is not an investment thesis. But it reduces one dimension of macro risk in a volatile global environment. Policymakers have simultaneously signaled realism on growth. China’s 2026 gross domestic product (GDP) target of 4.5% to 5% is the lowest in decades. Even so, it remains well above growth expected across most advanced economies, where forecasts generally cluster around 1%–2%.3 The modest target reduces the risk of abrupt tightening and allows Beijing to pursue structural reforms while maintaining targeted support for priority sectors.

Slower headline growth does not automatically imply weak equity returns. If growth composition improves—toward higher-value manufacturing, technology and domestic consumption—equity markets can respond positively even in a lower-growth regime.

Support for stabilization

China’s headline Consumer Price Index rose 0.8% year-over-year in December, with full-year inflation flat versus 2024. China’s Spring Festival data also showed resilience. Average daily travelers rose 8.7% year-over-year, retail sales in major regions increased meaningfully, and February production largely sustained January’s pace.4

Externally, China’s trade data underscores adaptability. Goods exports grew in the mid-single digits in 2025 despite elevated US tariffs, and China saw a record trade surplus of roughly US$1.2 trillion, supported by stronger flows to southeast Asia, Europe and emerging markets.5 The extension of tariff suspensions through late 2026 reduces near-term escalation risk, while dialogue around critical supply chains such as rare earths suggests a more pragmatic tone.

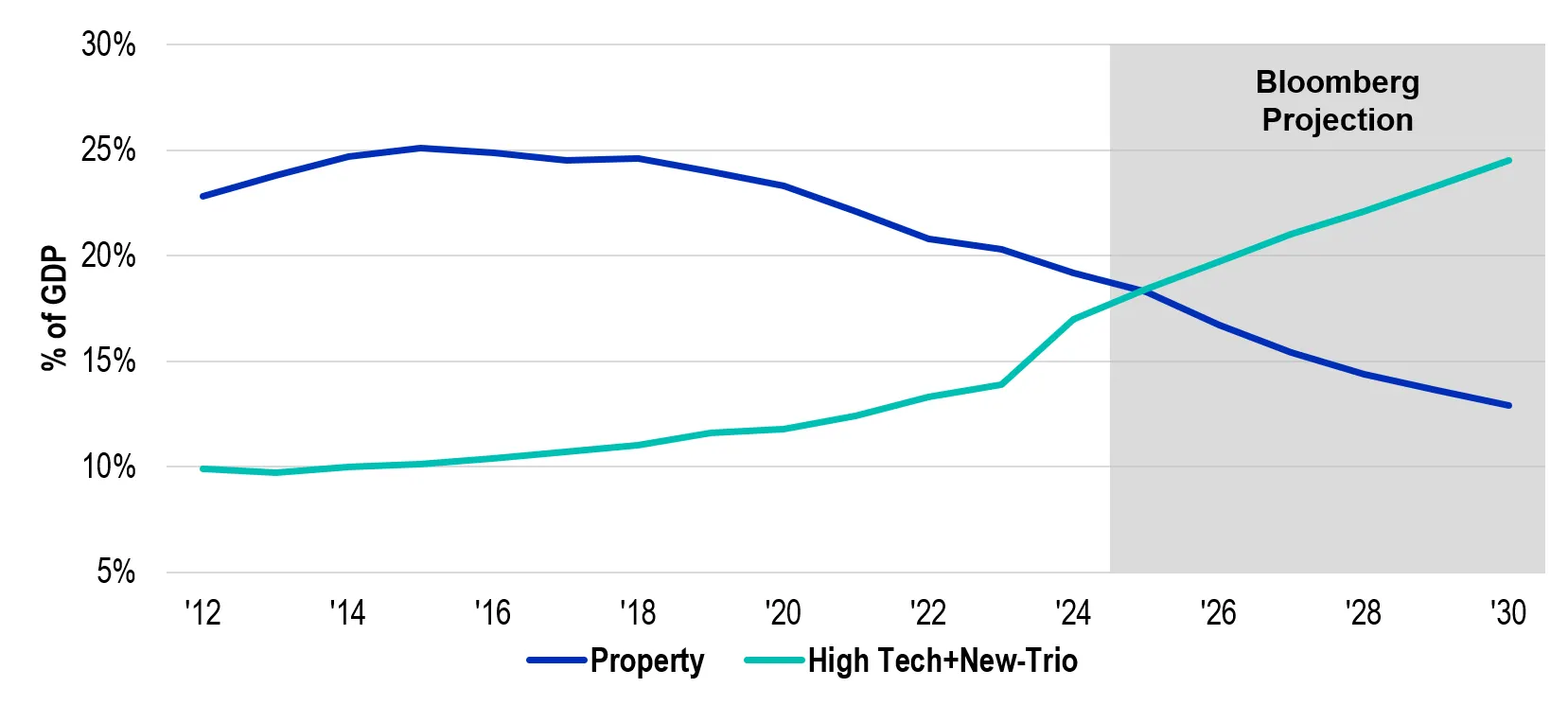

Structurally, the economy is shifting. High-tech and green industries (dubbed the “new trio” of electric vehicles (EVs), lithium-ion batteries and solar products) are projected to account for roughly 20% of GDP in 2026 and could rise further by 2030, while property’s share continues to decline.6

Tech and Green Industries Are Overtaking Property

2012 to 2030

Source: Bloomberg. There is no assurance that any estimate, forecast or projection will be realized. China's "new trio" driving economic growth consists of EVs, lithium-ion batteries and solar products.

Power shift

Index composition reflects this transition: China’s broad equity benchmarks are increasingly weighted toward artificial intelligence (AI) supply chains, advanced manufacturing, EV batteries and solar and communications equipment rather than property leverage. The country’s leadership across renewable energy continues to deepen, supported by sustained policy backing at the highest levels.

Notably, China leads global solar and wind deployment and dominates key segments of the EV supply chain. Its outbound investment in green power abroad—spanning renewable generation, grid infrastructure and clean technology manufacturing—also reached approximately US$80 billion through November last year, following roughly US$100 billion over the prior two years combined.7 That overseas capital deployment reinforces China’s position in global supply chains while extending its strategic reach. China is not only scaling its own transition but also financing and building clean energy capacity across markets such as Africa, Australia and Southeast Asia.

At the same time, the country possesses some of the world’s largest coal reserves and remains the largest producer and consumer globally, with coal still accounting for more than half of primary energy use. While renewables are expanding rapidly, coal continues to serve as a reliability anchor for the power grid.

China also holds a commanding role in critical minerals processing, including lithium, rare earths and other battery inputs. That industrial strength stands in contrast to equity valuations that remain compressed. The FTSE China RIC Capped Index trades near 12x forward earnings (2026 estimate), below its longer-term average and at a discount to developed market peers.8 Historically, China’s forward multiples have been closer to the mid-teens when growth and policy conditions were less strained. We believe current valuations reflect caution, which creates asymmetric risk-reward if earnings stabilize and policy remains supportive.

Key challenges remain clear. The property sector is still in transition. Deflation pressures persist. Stimulus has been targeted rather than aggressive. Growth is moderating compared to prior cycles. And geopolitical tensions may re-escalate.

But markets often reprice before macro clarity is fully visible. China in 2026 may not be a cyclical boom story. It may instead be a case of discounted valuations, structural rebalancing, policy flexibility and relative resilience in a volatile global backdrop. For global investors navigating the current market uncertainty and risk-off sentiment, we believe that combination warrants attention—and perhaps, a measured increase in allocation.

Endnotes

1. Sources: EIA: U.S. Energy Information Administration. “How Robust is China’s Energy Security?” CSIS: ChinaPower.

2. Source: Bloomberg. As of March 16, 2026. The FTSE RIC Capped Index represents the performance of the respective country’s large- and mid-capitalization stocks. Securities are weighted based on their free float-adjusted market capitalization and reviewed semi-annually. Net tax indexes are total return performance benchmarks that deduct withholding taxes from dividends. Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

3. Source: “Global Economy Watch – Projections.” PWC. February 2026.

4. Source: “Consumer Price Index in December 2025.” National Bureau of Statistics of China press release.

5. Source: “China Trade Surplus Beats Estimates.” Trading Economics. March 9, 2026.

6. Source: Bloomberg.

7. Source: Climate Energy Finance analysis, Bloomberg.

8. Source: Bloomberg, as of March 11, 2026.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

ETFs trade like stocks, fluctuate in market value and may trade at prices above or below their net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically. The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

WF: 9384944

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton

Read more commentaries by Franklin Templeton