The artificial intelligence (AI) trade that has dominated equity markets in recent years is showing signs of fragility. As investors reexamine the scale of the AI infrastructure build-out and optimistic assumptions around AI adoption, a group of “old-economy” sectors is quietly reasserting itself.

While the effect of the Iran war has taken center stage in markets for now, the trajectory of high-profile technology stocks will likely remain a prominent long-term theme for equity investors over time. But what does that mean for under-the-radar, old-economy stocks in less glamorous sectors like consumer staples, healthcare and energy? Many companies in these sectors have been chugging along steadily for years, generating strong profits, plenty of cash and attractive dividend yields.

Unfortunately, sound fundamentals don’t always translate into share-price gains. Even when companies beat estimates or adjust guidance upward, investor psychology can win the day. As a result, many old-economy stocks have seen little to no multiple expansion over the past few years despite strong earnings growth.

Cracks Begin to Show in Market Concentration

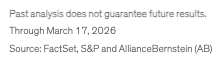

This trend is perhaps most evident in the constitution of major US equity indices. With investors funneling assets into the technology titans, the broader US market has become highly concentrated. As recently as the third quarter of 2025, the eight largest US stocks accounted for nearly 42% of the S&P 500’s market capitalization (Display), mostly driven by AI-related stocks in the information technology, communication services and consumer discretionary sectors. That means just 1% of the S&P’s constituents hold disproportionate sway over the markets.

Is that dynamic changing? By mid-March, the market cap of the top eight stocks had retreated to just under 38%—still elevated by historical standards, but a meaningful shift in a more equitable direction. While similar rotations in recent years quickly faded, we believe new circumstances could provide staying power for a broader market this time.

AI Buildout Is Changing Technology Firm Structures

The ongoing AI buildout is slowly changing what it means to be a technology company. Hyperscalers—large cloud-service and technology infrastructure providers—are expending enormous amounts of cash to build AI infrastructure such as data centers, power grids and computing resources. These giant firms have tapped the public bond markets and private credit for some of their capital needs, but many are also funding the buildout from their own cash reserves. This is putting a damper on the free cash flows of technology companies, while transforming them from traditionally asset-light entities into firms with significant assets on their balance sheets. And despite the heavy investment, there’s no guarantee that these AI assets will pay off—particularly given optimistic assumptions around AI adoption.

To be sure, some of the megacaps have robust business models and earnings prospects. However, the enormous amount of capital going into AI could also create more competition in the core businesses of technology companies.

And it’s not just the megacaps at risk.

The proliferation of AI threatens to disrupt software companies and other digital businesses of all sizes. Investor concerns are reflected in whipsaw market reactions to even minor revisions to earnings guidance—a sea change for an industry that has largely enjoyed positive investor sentiment.

Return of the Dinosaurs?

As tech shares struggle, investors are showing a new appreciation for companies with high free-cash conversion and greater resistance to the volatile AI trade. Although many have strong business models and recurring revenue streams, their valuations have been dormant for years because they haven’t grown as fast as the big tech companies that have sucked all the oxygen out of the room.

Perhaps we’re on the cusp of a “revenge of the dinosaurs trade,” as a Goldman Sachs analyst cleverly quipped in a recent research note.

In a new environment where pterodactyls could potentially trump terabytes, top-line growth may eventually become less important than competitive moats. Typically, moats imply barriers to entry. But increasingly, moats could also represent barriers to AI-linked disruption—including threats to core business models. Over time, this layer of insulation could offer lasting competitive advantages. By generating high free cash flow and modest but sustainable growth, old-guard companies could see continued multiple expansion if their moats hold. Those with entrenched brands and massive global reach may reap even more durable benefits.

AI can also help old-economy companies thrive. Some may even bolster their competitive moats via productivity enhancements from AI and new revenue from the AI buildout itself. Think industrials, energy, materials and financials. As we see it, the capex boom could be a boon for previously unloved companies in these sectors.

Old-Economy Valuations Remain Compelling

After years of compressed multiples, the equity market’s wide valuation dispersion may be starting to narrow. Recently, select names in the consumer staples, materials and energy sectors have seen renewed momentum (Display), although old-economy valuations remain attractive for the most part. Moreover, these firms have historically performed well in weaker economic conditions, which could make them more resilient as geopolitical upheaval triggers a spike in oil prices and threatens to upend the global economy.

The AI revolution will play out in fits and starts as the markets reassess winners, losers and timelines. As that process unfolds, we think underappreciated companies with durable cash flows and strong moats will be prized. For diversified investors, that opens a path to returns beyond big tech in overlooked businesses that can benefit from AI and withstand its disruption.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein