Muni Monthly: February 2026

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThis month’s Muni Monthly covers performance, supply and demand technicals, fundamentals and valuations for the month ending February 2026.

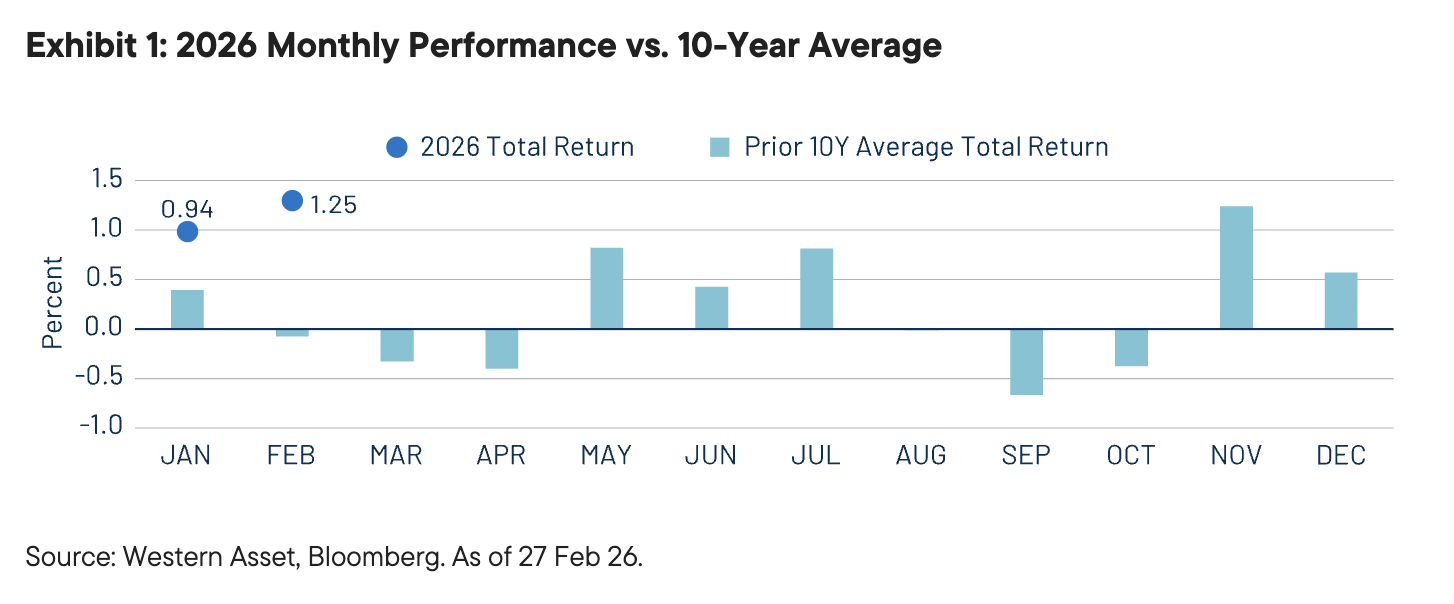

Performance Overview: Strong Municipal Performance in February Counters Recent Weakness

In February, market sentiment was shaped by escalating US-Iran geopolitical tensions and sector-specific selloffs driven by concerns about AI’s potential disruption to existing business models. Economic data presented a mixed picture, with January nonfarm payrolls increasing by 130,000 jobs, rebounding from December’s revised 48,000 gain, while the unemployment rate edged down to 4.3%. Inflation data for January eased from the prior month, with headline Consumer Price Index (CPI) falling to 2.4% year-over-year (YoY) from 2.7% and core CPI easing to 2.5% YoY from 2.6%. All told, Treasuries rallied across the curve, and the municipal yields followed suit but generally underperformed the risk-off sentiment. The Bloomberg Municipal Bond Index gained 1.25% leading year-to-date (YTD) returns higher to 2.20%. February’s strong performance counters recent weakness, with the index averaging negative returns in February, largely driven by softening demand ahead of tax season and limited new issuance.

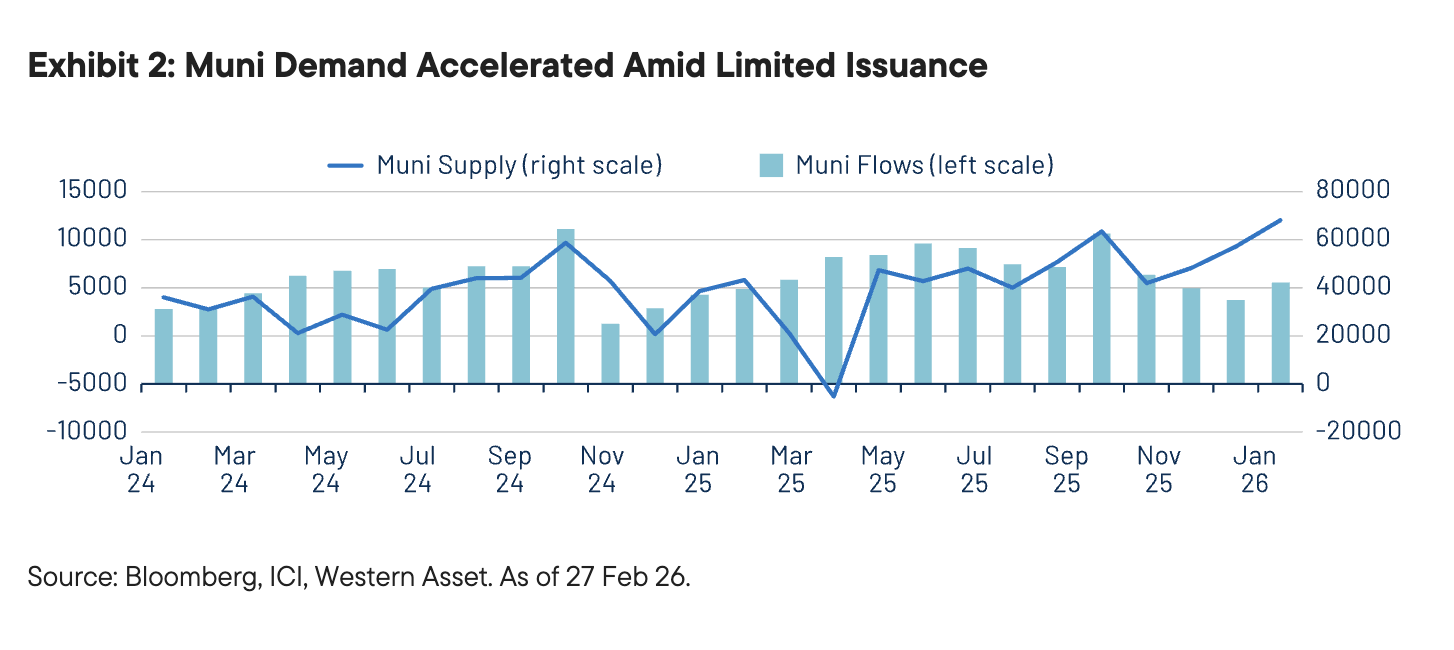

Technicals: Renewed Investor Demand Bolstered Muni Funds

The strong start of the year has been supported by renewed investor demand, as capital has moved decisively back into municipal mutual funds. Investors appear to show an increasing willingness to capitalize on relatively attractive municipal valuations during periods of elevated market volatility, particularly in longer maturities as the yield curve steepened. According to weekly and monthly Lipper and ICI data, municipal mutual funds and ETFs recorded over $10 billion of net inflows in February. Notably, Lipper estimates that approximately 86% of the $18 billion in YTD inflows has been concentrated in intermediate- and long-duration fund categories. Since January 2024, cumulative net inflows of over $126 billion on top of strong SMA demand have fully offset the $122 billion of net outflows experienced in 2022 and 2023.

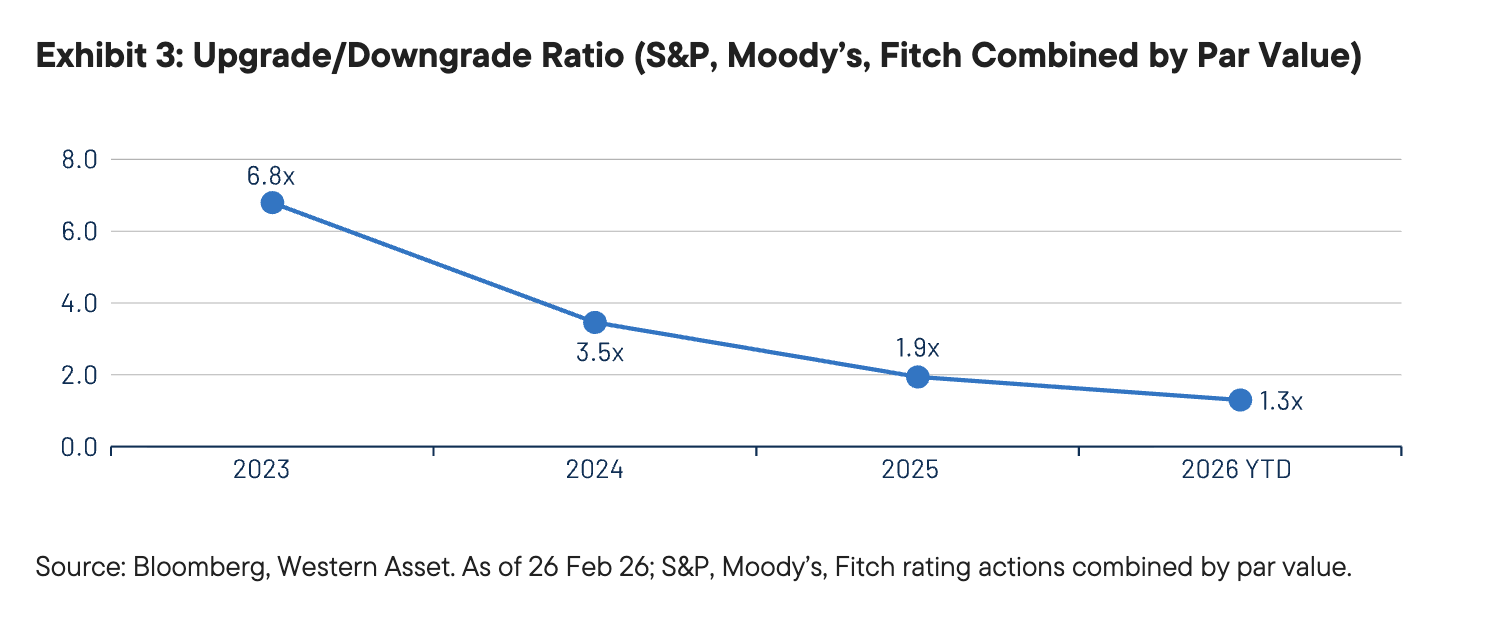

Fundamentals: Muni Fundamentals Remained Strong

Municipal fundamentals remained strong, supported by elevated tax collections. However, the pace of upgrades relative to downgrades has continued to moderate. Upgrades have outpaced downgrades YTD by a factor of 1.3x, compared to 3.5x in 2024 and 1.9x in 2025, according to Bloomberg. Notably, Fitch downgraded the city of Chicago during the month from A- to BBB+, while maintaining a negative outlook. Fitch cited consecutive operating deficits and a high reliance on one-time solutions as key drivers of the downgrade.

Valuations: Muni Valuation Disparities Create Tax-Efficient Opportunities for Active Managers

The strong YTD performance also represents a meaningful reversal of the underperformance the municipal market experienced in 2025, and muni supply and demand dynamics have shifted valuations in certain segments of the market. For example, AAA rated municipals maturing inside of 10 years now yield less than comparable Treasuries on an after-tax basis, assuming a 37% effective tax rate, largely attributable to high demand for SMA strategies concentrated in shorter maturities. In contrast, using the same tax rate, AAA municipals beyond 20 years offer more than 100 basis points of after-tax yield advantage relative to Treasuries. We believe these valuation disparities create opportunities for active managers to deliver tax-efficient outcomes.

Definitions:

“AAA” and “AA” (high credit quality) and “A” and “BBB” (medium credit quality) are considered investment grade. Credit ratings for bonds below these designations (“BB,” “B,” “CCC,” etc.) are considered low credit quality, and are commonly referred to as “junk bonds.”

One basis point (bps) is one one-hundredth of one percentage point (1/100% or 0.01%).

The Bloomberg Municipal “Muni” Bond Index covers the USD denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

The Bloomberg Municipal High Yield Bond Index is an unmanaged index made up of bonds that are non-investment grade, unrated, or rated below Ba1 by Moody’s Investors Service with a remaining maturity of at least one year.

The Bloomberg Taxable Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term taxable bond market. To be included in the index, bonds must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies if all three rate the bond: Moody’s, S&P, Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment-grade.

The Bloomberg US Corporate Bond Index measures the performance of the investment-grade, fixed-rate, taxable corporate bond market. It includes U.S. dollar-denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

The Bloomberg US Treasury Index measures the performance of US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with at least one year until final maturity. Treasuries, if held to maturity, offer a fixed rate of return and a fixed principal value; their interest payments and principal are guaranteed.

The Bloomberg Valuation Service (BVAL) provides prices on a daily basis for over 2.5 million securities across all asset classes.

The Bloomberg AAA BVAL Callable Municipal Credit Curve is represented by the US General Obligation AAA Muni BVAL Yield Curve. The BVAL curve is populated with pricing from uninsured AAA General Obligation bonds. The curve is populated with high quality US municipal bonds with an average rating of AAA from Moody’s and S&P. The yield curve is built using non-parametric fit of market data obtained from the Municipal Securities Rulemaking Board, new issues, and other proprietary contributed prices. The curve represents 5% couponing. The 3-month to 10-year points are bullet yields, and the 11-year to 30-year points are yields to worst for a 10-year call.

The yield curve shows the relationship between yields and maturity dates for a similar class of bonds.

Inverted yield curve refers to a market condition when yields for longer-maturity bonds have yields which are lower than shorter-maturity issues.

Yield to worst (YTW) is the lowest potential yield that can be received on a bond without the issuer actually defaulting.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Municipal income may be subject to state and local taxes. Some income may be subject to the federal alternative minimum tax for certain investors. Capital gains, if any, are taxable.

Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the US government. The US government guarantees the principal and interest payments on US Treasuries when the securities are held to maturity. Unlike US Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the US government. Even when the US government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

WF: 9435759

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All