You want your clients’ families to one day become your clients as well, but 80% of heirs leave their families’ advisors.1

An opportunity too big to pass up

It can be a complex challenge to establish relationships with client family members. However, it’s a challenge that isn’t just about client retention but growth. Millennials and Gen-X are expected to inherit $73 trillion between 2021 and 2045 and $16 trillion of that could be within the next decade.2

Here’s the good news: Many heirs can be open to meeting with advisors. One study showed that 87%3 of heirs plan to meet an advisor when they inherit. The same research showed that the openness to meet with an advisor is over 50% if the heir has a relationship with the advisor as an adult, but it’s much higher if the relationship is established first as a teen.4 At minimum, experts say to be sure to engage with family members at least five years before a possible wealth transfer.

Regardless of when you start, you need to know your audience if you want them to be your clients one day. Watch Ocean Park Asset Management’s webcast, “Building the Whole Family Relationship,” to learn about practical steps you can take to help establish your advisor role with your clients’ heirs. To start, let’s share some highlights from the webcast.

Steps you can take

Engaging with client family members may seem tricky, but it can start with simple questions to the client first. In fact, asking your client about the personalities and desires of their loved ones may be a way of deepening your understanding of your client’s financial needs.

Of course, there is the basic challenge of arranging to meet with client family members. There are several opportunities that you may have, and considerations that go along with them.

-

Financial Literacy:

Give your client’s children, regardless of their age, personal finance literacy.

o You can hold financial literacy seminars for your clients’ children, tailored to their age. This can build trust and increase engagement once they understand how financial moves like investing their inheritance can benefit them.

o You can offer to meet with your clients’ children to create simple but personalized financial plans for them.

-

Estate Planning:

If an estate plan is not communicated to heirs ahead of time, it can create family conflict. Emphasize to your client that among the most important gifts they can leave their loved ones is the gift of peace of mind, and a family discussion on the estate plan could help. Advisors can attend as objective intermediaries that explain the technical details of the estate plan.

-

Charitable Giving:

Your client may want to ensure their philanthropic legacy continues. This is a perfect opportunity to meet with family members to explain how approaches like donor-advised funds and qualified charitable distributions work.

-

Don’t overlook the spouse:

Prioritize meeting your client’s spouse, if you haven’t already. They’re typically the primary beneficiaries.

-

Know the generations:

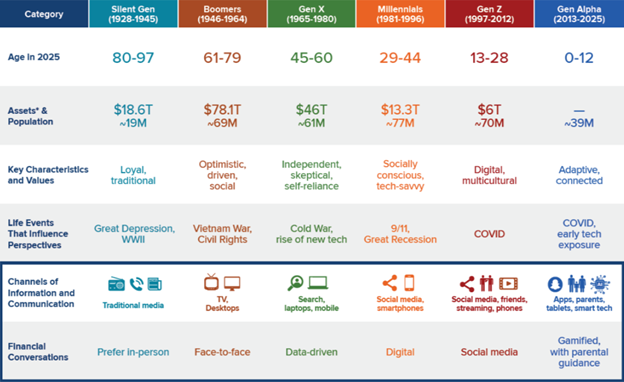

Each generation may view the value and role of a financial advisor differently. Gen X may prefer an in-person relationship with financial advisors. Millennials may take a more do-it-yourself approach through robo-advisors, so the value of a personal financial advisor needs to be proven. Gen Z may rely more on social media for financial advice and could respond to a social media presence. (See the chart below to learn more.)

Again, those are just some highlights from Ocean Park’s webcast, “Building the Whole Family Relationship,” which was presented with Bill Cates, host of the Top Advisor Podcast. To find out more, watch the replay.

Originally posted on Orion on February 17.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

1 Cerulli Associates, 2025 survey of investors with at least $250,000 in assets

2 Federal Reserve (2023), Cerulli Associates’ report, “U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2021: Evolving Wealth Demographics”

3 Nuveen Wealth Inheritor Research Study, 2023

4 Nuveen Wealth Inheritor Research Study, 2022

THESE DISCLOSURES CONTAIN IMPORTANT INFORMATION AND SHOULD BE REVIEWED CAREFULLY.

IMPORTANT DISCLOSURES

This information is for educational purposes and is not intended to provide, and should not be relied upon for, accounting, legal, tax, insurance, or investment advice. This does not constitute an off er to provide any services, nor a solicitation to purchase securities. The contents are not intended to be advice tailored to any particular person or situation. We believe the information provided is accurate and reliable, but do not warrant it as to completeness or accuracy. This information may include opinions or forecasts, including investment strategies and economic and market conditions; however, there is no guarantee that such opinions or forecasts will prove to be correct, and they also may change without notice.

Advisory services are offered through Ocean Park Asset Management, LLC, a registered investment adviser (“RIA”) regulated by the U.S. Securities and Exchange Commission (“SEC”). The advisory services are only

offered in jurisdictions where the RIA is appropriately registered. The use of the term “registered” does not imply any particular level of skill or training and does not imply any approval by the SEC. For information pertaining to the registration status of Ocean Park Asset Management, LLC, please call 1-844-727-1813 or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

This blog is sponsored by Ocean Park Asset Management. Orion Advisor Solutions, Inc. (“Orion”) or its affiliates and subsidiaries received compensation from Ocean Park Asset Management for the placement of this advertisement content. Ocean Park Asset Management and Orion are not affiliated companies, and the advertisement is not a recommendation or endorsement by Orion for any of the services referenced or provided.

This website may contain links to third-party websites. Any links to such third-party websites are provided solely as a convenience to you and not as an endorsement by Orion of the content on such third-party websites, or any affiliation or association with its operators. Orion is not responsible for the content of linked third-party websites, including, without limitation, any link contained in a linked website, or any changes or updates to a linked website, and do not make any representations regarding the information, services, products or accuracy of any material contained on such third-party websites.

This material does not constitute any representation as to the suitability or opportunities of any security, financial product or instrument. There is no guarantee that investment in any program or strategy discussed herein will be profitable or will not incur loss. This information is prepared for general information only. Individual client accounts may vary. It does not have regard to specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report (information). Investors should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed and should understand that statements regarding future prospects may not be realized. Investors should note that security values may fluctuate, and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not a guide to future performance. Investing in any security involves certain non-diversifiable risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any specific, or diversifiable, risk associated with particular investment styles or strategies.

Wealth management services provided by Orion Portfolio Solutions, LLC (“OPS”), a registered investment advisor. Orion OCIO services provided by TownSquare Capital, LLC (“TSC”), a registered investment advisor. OPS and TSC are affiliates and wholly owned subsidiaries of Orion Advisor Solutions, Inc.

Information presented herein with respect to any third-party service provider has been provided by those third-party service providers and has been reproduced here with their permission. Such information does not necessarily reflect the views and opinions of Orion Advisor Solutions, Inc. (“Orion”) or its affiliated companies. Orion does not endorse any particular third-party product or service. Our clients should undertake their own assessments to determine whether these parties meet their business and due diligence requirements. Ocean Park Asset Management and Orion Portfolio Solutions, LLC (“OPS”) are not affiliated companies, and the blog is not a recommendation or endorsement by OPS for any of the services referenced or provided. While some OPS solutions may contain one or more of the specific strategies mentioned, OPS is not making any comment as to the suitability of these, or any investment product for use in any portfolio.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by Orion